Image Credit: born1945 || When I was a boy, I spent many days caddying at the local country club.

(This is one of my occasional experiments. Bear with me if you will…)

==========================

Wagner: I don’t get the thrill.

Hawker: What’s not to like?

W: This is nothing like the investment memorandum said it would be.

H: It’s a work in progress. Don’t look at what it is now, think of what it will be like when everyone clamors to join us.

W: This is just a field.

H: So?

W: When I bought a small share in the ownership of this club, the memorandum had pictures of the golf course, lodge, tennis courts, bar, swimming pool, pro shop, and more. All that is here is this field.

H: You needed to read the memorandum more closely. One day we will have all that and more. As for now, we promote the potential of this place to the masses who will want to join us at a much higher price than we got in at.

W: So when will it be built?

H: That is a matter of secondary importance.

W: Huh? What’s of primary importance?

H: Encouraging others to buy shares in this, and never selling our interests.

W: Wait. You did not buy this so you could golf?

H: No merely to own, and never to sell.

W: So this is a speculation on this land?

H: Don’t say speculation! Bad word! This is an investment in the concept of getting something valuable in the future. Besides, the country club doesn’t technically own this field yet… there is a memorandum of understanding to acquire it once the price of ownership interests get high enough… at that point we will swap newly issued shares for the land. We transact everything in shares; it is our currency.

W: It doesn’t own this field? What does it own?

H: The future. Everyone is going to want to buy a share in this wondrous venture, and at progressively higher prices. Congratulate yourself, you got in on the ground floor.

W: There is no floor here! Where has the money gone that I have paid?

H: An earlier investor sold you some of his interests. Don’t worry, he still owns over 25% of the shares. Purely a portfolio management decision for him. The Founder strongly believes in the vision for this concept.

W: The concept of building a country club?

H: The concept of selling interests in the club at ever higher prices to the masses who will want an appreciating asset. And we have the track record. Prices of ownership interests have continually gone up. On a mark-to-market basis, the returns exceed 20%/year. How is that for a successful investment?!

W: I can understand the concept of buying rare and beautiful art to hang on the wall of my house as an investment. It might appreciate over time or not. I enjoy looking at it, and my friends as well, while I pay insurance premiums to protect it for my heirs. Is the only value of this investment possible monetary gain? At least will there be dividends paid?

H: You are missing the point. With this, your heirs will have something far more valuable than a stream of dividends. They will own a share in something that everyone wants to buy. Everyone wants to own an investment that only goes up.

W: So the only driver of value here is others envying what we have, and wanting to buy it from us at prices higher than what we paid?

H: Envy is an ugly word, but yes, and that is why we continually promote how wonderful this investment will be.

W: I am disappointed. I really wanted to golf. Hmm… what if I sold my interests and used the money to go golfing, whether I buy another country club membership, or just hit the links at the local public course?

H: And I am astounded. Why would you give up the glorious future of this enterprise?

W: I want to golf. Say, if you are so convinced, would you buy my interests from me at 5% more than I paid for them?

H: Well, I would be a “better buyer” at that price, but I don’t have enough cash to do that.

W: Would the Founder be interested?

H: The Founder continues to acquire ownership interests as a result of his labors as management. That is how he gets paid. As far as I have heard, he graciously sells them to those who want a piece of the action.

W: Uh-huh. At this point I would rather golf. I will sell my interests to the best bidder.

H: I thought better of you than that. Giving up on an astounding future just to play a game?

The operation of the “bull pool” at wallstreetbets resembles a Ponzi scheme. There are five things that make it different:

It is decentralized.

Because it is decentralized, there is no single party that controls it and rakes off some of the money for himself, at least not directly.

The assets can be freely sold in a somewhat liquid, but chaotic market. Most Ponzi schemes have time barriers for redemption.

They caught a situation where shorting was so rampant, that triggering a squeeze was easy. Situations where the shorts are so crowded are rare.

Gamestop [GME] and other companies whose stock prices get manipulated above their intrinsic value can take the opportunity to sell more shares, as can less than 10% holders of the holders of the stock, and even the greater than 10% holders once six months have passed since their last purchase.

You have to give wallstreetbets credit for one thing, and only one thing: wiping out the shorts. It was an incredibly crowded short, and they identified an easy squeeze. But now it is harder to short, margin requirements have been tightened for both longs and shorts, given the market volatility, and even more so for options. That not only applies to individuals but to brokerages, because with the volatility, there is a greater probability of settlement failure, and broker failure. Robinhood faced possible failure and raised capital. What shorts remain are better financed than previously. When volatility goes up, so must the capital of intermediaries, including brokerages.

Ponzi schemes typically need ever-increasing flows of money to satisfy the cash need from the money being raked off. But there is no sponsor here, so what plays the role of the rake? I can think of three rakes for the money:

Some companies like AMC Entertainment and American Airlines are issuing new shares to take advantage of the artificially high price. Maybe GME will do it next week.

And, those who are more intelligent at wallstreetbets know that GME is overvalued, and have booked their gains. This is definitely a place where the old Wall Street maxim applies: “Can’t go broke taking a profit.” or “Bulls can make money, Bears can make money, but Hogs get slaughtered.” (The Hogs in this situation are the ones who buy and hold GME. Buy-and-hold only works for undervalued assets.)

Now, the grand change that has happened in the last two months is that the investor base of GME has shifted from being fundamental investors to momentum investors. There may be more institutional money pushing GME than is commonly understood. That said, institutional momentum longs tend to react quickly and sell when momentum fails, which makes matters even more volatile. They have more of a risk control discipline than na�ve retail investors do.

This is similar to what happens with promoted penny stocks. Fundamentals seem not to matter, just the amount of money thrown at the stock. There is the pump; there is the dump. The amounts of money are bigger here. We have only seen the pump. The dump is coming. And penny stocks almost always lose.

There is no magic in markets — stock prices eventually revert to intrinsic value — it is only a question of how and when. Buyers can force a stock price above intrinsic value for a little while, but eventually the price will sag back, and the only winners will be those who sold stock to them.

When I was younger, I made a mistake with a microcap stock, and placed a market order to initiate a position. (Accident: I typically only use limit orders.) The stock was so thinly traded that I got filled at levels an average of 50% above where the bid was. The price promptly fell back to where it was prior to my purchase.� This is what will likely happen with GME, and other situations like it. Mere trading can’t permanently raise the price of an asset.

One last note: those at wallstreetbets and places life it should be careful. If you are communicating with other investors about a stock and you make money as a result of the communication, you may face legal troubles if that is deemed market manipulation. And, given that you have communicated it over the internet, that could be deemed “wire fraud.” This is the nature of a government with vague laws that likes to say “gotcha” when they deem something unsavory as illegal.

Do I think it should be illegal? No. Is it unethical? Certainly. No one should promote anything like a Ponzi scheme. But in US culture now, unethical and illegal get confused, and the ideas of “mail fraud,” “wire fraud,” etc., can be applied to unethical actions that may not strictly be illegal. Such logic has been applied to promoted penny stocks, with significant wins against the promoters.

So, to those at wallstreetbets, I would say that you are living on borrowed time. This isn’t going to work, and you and those that follow you will lose money, whether the government comes after you or not. Just as the Hunts tried to corner the silver market, and failed miserably as people sold their silver sets, and miners mined like crazy, in the same way pushing stock prices too high will only lead to dilution from the corporations, and losses to the buyers who came in late., if not the early ones as well.

Before I start writing this evening, I want to say that what I write here is correct in its major findings, but it is quite possible that I got some details wrong. This is complex, and there are a lot of issues involved.

I’ve had four friends ask me about GameStop [GME] over the last few days. Thus I am writing an explanation as to why things are so nuts here.

As a prelude, I want to tell everyone that I have no positions at present in GME, and have no intentions of taking a position in it ever. Mid-decade, I owned GME and lost a little bit on it. I came to the correct conclusion that their business model no longer worked before most of the market gave up on it. If anything, the business model is worse now than when I sold. I think the true value of GME is about $5/share, unless management does something clever with its overvalued stock. Fortunately, I have written a really neat article called How do you Manage a Company when the Stock is Considerably Overvalued? I’ll talk about this more toward the end of this piece.

One more note: I never short because it is very hard to control risk when shorting. When you are short, or levered long, you no longer control your trade in full, and an adverse price move could force you to buy or sell when you don’t want to.

I can imagine working at the hedge fund, and my boss says to me, “What should I do about GME?” My initial answer would be “Nothing, it’s too volatile.” If pressed, I would say, “Gun to the head, it is a short, if you can source the shares, and live with the possibility of being forced by the margin desk to put more capital.”

Now you know my opinion. Let me explain the technicals and the fundamentals here.

The Voting Machine

Ben Graham used to say that the stock market was a voting machine in the short-run, and a weighing machine in the long-run. In a mania, you can get a lot of people chasing the shares of a speculative company like GME, and in the short run, the aggressiveness of the buyers lifting the ask and buying call options can drive the stock higher.

With GME, there is another complicating factor — there are more shares shorted than there are shares issued. This means that some brokerages have been allowing “naked shorting,” i.e., allowing traders to sell short without borrowing shares. This is illegal, and I wouldn’t be surprised to see the SEC pursue a case against some brokers as a result.

When there are a lot of short sellers in a given stock, if buyers can get the price to rise, it can create a temporarily self-reinforcing cycle as shorts are forced by their brokers to put up more capital, or buy in their short position. This is called a “short squeeze.” I’m pretty certain that has been happening with GME.

Now, beyond that there are several other factors:

Longs that are locked because of large positions

Use of call options to magnify gains (and maybe losses)

Co-ordinated buying by small traders.

Possible use of total return swaps

Moving shares to the cash account

I’ll handle these in the above order. There are three entities that own more than 10% of GME. Blackrock, Fidelity, and RC Ventures (the investment vehicle of Ryan Cohen, CEO of Chewy.com). Once you own more than 10% of a company, you can’t sell shares until six months have passed since your last purchase. If you purchase more, you must notify the market within two days. If you finally get to the point where you can sell, you can’t buy again for six months, and if you sell you must notify the market within two days.

RC Ventures, which now has three board seats on the GME board, can’t sell GME shares until mid-June, as they bought their last shares in December. I have no idea when Blackrock and Fidelity last bought GME shares but it six months have passed, I would be bombing the market with shares. Since I haven’t seen a filing by either one, I assume they can’t do it for now.

