Caption from the WSJ: Regulators don?t think it is the place of Congress to second guess how they size up securities. Fed Chairwoman Janet Yellen said recently that legislation would ?interfere with our supervisory judgments.? PHOTO: BAO DANDAN/ZUMA PRESS

Catch the caption from the WSJ for the above picture:

Regulators don?t think it is the place of Congress to second guess how they size up securities. Fed Chairwoman Janet Yellen said recently that legislation would ?interfere with our supervisory judgments.?

Regulators are not required by the Constitution, but Congress, perverse as it is, is the body closest to the people, getting put up for election regularly. ? Of course Congress should oversee financial regulation and monetary policy from?an unelected Federal Reserve. ?That’s their job.

I’m not saying that the Congressmen themselves understand these things well enough to do anything — but that’s true of most laws, etc. ?If the Federal Reserve says they are experts on these matters, past bad results notwithstanding, Congress can get people who are experts as well to aid them in their decisions on laws and regulations.

The above is not my main point, though. ?I have a specific example to draw on: municipal bonds. ?As the Wall Street Journal headline says, are they “Safe or Hard to Sell?” ?For financial regulation, that’s the wrong question, because this should be an asset-liability management problem. ?Banks should be buying assets and making loans that fit the structure of their liabilities. ?How long are the CDs? ?How sticky are the deposits and the savings accounts?

If the maturities of the munis match the liabilities of the bank, they will pay out at the time that the bank needs liquidity to pay those who place money with them. ?This is the same as it would be for any bond or loan.

If a bank, insurance company, or any financial institution relies on secondary market liquidity in order to protect its solvency, it has a flawed strategy. ?That means any market panic can ruin them. ?They need table stability, not bicycle stability. ?A table will stand, while a bicycle has to keep moving to stay upright.

What’s that you say? ?We need banks to do maturity transformation so that long dated projects can be cheaply funded by short-term savers. ?Sorry, that’s what leads to financial crises, and creates the run on liquidity when the value of long dated assets falls, and savers want their money back. ?Let long dated assets that want debt financing be financed by REITs, pension plans, endowments, long-tail casualty insurers, and life insurers. ?Banks should invest short, and use the swap market t aid their asset liability needs.

Thus, there is no need for the Fed to be worrying about muni market liquidity. ?The problem is one of asset-liability matching. ?Once that is settled, banks can make intelligent decisions about what credit risk to take versus their liabilities.

In many ways, our regulators learned the wrong lessons in the recent crisis, and as such, they meddle where they don’t need to, while neglecting the real problems.

But given the strength of the banking lobby, is that any surprise?

Before I start this evening, I want to add one follow-up to last night’s piece on Berkshire Hathaway. ?My summary was that it wasn’t a great year, and the profit margins are likely to shrink in insurance, because BRK is being conservative there. ?So why do I still own it for my clients and me?

BRK is trading maybe 8% over the level at which it would begin buying back stock. ?Even in a pessimistic year, I expect BRK’s book value to rise to the level that triggers the buyback. ?Thus, I think the floor for the stock is pretty close below me, and there is a decent possibility that Buffett could do some things with the cash that are even better than buybacks, especially if the market falls into bear territory.

It is positioned well for most market environments, even one where insurance gets hit hard. ?BRK is “the last man standing” in any insurance crisis — they have the ability to prosper when other companies will have their capital impaired, and can’t write as much business as they want.

