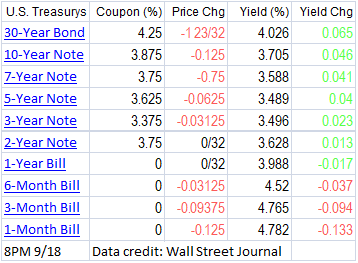

50 basis points of loosening was an upward surprise, so I take the steepening move in the yield curve as an expression that the market expects fewer cuts in the future, perhaps due to rising inflation, or just an unwillingness to lend more without additional compensation. I mean you two horrendously lousy presidential candidates making extreme promises to make the deficit even bigger. The GDP of the US grew faster when we ran balanced budgets — admittedly long ago. But fools think national credit is unlimited, and the grand enabler of that fantasy is the Federal Reserve.

Now, this just a day. Let ‘s watch what happens. The steepening could reverse, and even more so. But if this persists and goes further, you could see the Fed questioning whether they want to loosen more. Remember, the Fed is a slave to the bond market, not vice-versa.

Anyway, watch the slope of the yield curve. It tells you more about what is going on than the yammering of the Fed.

Photo Credit: Jason Woodhead || Forget the United States Oil Fund — if you want to own oil, buy a tank and store the oil on your own property. 😉

This should be a short post. Buffett likes to own T-bills when he doesn’t have anything that he wants to buy. Why? He is storing value until the time comes when he can buy something that he thinks offers a superb return over the long haul.

And now for something that seems completely different: commodity investing, when it was introduced in the nineties, offered “yield” from rolling the futures contracts from month-to-month. That ended when the trade got too crowded, and the “yield” went negative. The ETFs that pursued these strategies were inventory financing charities in disguise. They still are, even though their strategies are more complex than they were.

Think for a moment. Why should you earn a yield-type return off of owning a commodity? Really, that should not exist unless there is a scarcity of speculators willing to let producers hedge their risk with them. There is a speculative return, positive or negative, from holding a commodity, but in the present environment, where there is no lack of people willing to hold commodities, there is no yield-like return, unless it is negative.

As a result, commodities should be viewed as storage, not an investment. Do you think in the long run that gold will be more valuable than it is today? It might be wise to store some away. That said, you have to be careful here. In inflation-adjusted terms, most commodities have gotten cheaper over time, with occasional violent rallies that convince people to speculate (all too late).

Storage is not investing. Storage tucks something away, and it will not change, even if its price changes because of changes in the economy.

Investing is far less certain — you can lend to or buy equity in a venture which could produce astounding returns, or you could lose it all, or something in-between. With investing, it is rare that you will end up with what you started with.

This is not to say that storage is a bad thing — we exchange our savings in bank balances to store value in a different form. A bank could go bust. If enough go bust at the same time, value could be lost if the government does not back up the FDIC. Holding T-bills preserves value to the degree that the government is willing to pay on its own debts in fiat currency, which is pretty likely.

Holding a commodity with a price you think will correlate strongly with the prices you will experience in retirement is not a bad idea. That said, it is storage. It will not grow your purchasing power the way that investment will.

As such, I encourage you to mostly invest, and store a little. Storage is more certain, but has no return. Investing has returns, both positive and negative, but generally over time provides more value than storage.

PS — owning a home, except in a crowded area that is growing, is not an investment but is storage. You should not expect capital gains in real terms from owning a house. That said, it will provide you with rent-free living for a long time once the mortgage is paid off. (Please ignore the property taxes, insurance and maintenance costs.)

Photo Credit: Alane Golden || Sad but true — the crisis was all about bad monetary policy, a housing bubble, and poor bank risk management======================

1) The Federal Reserve and the People?s Bank of China

For different reasons, these two central banks kept interest rates too low, touching off a boom in risk assets in the USA.? The Fed kept interest rates too low for too long 2001-2004. The Fed explicitly wanted to juice the economy via the housing sector after the dot-com bust, and the withdrawal of liquidity post-Y2K.? Also, the slow, predictable way that they tightened rates did little to end speculation, because long rates did not rise, and in some cases even fell.

The Chinese Central Bank had a different agenda.? It wanted to keep the Yuan cheap to continue growing via exporting to the US.? In order to do that, it needed to buy US assets, typically US Treasuries, which balanced the books ? trading US bonds for Chinese goods ? and kept longer US interest rates lower.

Both of these supported the:

2) Housing Bubble

This is the place where there are many culprits.? You needed lower mortgage underwriting standards. This happened through many routes:

US policy pushing home ownership at all costs, including tax-deductibility of mortgage interest.

GSEs guaranteeing increasingly marginal loans, and buying lower-rated tranches of subprime RMBS. They ran on such a thin capital base that it was astounding.? Don?t forget the FHLBs as well.

Securitization of private loans separated origination from risk-bearing, allowing underwriting standards to deteriorate. Volume was rewarded, not quality.

