Picture credit: DonkeyHotey || Should bonds get longer?

When I visited the US Treasury during the first Treasury/Blogger summit I encouraged the US Treasury to issue debts longer than 30 years, and also floating rate debt. I said the insurance companies, pension funds and endowments would be willing buyers, and that it would be cheaper than issuing 30-year bonds. I thought that the yields on (say) 50-year bonds would be lower than 30-year bonds, because the yield curve for most of my life (at that point) had the yield curve peaking out at around 22 years or so. 30-year bonds usually yielded less than 20-year bonds.

The case for issuing longer debt was easy when 30-year bonds yielded less than 20-year bonds. That is no longer true, and has not been true since the financial crisis. In a low interest rate environment, 30-year bonds yield more than 20–year bonds. In a higher interest rate environment, the relationship flips.

So, should the US treasury issue 50-year, 100-year, or perpetual bonds? I still think the answer is yes, and for three reasons.

1) It’s an experiment. The market doesn’t always know what it wants until you offer an option to it. No degree of discussion with the advisory committee can beat an actual offering to the market. There used to be callable T-notes, and even a Treasury note denominated in Swiss Francs. Experiments are worth trying on a small level just to see what happens. Knowledge is a valuable thing — theory is worth less than tangible data.

2) Rates are low. Why not lock in the low rates? Even if 50-year bonds have a premium yield to 30-year bonds, those yields are likely lower than what you might get when interest rates are high.

3) It would be genuinely useful for life insurance companies and pension funds to have a benchmark for 50-year bonds, which would encourage the corporate market to issue debt as well. Those who make long promises need others who will make similarly long fixed commitments.

Then there are the speculators, who I don’t care much about. They would appreciate longer debt as well, as it would give them a greater place to speculate.

My advice to the US Treasury is this: issue longer debt as an experiment. If there is additional cost in the short-run, see if it is cheaper in the long run. There is a market for longer debt, even if your advisory committee thinks differently.

The future return keeps getting lower, as the market goes higher

=================

Jeff Bezos has a saying, “Your margin is my opportunity.”? He has found ways to eat the businesses of others by providing the same goods and services at a lower cost.? Now, that makes Amazon more productive and others less productive.? The same is true of other internet-related businesses like Google, Netflix, etc.

And, there is a slight net benefit to the economy from the creative destruction.? Old capital gets recycled.? Malls that are no longer so useful serve lower-margin businesses for locals, become homes to mega-churches, other area-intensive human gatherings, or get destroyed, and the valuable land so near many people gets put to alternative uses that are better than the mall, but not as profitable as the mall prior to the internet.

Laborers get released to other work as well.? They may get paid less than they did previously, but the system as a whole is more productive, profits rise, even as wages don’t rise so much.? A decent part of that goes to the pensions of oldsters — after all, who owns most of the stock?? Indirectly, pension plans and accounts own most of it.? As I have sometimes joked, when there are layoffs because institutional investors representing pension plans? are forcing companies to merge, or become more efficient in other ways, it is that the parents are laying off their children, because there are cheaper helpers that do just as well, and the added profits will aid their deservedly lush retirement, with little inheritance for their children.

It is a joke, though seriously intended.? Why I am mentioning it now, is that a hidden assumption of my S&P 500 estimation model is that the return on assets in the economy as a whole is assumed to be constant.? Some will say, “That can’t be true.? Look at all of the new productive businesses that have been created! The return on assets must be increasing.”? For every bit of improvement in the new businesses, some of the old businesses are destroyed.? There is some net gain, but the amount of gain is not that large in aggregate, and these changes have been happening for a long time.? Technological progress creates and destroys.

As such, I don’t think we are in a “New Era.”? Or maybe we are always in a “New Era.”? Either way, the assumption of a constant return on assets over time doesn’t strike me as wrong, though it might seem that way for a decade or two, low or high.

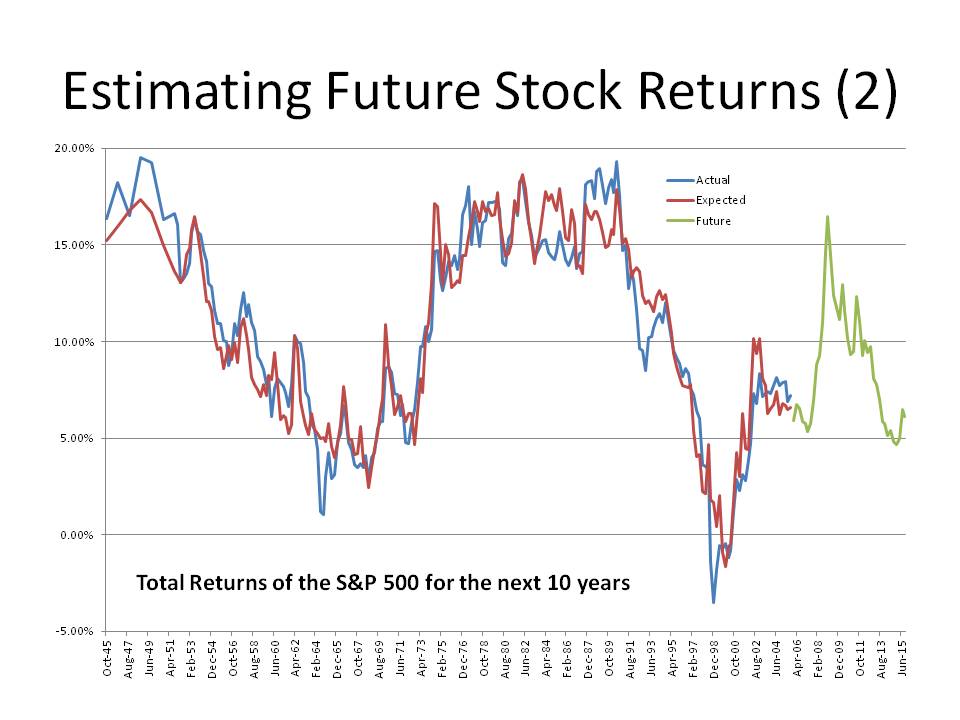

As it is today, the S&P 500 is priced to deliver returns of 3.24%/year not adjusted for inflation over the next ten years.? At 12/31/2017, that figure was 3.48%, as in the graph above.

