?It ain?t what you don?t know that hurts you, it?s what you know that ain?t so.?

(Attributed to Mark Twain, Will Rogers,?Satchel Paige, Charles Farrar Browne,?Josh Billings,?and a number of others)

A lot of what passes for investment knowledge is history-dependent, and may not serve us well in the future. ?Further, a certain amount of it is misinterpreted, or, those writing about it, even really bright people, don’t understand the hidden assumptions that they are making. ?I’m going to clarify this by commenting on three graphs that I have seen recently — two that I think deceive, and one that I think is accurate. ?Let’s start with one of the two, which come from this article at AAII, interviewing Jeremy Siegel:

Leaving aside the difficulties with the data from 1802-1871, there is an implicit assumption of buying and holding that undergirds these statistics. ?Though the lines look really smooth now in hindsight, for those investing at the time they were often scared to death in bear markets, selling out at the worst possible time, and in bull markets, getting greedy at the worst possible time.

Now one might say to me, “But David, forget what happened to individuals. ?As a group, people must made returns like this, because every buyer has a seller — even if some panicked or got greedy, someone had to take the other side of the trade and benefit.” ?True enough, though I am suggesting that average people can’t live with that much volatility. ?Even if you cut 1929-32 in half by being 50/50 Stocks/Treasury Notes, how many people could live with a 40% downdraft without selling out?

But there is another problem: when does cash enter and exit the stock market? ?Hint: it doesn’t happen via secondary trading.

Cash Enters the Stock Market

- An Initial Public Offering [IPO], secondary IPO, or rights offering leads people to give money to a corporation in exchange for new shares.

- Employees forgo pay to receive company stock.

- Shares get issued to suppliers in lieu of cash (common with scammy promoted stocks)

- Warrants get exercised, and new shares are issued for the price of cash plus warrants.

Cash Exits the Stock Market

- Cash dividends get paid, and not reinvested in new shares

- Stock gets bought back for cash

- Companies get bought out either entirely or partially for cash.

I’m sure there are other ways that cash enters and exits the stock market, but you get the idea. ?It means that cash is exchanged with the company for shares, and vice versa, not the trading that goes on every day. ?Now, here’s the critical question: when do these things happen? ?Is it random?

Well, no. ?Like any other thing in investing, n one is out to do you a favor. ?New stock tends to be offered at a time when valuations are high, and companies tend to be taken private when valuations are low. ?Thus back in the tech bubble, 1998-2000, a lot of cash got soaked up into companies with dubious valuations and business models. ?With a few exceptions, most lost over 90%+. ?Now consider October 2002. ?How many companies IPO’ed then? ?Very few, but?I remember one, Safety Insurance, that came public at the worst possible moment because it had?no other choice. ?Why else would the IPO price be below liquidation value? ?Great opportunity for those who had liquidity at a bad time.

The upshot is that because stock is issued at times that do not favor new investors, and stock is retired at times that do not favor existing investors, the dollar-weighted?returns for stocks in the above graph are overestimated by 1-2%/year. ?Stocks still beat bonds, but not by as much as one would think.

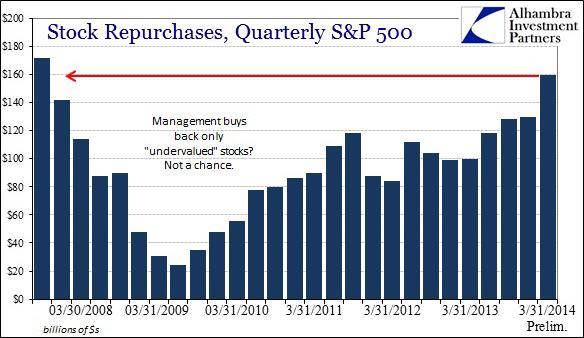

But here’s a counterexample, taken from Alhambra Investment Partners’ blog:

Note that buybacks don’t follow that pattern. ?Corporate managements often exist to justify themselves, and so a great number of them do not behave like value investors when they buy back stock. ?Part of this is that capital seems cheap during the boom phase of the market, and so they lever the company up, issuing debt to buy back stock at high prices. ?It increases earnings in the short-run, but when the bear market comes, the debt hangs ?around, and intensifies the fall in the stock price.

This is why I favor companies that shut off their buybacks at a certain valuation level. ?If they have to dispose of excess cash to avoid takeovers, pay out special dividends… leave the reinvestment issues to shareholders. ?If they buy back stock at levels that are too high, it does not increase the intrinsic value of the firm, though it might keep the price higher for a little while.