Appraisers went along with the game, as did regulators, which could have stopped the banks from lowering credit standards. Part of the fault for the regulatory mess was due to the Bush Administration downplaying financial regulation.

Financial guarantors insured mortgage paper without having good models to understand the real risk.

People were stupid enough to borrow too much, assuming that somehow they would be able to handle it.? As with most bubbles, there were stupid writers pushing the idea that investing in housing was “free money.”

3) Bank Asset-liability management [ALM] for large commercial and investment banks was deeply flawed. ?It resulted in liquid liabilities funding illiquid assets.? The difference in liquidity was twofold: duration and credit.? As for duration, the assets purchased were longer than the bank?s funding structures.? Some of that was hidden in repo transactions, where long assets were financed overnight, and it was counted as a short-term asset, rather than a short-term loan collateralized by a long-term asset.

Also, portfolio margining was another weak spot, because as derivative positions moved against the banks, some banks did not have enough free assets to cover the demands for security on the loans extended.

As for credit, many of the assets were not easily saleable, because of the degree of research needed to understand them.? They may have possessed investment grade credit ratings, but that was not enough; it was impossible to tell if they were ?money good.?? Would the principal and interest eventually be paid in full?

The regulatory standards let the banks take too much credit risk, and ignored the possibility that short-term lending, like repos and portfolio margining could lead to a ?run on the bank.?

4) Accounting standards were not adequate to show the risks of repo lending, securitizations, or derivatives.? Auditors signed off on statements that they did not understand.

===============

That?s all, I wanted to keep this simple.? I do want to say that Money Market Funds were not a major cause of the crisis.? The reaction to the failure of Reserve Primary was overdone.? Because of how short the loans in money market funds are, the losses from money market funds as a whole would have been less than two cents on the dollar, and probably a lot smaller.

Also, bailing out the banks sent the wrong message, which will lead to more risk later.? No bailouts were needed.? Deposits were protected, and there is no reason to protect bank stock or bondholders.? As it was, the bailouts were the worst possible, protecting the assets of the rich, while not protecting the poor, who still needed to pay on their loans.? Better that the bailouts should have gone to reduce the principal of loans of those less-well-off, rather than protect the rich.? It is no surprise that we have the politics? we have today as a result.? Fairness is more important than aggregate prosperity.

PS — the worst of all worlds is where the government regulates and gives you the illusion of protecting you when it does not protect you much at all.? That tricks people into taking risks that they should not take, and leaves individuals to hold the bag when bad economic and regulatory policies fail.

Listening to the Fed Chair’s press conference, there was one thing where I disagreed with what Powell was saying.? He said a few times that they only made one decision at the FOMC meeting, that of raising the Fed Funds rate and the reverse repo rate by 0.25%.? They made another decision as well.?The decided to raise the rate of quantitative tightening [QT] by increasing the rate of Treasury, MBS and agency bonds rolloff by $10B/month starting in April. They did that by increasing the rate of reduction of MBS and agency bonds from $8B to $12B/month, and Treasuries from $12B to $18B/month. The total rate of QT goes from $20B to $30B/month.? This may raise rates on the longer end, because the Fed will no longer buy so much debt.

There was also a little concern over people overinterpreting the opinions of the Fed Governors, especially over the “dot plot,” which shows their opinions over real GDP growth, the unemployment rate, PCE inflation, and the Fed funds rate.? My point of view is simple.? If you don’t want people to misinterpret something, you need to defend it or remove it.

Personally, I think the FOMC invites trouble by doing the forecasts.? First, the Fed isn’t that good at forecasting — both the staff economists and the Fed Governors themselves.? Truly, few are good at it — people tend to either follow trends, or call for turns too soon.? Rare is the person that can pick the turning point.

Let me give you the charts for their predictions, starting with GDP:

The Fed Governors have raised their GDP estimates; they raised the estimates the most for 2018, then 2019, then 2020, but they did not raise them for the longer run.? I seems that they think that the existing stimulus, fiscal and monetary, will wear off, and then growth will return to 1.8%/year.? Note that even they don’t think that GDP will exceed 3%/year, and generally the Fed Governors are paid to be optimists.? Wonder if Trump notices this?

Then there is the unemployment rate.? This graph is the least controversial.? The short take is that?unemployment rate estimates by the Fed governors keep coming down, bottoming in 2019, and rising after that.

Then there is PCE Inflation.? Estimates by the Fed Governors are rising, and in 2019 and 2020 they exceed 2%.? In the long run the view of the Fed Governors is that they can achieve 2% PCE inflation.? Flying in the face of that is that they haven’t been able to do that for the duration of this experiment, so should we believe in their power to do so?

Finally, there is the Fed Funds forecast of the Fed Governors — the only variable they can actually control. Estimates rose a touch for 2018, more for 2019, more for 2020, and FELL for the long run. Are they thinking of overshooting on Fed Funds to reduce future inflation?

