Sorted Weekly Tweets

Market Impact

- Companies Squeeze 401K Plans From Facebook to JPMorgan http://t.co/2glTizHOjm This should not surprise, many companies shrink labor costs $$ Feb 15, 2014

- Wells Fargo edges back into subprime as US mortgage market thaws http://t.co/s8AJCKuzOH Isn’t a problem now, problem comes w/imitators $$ Feb 15, 2014

- Homebuyers Get Break as Loan Rates Defy Fed Tapering http://t.co/i7PdmGThdz Housing & general economy weakened, so mortgage rates fell $$ Feb 13, 2014

- Pension politics http://t.co/3NaaI61AxM @felixsalmon points out how defined benefit plans r in general better 4 workers. Mind the PBGC $$ Feb 13, 2014

- Colleges Raise Record $33.8B Exceeding US Peak in 2009 http://t.co/PRjlMrKM9i Donations always follow creation of unrealized cap gains $$ Feb 12, 2014

- Some Lines Say Maybe the Stock Market Will Go Down http://t.co/FdkJdRT9qe @matt_levine correctly criticizes the 1928-9 $SPY graph overlay $$ Feb 13, 2014

- 1929 Stock Market Crash Chart Is Garbage http://t.co/PyPIulerCH Unequal left & right scales make the relationship look tighter than it is $$ Feb 12, 2014

- ?When to Ignore the Investment Experts http://t.co/K2vyHgb1gv ?When all the experts &forecasts agree ? something else is going 2 happen.? $$ Feb 11, 2014

- Comparing Economic Recoveries http://t.co/5za6QtEFKD In 1984-2006, growth was borrowed from future by increasing debt levels-> #payback $$ Feb 11, 2014

- Aluminum Lines Still Trouble the London Metal Exchange http://t.co/f5OyWC5EHC Aluminum inventories will b a prob, til short intrates rise $$ Feb 11, 2014

- Top Anecdotal Signs of a Market Bubble http://t.co/MavPhxB6vZ Good piece, like one of mine: http://t.co/bON7nJJFfk Watch the credit cycle $$ Feb 11, 2014

- Ten Stocks to Own During a Market Correction http://t.co/RzBdaNf1ff Good list. I own a few of them. $$ Feb 11, 2014

- Does trend-chasing explain financial markets? http://t.co/3Mkg4R99dx Partly. Difference between investment IRR and total return is big $$ Feb 10, 2014

- ?Security. Safety. Stability.? http://t.co/VfKVcGgMRJ from @reformedbroker Gold is useful at certain points, but only when it is hated $$ Feb 10, 2014

- Flows Don?t Follow Value, They Follow Performance http://t.co/9oIJ4M7HMo @reformedbroker wrote this little gem. Learn & internalize it $$ Feb 10, 2014

- Long Term Charts 2: Western Markets Since The Middle Ages http://t.co/lsBfIot8pi Interesting charts from very messy data at Zero Hedge $$ Feb 10, 2014

- Most Expensive Place to Find Out Who You Are http://t.co/szQfeKFZxT @jasonzweigwsj : Your reaction 2 minor crisis shows yr risk tolerance $$ Feb 10, 2014

?

Companies & Industries

- AIG Takes $832 Million Charge on Death Bets as Hedge Funds Gain http://t.co/JmI7hBy9MH Life settlements should b illegal $$ $MET $AIG $PRU Feb 14, 2014

- To Stop the Coffee Apocalypse, Starbucks Buys a Farm http://t.co/CPkyVAUnsR $SBUX helps create a variety of rust resistant Arabica trees $$ Feb 13, 2014

- Former BlackRock Manager Finds Billions on Rice Energy http://t.co/aBPTo3u4Ky Few investment mgrs have operating talent; Daniel Rice does $$ Feb 13, 2014

- Buffett’s Pal Munger Heads a Very Weird Company http://t.co/ztr3XizpKM Growth of $DJCO thru investing leads 2 # of growing pains & 13F $$ Feb 13, 2014

- Here?s Why the Biggest Cable Company in the Country Thinks It Can Get Bigger http://t.co/04cdg1J9VP Feds tolerant of cable re antitrust $$ Feb 13, 2014

- Why AOL ended up spending millions on ‘distressed babies’ http://t.co/d2lWs8eJit $AOL chose 2b in healthcare biz 4 its employees & lost $$ Feb 13, 2014

- 3 High-Yielders To Buy On The Pullback http://t.co/8SUBI1M0ut In total $SNH issues more stock than it pays in divs. Divs -> cap losses $$ Feb 13, 2014

- Who is John Thompson? A look at Microsoft’s new chairman http://t.co/W7SrXqxtwm May have right stuff to protect new CEO from meddling $$ Feb 10, 2014