With call options, when a call is sold, the writer of the option must either:

Bear the risk in full

Buy other call options to hedge, and/or

Buy GME stock to hedge, with the risk that you will have to buy more if the stock goes higher, or sell if the stock goes lower.

Buying call options is a leveraged strategy — you can win or lose a lot — usually it is lose. On net, the market is not affected much — for every buyer there is a seller, and derivative positions like calls net to zero. The only time when that is not true is when prices move so fast that margin desks can’t keep up. At that point, brokers take rare losses.

Co-ordinated trading by small traders, perhaps influenced by wallstreetbets at Reddit is something new-ish, though it is reminiscent of the bull pools that existed in the early 20th century. The main difference is that it is a lot of little guys versus a few big guys. Regulations today call a few big guys trying to manipulate the price of a stock “market manipulation,” which is illegal. That does not apply to little guys talking to each other, most likely.

But there is a greater problem here. Even if you are participating with wallstreetbets, how do you know when others will sell to lock in profits.? It’s not as if anyone is looking at the likely flow of future dividends. The dividend has been suspended. Eventually the willingness of the “bull pools” to extend more liquidity will run out. Then there will be a run for the exits — this is a confidence game. Don’t be a bagholder.

With respect to total return swaps, it is the same issue as call or put options. Someone has to take the other side of the trade, and either bear the risk or hedge the risk. There usually should be no net effect.

Finally, there is moving GME shares to the cash account, which means those shares can’t be borrowed in order to short them. There are two points here:

There is already illegal naked shorting going on here, so moving shares to the cash account may not do much.

If you are a monomaniac, and are pursuing only GME, you might decide to lever your position via margin. At that point it is not possible to move shares to the cash account.

That takes care of the technicals, now on to the fundamentals.

The Weighing Machine

The fundamentals of GME are lousy. How many of you know their debt ratings? I see one guy in the back raising his hand at half mast. Well, let me tell you that GME has two bonds outstanding:

$216+ million of a secured first-lien note rated B2/B- maturing in 2023 with a 10% coupon trading in the mid-$103 area for a mid-6% yield-to-worst, which GME can’t likely call.

$73+ million of an 6.75% unsecured note rated Caa1/CCC+ maturing in less than two months with a mid-5% yield.

Both of these notes are trading above par, but they still trade as junk. If it were not from the interest of RC Ventures they would trade a lot lower. They did trade much lower before RC Ventures bought their stake — yields for the unsecured debt exceeded 40% annualized.

This is a troubled company that would be teetering on the brink of bankruptcy were it not for the efforts of RC Ventures. As such, I would say that the value of GME is at most the price that RC Ventures is willing to pay for it, and that amount is uncertain. (Did I mention that they are losing money regularly?)

And to the bulls I would add, don’t discount the possibility of a trading suspension where you can’t get out of your positions. I can tell you that if that happens the price of GME will be a LOT lower when trading resumes.

What is not “Advice”

Here is my non-advice for everyone.

For those that own GME, sell now. I said NOW, you waited ten seconds.

For those that are short GME, hold your short to the degree that you can.

To the management of GME, do a PIPE, sell a convertible bond or preferred stock. Buy another company in a stock swap. Do anything you can to monetize the idiocy of the bull pool at wallstreetbets. They are offering you a free lunch. Hey, and as an added incentive, RC Ventures can’t sell right now, but you can. Every bit of monetization that you do will benefit RC Ventures to a degree, and dilute them as well (a plus!).

Take the dopes at wallstreetbets to the cleaners, and show them the power of the primary market as you dilute them. Oh, and while you have the opportunity, pay off your bonds, or at least set the money aside in escrow to redeem them at the call date. That is the rescue strategy for GME: sell stock to the losers who have foolishly bid the price up, and use it to rebuild you business. Even RC Ventures may thank you.

23 trading days from bull market peak to bear market bottom. 12 trading days from bear market bottom to the start of the new bull market. Both are records.

As I have often said. �Weird begets weird.� When things are weird, it may not be prudent to rely on prior statistical measures. It might be better to think about the structural economy and try to reason about what is going on.

As for me, I am tracking the leading cause of the weirdness � COVID-19, and trying to get a grasp on when the new cases will be minimal.

Things are going better than the politicians are saying. That is why the market has been rallying.

It may take 6-12 months for the economy to return to normal, assuming that the government does its job well with respect to its restrictions.

All that said, it will be volatile. After all,one thing that is utterly new is that the economy would be voluntarily shut down. There were better ways to do this, and there will be many arguments as the actions of governments are debated after this crisis.

PIcture credit: Aleph Blog, and the same for all the graphs and charts in this post. All liability for mistakes here is mine.

Since then I never pay attention to anything by “experts”. I calculate everything myself.

Dr. Richard Feynman, Part 5: “The World of One Physicist”, “The 7 Percent Solution”, p. 255, quoted here.

Outline

Summary

Introduction

On the Limitations of this Model

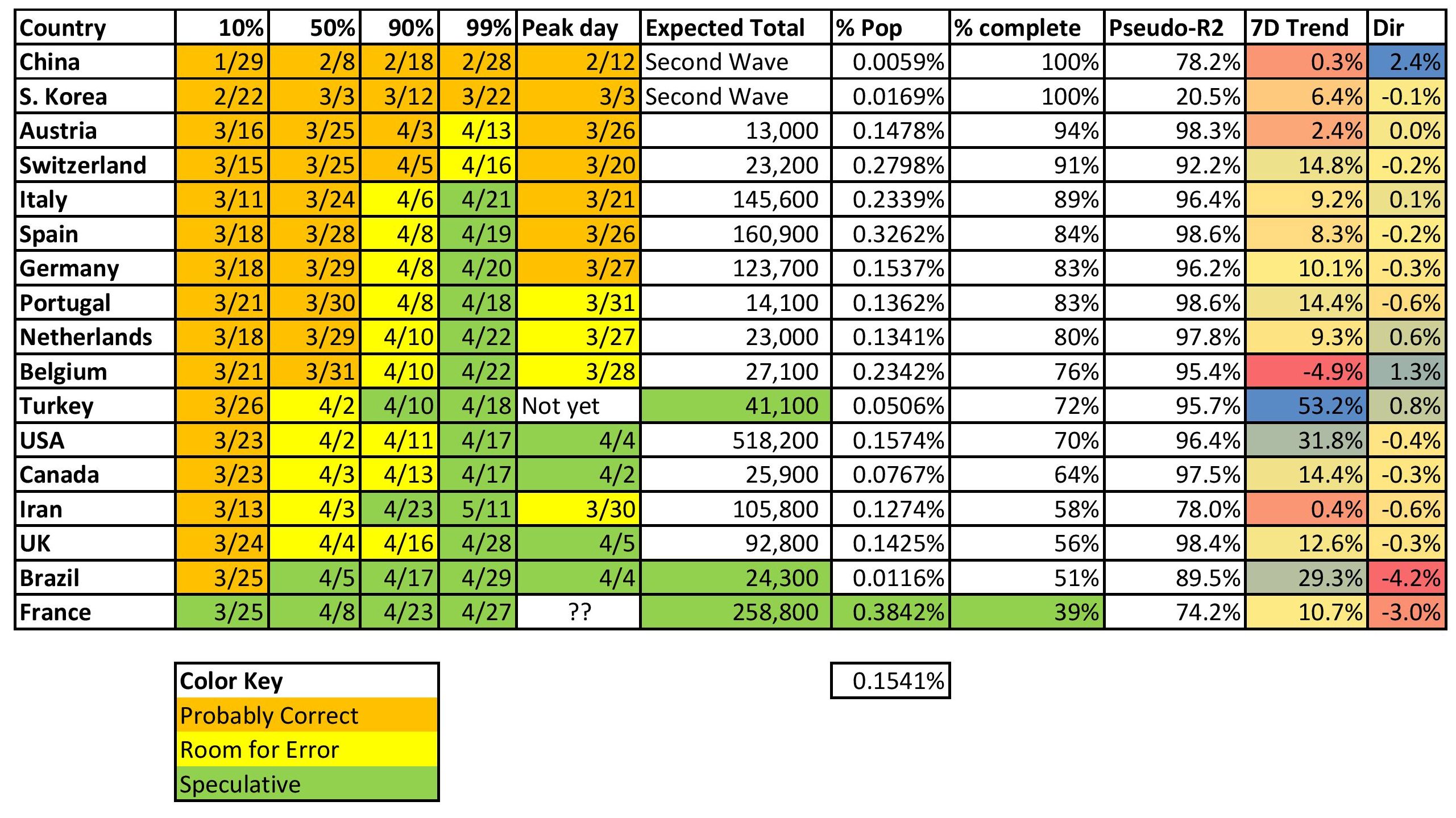

The Graphs — Second Wave, FInishing the First Wave, Coming to the Turning Point, Problem Children (Turkey, USA, Canada, Iran, UK, Brazil, and France)

Closing

Summary

Though the USA model has lagged considerably, and a some of the other modeled countries have lagged a little, the central thesis still stands. Things are getting better faster than most of the politicians, policymakers and media have been forecasting.

Introduction

To those reading me for the first time, you should read the following articles to get up to speed. Those who have read me for a long time know that natively I am a pessimist, so it is unusual for me to be writing as I am doing now.

Before I go on, I want to explain what the two rightmost columns on the tables above and below mean.

7D Trend — the seven day sum of forecast errors as a ratio of the number of cases at the beginning of the seven days. Positive means the model has been underestimating. Negative, overestimating.

Dir — Direction of the seven days of forecast errors — beta coefficient of the forecast errors versus time as a ratio of the number of cases at the beginning of the seven days.

The idea is to try to point out where the model is persistently missing, how large is it, and is it correcting or getting worse?

On the Limitations of this Model

All models have limitations. This model, being used to extrapolate, definitely has limitations. Extrapolation, as I have said, is dangerous. It’s dangerous because we know the past data with some degree of error, and the future not at all. Extrapolation, even if the underlying functional form used for estimation is right, assumes that all processes generating the values estimated are not shifting. If that is a good approximation to the reality that comes, luck will come marching in as genius.

This is a time series model. There are many structural models out there, and the “experts” estimate and use them. They have more data than I do. Those models suffer many of the same problems that complex economic models do. There are too many parameters to estimate, and they face the same problem I do with the future shifting, and errors in past data, as well as functional form issues. They are also subject to social and economic pressures that I don’t have to the same degree.