Monetary policy works with long and variable lags, as it is commonly said.? That is why I said, “Just Don?t Invert the Yield Curve.”? Powell was asked about inverting the yield curve at his press conference, and he hemmed and hawed over it, saying the evidence isn’t clear.? I will tell you now that if the Fed Funds rate follows that path, the Fed will blow something up, and then start to loosen again.? If they stop and wait when 10-year Treasury Note yields exceed 2-year yields by 0.25%, they might be able to do something amazing, where monetary policy hits the balancing point.? Then, just move Fed funds to keep the yield curve slope near that 0.25% slope.

There would be enough slope to allow prudent lending to go on, but not enough to go nuts.? Much better than the present policy that amplifies the booms and busts.? The banks would hate it initially, and regulators would have to watch for imprudent lending, because there would be no more easy money to be made.? Eventually the economy and banks would adjust to it, and monetary policy would become boring, but predictably good.

I thought this old post from RealMoney.com was lost, never to be found again.? This was the important post made on November 22, 2006 that forecast some of the troubles in the subprime residential mortgage backed securities market.? I favored the idea that there there would be a crash in residential housing prices, and the best way to play it would be to pick up the pieces after the crash, because of the difficulties of being able to be right on the timing of shorting could be problematic.? In that trade, too early would mean wrong if you had to lose out the trade because of margin issues.

With that, here is the article:

====================

I have tried to make the following topic simple, but what I am about to say is complex, because it deals with the derivative markets. It is doubly or triply complex, because this situation has many layers to unravel. I write about this for two reasons. First, since residential housing is a large part of the US economy, understanding what is going on beneath the surface of housing finance can be valuable. Second, anytime financial markets are highly levered, there is a higher probability that there could be a dislocation. When dislocations happen, it is unwise for investors to try to average down or up. Rather, the best strategy is to wait for the trend to overshoot, and take a contrary position.

There are a lot of players trotting out the bear case for residential housing and mortgages. I’m one of them, but I don’t want overstate my case, having commented a few weeks ago on derivatives in the home equity loan asset-backed securities market. This arcane-sounding market is no small potatoes; it actually comprises several billions of dollars’ worth of bets by aggressive hedge funds — the same type of big bettors who blew up so memorably earlier this year, Amaranth and Motherrock.

A shift of just 10% up or down in residential housing prices might touch off just such another cataclysm, so it’s worth understanding just how this “arcane-sounding” market works.

I said I might expand on that post, but the need for comment and explanation of this market just got more pressing: To my surprise, one of my Googlebots dragged in a Reuters article and a blog post on the topic. I’ve seen other writeups on this as well, notably in Grant’s Interest Rate Observer (a fine publication) and The Wall Street Journal.

How a Securitization Works (Basically)

It’s difficult to short residential housing directly, so a market has grown up around the asset-backed securities market, in which bulls and bears can make bets on the performance of home equity loans. How do they do this?

First, mortgage originators originate home equity loans, Alt-A loans and subprime loans. They bring these loans to Wall Street, where the originator sells the loans to an investment bank, which dumps the loans into a trust. The investment bank then sells participation interests (“certificates”) in the trust.

There are different classes of certificates that have varying degrees of credit risk. The riskier classes receive higher interest rates. Typically the originator holds the juniormost class, the equity, and funds an overcollateralization account to give some security to the next most junior class.

Principal payments get allocated to the seniormost class. Once a class gets its full share of principal paid (or cancelled), it receives no more payments. Interest gets allocated in order of seniority. If, after paying interest to all classes, there is excess interest, that excess gets allocated to the overcollateralization account, until the account is full — that is, has reached a value equal to the value of the second most junior class of trust certificates — and then the excess goes to the equity class. If there’s not enough interest to pay all classes, they get paid in order of seniority.

If there are loan losses from nonpayment of the mortgages or home equity loans, the losses get funded by the overcollateralization account. If the overcollateralization account gets exhausted, losses reduce the principal balances of the juniormost certificates — those usually held by the originator — until they get exhausted, and then the next most junior gets the losses. There’s a little more to it than this (the prospectuses are often a half-inch thick on thin paper), but this is basically how a securitization works.

From Hedging to Speculation

The top class of certificates gets rated AAA, and typically the lowest class before the equity gets rated BBB-, though sometimes junk-rated certificates get issued. Most of the speculation occurs in securities rated BBB+ to BBB-.

The second phase of this trade involves credit default swaps (CDS). A credit default swap is an agreement where one party agrees to make a payment to another party when a default takes place, in exchange for regular compensation until the agreement terminates or a default happens. This began with corporate bonds and loans, but now has expanded to mortgage- and asset-backed securities.

Unlike shorting stocks, where the amount of shorting is generally limited by the float of the common stock, there can be more credit default swaps than bonds and loans. What began as a market to allow for hedging has become a market to encourage speculation.

With CDS on corporate debt, it took eight years for the notional size (amount to pay if everyone defaulted) of the CDS market to become 4 times the size of the corporate bond market. With CDS on home equity asset-backed securities, it took less than 18 months to get to the same point.