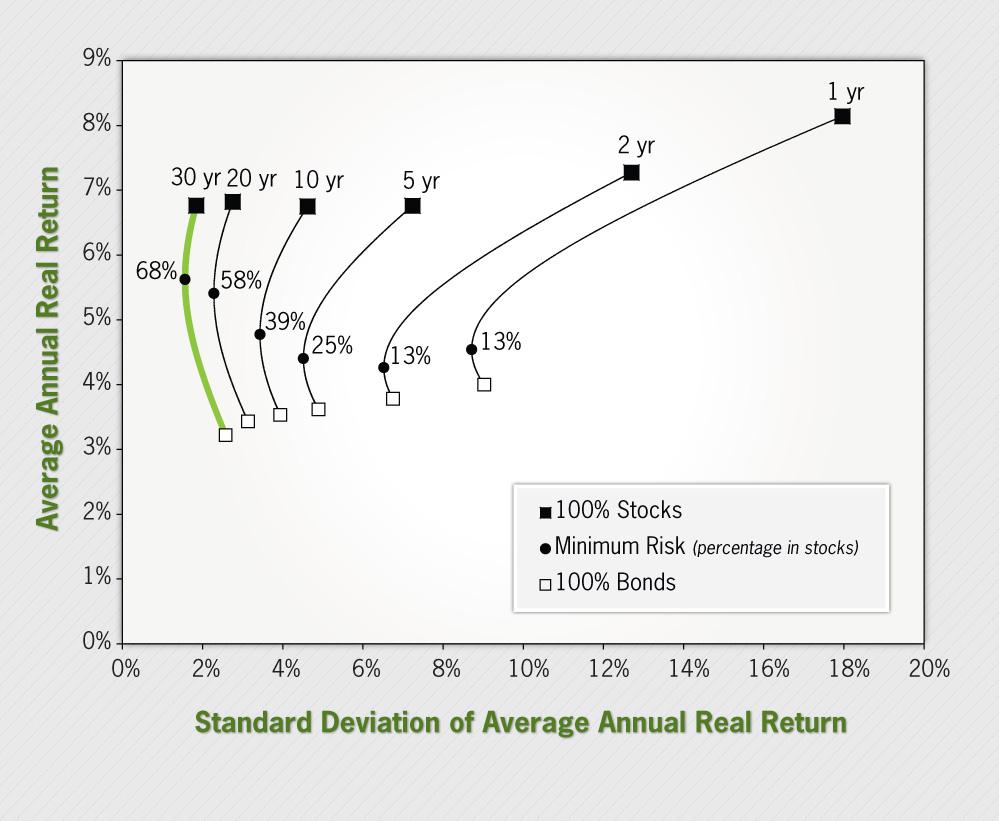

Here’s the other graph??from?this article at AAII, interviewing Jeremy Siegel:

What this graph is trying to say is that if you just buy and hold on long enough, results get really, really certain, and investing a lot in stocks reduces your risks, it does not raise your risks.

I’m here to tell you that is an amplification of the past, and maybe not even the best amplification of the past. ?This is where the victors write the history books. ?Your nation is blessed if:

- You haven’t had war on your home soil.

- There are no plagues or famines

- Socialism is kept in check; expropriation is not a risk (note the many countries grabbing pension assets today)

- Hyperinflation is avoided (we can handle the ordinary inflation)

Any of those, if bad enough, can really dent a portfolio. ?We can have fancy statistics, and draw smooth curves, but that only says that the future?will be like the past, only more so. 😉 ?I try to avoid the idea that?mankind will avoid the worst outcomes out of self-interest. ?There have been enough cases in history where that has not proven true, and envy and revenge dominate over shared prosperity.

I’ve already made the comment on how many can’t bear with short-run volatility. ?There is another factor: when you look at the above graph, it represents the average valuation level, yield curve shape, etc. ?If you are applying this model to today, where credit spreads are low, cash earns nothing, the yield curve is wide, equity valuations are medium-high, you would have to adjust the expected returns to reflect what the likely outcomes are, and the graph would not look as favorable. ?Volatility looks low today, but realized volatility is likely to be higher, and will not likely follow a normal distribution.

Closing

My main point here is to beware of history sneaking in and telling you that stocks are magic. ?Don’t get me wrong, they are very good, but:

- they?rely on a healthy nation standing behind them

- their past results are overstated on a dollar-weighted basis, and

- their past results come from a prosperous time which may not repeat to the same degree in the future

- you may not have the internal fortitude to buy and hold during hard times.

6 thoughts on “The Victors Write the History Books, Even in Finance”