Scientists need the approval of their peers in order to publish and for general happiness. They need to be able to make money to survive. It is difficult to get tenure, and most scientists won’t take chances with that process.

It gets worse when science is being used for policy purposes, and gets picked up by the media. Caution is ordinarily a good thing,, but not when it misstates what is going on in order to achieve the ends of third parties. Tell the truth, and then let the politicians, policymakers, lawyers, businessmen, etc. figure out what they will do. The media almost always prefers sensational, sharp, easy-to-tell stories, over the complexity of what is true. The same is true of most average people who would rather not think hard, but just imitate the behavior of others.

Thus I tend to distrust “experts” whose ideas are used for political or policy purposes, and get trumpeted in the media. Their incentives are skewed — once you get close to fame, power, and maybe even money, you’d like to keep it, and that is a snare for many.

Practically, for this model, the difficulty comes around the middle, where the shift is happening — new cases peaking, growth in total cases decelerates. Why is it difficult? Small changes make a big difference to the shape and height of the curve. The prior day’s curve is anticipating a certain amount of deceleration in the growth in total claims. When the data arrives with more new cases than anticipated, the new curve will be taller and longer. VIce-versa if less new cases arrive. That is why for some areas that I modeled, the process seems to stall around 40-60%.

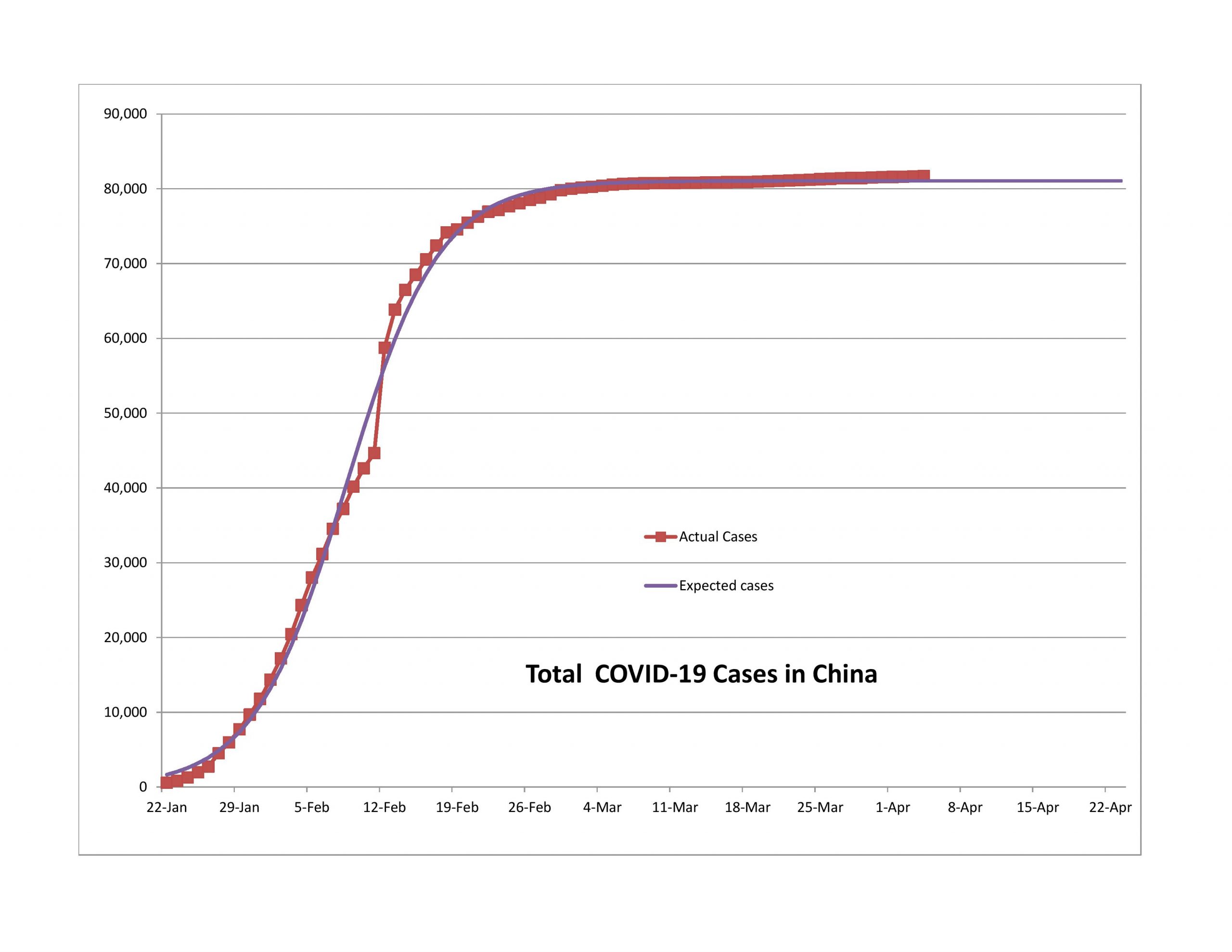

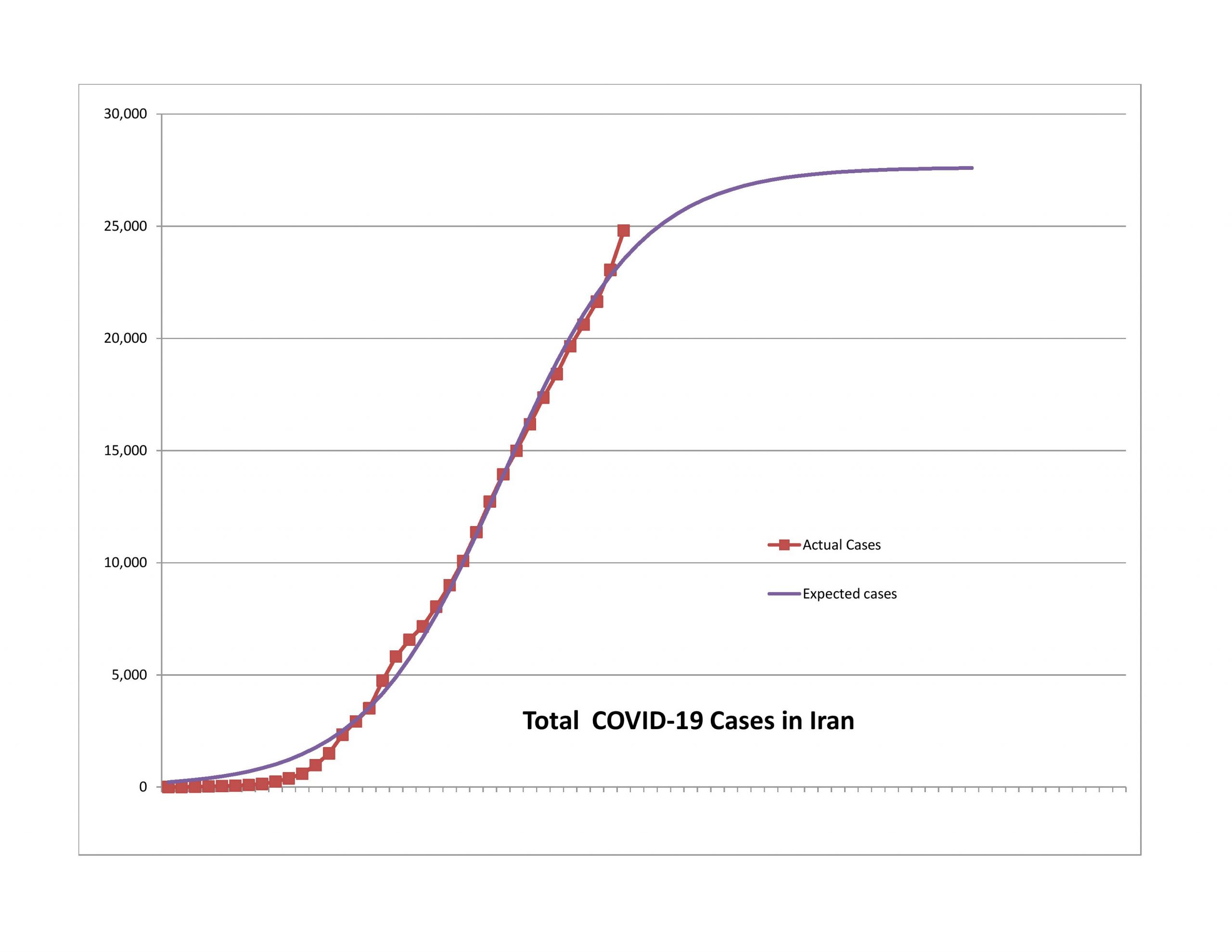

Now, there are raw data errors as well, like China on 2/12 and France on 4/3. There are nations like Iran where the political turmoil may have led to delayed reporting.

But for the most part, the models have worked well, just not so well for the US yet. We’ll get to that later. Before I do, I want to state a few things I have learned as I have gone through the modeling, which has been a learning process for me.