The payment received for insuring the risk is loosely related to the credit spread on the debt that is protected. Given that the CDS can serve as a hedge for the debt, one might think that the two should be equal. There are a couple reasons that isn’t so.

First, when a default happens, the bond that is the cheapest to deliver gets delivered. That option helps to make CDS trade cheap relative to credit spreads. But a bigger factor is who wants to do the CDS trading more. Is it those who want to receive payment in a default, or those who want to pay when a default occurs?

How It Impacts Housing

With CDS on asset-backed securities, the party writing protection makes a payment when losses get allocated to the tranche in question. Most protection gets written on tranches rated BBB+ to BBB-.

This is where shorting residential housing comes into the picture. There is more interest in shorting the residential housing market through buying protection on BBB-rated home equity asset-backed securities than there are players wanting to take on that risk at the spreads offered in the asset-backed market at present. So, those who want to short the market through CDS asset-backed securities have to pay more to do the trade than those in the cash asset-backed securities market receive as a lending spread.

One final layer of complexity is that there are standardized indices (ABX) for home equity loan asset-backed securities. CDS exists not only for the individual asset-backed securities deals, but also on the ABX indices as well. Those not wanting to do the credit work on a specific deal can act on a general opinion by buying or selling protection on an ABX index as a whole. The indices go down in quality from AAA to BBB-, and aggregate similar tranches of the individual deals. Those buying protection receive pro-rata payments when losses get allocated to the tranches in their index.

So, who’s playing this game? On the side of falling housing prices and rising default rates are predominantly multi-strategy and mortgage debt hedge funds. They are paying the other side of the trade around 2.5% per year for each dollar of home equity asset-backed securities protection bought. (Deals typically last four years or so.) The market players receiving the 2.5% per year payment are typically hedge and other investment funds running collateralized debt obligations. They keep the equity piece, which further levers up their returns. They are fairly yield-hungry, so from what I’ve heard, they’re none too picky about the risks that they take down.

Who wins and who loses? This is tricky, but if residential real estate prices fall by more than 10%, the buyers of asset-backed securities protection will probably win. If less, the sellers of protection probably win. This may be a bit of a sideshow in our overly leveraged financial markets, but the bets being placed here exceed ten billion dollars of total exposure. Aggressive investors are on both sides of this trade. Only one set of them will end up happy.

But how can you win here? I believe the safest way for retail investors to make money here is to play the reaction, should a panic occur. If housing prices drop severely, and home equity loan defaults occur, and you hear of hedge fund failures resulting, don?t act immediately. Wait. Watch for momentum to bottom out, or at least slow, and then buy the equities of financially strong homebuilders and mortgage lenders, those that will certainly survive the downturn.

If housing prices rise in the short run (unlikely in my opinion), and you hear about the liquidations of bearish hedge funds, then the best way to make money is to wait. Wait and let the homebuilders and mortgage finance companies run up, and then when momentum fails, short a basket of the stocks with weak balance sheets.

Why play the bounce, rather than try to bet on the success of either side? The wait could be quite long before either side loses? Do you have enough wherewithal to stay in the trade? Most players don?t; that?s why I think that waiting for one side or the other to prevail is the right course. Because both sides are levered up, there will be an overshoot. Just be there when the momentum fails, and play the opposite side. Personally, I?ll be ready with a list of homebuilders and mortgage lenders with strong balance sheets. Though prospects are not bright today, the best will prosper once the crisis is past.

Ten years ago, things were mostly quiet. ?The crisis was staring us in the face, with a little more than a year before the effects of growing leverage and sloppy credit underwriting would hit in full. ?But when there is a boom, almost no one wants to spoil the party. ?Yes a few bears and financial writers may do so, but they get ignored by the broader media, the politicians, the regulators, the bulls, etc.

It’s not as if there weren’t some hints before this. ?There were losses from subprime mortgages at HSBC. ?New Century was bankrupt. ?Two hedge funds at Bear Stearns, filled with some of the worst exposures to CDOs and subprime lending were wiped out.

And, for those watching the subprime lending markets the losses had been rising since late 2006. ?I was following it for a firm that was considering doing the “big short” but could not figure out an effective way to do it in a way consistent with the culture and personnel of the firm. ?We had discussions with a number of investment banks, and it seemed obvious that those on the short side of the trade would eventually win. ?I even wrote an article on it at RealMoney in November 2006, but it is lost in the bowels of theStreet.com’s file system.

Some of the building blocks of the crisis were evident then:

European banks in search of any AAA-rated structured product bonds that had spreads over LIBOR. ?They were even engaged in a variety of leverage schemes including leveraged AAA CMBS, and CPDOs. ?When you don’t have to put up any capital against AAA assets, it is astounding the lengths that market players will go through to create and swallow such assets. ?The European bank yield hogs were a main facilitator of the crisis that was to come, followed by the investment banks, and bullish mortgage hedge funds. ?As Gary Gorton would later point out, real disasters happen when safe assets fail.