We are at the 95th percentile of valuations.? Can we go higher?? Yes.? Is it likely?? Yes, but it is not likely to stick.? Someday the S&P 500 will go below 2000.? I don’t know when, but it will.? There are enough imbalances in the world — too many liabilities relative to productivity, that crises will come.? Debt creates its own crises, because people rely on those payments in the short-run, unlike stocks.

There are many saying that “there is no alternative” to owning stocks in this environment — the TINA argument.? I think that they are wrong.? What if I told you that the best you can hope for from stocks over the next 10 years is 4.07%/year, not adjusted for inflation?? Does 1.24%/year over the 10-year Treasury note really give you compensation for the additional risk?? I think not, therefore bonds, low as they may be, are an alternative.

The top line there is a 4.07%/year return, not adjusted for inflation

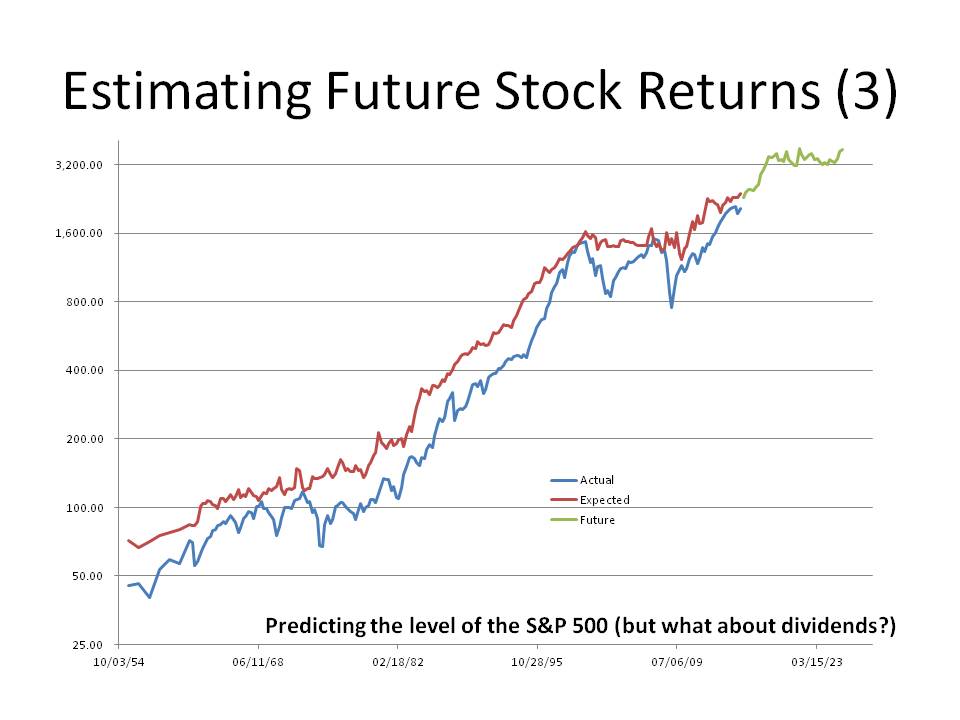

If you are happy holding onto stocks, knowing that the best scenario from past history would be slightly over 3400 on the S&P 500 in 2028, then why not buy a bond index fund like AGG or LQD that could virtually guarantee something near that outcome?

Is there risk of deflation?? Yes there is.? Indebted economies are very susceptible to deflation risk, because wealthy people with political influence will always prefer an economy that muddles, to higher taxes on them, inflation, or worst of all an internal default.

That is why I am saying don’t assume that the market will go a lot higher.? Indeed, we could hit levels over 4000 on the S&P if we go as nuts as we did in 1999-2000.? But the supposedly impotent Fed of that era raised short-term rates enough to crater the market.? They are in the process of doing that now.? If they follow their “dot plot” to mid-2019 the yield curve will invert.? Something will blow up, the market will retreat, and the next loosening cycle will start, complete with more QE.

Thus I am here to tell you, there is an alternative to stocks.? At present, a broad market index portfolio of bonds will likely outperform the stock market over the next ten years, and with lower risk.? Are you ready to make the switch, or at least, raise your percentage of safe assets?

Picture Credit: Roadsidepictures from The Little Engine That Could By Watty Piper, Illustrated By George & Doris Hauman | That said, for every one that COULD, at least two COULDN’T

======================================

So what do you think of the market?? Why are both actual and implied volatility so low?? Why are the moves so small, but predominantly up?? Is this the closest impression of the Chinese Water Torture that a stock market can pull off?

Why doesn’t the market care about external and internal risks?? Doesn’t it know that we have divisive, seemingly incompetent President who looks like he doesn’t know how to do much more than poke people in the eyes, figuratively?? Doesn’t it know that we have a divided, incompetent Congress that can’t get anything of significance done?

Leaving aside the possibility of a war that we blunder into (look at history), what if the inability of Washington DC to do anything is a plus?? Government on autopilot for four years, maybe eight if we decide we are better of without change — is that a plus or minus?? Just ignore the noise, Trump, other politicians, media… ahh, the quiet could be nice.

Then think about Baby Boomers showing up late for retirement, and wondering what they are going to do.? Then think about their surrogates, the few who still have defined benefit pension plans.? What are they going to do?? Say that the rate that they are targeting for investment earnings is 7%/year forever.? Even if my model for investment returns is wrong in a pessimistic way — i.e., my 4% nominal should be 6%/year nominal, you still can’t hit your funding target.? As for those with defined contribution plans, when you are way behind, even contributing more won’t do much unless investment earnings provide some oomph.

I am personally not a fan of TINA — “there is no alternative” to stocks in the market, but I recognize the power of the idea with some.? It is my opinion that more people and their agents will run above average risks in order to try to hit an unlikely target rather than lock in a loss versus what is planned.? Most will “muddle in the middle” taking some risk even with a high market, and realizing that they aren’t going to get there, but maybe a late retirement is better than none.

That’s the power of bonds returning 3% at best over the forecast horizon, unless interest rates jump, and then we have other problems, like risk assets repricing.? If you are older, almost no plan is achievable at reasonable cost if you are coming to the game now, rather than starting 15+ years ago.

And so I come to “the little market that could…” for now.? My view is that those with retirement obligations to fund are bidding up the market now.? That does two things.? Shares of risk assets (stocks) move from the hands of stronger investors to weaker investors, while cash flows the opposite direction.? In the process, prices for risk assets get bid up relative to their future free cash flows.

Unlike “the little engine that could,” the little market that could has climbed some small hills relative to the funding targets that investors need. Ready for the Himalayas?? The trouble with those targets is that regardless of what the trading price of the risk assets is, the cash flows that they produce will not support those targets.