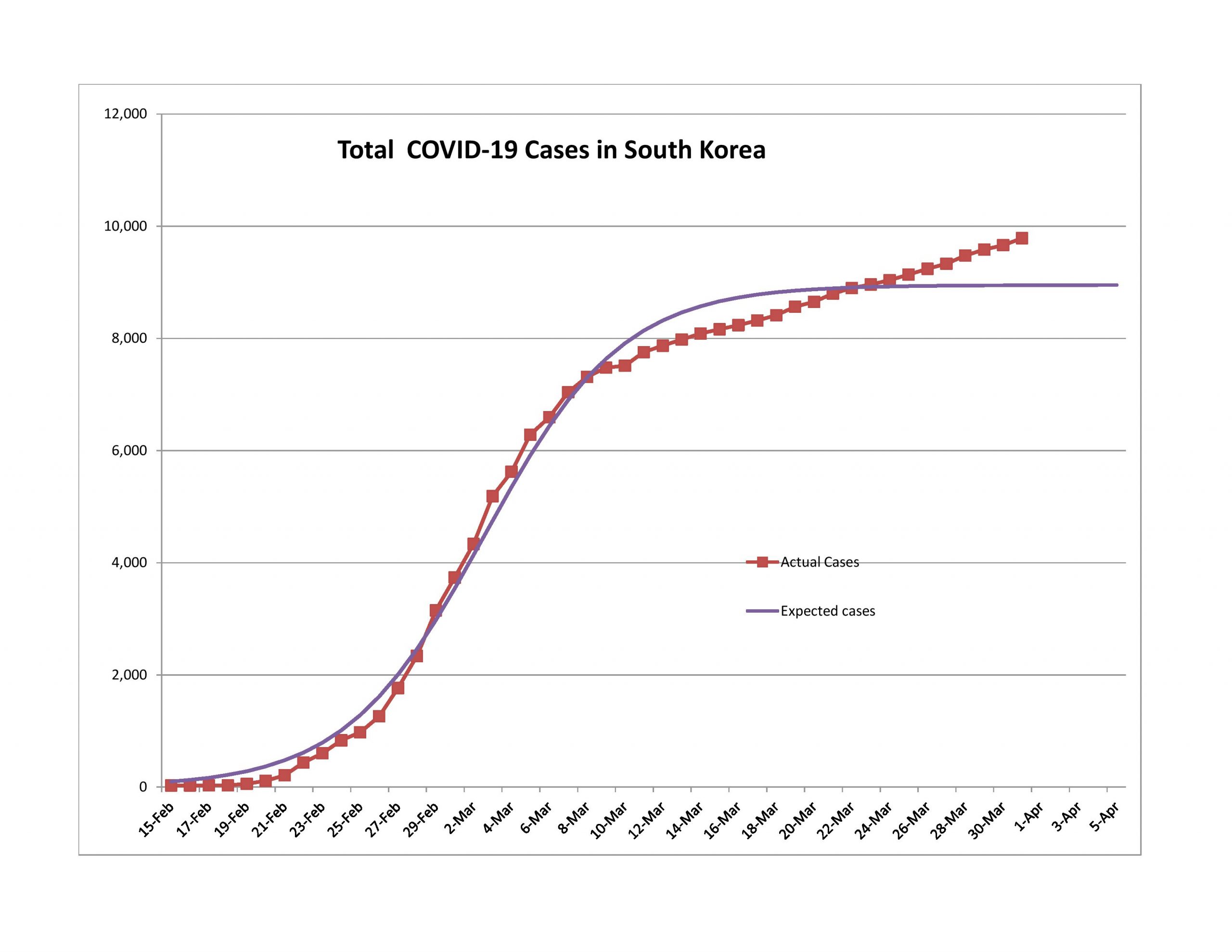

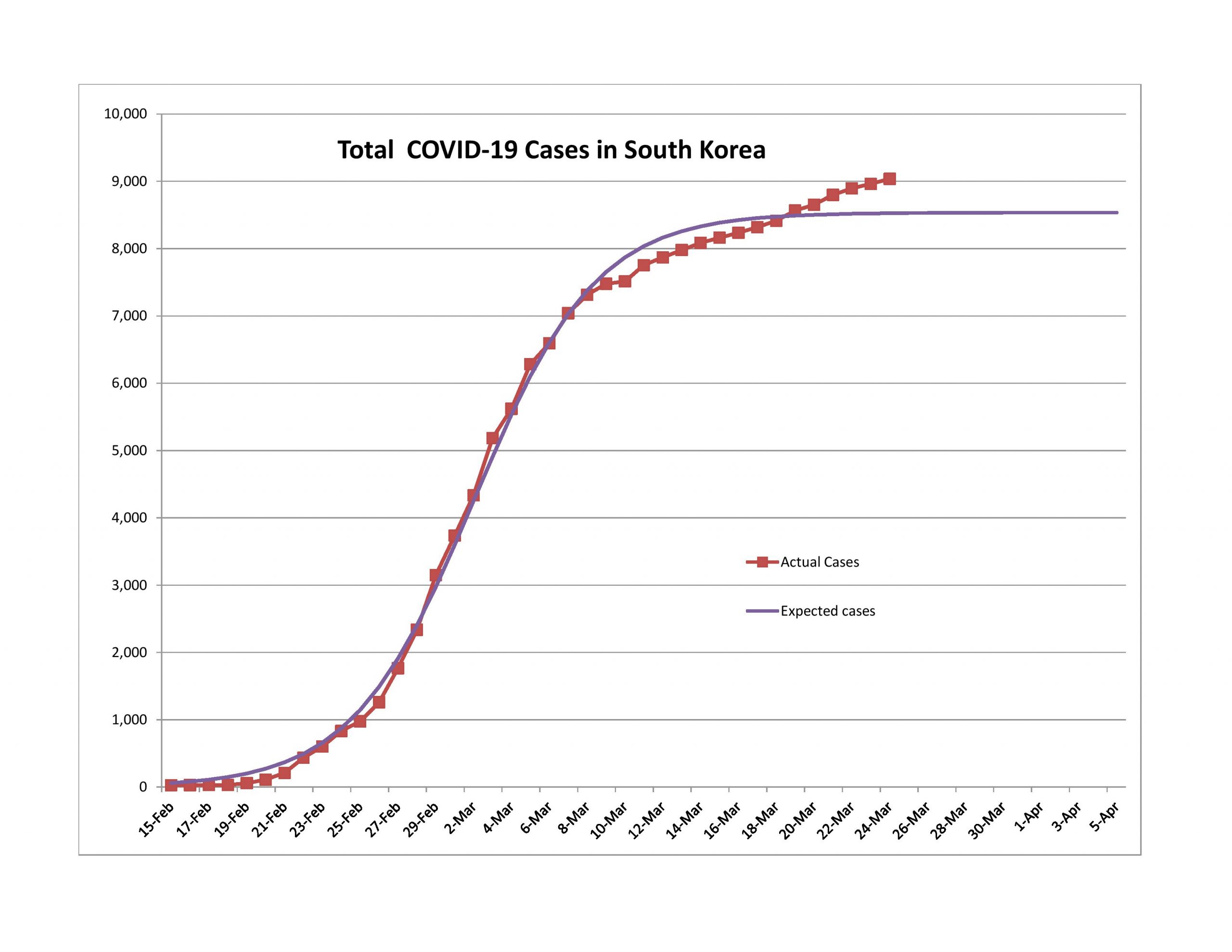

Look at the percentage of population that the model is projecting for reported infections. If it’s not high enough, the model is wrong. Unless a nation jumped on the problem immediately, you won’t get results like South Korea.

The nations that tested more as a percentage of population, particularly early in the epidemic, did a lot better.

Repeated forecast errors in the same direction indicate the process for new claims is changing, and the model is trying to adjust.

In that situation, if we?re only getting better at finding those infected, the upper part of the curve should tail off sharply.? On the other hand, if the if the ratio of new cases to total cases is protractedly rising because more infections are occurring, that?s an increase in the ultimate level of reported cases.

Once a nation gets to the 10% point, getting to the 90% point takes three weeks or so. Getting to the 99% point takes 4-5 weeks.

The markets will anticipate the end, with false starts, and a lot of noise.

As Buffett says (something like): I’d rather be approximately right than precisely wrong… or, Rule 65: “The second-best plan that you can execute is better than the best plan that you can?t execute.” My goal was to get some idea of when the market might turn. In that sense, this has been a success.

The Graphs

As in prior posts, I will run through the graphs now.