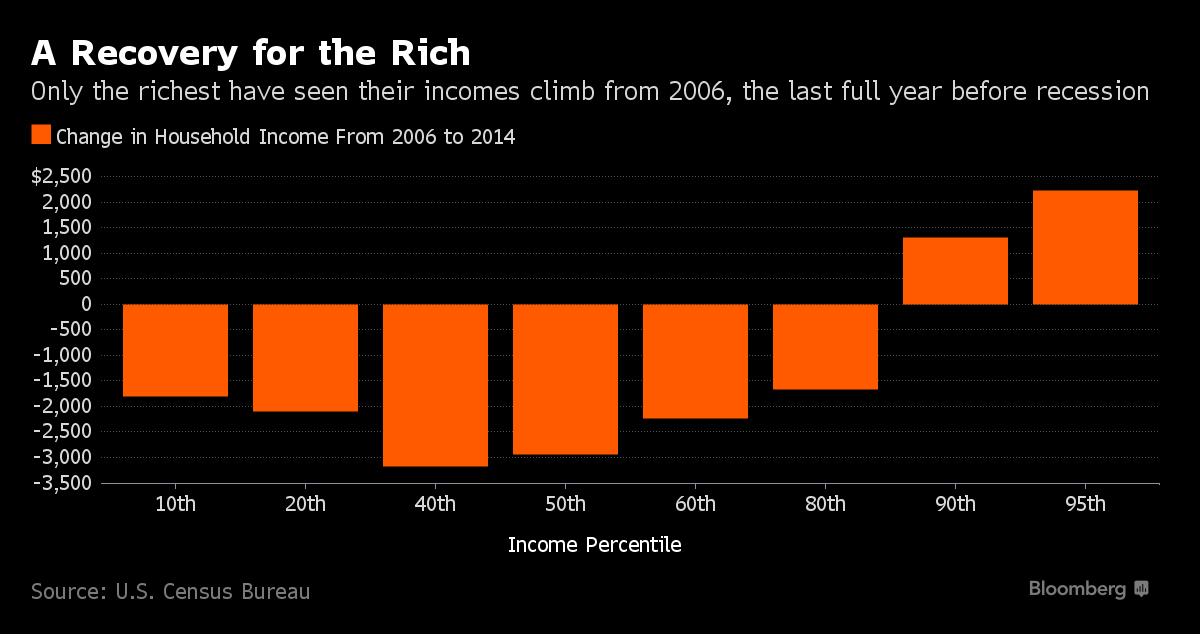

Incomes have not improved for the bottom 80% of Americans over the last decade. ?Before I go on, recognize that the income distribution is not static. ?The same people are not in each decile today, as were in 2006. ?Examples:

Highly skilled students in a field that is in demand graduate and get jobs that pay well.

Highly skilled immigrants?in a field that is in demand come to the US?and get jobs that pay well.

Less skilled people who relied on the private debt culture to keep getting larger no longer have jobs that pay well in finance, construction, real estate, etc.

Workers and businessman who expected the commodities and crude oil boom to go on forever have seen their prospects diminish.

Some people have retired and their income has fallen as a result.

Layoffs have come in some industries because many people did not realize that they were lower skilled workers, and as such the work that they did could be automated or transferred to other countries.

Manufacturing continues to get more efficient, and we need fewer jobs in manufacturing to produce the same output (or more). ?This is true globally; manufacturing jobs are being reduced globally.

Technology firms that apply the advantages of the internet gain value, while legacy firms lose value. ?Whole classes of goods go away because they are replaced, and in other cases, some firms find that they can’t price their products to make a decent profit, while other firms can.

Some effects are demographic, like mothers ceasing work to raise children, or industries with a lot of older workers becoming uncompetitive because their pension plans are too expensive to fund.

Divorce usually ruins the prospects of the wife, if not the husband.

Throw in death, disability, substance abuse, and serious diseases.

And more…

Thus there is a lot of reason to look at the graph and not say, “The rich are getting richer,” but, “Those who are getting rich today are doing so faster than those who were getting rich back in 2006.”

My life is even an example of that… I make less than 30% of what I was making in 2006. ?On an income basis, I’ve gone from the top of the graph to the middle. ?I’m not upset, because I’m debt free, and manage my finances well. ?I’m grateful to have my own little firm, and every client that I have.

Resentment

That said, many feel that the comfortable life that was theirs has been denied to them by forces beyond their control. They think that shadowy elites want to turn previously well-off people into modern serfs.

It’s a tempting thought, because most of us don’t like to blame ourselves. ?Myself included, we all make mistakes. ?Here is a sampling:

Did we make a bad decision in the industry in which we chose to work? ?The particular firm?

Did we choose a bad field of study in college? ?Rack up too much student loan debt?

Did we borrow too much money at the wrong time? ?(Remember, debt is always a risk. ?If you don’t know that, you shouldn’t borrow money.)

Did you make bad decisions regarding your assets, and get too greedy or fearful at the wrong times?

Did you spend too much during your good years, and not save enough for the future?

Did you not buy the insurance that would have protected you from the disaster that hit you?

Throw in relationship errors, etc.

The truth is, changes in technology, and to a lesser extent demography, affect the entities that we work in, and affect our personal economics as a result. ?There are some politicians blaming immigrants for our problems, and that’s not a major source of our difficulties. ?Most people don’t want to do the work that unskilled immigrants do, and skilled immigrants get hired when there aren’t enough people seeking those positions.