Well, guess what?? In the long run, the returns from public stock investments reflect just that — the distributable amount of earnings that they generate, regardless of what a marginal bidder is willing to pay for them at any point in time.? Stocks aren’t magic, any more than the firms that they represent ownership in.

So… we can puzzle over the current moment and wonder why the market is behaving in a placid, slow-climbing manner.? Or, we can look at the likely inadequacy of asset cash flows versus future demands for those cash flows for retirement, etc.? Personally, I think they are related as I have stated above, but the second view, that asset returns will not be able to fund all planned retirement needs is far more certain, and is one mountain that “the little market that could” cannot climb.

Thus, consider the security of your own plans, and adjust accordingly.? As I commented recently, for older folks with enough assets, maybe it is time to lock in gains.? For others, figure out what adjustments and compromises will need to be made if your assets can’t deliver enough.

Tough stuff, I know.? But better to be realistic about this than to be surprised when funding targets are not reached.

I am a fiduciary in my work that I do for my clients. I am also the largest investor in my own strategies, promising to keep a minimum of 80% of my liquid net worth in my strategies, and 50% of my total net worth in them (including my house, etc.).

I believe in eating my own cooking. ?I also believe in treating my clients well. ?I’ve treated part of this in an earlier post called?It?s Their Money, where I describe how I try to give exiting clients a pleasant time on the way out. ?For existing clients, I will also help them with situations where others are managing the money at no charge, no payment from another party, and no request that I manage any of those assets. ?I do that because I want them to be treated well by me, and I know that getting good advice is hard. ?As I wrote in a prior article?The Problem of Small Accounts:

We all want financial advice.? Good advice.? And we want it for free.? That?s why we come to the Aleph Blog, where advice is regularly dispensed, and at no cost.

But? I can?t be personal, and give you advice that is tailored to your situation.? And in my writing here, much as I try to be highly honest, I am not acting as a fiduciary, even though I still make my writings hold to such a standard.

Ugh.? Here?s the problem.? Good advice costs money.? Really good advice costs a lot of money, and is worth it, if you have enough money to spread the cost over.

But when you have a small account, you have a problem in getting advice.? There is no way for someone who is fiduciary (like me) to make money addressing your concerns.? That is why I have a high minimum for investing: $100,000.? With that, I can spend time on clients, even helping them with assets from which I make no money.

What extra things have I done for clients over time? ?I have:

Analyzed asset allocations.

Analyzed the performance of other managers.

Advised on changing jobs, negotiating salary, etc.

Explained the good and bad points of certain insurance companies and their policies, and suggested alternatives.

Analyzed chunky assets that they own elsewhere, aiding them in whether they keep, sell, or sell part of the asset.

Analyzed a variety of funky and normal investment strategies.

Advised on buying a building, and future business plans.

Told a client he was better off reinvesting the slack funds in his business that needed?financing, rather than borrow and invest the funds with me.

Told a client to stop sending me money, and pay down his mortgage. ?(He has since resumed sending money, but he is now debt-free.)

I take the fiduciary side of this seriously, and will?tell clients that want to put a?lot of their money in my stock?strategy that they need less risk, and should put funds in my bond strategy, where I earn less.

I’ve got a lot already. ?I don’t need to feather my nest at the expense of the best interests of my clients.

Over the last six years, around half of my clients have availed themselves of this help. ?If you’ve read Aleph Blog for awhile, you know that I have analyzed a wide number of things. ?Helping my clients also sharpens me for understanding the market as a whole, because issues come into focus when the situation of a family makes them concrete.

So informally, I am more than an “investments only” RIA [Registered Investment Advisor], but I only earn money off of my investment fees, and no other way. ?Personally, I think that other “investments only” RIAs would mutually benefit their clients if they did this as well — it would help them understand the struggles that they go through, and inform their view of the economy.

Thus I say to my competitors: do you want to justify your fees? ?This is a way to do it; perhaps you should consider it.

Postscript

Having some people in an “investment only” shop that understand the basic questions that most clients face also has some crossover advantages when it comes to understanding financial companies, and different places that institutional money gets managed. ?It gives you a better idea of the investment ecosystem that you live and work in.

Aside from the bankruptcy of a plan sponsor, the benefits of someone being paid their pension can’t be cut. ?Right?

Well, mostly true. ?With governments in trouble, benefits have been cut, as in Rhode Island, Detroit, and a variety of other places with badly managed finances. ?Usually that’s a big political fight. ?Concessions come partly as a result that you could end up with less if you fight it, and don’t take the deal.

With corporations, the protection of the Pension Benefits Guarantee Corporation [PBGC] has kept pensions safe up to a limit — as of 2016, up to roughly $60K/year for those retiring at age 65 (less for younger retirees) from single-employer plans, and $12,870/year at most for those in multiemployer plans. ?(For some complexities, read more here. ?Also note that the PBGC itself is underfunded and faces antiselection problems as well.)

Multiemployer plans are an inherently weak structure, because?insolvent employers can’t contribute to fund plan deficits, and typically, multiemployer plans arise from collective bargaining arrangements, so that the firms employing the laborers are all in the same industry. ?Insolvency in industries, particularly where there is collective bargaining pushing up costs and limiting work process flexibility, tends to be correlated across firms. ?My poster child for that was the steel industry in 2002, where 20+ firms went insolvent. ?Employer insolvencies in an underfunded multiemployer plan affect all participants, including those working for solvent firms. ?(Note that solvent employers have to pay their pro-rata?share of underfunding in order to exit a multiemployer plan, as I noted for UPS in this article.)

Now in 2014, Congress passed a law called the?Kline-Miller Multiemployer Pension Reform Act of 2014. ?That allowed the PBGC, together with the Departments of Treasury and Labor, to negotiate benefit cuts to the pension plans in order to avoid the plans going insolvent — at which point, all pensioners would be limited to the PBGC limits for their payments. ?Workers in the plan — active, vested, and retired, would have to vote on any deal. ?Majority of those voting wins, so to speak.

The first plan to successfully go through this procedure and cut benefits to participants happened a few weeks ago, in the Iron Workers Local 17 Pension fund. ?Average benefits were cut 20%, with some cut as much as 60%, and some not cut at all. ?The plan was funded to a 24% level, and there are only 632 active employed workers to cover the benefits of 2,042 participants. ?The fund would likely run out of money in 2024. ?Note that only 900+ voted on the cuts, with the cuts passing at roughly 2-1.