Second Wave

Finishing the First Wave

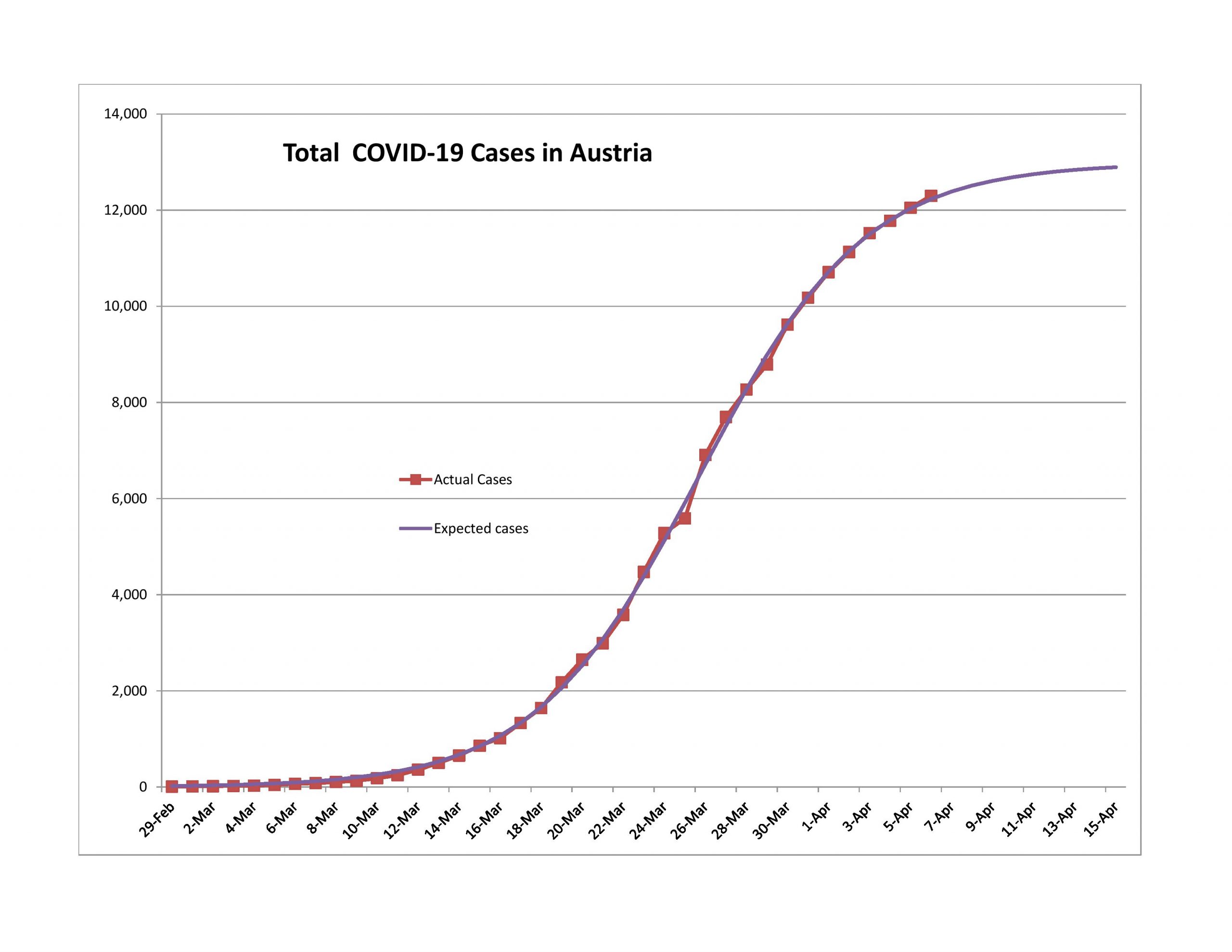

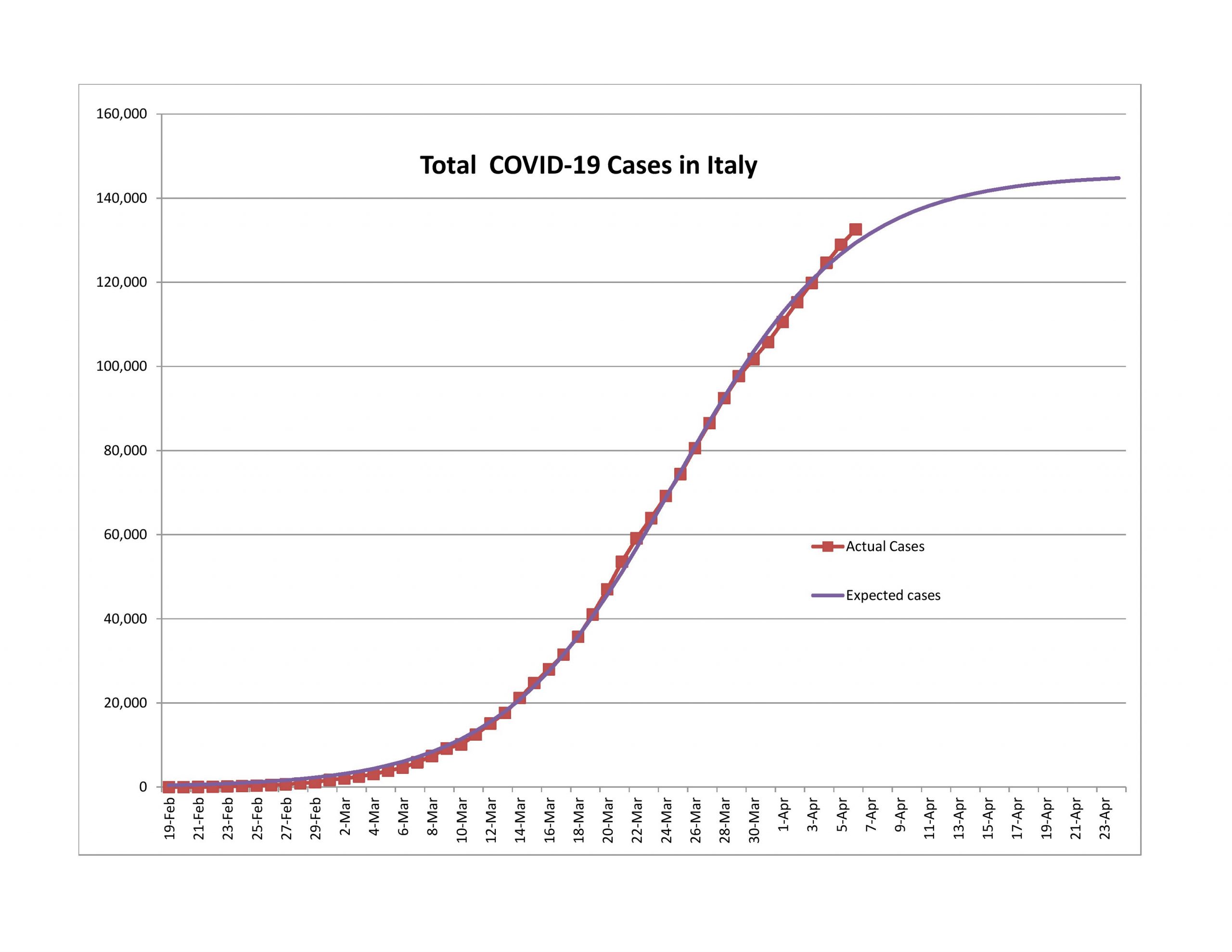

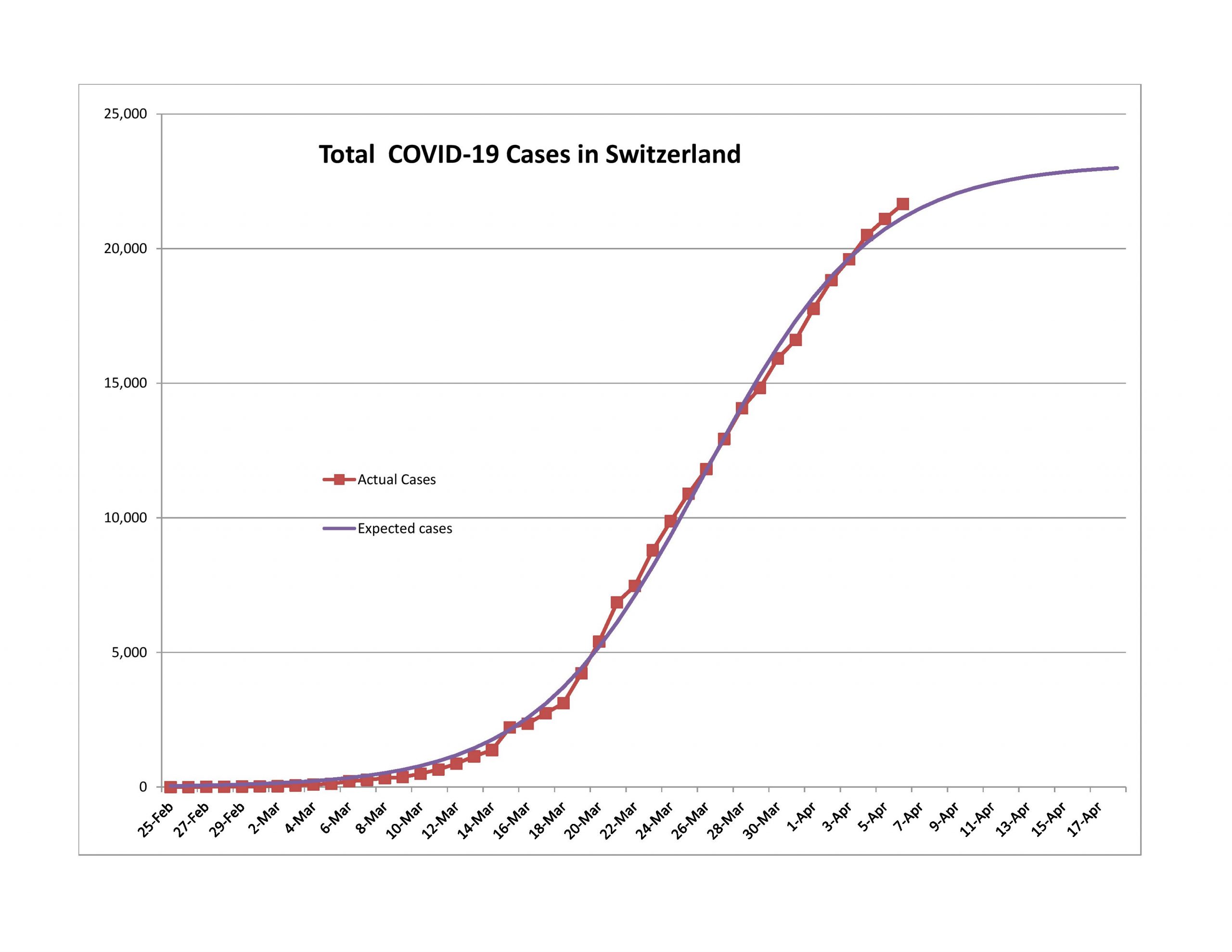

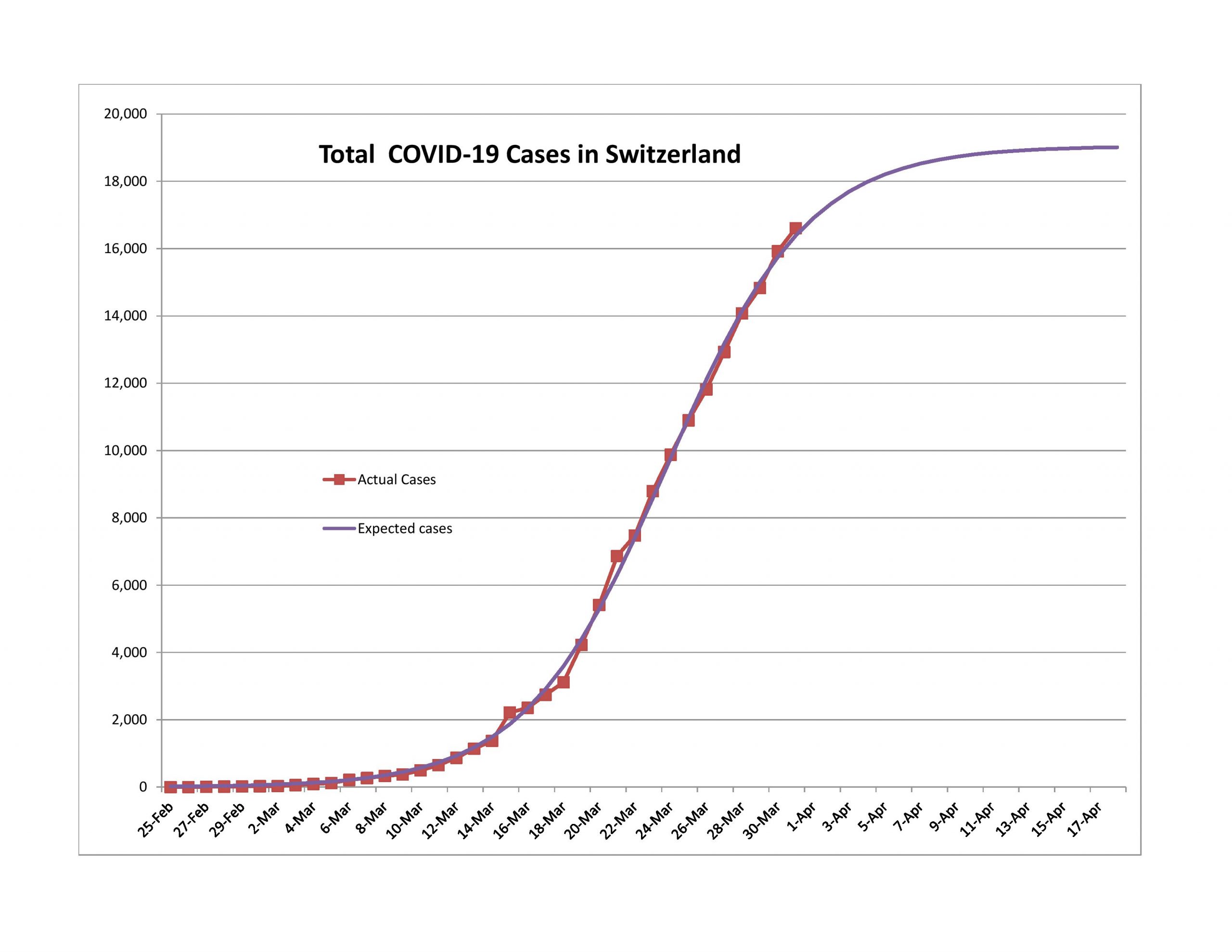

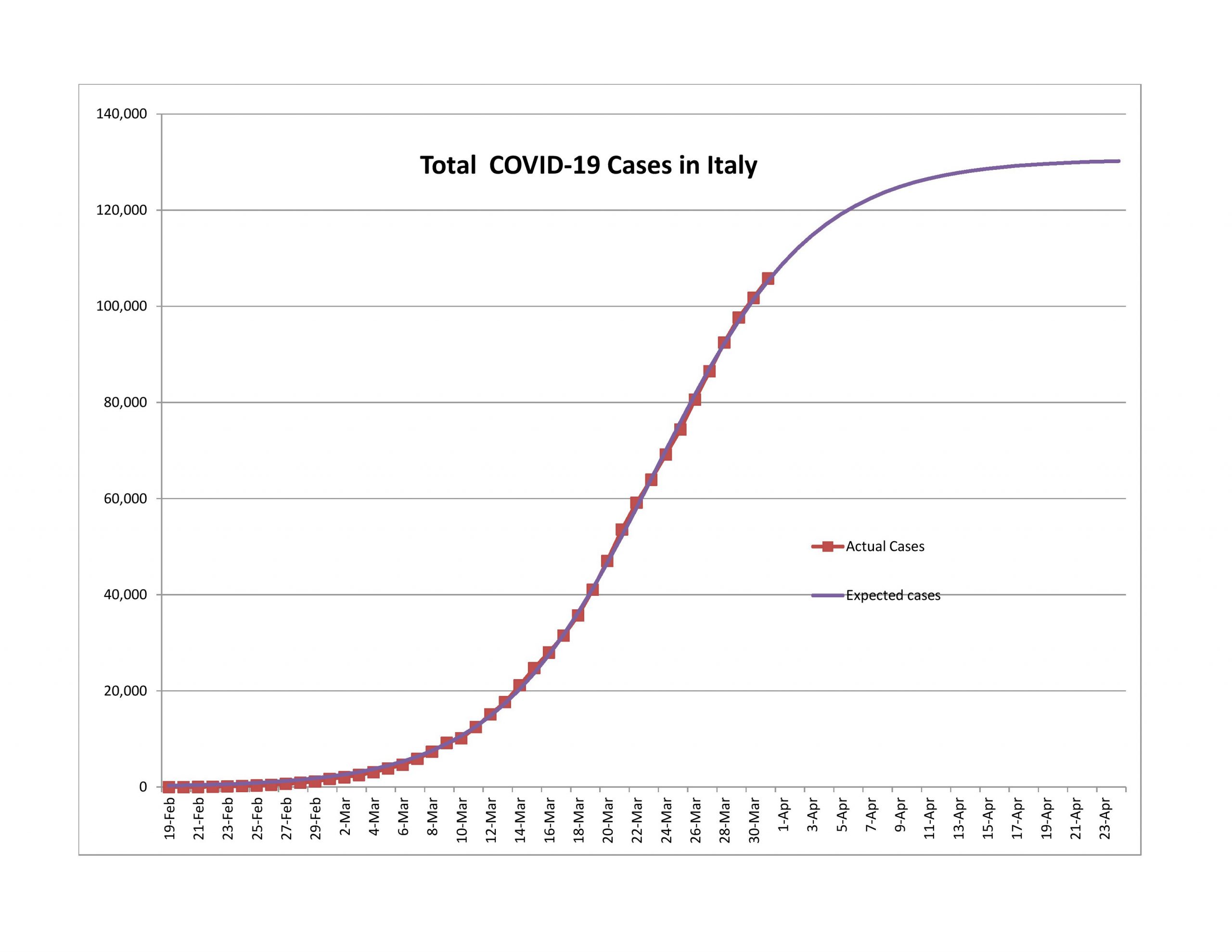