There is a need for retraining, but even that has its difficulties, as technology is changing rapidly enough that more areas may face job reductions. ?Again, this is a global thing. ?Those that think that?making trade less free will help matters are wrong. ?It’s not trade; it’s technology.

Some think that matters can be fixed by changing government taxes and spending. ?That would only help limitedly, if at all. ?Businesses and people can move to other countries. ?In an era of the internet, many more things can move than ever did previously.

Now, if the developed ?countries collaborated to unify tax policies, some of that would end. ?But cheating under such a regime is too tempting, just as Indiana and Wisconsin try to attract businesses to move out of Illinois. ?The relatively healthy governmental entities have advantages that allow them to prosper at the expense of the sick ones.

You’re Going to be Disappointed

Politicians live to promise. ?I can tell you right now that not one of the surviving candidates for President has a realistic proposal that could be voted up by the next Congress or the buyers in the US Treasury market. ?It’s all airy-fairy… just as most politicians have been since we stopped running balanced budgets.

I would encourage you therefore to look at your own situation and resources soberly, and assume that the next government will do nothing better for you than the current one. ?All of the main drivers of what could improve matters for the middle class are outside the power of any individual government, so plan your own situation accordingly and adjust your economic expectations down. ?After all, there is no place in the world that can promise its people prosperity. ?Why should the USA be any different in this matter?

Last year, when BRK [Berkshire Hathaway] reported their annual earnings with the letter, report, and 10K, I concluded:

From an earnings growth standpoint, there was nothing that amazing about the earnings in 2014. ?A few new subsidiaries like NV Energy added earnings, but existing subsidiaries? earnings were flattish. ?Comprehensive income was considerably lower because of the lesser degree of unrealized appreciation on portfolio holdings.

On net, it was a subpar year for Berkshire Hathaway. ?The annual letter provided a lot of flash and dazzle, but 2014 was not a lot to write home about, and limits to the BRK business model with respect to float are becoming more visible.

What I said one year ago would be a good summary for this year, though Buffett was more upbeat about outcomes this year, with BRK’s book value advancing while the S&P 500 fell on a total return basis.

Overall, BRK had a mediocre year. ?Insurance wasn’t that great. ?Here are my summary points:

BRK is reducing reinsurance — i suspect they aren’t getting the rates that they want. ?There are too many reinsurance wannabes attempting to write business to generate float that they can invest against. ?Typically, writing insurance in order to invest usually doesn’t work out. ?People forget how much money was lost writing marginal insurance business in soft markets thinking they would more than make up the losses with investment income. ?BRK is showing some discipline here — good.

Aside from new lines of business (specialty insurance), growth is slowing; BRK is trying to remain a conservative underwriter.

Reserving conservatism has not changed.

Asbestos position has not materially changed.

GEICO had a bad year for claims — maybe they grew too much, and maybe picked up a lower class of auto driver.

Profit margins falling

Float growth slowing

Continued problems with workers’ comp and long-term care at Gen Re. ?Also problems with payment annuities (blames FX, should blame longevity) and Life Reinsurance.

A few?quotes from the 10K on insurance issues:

“We define pre-tax catastrophe losses in excess of $100 million from a single event or series of related events as significant. In 2015, we recorded estimated losses of $136 million in connection with a property loss event in China.”

and on GEICO:

“Losses and loss adjustment expenses incurred in 2015 increased $2.7 billion (17.1%)?over 2014. Claims frequencies (claim counts per exposure unit) in 2015 increased in all major coverages over 2014, including property damage and collision coverages (three to five percent range), bodily injury coverage (four to six percent range) and personal injury protection (PIP) coverage (one to two percent range). Average claims severities were also higher in 2015 for property damage and collision coverages (four to five percent range), bodily injury coverage (six to seven percent range) and PIP coverage (two to four percent range). We believe that increases in miles driven, repair costs (parts and labor) and medical costs, as well as weather conditions contributed to the increases in frequencies and severities.”

Regarding Gen Re:

“The property/casualty business generated pre-tax underwriting gains in 2015 of $944 million compared to $1.4 billion in 2014. In 2015, we incurred losses of $86 million from an explosion in Tianjin, China. There were no significant catastrophe losses in 2014. Underwriting results in 2015 included comparatively lower gains from property catastrophe reinsurance and the run off of prior years? business.”

I found the mention of two large loss events in China interesting — maybe it was just one event of $136 million, but they could have been more clear.