There are at least four other multiemployer plans with similar applications to cut benefit payments. ?Prior to this four other multiemployer plans had such applications denied — there were a variety of reasons for the denials: the cuts were done in an inequitable way in some cases, return assumptions were unreasonably high, etc.

My original source for this piece is note by David Gonzales of Moody’s. ?They rate these actions as credit positive because it potentially ends the process where an underfunded multiemployer plan would encourage an employer to default because it can’t afford the liability. ?Somewhat perverse in a way, because the pain has to go somewhere on an underfunded plan — it’s all a question of who gets tapped. ?Note that it also protects the PBGC Multiemployer Trust, which itself is likely to run out of money by 2025. ?After that, those relying on the PBGC for multiemployer pension payments get zero, unless something changes.

You might think this is an extreme situation, and yes, it is extreme. ?It’s not so extreme that there aren’t other underfunded plans as bad off as this multiemployer plan. ?I would encourage everyone who has a defined benefit plan to take a close look at their funded status. ?I don’t care about what your state constitution says on protecting your pension benefits. ?If the cash gets close to running out, “the?powers that be” will find a way around that. ?After all, what happened with the?Iron Workers Local 17 Pension Fund was illegal prior to 2014. ?Now it is 2017, and benefits were cut.

Because of underfunding, there will be more cuts. ?Depend on that happening for the worst funds, and at least run through the risk analysis of what you would do if your pension benefit were cut by 20% for a municipal plan, or to the PBGC limit for a corporate plan. ?Why? ?Because it could happen.

If you want a full view of what I am writing about today, look at this article from The Post and Courier, “South Carolina’s looming pension crisis.” ?I want to give you some perspective on this, so that you can understand better what went wrong, and what is likely to go wrong in the future.

Before I start, remember that the rich get richer, and the poor poorer even among states. ?Unlike what many will tell you though, it is not any conspiracy. ?It happens for very natural reasons that are endemic in human behavior. ?The so-called experts in this story are not truly experts, but sourcerer’s apprentices who know a few tricks, but don’t truly understand pensions and investing. ?And from what little I can tell from here, they still haven’t learned. ?I would fire them all, and replace all of the boards in question, and turn the politicians who are responsible out of office. ?Let the people of South Carolina figure out what they must do here — I’m a foreigner to them, but they might want to hear my opinion.

Let’s start here with:

Central Error 1: Chasing the Markets

Credit: The Courier and Post

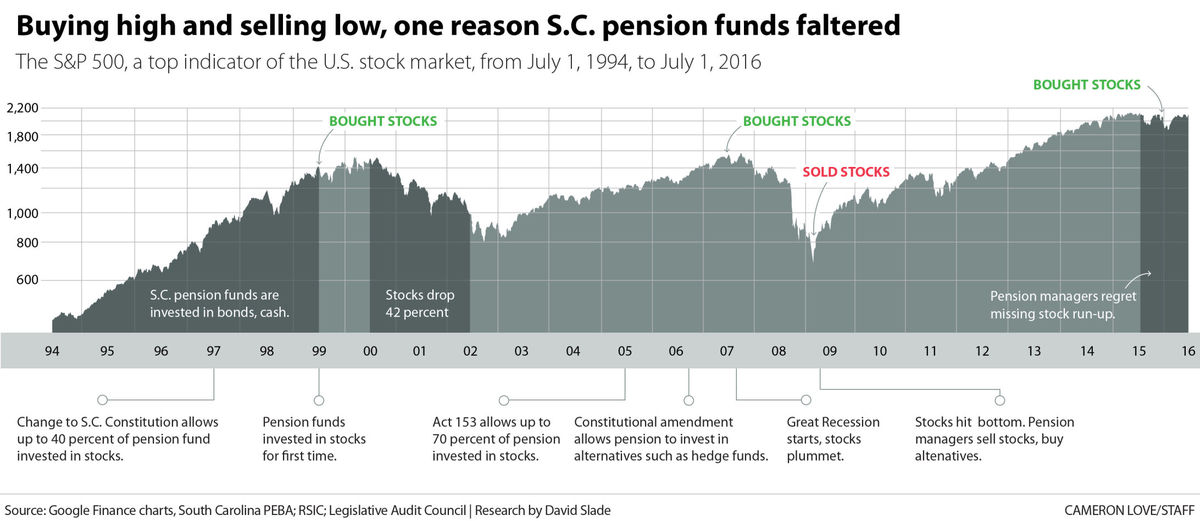

Much as inexperienced individuals did, the South Carolina?Retirement System Investment Commission [SCRSIC] chased the markets in an effort to earn returns when they seemed easy to get in hindsight. ?As the article said:

It used to be different, before the high-octane investment strategies began. South Carolina?s pension plans were considered 99 percent funded in 1999, and on track to pay all promised benefits for decades to come.

That was the year the pension funds started investing in stocks, in hopes of pulling in even more income. A change to the state constitution and action by the General Assembly allowed those investments. In the previous five years, U.S. stock prices had nearly tripled.

Prior to that time, the pension funds were largely invested in bonds and cash, which actually yielded something back then. ?If the pension funds were invested in bonds that were long, the returns might not have been so bad versus stocks. ?But in the late ’90s the market went up aggressively, and the money looked easy, and it was easy, partly due to loose monetary policy, and a mania in technology and internet stocks.

Here’s the real problem. ?It’s okay to invest in only bonds. It’s okay to invest in bonds and stocks in a fixed proportion. ?It’s okay even to invest only in stocks. ?Whatever you do, keep the same policy over the long haul, and don’t adjust it. ?Also, the more nonguaranteed your investments become (anything but high quality bonds), the larger your provision against bear markets must become.

And, when you start a new policy, do what is not greedy. ?1999-2000 was the right time to buy long bonds and sell stocks, and I did that for a small trust that I managed at the time. ?It looked dumb on current performance, but if you look at investing as a business asking what level of surplus?cash flows the underlying investments will throw off, it was an easy choice, because bonds were offering a much higher future yield than stocks. ?But the natural tendency is to chase returns, because most people don’t think, they imitate. ?And that was true for the SCRSIC,?bigtime.

Central Error 2:?Bad Data

The above quote said that “South Carolina?s pension plans were considered 99 percent funded in 1999.” ?That was during an era when government accounting standards were weak. ?The?standards are still weak, but they are stronger than they were. ?South Carolina was NOT 99% funded in 1999 — I don’t know what the right answer would have been, but it would have been considerably lower, like 80% or so.