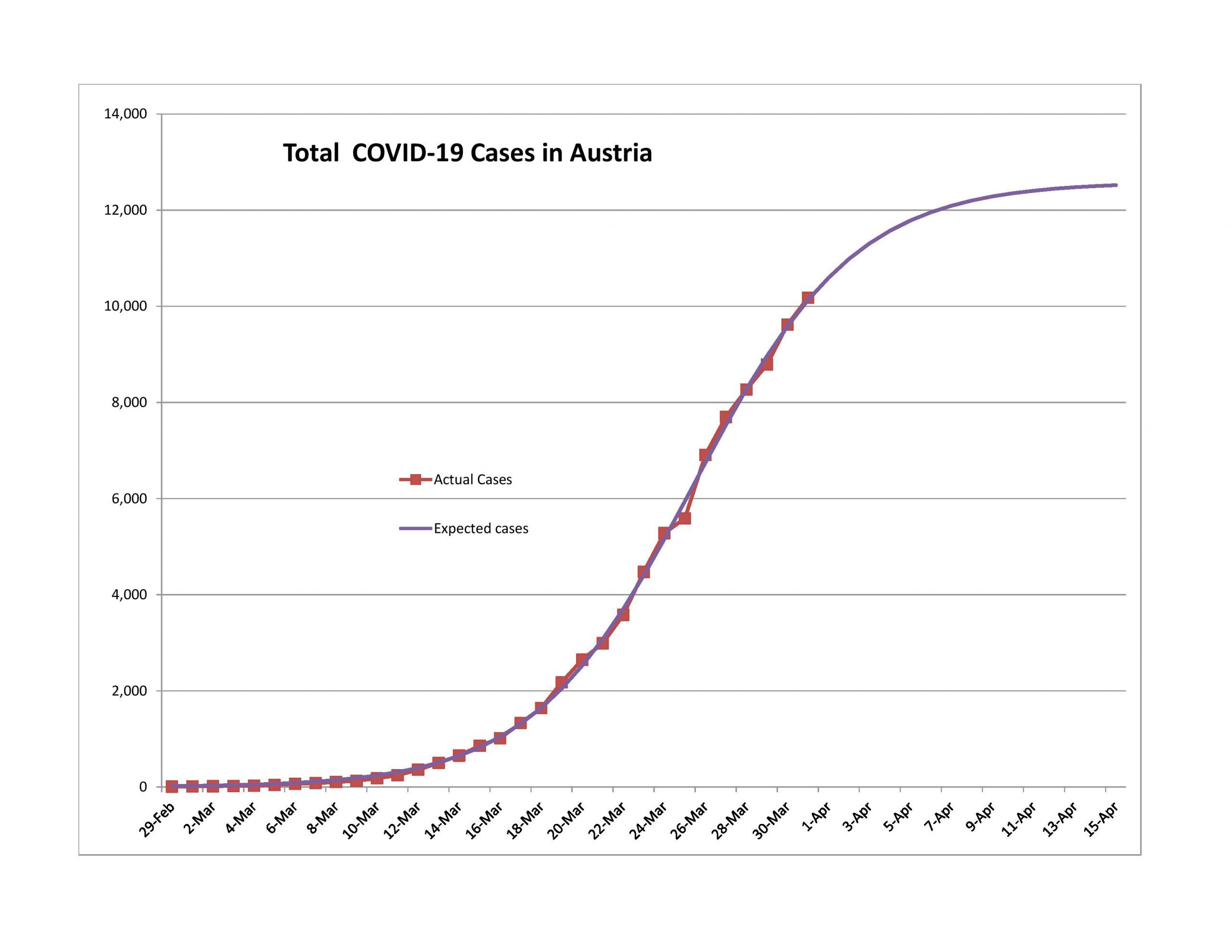

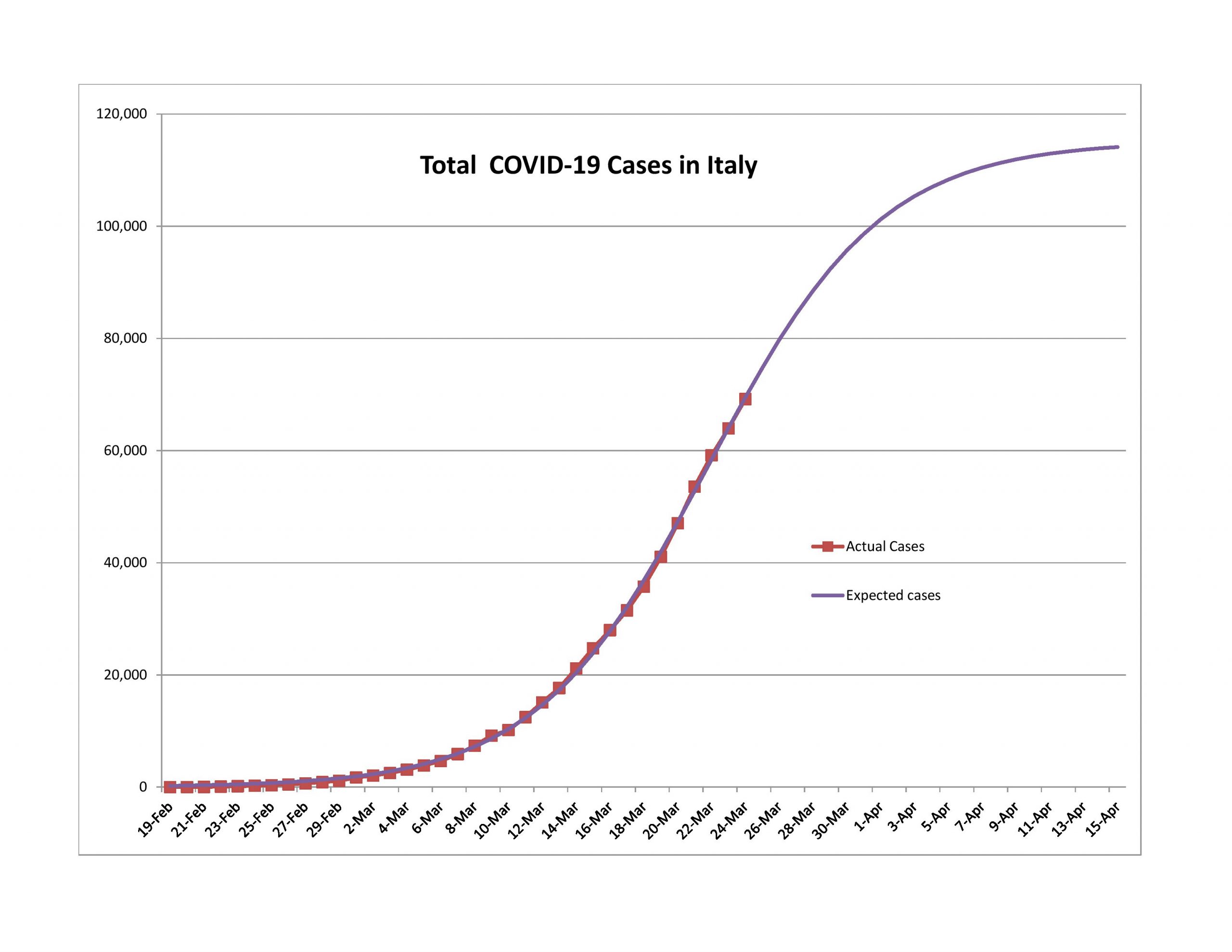

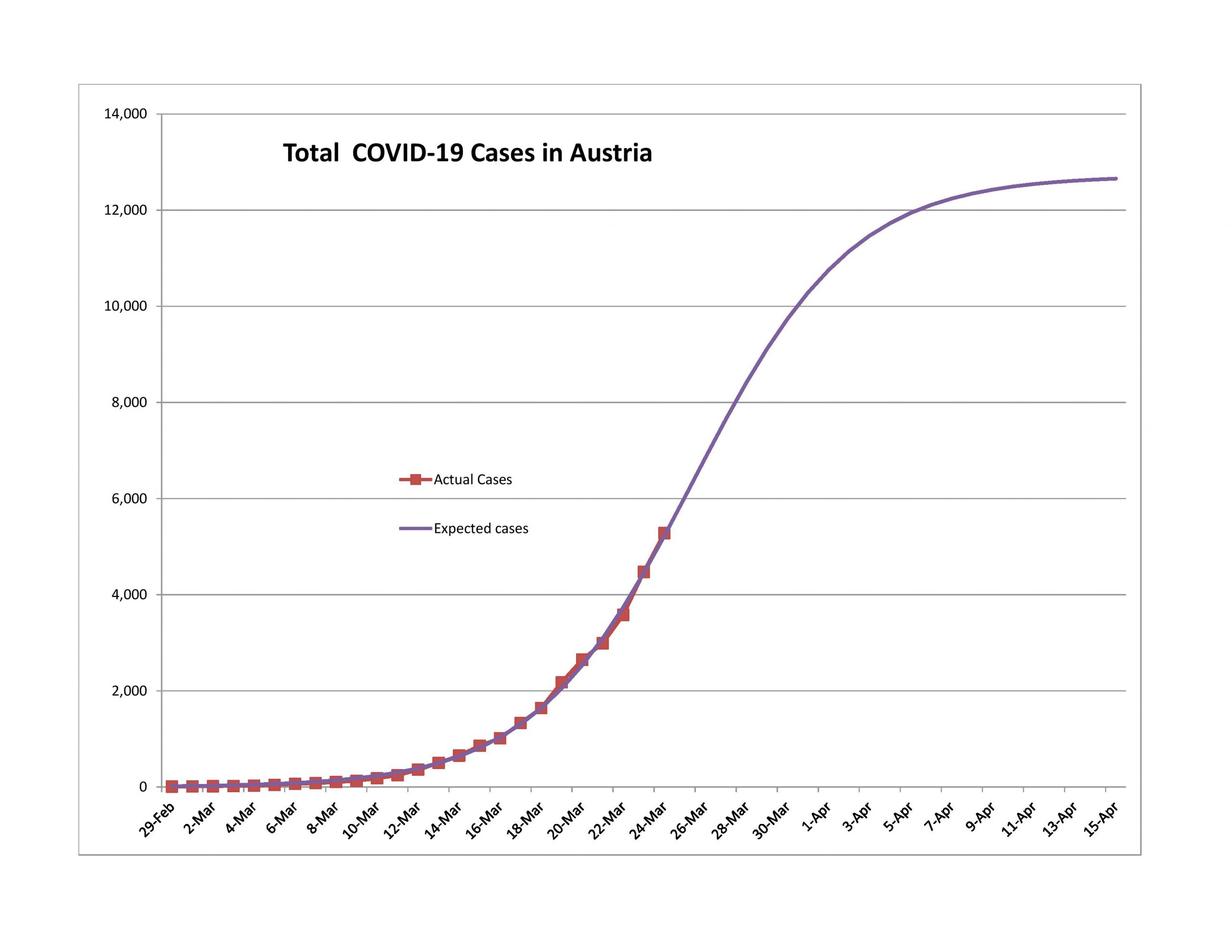

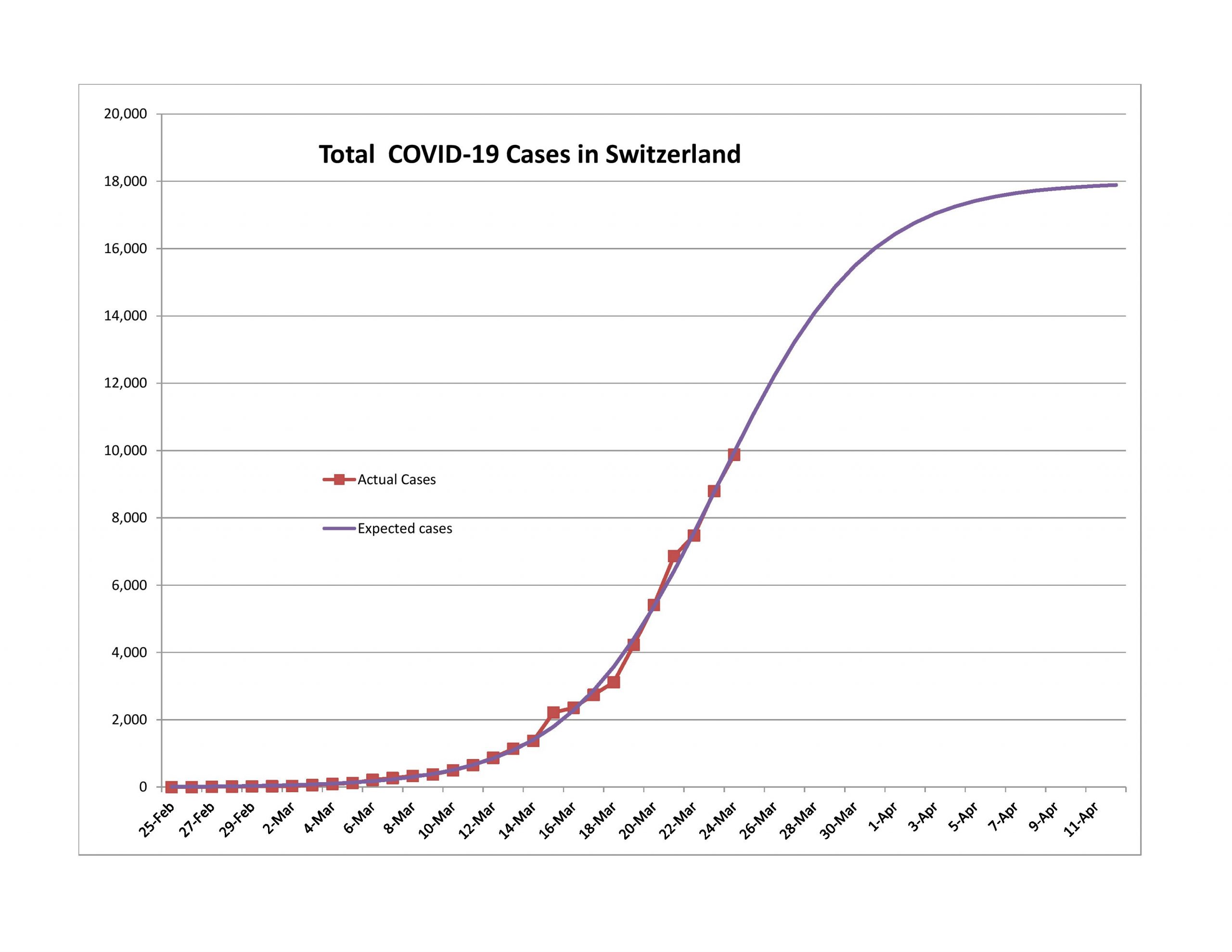

I write this with a little concern that I might be early on Italy and Switzerland, but new cases have been slowly rapidly for the two of them and Austria. Note that all three of them did a lot more testing per capita than most nations. You can see that here. The table sorts itself if you click on the top of the columns.