Float Note

Before I leave the topic of insurance, I do want to set the record straight on how valuable float is. ?This is my best article on the topic. ?Buffett is a bit of a salesman in his annual letter, but generally an honest one.

Float is only as good as the insurance business generating it. ?If it is generating underwriting losses, the investments will have to earn at least as much per year as the losses divided by the average duration of how long the float will exist in years, in order to break even.

We’re coming off of years where there have been no underwriting losses, so float is?magical — but the P&C insurance industry is getting more competitive, and float will no longer be costless.

Widespread use of float for financing is like trying to finance off of other seemingly costless liabilities — in the hands of some?investors, that can lead to disaster — after all, consider all of the disasters that I have written about where people finance short to invest long.

Conservative insurers invest their premium reserves in cashlike instruments, and their loss reserves they invest in bonds of a similar duration. ?They typically don’t invest float in equities, and certainly not whole businesses.

Buffett has done just that and done well. ?That said, he runs his insurers at lower levels of leverage than most insurers, to allow room for taking more investment risk.

Note that BRK doesn’t guarantee the debts of BNSF, BHE, etc., but does guarantee the debts of the finance arms.

There is room for another article on float and cost of capital — not sure when I will get to it, but it will be a WACC-y article. 😉

Final Notes:

1) Note that Buffett keeps profits overseas also. Quoting the 10K: “We have not established deferred income taxes on accumulated undistributed earnings of certain foreign subsidiaries. Such?earnings were approximately $10.4 billion as of December 31, 2015 and are expected to remain reinvested indefinitely.” ?My guess is that he will use them to buy a foreign subsidiary.

2) BRK Pays taxes at about a 30% rate.

3) Regarding his comments on goodwill amortization — he thinks some of it is economically valid, and some not. ?Buffett has the option of putting more data on the income statement if he wants. ?Or put it in note 11 (goodwill). ?He already does that by breaking apart revenues and expenses by corporate divisions on the income statement. ?Do us all a favor, BRK, and split the goodwill into what you think is economically valid, and what is not.

4) Buffett gives an extended defense of Clayton Homes lending. ?In general, I thought his points were good — even before Buffett, Clayton was the “class act” in manufactured housing, and financing it.

5)?Even BRK has underfunded pension plans, and it has a relatively conservative 6.5% expected return on assets.

6) I note a modest change in 10K risk factors — BNSF and the automatic braking issue. ?BNSF will have to spend a lot of money to deal with the need to stop runaway trains remotely. ?True of all?US and Canadian railroads.

7)?BRK has less free cash flow to invest in new projects because more of their businesses are capital-intensive. ?BRK invested $16B in property, plant and equipment.

8 ) BNSF had a good year. ?BH Energy had a good year, mostly from a new Canadian Transmission utility, and their home brokerage arm.

9) BRK bought Precision Castparts, Van Tuyl (auto dealerships), and AltaLink (the Canadian Transmission utility). ?Also bolt-ons to existing subsidiaries.

10) Kraft merged with Heinz.?Heinz preferred will be redeemed.

11) The big four publicly traded firms owned by BRK didn’t have a good year. AXP, KO, IBM, WFC — he bought more of IBM and WFC. ?Buffett argues that the retained earnings of the firms benefit BRK. ?I’m dubious. ?IBM has particularly been a dog — look at free cash flow. ?Much of the earnings at IBM?aren’t real. ?You can’t use what they don’t dividend.

12) Quoting Buffett from his section?on optimism about the US, he tempered it by saying: “Though the pie to be shared by the next generation will be far larger than today?s, how it will be divided?will remain fiercely contentious.”

Well, you can say that again, but fairness is a squishy concept. ?Is fairness:

Even division (from each according to his ability, to each according to his needs)

Proportionate to productivity

Equal to what you negotiate

Derived from the formula of a bureaucrat

What you can negotiate through the political process

Impossible

Or something else?

Buffett worked with the easy stuff, and waved his hands at the hard stuff. ?I’ll phrase it this way: in general, the US has done well because we have not wrangled as much as the rest of the world over distribution issues, and have left a lot of room for people to?gain a lot from their own productivity. ?That has led to a lot of wealth, and in general, a growing pie for everyone to benefit from.

Productivity goes in waves, and labor plays catchup with capital after technological progress. ?We have seen people redeployed from agriculture and servanthood/slavery in the past 150 years. ?We will see them redeployed from manufacturing in the next 100 years. ?They will provide services to their fellow men, should there continue to be peace and tranquility, allowing labor income to catch up with that of capital.