US Politics & Policy

- Runaway Drones Map Land, Film ‘Wolf,’ Knock Down People, FAA Gives Chase http://t.co/rcTnjug8w1 Drones r here 2 stay; time license them $$ Feb 15, 2014

- Teacher Tenure Put to the Test in California Lawsuit http://t.co/XP5fx6HpR3 Tenure has outlived its usefulness; older teachers can b lazy $$ Feb 15, 2014

- Lincoln’s Foreign Policy in Today’s World http://t.co/t2RELj7uRB Kept England & France from joining Civil War; otherwise pragmatic $$ $SPY Feb 15, 2014

- What Would Lincoln Do? http://t.co/hi6n4Rb8hl A clever man w/principles, who did not cease to be pragmatic pursuing 1 main goal – Union $$ Feb 15, 2014

- Harvard Professor Attacking Google Thrives as Web Sheriff http://t.co/g1W7KXH94K At some point, lack of disclosure will blow up on him $$ Feb 14, 2014

- The $2.2B Bird-Scorching Solar Project http://t.co/hIYWhJpUwQ Get used 2 idea: almost every form of energy imposes environmental costs $$ Feb 13, 2014

- Obamacare Damage-Control Teams Seek to Calm Complaints http://t.co/bPU95rVMxM Things r tough when u r trying to avoid media embarrassment $$ Feb 13, 2014

- Billionaire Musk Gets Brownsville to Pay for SpaceX http://t.co/eoAiygs9mq Like a football owner bargaining 2 get taxpayers buy a stadium $$ Feb 13, 2014

- Snowden Swiped Password From NSA Coworker http://t.co/1mJ5D6vGH3 & it cost him his job. Snowden denies it; NSA is Not Saying Anything $$ Feb 13, 2014

- Puerto Rico Legislators Amend Bill Calling for Bank-Deposit Shift http://t.co/fMaCvMi7ab Provincial govt’s attempt 2raid cookie jar stopd $$ Feb 13, 2014

- Obamacare Will, in Fact, Encourage Employers to Cut Jobs http://t.co/D3vaCFHOZY As the employer mandate comes into force, jobs will b cut $$ Feb 12, 2014

- Tea Party Scorns Republicans as House Lifts Debt Ceiling http://t.co/fPohsF6Kbi t-party can b “pure” as Dems raise ceiling w/few GOP $$ $TLT Feb 12, 2014

- A Lame Duckish Calm Falls Over the Capital http://t.co/u6bG2cg1nL Parties in DC act as if the next event is the November elections $$ $TLT Feb 12, 2014

- Obama Rewrites ObamaCare http://t.co/Ym3CtHt3pI Another day, another lawless exemption, once again for business; WSJ bangs populist drum $$ Feb 11, 2014

- The US Senate Again Insists on USPS Saturday Mail Delivery http://t.co/YnzmKE5Xrh 2 timid; end Wednesday & Saturday delivery $$ $UPS $FDX Feb 11, 2014

- US firms ?paid effective tax rate of 2.2% in 2011? http://t.co/f2T5Qnrhri More than a tax haven, Ireland helps insurers shave reserves $$ Feb 11, 2014

- No Honeymoon for Janet Yellen http://t.co/86QPfTcVE0 QE withdrawal will bite, & what will become of all the deposits? $$ Feb 11, 2014

- Please Hold Your Bernanke Applause http://t.co/DCKPttFHNU Remember, when Greenspan left, he was viewed as a success, same as BB now $$ $TLT Feb 11, 2014

- Sounding the Tax Alarm, to Little Applause http://t.co/r9JQmmaeLB IRS stiffs whistleblowers who often lose employability 4 being a tipper $$ Feb 10, 2014

Rest of the World

- Putin is Playing a Game of His Own http://t.co/19Arh0aJOH Not so fast. Russia has significant resources & influence in Eastern H’sphere $$ Feb 15, 2014

- Boy?s Life Hanging on 8-Hour Trip Shows Why Venezuelans Protest http://t.co/8G8CgGwGST Socialism is like a cancer that spreads til death $$ Feb 14, 2014

- Let’s Watch Venezuela Destroy Itself http://t.co/g1Uy3zk1W3 Logical extreme of Socialism falls apart; pity that Chavez never lived 2c it $$ Feb 14, 2014

- Chinese Join Winklevosses in L.A. Luxury Home Hedges http://t.co/TUdw4AItw8 Amazing what the wealthy will pay 4a fancy foreign retreat $$ Feb 14, 2014

- Next crisis won?t come from the emerging markets http://t.co/Jei7oKJ8BD Argues France, Germany, Britain, Australia & Canada-> 2 much debt $$ Feb 13, 2014