Regulators were unwilling to clamp down on bad underwriting, and they had the power to do so, but were unwilling, as banks could choose their regulators, and the Fed didn’t care, and may have actively inhibited scrutiny.

Not only were subprime loans low in credit quality, but they had a second embedded risk in them, as they had a reset date where the interest rate would rise dramatically, that made the loans far shorter than the houses that they financed, meaning that the loans would disproportionately default near their reset dates.

The illiquidity of the securitized Subprime Residential Mortgage ABS highlighted the slowness of pricing signals, as matrix pricing was slow to pick up the decay in value, given the sparseness of trades.

By August 2007, it was obvious that residential real estate prices were falling across the US. ?(I flagged the peak at RealMoney in October 2005, but this also is lost…)

Amid all of this, the “big short” was not a sure thing as those that entered into it had to feed the trade before it succeeded. ?For many, if the crisis had delayed one more year, many taking on the “big short” would have lost.

A variety of levered market-neutral equity hedge funds were running into trouble in August 2007 as they all pursued similar Value plus Momentum strategies, and as some fund liquidated, a self reinforcing panic ensued.

Fannie and Freddie were too levered, and could not survive a continued fall in housing prices. ?Same for AIG, and most investment banks.

Jumbo lending, Alt-A lending and traditional mortgage lending had the same problems as subprime, just in a smaller way — but there was so much more of them.

Oh, and don’t forget hidden leverage at the banks through ABCP conduits that were off balance sheet.

Dare we mention the Fed inverting the yield curve?

So by the time that BNP Paribas announced that three of their funds that bought?Subprime Residential Mortgage ABS had pricing issues, and briefly closed off redemptions, and Countrywide announced that it had to “shore up its funding,” there were many things in play that would eventually lead to the crisis that happened.

Some of us saw it in part, and hoped that things would be better. ?Fewer of us saw a lot of it, and took modest actions for protection. ?I was in that bucket; I never thought it would be as large as it turned out. ?Almost no one saw the whole thing coming, and those that did could not dream of the response of the central banks that would take much of the losses out of the pockets of savers, leaving bad lending institutions intact.

All in all, the crisis had a lot of red lights flashing in advance of its occurrence. ?Though many things have been repaired, there are a lot of people whose lives were practically ruined by their own greed, and the greed of others. ?It’s a sad story, but one that will hopefully make us more careful in the future when private leverage rises, creating an asset bubble.

But if I know mankind, the lesson will not be learned.

PS — this is what I wrote one decade ago. ?You can see what I knew at the time — a lot of the above, but could not see how bad it would be.

I was driving to a meeting of the Baltimore CFA Society, and listening to Bloomberg Radio, which was carrying President-Elect Trump’s Press Conference. I didn’t think too much about what I heard until Sheri Dillon talk about what was being done to eliminate conflicts of interest. Here is an excerpt:

Some have asked questions. Why not divest? Why not just sell everything? Form of blind trust. And I?d like to turn to addressing some of those questions now.

Selling, first and foremost, would not eliminate possibilities of conflicts of interest. In fact, it would exacerbate them. The Trump brand is key to the value of the Trump Organization?s assets. If President-elect Trump sold his brand, he would be entitled to royalties for the use of it, and this would result in the trust retaining an interest in the brand without the ability to assure that it does not exploit the office of the presidency.

[snip]

Some people have suggested that the Trump ? that President-elect Trump could bundle the assets and turn the Trump Organization into a public company. Anyone who has ever gone through this extraordinarily cumbersome and complicated process knows that it is a non-starter. It is not realistic and it would be inappropriate for the Trump Organization.

It went on from there, but I choked on the last paragraph that I quoted above. (Credit: New York Times, not all accounts carried the remarks of Ms. Dillon, a prominent attorney with the firm Morgan Lewis who structured the agreements for Trump) ?As I said before:

Trump to Outline Plans for ?Leaving My Great Business? Dec. 15 https://t.co/iIwweP2LcN Time to IPO and sell off the Trump Organization $$

An IPO of the Trump Organization was?realistic. ?I’m not saying it could have been done by the inauguration, but certainly by the end of 2017, and likely a lot earlier. ?I’ve seen insurance companies go through IPO processes that took a matter of months, a few because they had to sell the company to raise liquidity quickly for some reason.

In an IPO, Trump, all of Trump’s children and anyone else with an equity interest would have gotten their proportionate share of the new public company. ?Trump could have provided a lot of shares for the IPO, and instructed the trustee for his assets to sell it off?the remainder over the next year or so.

While difficult, this would not have been impossible or imprudent. ?Trump?might lose some value in the process, but hey, that should be part of the cost for a very wealthy man who becomes President of the US. ?There would be the countervailing advantage that all capital gains are eliminated, and who knows, that might settle his existing negotiations with the IRS.

Ending the counterfactual, though conflict of interest rules don’t apply to the President, Trump had?an opportunity to eliminate all conflicts of interest, and did not take it.