Central Error 3: Unintelligent Diversification into “Alternatives”

In 2009, I had the fun of writing a small report for CALPERS. ?One of my main points was that they allocated money to alternative investments too late. ?With all new classes of investments the best deals get done early, and as more money flows into the new class returns surge because the flood of buyers drives prices up. ?Pricing is relatively undifferentiated, because experience is early, and there have been few failures. ?After significant failures happen, differentiation occurs, and players realize that there are sponsors with genuine skill, and “also rans.” ?Those with genuine skill also limit the amount of money they manage, because they know that good-returning ideas are hard to come by.

The second aspect of this foolishness comes from the consultants who use historical statistics and put them into brain-dead mean-variance models which spit out an asset allocation. ?Good asset allocation work comes from analyzing what economic return the underlying business activities will throw off, and adjusting for risk qualitatively. ?Then allocate funds assuming they will never be able to trade something once bought. ?Maybe you will be able to?trade, but never assume there will be future liquidity.

The article kvetches about the expenses, which are bad, but the strategy is worse. ?The returns from all of the non-standard investments were poor, and so was their timing — why invest in something not geared much to stock returns when the market is at low valuations? ?This is the same as the timing problem in point one.

Alternatives might make sense at market peaks, or providing liquidity in distressed situations, but for the most part they are as saturated now as public market investments, but with more expenses and less liquidity.

Central Error 4: Caring about 7.5% rather than doing your best

Part of the justification for buying the alternatives rather than stocks and bonds is that you have more of a chance of beating the target return of the plan, which in this case was 7.5%/yr. ?Far better to go for the best risk-adjusted return, and tell the State of South Carolina to pony up to meet the promises that their forbears made. ?That brings us to:

Central Error 5: Foolish politicians who would not allocate more money to pensions, and who gave?pension increases rather than wage hikes

The biggest error belongs to the politicians and bureaucrats who voted for and negotiated higher pension promises instead of higher wages. ?The cowards wanted to hand over an economic benefit without raising taxes, because the rise in pension benefits does not have any immediate cash outlay if one can bend the will of the actuary to assume that there will be even higher investment earnings in the future to make up the additional benefits.

[Which brings me to a related pet peeve. ?The original framers of the pension accounting rules assumed that everyone would be angels, and so they left a lot of flexibility in the accounting rules to encourage the creation of defined benefit plans, expecting that men of good will would go out of their way to fund them fully and soon.

The last 30 years have taught us that plan sponsors are nothing like angels, playing for their own advantage, with the IRS doing its bit to keep corporate plans from being fully funded so that taxes will be higher. ?It would have been far better to not let defined benefit plans assume any rate of return greater than the rate on Treasuries that would mimic their liability profile, and require immediate relatively quick funding of deficits. ?Then if plans outperform Treasuries, they can reduce their contributions by that much.]

Error 5 is likely the biggest error, and will lead to most of the tax increases of the future in many states and municipalities.

Central Error 6: Insufficient Investment Expertise

Those in charge of making the investment decisions proved themselves to be as bad as amateurs, and worse. ?As one of my brighter friends at RealMoney, Howard Simons, used to say (something like), “On Wall Street, to those that are expert, we give them super-advanced tools that they can use to destroy themselves.” ? The trustees of?SCRSIC received those tools and allowed themselves to be swayed by those who said these magic strategies will work, possibly without doing any analysis to challenge the strategies that would enrich many third parties. ?Always distrust those receiving commissions.

Central Error 7: Intergenerational Equity of Employee Contributions

The last problem is that the wrong people will bear the brunt of the problems created. ?Those that received the benefit of services from those expecting pensions will not be the prime taxpayers to pay those pensions. ?Rather, it will be their children paying for the sins of the parents who voted foolish people into office who voted for the good of current taxpayers, and against the good of future taxpayers. ?Thank you, Silent Generation and Baby Boomers, you really sank things for Generation X, the Millennials, and those who will follow.

Conclusion

Could this have been done worse? ?Well, there is Illinois and Kentucky. ?Puerto Rico also. ?Many cities are in similar straits — Chicago, Detroit, Dallas, and more.

Take note of the situation in your state and city, and if the problem is big enough, you might consider moving sooner rather than later. ?Those that move soonest will do best selling at?higher real estate prices, and not suffer the soaring taxes and likely?diminution of city services. ?Don’t kid yourself by thinking that everyone will stay there, that there will be a bailout, etc. ?Maybe clever ways will be found to default on pensions (often constitutionally guaranteed, but politicians don’t always honor Constitutions) and municipal obligations.

Forewarned is forearmed. ?South Carolina is a harbinger of future problems, in their case made worse by opportunists who sold the idea of high-yielding investments to trustees that proved to be a bunch of rubes. ?But the high returns were only needed because of the overly high promises made to state employees, and the unwillingness to levy taxes sufficient to fund them.

[bctt tweet=”Seven central errors committed by the South Carolina Retirement System and politicians” username=”alephblog”]

If you knew me when I was young, you might not have liked me much. ?I was the know-it-all who talked a lot in the classroom, but was quieter outside of it. ?I loved learning. ?I mostly liked my teachers. ?I liked and I didn’t like my fellow students. ?If the option of being home schooled had been offered to me, I would have jumped at it in an instant, because then I could learn with no one slowing me down, and no kids picking on me.

I read a lot. A LOT. ?Even when young I spent my time on the adult side of the library. ?The librarians typically liked me, and helped me find stuff.

I became curious about investing for two reasons. 1) my mother did it, and it was difficult not to bump into it. ?She would watch Wall Street Week, and often, I would watch it with her. ?2) Relatives gave me gifts of stock, and my Mom taught me where to look up the price in the newspaper.

Now, if you knew the stocks that they gave me, you would wonder at how I still retained interest. ?The two were the conglomerate Litton Industries, and the home electronics company?Magnavox. ?Magnavox was bought out by Philips in 1974 for a price that was 25% of the original cost basis of my shares. ?We did worse on Litton. ?Bought in the mid-to-late ’60s and sold in the mid-’70s for a 80%+ loss. ?Don’t blame my mother for any of this, though. ?She rarely bought highfliers, and told me that she would have picked different stocks. ?Gifts are gifts, and I didn’t need the money as a kid, so it didn’t bother me much.

At the library, sometimes I would look through some of the research volumes that were there for stocks. ?There are a few things that stuck with me from that era.