- Mister Donut, Pan Am and Friendster Found Alive and Well http://t.co/vDaGi33cEN Old brands never die, they just move overseas & make $$ $SPY Feb 13, 2014

- Bank of England points to 2015 rate rise, blurs guidance http://t.co/AWhyd8GZmd More precision than 1 can know; the world is messy $$ $FXB Feb 13, 2014

- Italy Pays Record Low to Sell 3-Year Debt at Auction http://t.co/PWmUhXufjb Let the leverage build for the next crisis $$ Feb 13, 2014

- Fink to Mobius Touting Emerging Stocks Fails to Stem Outflow http://t.co/8PFKbOH8Lg A time 2 nibble, not a time 2 gulp $$ $EEM Be wary Feb 13, 2014

- Greek Truckers Show Plight as Groceries Show Up Frozen http://t.co/XgAM737A7h Freeing up the labor market will work as attitudes change $$ Feb 13, 2014

- Tunisians Bolt Doors Even After New Constitution Passed http://t.co/lBhXz8iqWb Constitutions cannot create cultural change; asks 2 much $$ Feb 13, 2014

- Israel Desalination Shows California Not to Fear Drought http://t.co/BFidhnEF7S When resources r tight there are incentives 2 create tech $$ Feb 13, 2014

- London Walkie Talkie Owners to Shield Car-Melting Beam http://t.co/76TP0u2tuT Reflective parabolic curve of building melts cars @ a spot $$ Feb 12, 2014

- Rouhani Seeks Economic Fix as Iran Commemorates Revolution http://t.co/EDNL5WLOvB Will have to get the agreement of unelected true rulers $$ Feb 11, 2014

- Argentina to Replace Bogus Inflation Index to Mend IMF Ties http://t.co/iSzQizrgnF Argentina tries 2 find cheapest way out of this mess $$ Feb 11, 2014

- Who Should Pay for Trusts that Go Bust? http://t.co/aOXFbDltCZ If China is smart, protect depositors, but let banks & WMP holders fail $$ Feb 11, 2014

- Iceland Girds for Fight as Suit Targets Half $14B GDP http://t.co/hX6M12PZ48 Icelandic taxpayer will refuse the bill; UK will b stiffed $$ Feb 11, 2014

- Mobius Says Emerging-Market Rout Near End as Valuations Lure http://t.co/MMLjlAmN49 I dunno, a 4% earnings yield premium seems small $$ $EEM Feb 11, 2014

- Rehabilitating Portugal http://t.co/tFy3GnIwRQ Long; Argues that a Greek-style bailout should b done, or Portugal will eventually default $$ Feb 11, 2014

- Iranian TV Shows Rare Broadcast of Band Playing Music http://t.co/jTBFNcRsHJ Christianity has always been easier on music than Islam $$ Feb 11, 2014

Work Trends

- Sheep-Shearing Wells Fargo Banker Bridges US Income Gap http://t.co/utMe1ekmir Sells coffeemakers too; many in US work multiple jobs $$ $TLT Feb 13, 2014

- Workers Shed Caution, in a Healthy Sign for Labor Market http://t.co/zTq0NgbO0f When workers r willing 2 quit, labor mkt is healthy $$ $TLT Feb 11, 2014

Practical

- A Little Valentine’s Day Straight Talk http://stks.co/j0I6p Sage counsel 2 younger women if they want to get married: start early $$ Feb 15, 2014

- The Sex Question Readers Want Answered Most http://t.co/kRhYIgwI2Z Even Long-Married Happy Couples Ask, ‘How Can We Have Sex More Often?’ $$ Feb 11, 2014

- Ten Ways You’re Probably Leaving Money on the Table http://t.co/KkjetkJsp9 Simple list of ways to save money for avg upper-middle class $$ Feb 11, 2014

- Why Mom’s Time Is Different From Dad’s Time http://t.co/0Xr4IMsFfs Husbands, u can win if u reduce chaos for your overburdened wives $$ Feb 11, 2014

Other

- US Scores Fusion-Power Breakthrough http://t.co/h6wDtXHcVj Bad news is Tritium very expensive @ $100K per gram; takes much energy 2 make $$ Feb 13, 2014

- If Ocean Heat Pump Switches On, Expect to Feel It http://t.co/FlsYni5c62 Speculative; we don’t understand climate or hurricanes well $$ Feb 11, 2014

- Who is Steven Reisman? Meet Hip-Hop VIPs’ Favorite Lawyer, The Man With The $2 Bills http://t.co/B3v87YDWrt Weird. Very, very weird $$ $SPY Feb 11, 2014

- What Really Happened to Flappy Bird? http://t.co/3IiBxSIhYx Beware the success u wish 4? Also: http://t.co/ld6A2XaiKs Still a puzzle $$ $SPY Feb 11, 2014

Wrong, etc.