PS — Many major hotels are in the “name licensing” business — I also don’t buy the argument that Trump could not sell off the organization in entire, with no future payments for the rights of using the name. ?A bright businessman could create a new brand easily. ?It’s been done before.

How would you like a really good model to make money as a money manager? You would? Great!

What I am going to describe is a competitive business, so you probably won’t grow like mad, but what money you do bring in the door, you will likely keep for some time, and earn significant fees.

This post is inspired by a piece written by Jason Zweig at the Wall Street Journal:?The Trendiest Investment on Wall Street?That Nobody Knows About. ?The article talks about interval funds. ?Interval funds hold illiquid investments that would be difficult to sell at a fair price ?quickly. ?As such, liquidity is limited to quarterly or annual limits, and investors line up for distributions. ?If you are the only one to ask for a distribution, you might get a lot paid out, perhaps even paid out in full. ?If everyone asked for a part of the distribution, everyone would get paid their pro-rata share.

But there are other ways to capture assets, and as a result, fees.

Various types of business partnerships, including Private REITs, Real Estate Partnerships, etc.

Illiquid?debts, such as structured notes

Variable, Indexed and Fixed Annuities with looong surrender charge periods.

Life insurance as an investment

Weird kinds of IRAs that you can only set up with a venturesome custodian

Odd mutual funds that limit withdrawals because they offer “guarantees” of a sort.

And more, but I am talking about those that get sold to or done by retail investors… institutional investors have even more chances to tie up their money for moderate, modest or negative incremental returns.

(One more aside, Closed end funds are a great way for managers to get a captive pool of assets, but individual investors at least get the ability to gain liquidity subject to the changing premium/discount versus NAV.)

My main point is short and simple. ?Be wary of surrendering liquidity. ?If you can’t clearly identify what you are gaining from giving up liquidity, don’t make the investment. ?You are likely being hoodwinked.

It’s that simple.

[bctt tweet=”If you can’t clearly identify what you are gaining from giving up liquidity, don’t make the investment.” username=”alephblog”]

Photo Credit: Daniel Mennerich || A bridge described in fiction to bridge me to the counterfactual argument of this post

==============================

I received an email from a longtime reader:

David, here is a (possibly useless) thought experiment.

In 2005, PIMCO’s Paul McCulley was begging Ben Bernanke to halt the on- going quarter-point raises in the Fed Funds rate at 3.5 percent. I forget his exact reasoning, but he clearly thought that the financial markets couldnot accommodate short-term rates above 3.5 percent without substantial disruptions.

Suppose that Bernanke had listened to McCulley and capped the Fed Funds rate at 3.5 percent until it was clear how the markets would fare at that level. Would that alone have been sufficient to postpone or even avert the housing crisis? Or would it have made the crash even worse?

According to FRED, the Funds rate reached 3.5 percent in August 2005, and as we know housing prices nationally peaked about one year later, just as the Funds rate was topping out at 5.25 percent. Question is, did the additional 1.75 percent of increases serve to tip the housing market into decline, or was the collapse inevitable with or without the last seven quarter-point raises?

Any thoughts?

Here was my response:

I proposed the same thing at RealMoney, except I think I said 4%.? My idea was to stop at a yield curve with a modestly positive slope.? It might have postponed the crisis, and maaaaybe allowed banks and GSEs to slowly eat up all of the bad loan underwriting.

I had Googlebots tracking housing activity daily, and August 2015 was when sales activity peaked.? I announced it tentatively at RealMoney, and confirmed it two months later.? From data I was tracking, housing prices flatlined and started heading down in 2006.? The damage was probably done by 2005 — maybe the right level for Fed funds would have been 3%.

The trouble is, hedge funds and other entities were taking risk every which way, and a mindset had overwhelmed the markets such that we had the correlation crisis in May 2005, and other bits of bizarre behavior.? Things would have blown up eventually.? Speculative frenzy rarely cools down without the bear phase of the credit cycle showing up.

So, much as it would have been worth a try, it probably wouldn’t have worked.? The housing stock was already overvalued and overleveraged.? But it might have taken longer to pop, and it might not have been as severe.

But now for the fun question.? Is the Fed trying to do something like that now?? Are they so afraid of popping any sort of asset bubble that they have to be extra ginger in raising rates?? It seems any market “burp” takes rate rises off the table for a few months.

I don’t know.? I do know that the FOMC has only 1% of tightening to play with before the yield curve gets flat.? Also, obvious speculation is limited right now.? There is a lot that is overvalued, but there is no frenzy… unless you want to call nonfinancial corporation and government borrowing a frenzy.

Thanks for writing.