1) All bonds traded at discounts. ?It’s not that I understood it well, but I remember looking at bond guides, and noted that none of the bonds traded over $100 — and not surprisingly, they all had low coupons.

In those days, some people owned individual bonds for income. ?I remember my Grandma on my mother’s side talking about how little one of her bonds paid in interest, given that inflation was perking up in the 1970s. ?Though I didn’t hear it in that era, bonds were sometimes called “certificates of confiscation” by professionals ?in the mid-to-late ’70s. ?My Grandpa on my father’s side thought he was clever investing in short-term CDs, but he never changed on that, and forever missed the rally in stocks and long bonds that kicked off in 1982.

When I became a professional bond investor at the ripe old age of 38 in 1998, it was the opposite — almost all bonds traded at premiums, and had relatively high coupons. ?Now, at that time I knew a few firms that were choking because they had a rule that said you can never buy premium bonds, because in a bankruptcy, the premium will be automatically lost. ?Any recoveries will be off the par value of the bond, which is usually $100.

2) Many stocks paid dividends that were higher than their earnings. ?I first noticed that while reading through Value Line, and wondered how that could be maintained. ?The phrase “borrowing the dividend” was bandied about.

Today as a professional I know that we should look at free cash flow as a limit for dividends (and today, buybacks, which were unusual to unheard of when I was a boy), but earnings still aren’t a bad initial proxy for dividend viability. ?Even if you don’t have a cash flow statement nearby, if debt is expanding and earnings don’t cover the dividend, I would be concerned enough to analyze the situation.

3) A lot of people were down on stocks and bonds — there was a kind of malaise, and it did not just emanate from Jimmy Carter’s mind. [Cue the sad Country Music] Some concluded that inflation hedges like homes, short CDs, and gold/silver were the only way to go. ?I remember meeting some goldbugs in 1982 just as the market was starting to take off, and they disdained the idea of stocks, saying that history was their proof.

The “Death of Equities” came and went, but that reminds me of one more thing:

4) There was a decent amount of pessimism about defined benefit plan pension funding levels and life insurer solvency. ?Inflation and high interest rates made life insurers look shaky if you marked the assets alone to market (the idea of marking liabilities to market was at least 10 years off in concept, and still hasn’t really arrived, though cash flow testing accomplishes most of the same things). ?Low stock and bond prices made pension plans look shaky. ?A few insurance companies experimented with buying gold and other commodities, just in time for the grand shift that started in 1982.

Takeaways

The biggest takeaway is to remember that as a fish you don’t notice the water that you swim in. ?We are so absorbed in the zeitgeist (Spirit of the Times)?that we usually miss that other eras are different. ?We miss the possibility of turning points. ?We miss the possibility of things that we would have not thought possible, like negative interest rates.

In the mid-2000s, few thought about the possibility of debt deflation having a serious impact on the US economy. ?Many still feared the return of inflation, though the peacetime inflation of the late ’60s through mid-’80s was historically unusual.

The Soviet Union will bury us.

Japan will bury us. ?(I’m listening to some Japanese rock as I write this.) 😉

China will bury us.

Few people can see past the zeitgeist. ?Many can’t remember the past.

Should we?be concerned about companies not being able pay their dividends and fulfill their buybacks? ?Yes, it’s worth analyzing.

Should we be concerned about defined benefit plan funding levels? Yes, even if interest rates rise, and percentage deficits narrow. ?Stocks will likely fall with bonds if real interest rates rise. ?And, interest rates may not rise much soon. ?Are you ready for both possibilities?

Average people don’t seem that excited about any asset class today. ?The stock market is at new highs, and there isn’t really a mania feel now. ?That said, the ’60s had their highfliers, and the P/Es eventually collapsed amid inflation and higher real interest rates. ?Those that held onto the Nifty Fifty may not have lost money, but few had the courage. ?Will there be a correction for the highfliers of this era, or, is it different this time?

It’s never different.

It’s always different.

Separating the transitory from the permanent is tough. ?I would be lying to you if I said I could do it consistently or easily, but I spend time thinking about it. ?As Buffett has said, (something like)?”We’re paid to think about things that can’t happen.”

Ending Thoughts

Now, lest the above seem airy-fairy, here are my biases at present as I try to separate the transitory from the permanent:

The US is in better shape than most of the rest of the world, but its securities are relatively priced for that reality.

Before the US has problems, Japan, China, OPEC, and the EU will have problems, in about that order. ?Sovereign default used to be a large problem. ?It is a problem that is returning. ?As I have said before — this era reminds me of the 1840s — huge debts and deficits, with continued currency debasement. ?Hopefully we don’t get a lot of wars as they did in that decade.

I am treating long duration bonds as a place to speculate — I’m dubious as to how much Trump can truly change things. ?I’m flat there now. ?I think you almost have to be a trend follower there.

The yield curve will probably flatten quickly if the Fed tightens more than once more.

The internet and global demographics are both forces for deflationary pressure. ?That said, virtually the whole world has overpromised to their older populations. ?How that gets solved without inflation or defaults is a tough problem.

Stocks are somewhat overvalued, but the attitude isn’t frothy.

DIvidend stocks are kind of a cult right now, and will suffer some significant setback, particularly if interest rates rise.

Eventually emerging markets and their stocks will dominate over developed markets.

Value investing will do relatively better than growth investing for a while.

That’s all for now. ?You may conclude very differently than I have, but I would encourage you to try to think about the hard problems of our world today in a systematic way. ?The past teaches us some things, but not enough, which should tell all of us to do risk control first, because you don’t know the future, and neither do I. 🙂

There are many alternative models for attempting to estimate how undervalued or overvalued the stock market is. ?Among them are:

Price/Book

P/Retained Earnings

Q-ratio (Market Capitalization of the entire market /?replacement cost)

Market Capitalization of the entire market / GDP

Shiller?s CAPE10 (and all modified versions)

Typically these explain 60-70% of?the variation in stock returns. ?Today I can tell you there is a better model, which is not mine, I found it at the blog?Philosophical Economics.? The basic idea of the model is this: look at the proportion of US wealth held by private investors in stocks using the?Fed?s Z.1 report. The higher the proportion, the lower future returns will be.

There are two aspects of the intuition here, as I see it: the simple one is that when ordinary people are scared and have run from stocks, future returns tend to be higher (buy panic). ?When ordinary people are buying stocks with both hands, it is time to sell stocks to them, or even do IPOs to feed them catchy new overpriced stocks (sell greed).