?

- Skeptical: Blackstone-Fueled Single-Family Home Boom Lifts Chicago http://t.co/sETcWifBGx In past hi levels of investor ownership bearish $$ Feb 15, 2014

- Wrong: Pros Panic, Retail Investors Stay Cool on Emerging Markets http://t.co/QXXpOcqKYw Too short a period time to judge $$ Feb 14, 2014

- Wrong: Social norms: The indignity of no work http://t.co/6isHJo9fkw New technologies will create new jobs & make the whole world better $$ Feb 13, 2014

- Wrong: Warren Buffett is laughing at you for selling http://t.co/S5LFS3jUk5 Poorly thought-out piece glues 2unrelated ideas together $$ $EEM Feb 13, 2014

- Wrong: The #1 High-Yield Investment Of America’s Elite http://t.co/FUVyBblQpZ Spammy article that talks about REITs as if they r a secret $$ Feb 11, 2014

?

Replies, Retweets & Comments

?

- 10 miles west of Baltimore, MD, we got ~15 inches of snow over the last last 2 days. #snow #weather #pax $$ Feb 14, 2014

- “I made this comment six months ago: http://t.co/a82j8TRxm1… & then, I tipped the SEC. ?” ? David_Merkel http://t.co/gthPe5eQoA $$ $DJCO Feb 13, 2014

- “Administrative Services Only” plus individual stop loss protection is in general the smart way2?” ? David_Merkel http://t.co/fPV6fQo1i1 $$ Feb 13, 2014

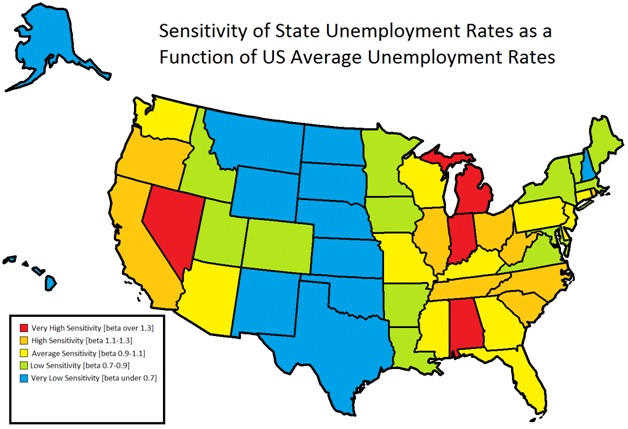

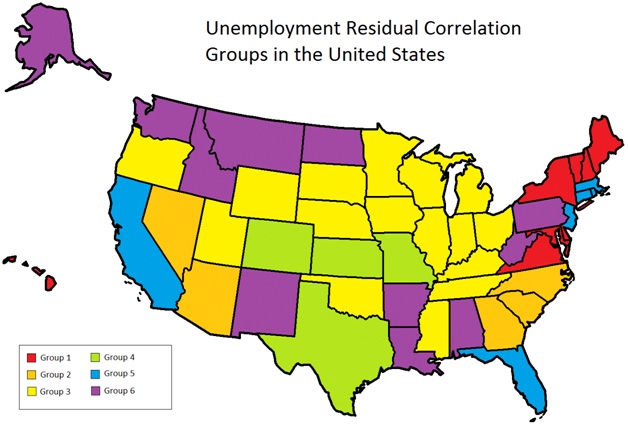

- “This is a common confusion in statistics — you can have a high correlation and a low beta. Second?” ? Merkel http://t.co/sa6PLqEhdU $$ Feb 13, 2014

- RT @Pawelmorski: Scary parallel my foot. http://t.co/omyovAKQaX Feb 12, 2014

- @davidgaffen that would only be a temporary fix. I wrote this 3.5 yrs ago on the topic: http://t.co/q3lbyELN9d The internet eats USPS Feb 11, 2014

- @quakkelaar I miss you too. If you are ever near Baltimore/DC, let me know; we can get together, brother. Last few years have been hard Feb 11, 2014

- RT @ReformedBroker: Please explain how the wording of this investment advertisement on the Washington Post site could be legal: http://t.co? Feb 10, 2014

- ‘ @quakkelaar Hail old friend. Yes, same old mistakes, b/c those wishing to retire are making the money sweat, until it rebels on them $$ Feb 09, 2014

?

Failure. We’ve all experienced it. Can we benefit from it?? The answer is maybe, depending on the costs of failure.

Failure. We’ve all experienced it. Can we benefit from it?? The answer is maybe, depending on the costs of failure.