=============================================

The FOMC is Afraid of its own Shadow

If I were the Fed, I would end the useless jabbering that they do. ?I would also end the quarterly forecasts and press conference. I would also end publishing the statement and the minutes, and let people read the transcripts five years later. We would go back to the pre-Greenspan years, when monetary policy was managed better. ? Before I did that I would say:

The Fed has three responsibilities: controlling inflation, promoting full employment, and regulating the solvency of the banking system. ?We are not responsible for the health and well-being of financial markets. ?The ‘Greenspan Put’ is ended.

We will act to limit speculation within the banks, such that market volatility will have minimal impact on them. ?We want our pursuit of limited inflation and full employment to not be hindered by looking over our shoulder at the boogeyman that could affect the banking system. ?To that end, please realize that we will not care if significant entities lose money, including countries that may get whipped around by our pursuit of monetary policy in a way that benefits the American people.

We are not here as guarantors of prosperity for speculators. ?Really, we’re not here to guarantee anything except pursue a stable-ish price level, and to the weak extent that monetary policy can do so, aid full employment.

We hope you understand this. ?We do not intend to use our “lender of last resort” authority again, and will manage bank solvency in a way to avoid this. ?We may get called ‘spoilsports’ by the banks that we regulate, but in the end we are best served as a nation if solvency concerns dominate over the profitability of the banking industry.

As it is, the present FOMC fears acting because it might derail the recovery or spark a bear market in risky assets. ?Going beyond the mandate of the Fed has led to bad results in the past. ?It will continue to do so in the future.

The best way for the Fed to maintain its independence is to act independently and responsibly. ?Don’t listen to outside influences, particularly when hard things need to be done. ?Be the adult in the room, and tell the children that the medicine that you give them is for their good. ?Recessions are good, because they clear away bad uses of capital from the ecosystem, and make room for new more productive ideas to use the capital instead.

As it is, the Fed is afraid of its own shadow, and will not take any hard actions. ?That will either end with inflation, or an asset bubble that eventually affects the banks. ?A central bank like that does not follow its mandate does not deserve its independence. ?So Fed, if you won’t act for our long-term good, will you act to preserve your existence in your?present form?

When I was 29, nearly half a life ago, Donald Trump was a struggling real estate developer. ?In 1990, I was still trying to develop my own views of the economy and finance. ?But one day heading home from work at AIG, I was listening to the business report on the radio, and I heard the announcer say that Donald Trump had said that he would be “the king of cash.” ?My tart comment was, “Yeah, right.”

At that point in time, I knew that a lot of different entities were in need of financing. ?Though the stock market had come back from the panic of 1987, many entities had overborrowed to buy commercial real estate. ?The major insurance companies of that period were deeply at fault in this as well, largely driven by the need to issue 5-year Guaranteed Investment Contracts [GICs] to rapidly growing stable value funds of defined contribution plans. ?Outside of some curmudgeons in commercial mortgage lending departments, few recognized that writing 5-year mortgages with low principal amortization rates against long-lived commercial properties was a recipe for disaster. ?This was especially true as lending yield spreads grew tighter and tighter.

(Aside: the real estate area of Provident Mutual avoided most of the troubles, as they sold their building that they built seven years earlier for twice what they paid to a larger competitor. ?They also focused their mortgage lending on small, ugly, economically necessary properties, and not large trophy properties. ?They were unsung heroes of the company, and their reward was elimination eight years later as a “cost saving move.” ?At a later point in time, I talked with the lending group at Stancorp, which had a similar philosophy, and expressed admiration for the commercial mortgage group at Provident Mutual… Stancorp saw the strength in the idea, and still follows it today as the subsidiary of a Japanese firm. ?But I digress…)

Many of the insurance companies making the marginal commercial mortgage loans had come to AIG seeking emergency financing. ?My boss at AIG got wind of the fact that I was looking elsewhere for work, and subtly regaled me of the tales of woe at many of the insurance companies with these lending issues, including one at which I had recently interviewed. ? ?(That was too coincidental for me not to note, particularly as a colleague in another division asked me how the search was going. ?All this from one stray comment to an actuary I met coming back from the interview…)

Back to the main topic: good investing and business rely on the concept of a margin of safety. ?There will be problems in any business plan. ?Who has enough wherewithal to overcome those challenges? ?Plans where everything has to go right in order to succeed will most likely fail.

With Trump back in 1990, the goal was admirable — become liquid in order to purchase properties that were now at bargain prices. ?As was said in the Wall Street Journal back in April of 1990, the article started:

In a two-hour interview, Mr. Trump explained that he is raising cash today so he can scoop up bargains in a year or two, after the real estate market shakes out. Such an approach worked for him a decade ago when he bet big that New York City’s economy would rebound, and developed the Trump Tower, Grand Hyatt and other projects.

“What I want to do is go and bargain hunt,” he said. “I want to be king of cash.”

That’s where?Trump said it first. ?After that he received many questions from reporters and creditors, because his businesses were heavily indebted, and?property values were deflated, including the properties that he owned. ?Who wouldn’t want to be the “king of cash” then? ?But to be in that position would mean having sold something when times were good, then sitting on the cash. ?Not only is that not in Trump’s nature, it is not in the nature of most to do that. ?During good times, the extra cash that Buffett keeps on hand looks stupid.