The second intuitive way to view it is that it is analogous to Modiglani and Miller’s capital structure theory, where assets return the same regardless of how they are financed with equity and debt. ?When equity is a small component as?a percentage of market value, equities will return better than when it is a big component.

What it Means Now

Now, if you look at the graph at the top of my blog, which was estimated back in mid-March off of year-end data, you can notice a few?things:

The formula explains more than 90% of the variation in return over a ten-year period.

Back in March of 2009, it estimated returns of 16%/year over the next ten years.

Back in March of 1999, it estimated returns of -2%/year over the next ten years.

At present, it forecasts returns of 6%/year, bouncing back from an estimate of around 4.7% one year ago.

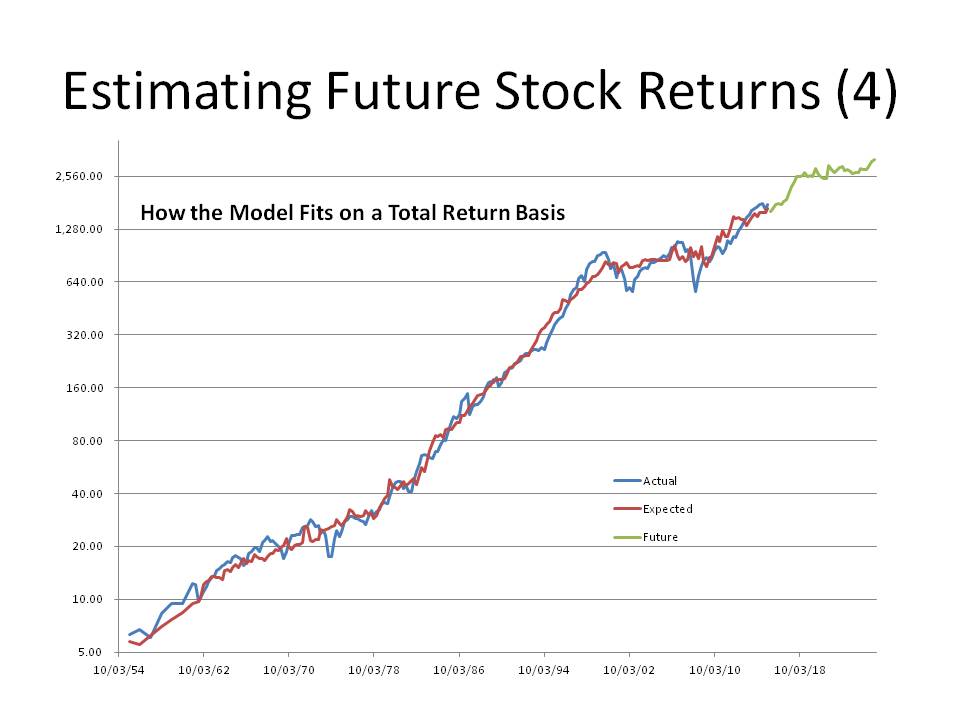

I have two more graphs to show on this. ?The first one below is showing the curve as I tried to fit it to the level of the S&P 500. ?You will note that it fits better at the end. ?The reason for that it is?not a total return index and so the difference going backward in time are the accumulated dividends. ?That said, I can make the statement that the S&P 500 should be near 3000 at the end of 2025, give or take several hundred points. ?You might say, “Wait, the graph looks higher than that.” ?You’re right, but I had to take out the anticipated dividends.

The next graph shows the fit using a homemade total return index. ?Note the close fit.

Implications

If total returns from stocks are only likely to be 6.1%/year (w/ dividends @ 2.2%) for the next 10 years, what does that do to:

Pension funding / Retirement

Variable annuities

Convertible bonds

Employee Stock Options

Anything that relies on the returns from stocks?

Defined benefit pension funds are expecting a lot higher returns out of stocks than 6%. ?Expect funding gaps to widen further unless contributions increase. ?Defined contributions face the same problem, at the time that the tail end of the Baby Boom needs returns. ?(Sorry, they *don’t* come when you need them.)

Variable annuities and high-load mutual funds take a big bite out of scant future returns — people will be disappointed with the returns. ?With convertible bonds, many will not go “into the money.” ?They will remain bonds, and not stock substitutes. ?Many employee stock options and stock ownership plan will deliver meager value unless the company is hot stuff.

The entire capital structure is consistent with low-ish?corporate bond yields, and low-ish volatility. ?It’s a low-yielding environment for capital almost everywhere. ?This is partially due to the machinations of the world’s central banks, which have tried to stimulate the economy by lowering rates, rather than letting recessions clear away low-yielding projects that are unworthy of the capital that they employ.

Reset Your Expectations and Save More

If you want more at retirement, you will have to set more aside. ?You could take a chance, and wait to see if the market will sell off, but valuations today are near the 70th percentile. ?That’s high, but not nosebleed high. ?If this measure got to levels 3%/year returns, I would hedge my positions, but that would imply the S&P 500 at around?2500. ?As for now, I continue my ordinary investing posture. ?If you want, you can do the same.

A defined benefit pension is a stream of payments that continues until the beneficiaries die, mainly. ?It is funded from the assets set aside?by the sponsor, and the earnings that flow from them, as well as additional contributions, should the assets not?be enough. ?With municipal pensions that means taxes.

Pension benefits are like debt, and sometimes more so. ?What I mean is this — pension benefits earned can’t be?reduced, except in bankruptcy. ?Many states give municipal pension payments preferential treatment, so troubled municipalities can’t compromise pension payments easily, even in bankruptcy, if allowed. ?(The main point of the third article is that underfunded pension plans in California will lead to taxes rising further, or, some sort of compromise, with a huge political fight either way.)

In principle, if defined benefit pensions had been funded properly, there wouldn’t be a lot of furor over them. ?From inception, funding rules were not conservative enough, particularly in what plans could assume they would earn off investments.

Thus the second article is no surprise. ?From my start in investment writing over 20 years ago, I predicted that more corporate pensions would get frozen, terminated, and replaced with defined contribution plans. ?Plans assumed too much in the way of investment earnings. Sponsors contributed too little, encouraged by the IRS, that wanted more tax revenue, and thus limited the amount sponsors could contribute.

Things could always be worse, though… many nations in Europe will undergo a lot of strain trying to pay all of the benefits that were promised. ?Here’s a quotation?from the first article:

?Western European governments are close to bankruptcy because of the pension time bomb,? said Roy Stockell, head of asset management at Ernst & Young. ?We have so many baby boomers moving into retirement [with] the expectation that the government will provide.?

Even the U.S., with a Social Security trust fund of $2.8 trillion, faces criticism for promising more than it can afford. That is because the fund?which is mostly in the form of IOUs from the Treasury?is projected to fall short of the sums needed to cover all benefits in a dozen years or so, and run out in 2035. Europe?s situation is much worse.

When taxes are already high, and because of demographics, the ratio of workers to pensioners is falling, it gets difficult to figure out what many European governments will do. ?It will be a political fight. ?Think Greece — but more widespread.

And from the article, one thing that all should expect is that older people will work to supplement their economic needs — the homey example was the lady raising berries to sell, and rabbits?for her personal consumption.

The fourth article had a lot of pension factoids:

New York is the worst state to retire in, by one survey. ?(But no state?is that well off.) ?Wyoming,?South Dakota, Colorado, Utah, and Virginia are supposedly?the five best states for retirement.

The odds for a woman of being in poverty after age 65 are high. ?Part of that is that women live longer. ?Also, the private pensions of most women are smaller. ?Another part is that joint pensions for the often higher-earning husband drop in amount paid after he dies. ?Two *do* live more cheaply than one, so that *is* a loss.

Most people think they won’t have as comfortable a retirement as their parents. (Probably true.)

Altogether, many are worried about retirement. ?That is a rational fear. ?I have older friends who have thought ahead, and retrained for lower-impact occupations. ?If you don’t have assets, you will probably end up working. ?Best to think about that sooner, rather than later. ?After all, many Americans get to age 65 with less than $100,000 saved. ?In this low interest rate environment, getting less than $4,000/year from your savings won’t do much to pad old age, but maybe working in a nice place could.

This isn’t the advice that many?want to hear, but for 75% of Americans reaching 65, it is realistic. ?Be grateful if you get to retire. ?Be more grateful if you don’t get bored.

In general, people don’t do well with amounts of money significantly larger than they are used to handling. ?The most obvious example of that is people who win lotteries. ?The money typically gets wasted — bad purchases, bad investments.

Thus I would encourage you to be very careful with any large distributions of money that you might receive. ?Examples include:

Life insurance settlements

Disability insurance settlements

Structured settlements arising from winning a court case over a tort against you.

Lotteries

Pension lump sums

Inheritances

Big paydays, if you are one of the rare ones in a high-paying short career like entertainment or sports

There are three problems with lump sums — receiving them, investing them, and rate of their use for consumption. ?Let me take these topics in the order that they should occur.

Receiving a Lump Sum

Let’s start with the cases where you have?a stream of payments coming where a third party comes to you and says that you can get all of the money now. ?I am speaking of structured settlements and inheritances where trusts have been structured to dole out the money slowly. ?There is one simple bit of advice here: don’t do it. ?Take the payments over time. ?None of the third parties offering to give you cash now are giving you a good deal, so avoid them.

Then there are the cases where an insurance company is making the payments from a disability claim, a structured settlement, a lottery, a pension buyout, or an annuity that someone bought for you on your life. ?The insurance company will be more fair than any third party, because they aren’t usually looking to make an obscene gain, just a big one, because it reduces their risk, and cleans up their balance sheet, so they can do more business. ?One simple bit of advice here: still don’t do it. ?You can do better by taking payments, and building up money for larger purchases. ?Be patient.

People do best when they receive money little by little. ?When they get money materially faster than the speed at which they have previously earned money, they tend to waste it. ?It is almost always better not to take a lump sum if you have the option to do otherwise.

The last set of situations is when the party that owes the set of payments?offers you a lump sum. ?It could be a life insurance company, a defined-benefit pension plan, a lottery, or some option uncommonly granted by another payor. ?I would still tell you not to do it, but the issue of getting cheated is reduced here for a variety of reasons.

The defined benefit plan has rates set by law at which it can cash you out, so they can’t hurt you badly. ?That said, you will likely not earn enough off of your investments with safety to equal the stream you are giving up. ?The lottery is often similarly constrained, but do your homework, and see what you are giving up.

One place to take the lump sum is with life insurance companies off of a death benefit. ?The rates at which they offer to pay an annuity to you are frequently not competitive, so take the lump sum and invest it wisely.

Economically, the key question to ask on a lump sum versus a stream of payments is what you would have to earn to replicate the stream of payments. ?Most of the time, the stream is worth more than the lump sum, so don’t take the lump sum.

The second question is more important. ?Can you be disciplined and not waste the lump sum? ?Ask those close to you what your money habits are like, if you don’t know for sure. ?Ask them to be brutally honest.

Investing the Lump Sum

Again, one nice thing about taking payments, is that you don’t have to invest the lump sum. ?If you do take the lump sum:

First, pay off high interest rate debts.

Second, avoid buying big things and calling them investments. ?Don’t buy a big house when you don’t need a big one.

Third, don’t invest in any of your relatives’ or friends’ business ventures. ?Tell them you try to keep personal affection and money separate. ?It avoids hurt feelings.

Fourth, look at the time horizon of your real needs. ?Plan for retirement, college, etc. ?Invest accordingly — get a trustworthy adviser who will help you. ?Trustworthiness is the most important factor here, with competence a close second.

Fifth, don’t so it yourself, unless you have developed the skill to do it previously. ?If you want to do it yourself, you will have to gauge whether the various markets are rich or cheap in order to decide where to invest. ?For some general, non-tailored advice, you can look at articles in my asset allocation category. ?As an aside, don’t invest in anything unusual unless you are an expert.

Receiving Spending?Money from Your Investment Fund

The first thing is to decide on a spending rule: many use a rule that says you can take 4% of the assets from the fund. ?My rule is a little more complex, but will keep you safer, and adapt to changing conditions: as a percentage of assets, take 1% more than the yield on the 10-year Treasury Note, or 7% if less. ?At present, that percentage would be 2.21% + 1% = 3.21%.

Whatever rule you use, be disciplined about your spending. ?Don’t bend your spending rule for any trivial reasons. ?Size your budget to reflect your income from your investment fund and all of your other income sources.

Conclusion

Remember that most people who get a lump sum end up wasting a lot of it. ?The only thing that can keep you from a similar fate would be discipline. ?If you don’t have discipline, don’t take a lump sum. ?Take the payments over time. ?That will give you the maximum benefit from what is a very valuable asset.