Trump did not get out of the mess by raising cash, but by working out a deal with his creditors in bankruptcy. ?Give Trump credit, he had convinced most of his creditors that they were better off continuing to finance him rather than foreclose, because the Trump name made the properties more valuable. ?Had the creditors called his bluff, Trump?would have lost a lot, possibly to the point where we wouldn’t be hearing much about him today.

Trump escaped, but most other debtors don’t get the same treatment Trump did. ?The only way to survive in a credit crunch is plan ahead by getting adequate long-term financing (equity and long-term debt), and keep a “war kitty” of cash on the side.

During 2002, I had the chance to test this as a bond manager. ?With the accounting disasters at mid-year, on July 27th, two of my best brokers called me and said, ?The market is offered without bid.? We?ve never seen it this bad.? What do you want to do??? I kept a supply of liquidity on hand for situations like this, so with the S&P falling, and the VIX over 50, I put out a series of lowball bids for BBB assets that our analysts liked.? By noon, I had used up all of my liquidity, but the market was turning.? On October 9th, the same thing happened, but this time I had a larger war chest, and made more bids, with largely the same result.

That’s tough to do, and my client pushed me on the “extra cash sitting around.” ?After all, times are good, there is business to be done, and we could use the additional interest to make the estimates next quarter.

To give another example, we have the visionary businessman Elon Musk facing a?cash crunch?at Tesla?and?SolarCity. ?Leave aside for a moment his efforts to merge the two firms when stockholders tend to prefer “pure play” firms to conglomerates — it’s interesting to look at how two “growth companies” are facing a challenge raising funds at a time when the stock market is near all time highs.

Both Tesla and Solar City are needy companies when it comes to financing. ?They need a lot of capital to grow their operations before the day comes when they are both profitable and cash flow from operations is positive. ?But, so did a lot of dot-com companies in 1998-2000, of which a small number exist to this day. ?Elon Musk is in a better position in that presently he can dilute?issue shares of Tesla to finance matters, as well as buy 80% of the Solar City bond issue. ?But it feels weird to have to finance something in less than a public way.

There are other calls on cash in the markets today — many companies are increasing dividends and buying back stock. ?Some are using debt to facilitate this. ?I look at the major oil companies and they all seem to be levering up, which is unusual given the recent trajectory of crude oil prices.

We are in the fourth phase of the credit cycle now — borrowing is growing, and profits aren’t. ?There’s no rule that says we have to go through a bear market in credit before that happens, but that is the ordinary?way that excesses get purged.

That is why I am telling you to pull back on risk, and review your portfolio for companies that need financing in the next three years or they will croak. ?If they don’t self finance, be wary. ?When things are bad only cash flow can validate an asset, not hopes of future growth.

With that, I close this article with a poem that I saw as a graduate student outside the door of the professor for whom I was a teaching assistant when I first came to UC-Davis. ?I did not know that is was out on the web until today. ?It deserves to be a classic:

Once upon a midnight dreary as I pondered weak and weary

Over many a quaint and curious volume of accounting lore,

Seeking gimmicks (without scruple) to squeeze through

Some new tax loophole,

Suddenly I heard a knock upon my door,

Only this, and nothing more.

Then I felt a queasy tingling and I heard the cash a-jingling

As a fearsome banker entered whom I?d often seen before.

His face was money-green and in his eyes there could be seen

Dollar-signs that seemed to glitter as he reckoned up the score.

?Cash flow,? the banker said, and nothing more.

I had always thought it fine to show a jet black bottom line.

But the banker sounded a resounding, ?No.

Your receivables are high, mounting upward toward the sky;

Write-offs loom.? What matters is cash flow.?

He repeated, ?Watch cash flow.?

Then I tried to tell the story of our lovely inventory

Which, though large, is full of most delightful stuff.

But the banker saw its growth, and with a might oath

He waved his arms and shouted, ?Stop!? Enough!

Pay the interest, and don?t give me any guff!?

Next I looked for noncash items which could add ad infinitum

To replace the ever-outward flow of cash,

But to keep my statement black I?d held depreciation back,

And my banker said that I?d done something rash.

He quivered, and his teeth began to gnash.

When I asked him for a loan, he responded, with a groan,

That the interest rate would be just prime plus eight,

And to guarantee my purity he?d insist on some security?

All my assets plus the scalp upon my pate.

Only this, a standard rate.

Though my bottom line is black, I am flat upon my back,

My cash flows out and customers pay slow.

The growth of my receivables is almost unbelievable:

The result is certain?unremitting woe!

And I hear the banker utter an ominous low mutter,

?Watch cash flow.?

Herbert S. Bailey, Jr.

Source: ?The January 13, 1975, issue of Publishers Weekly, Published by R. R. Bowker, a Xerox company.? Copyright 1975 by the Xerox Corporation. ?Credit also to?aridni.com.