Coming to the Turning Point

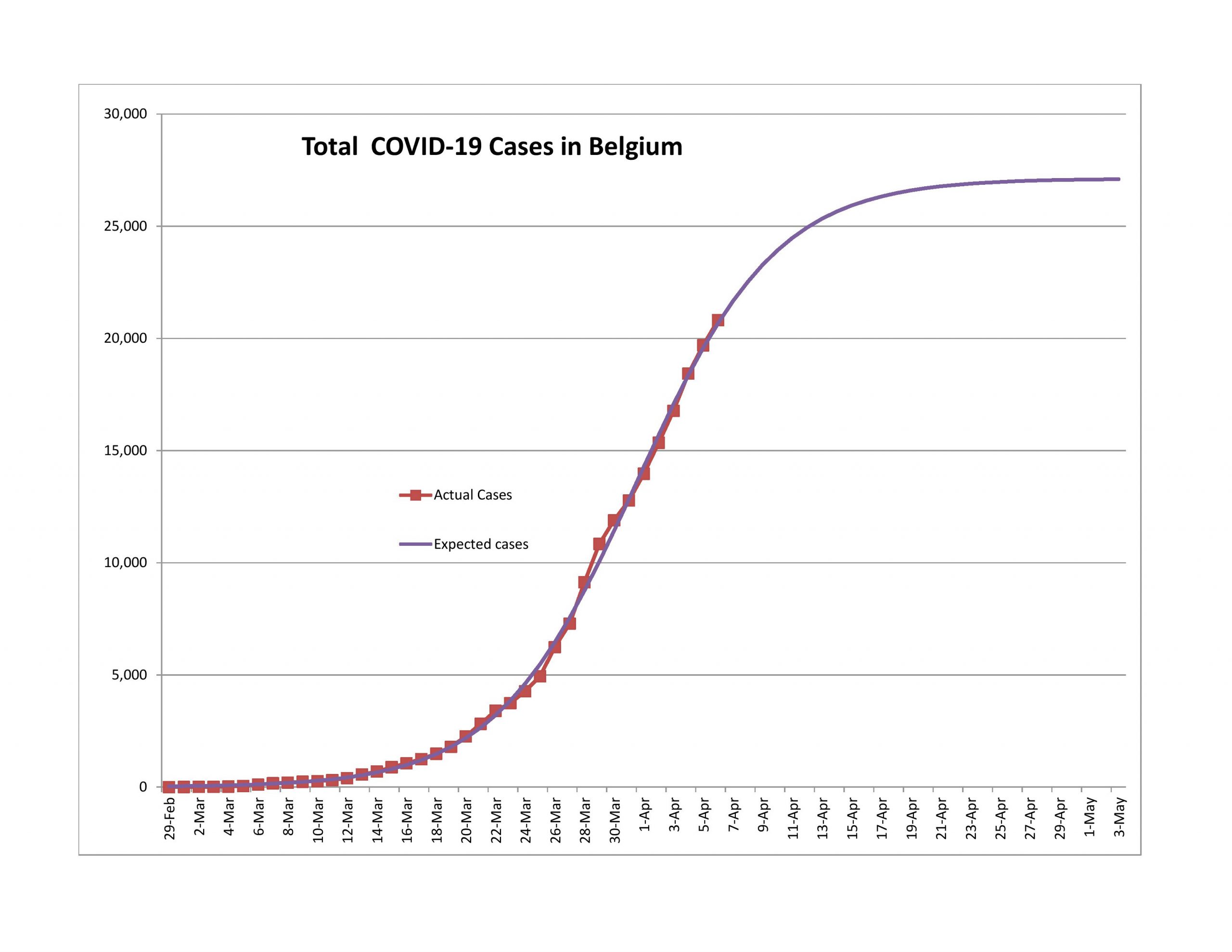

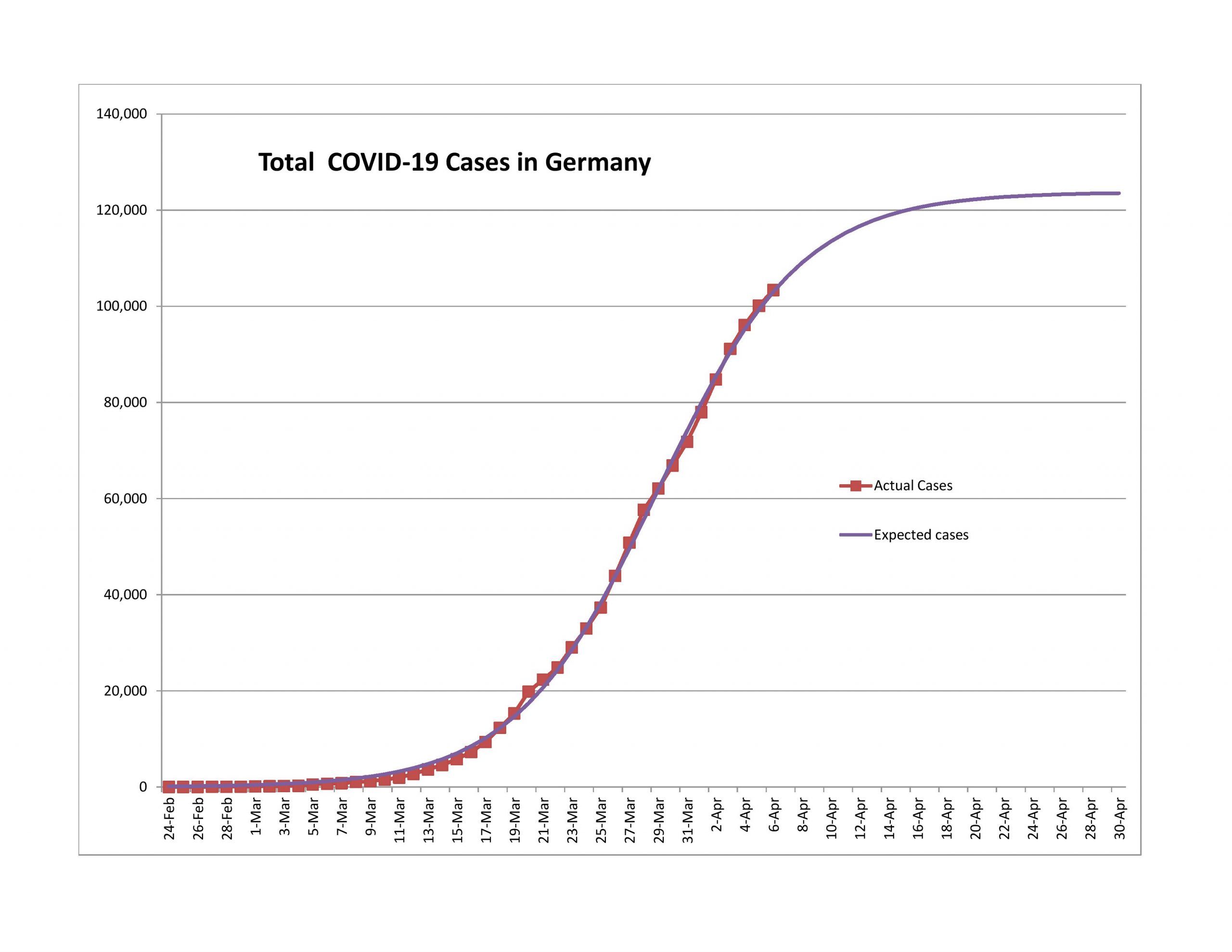

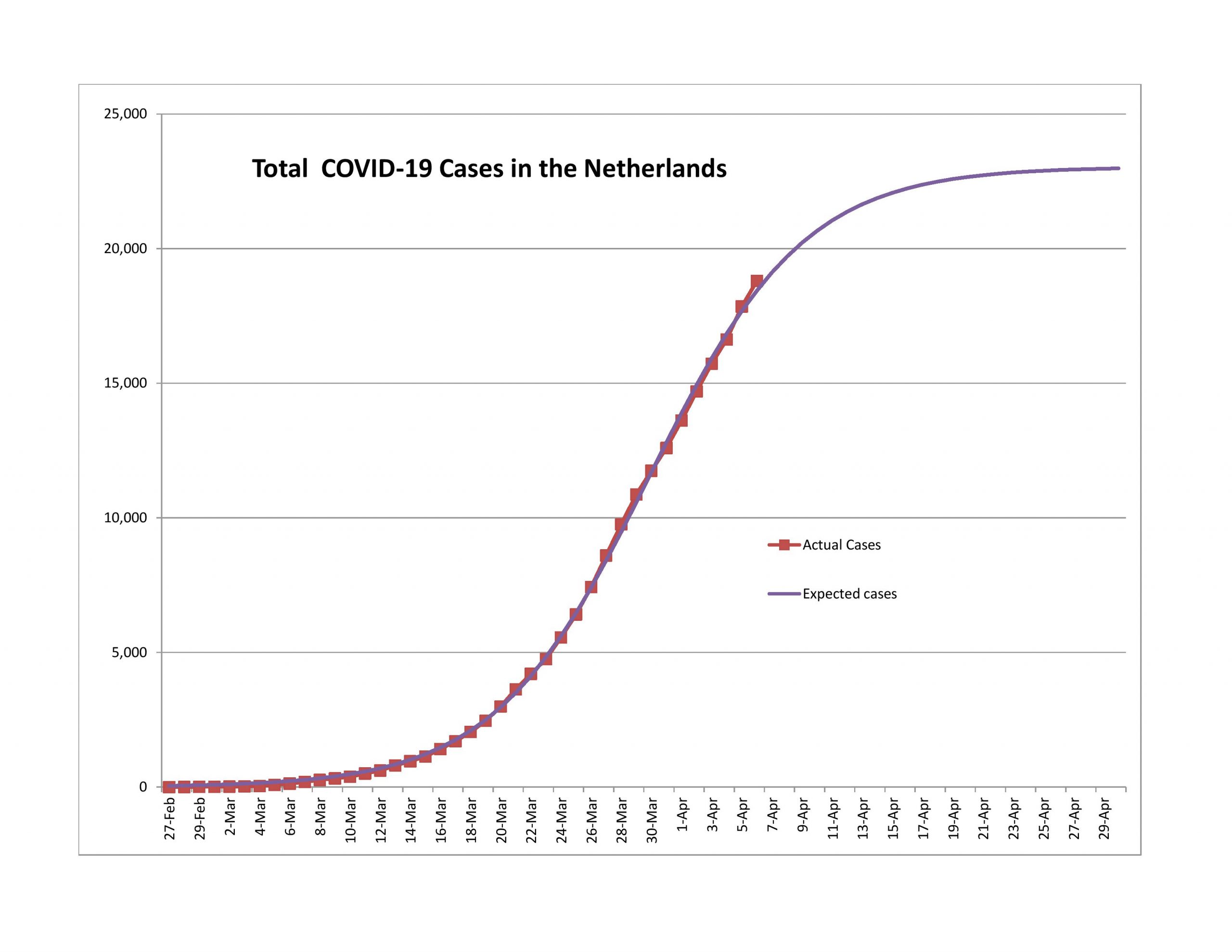

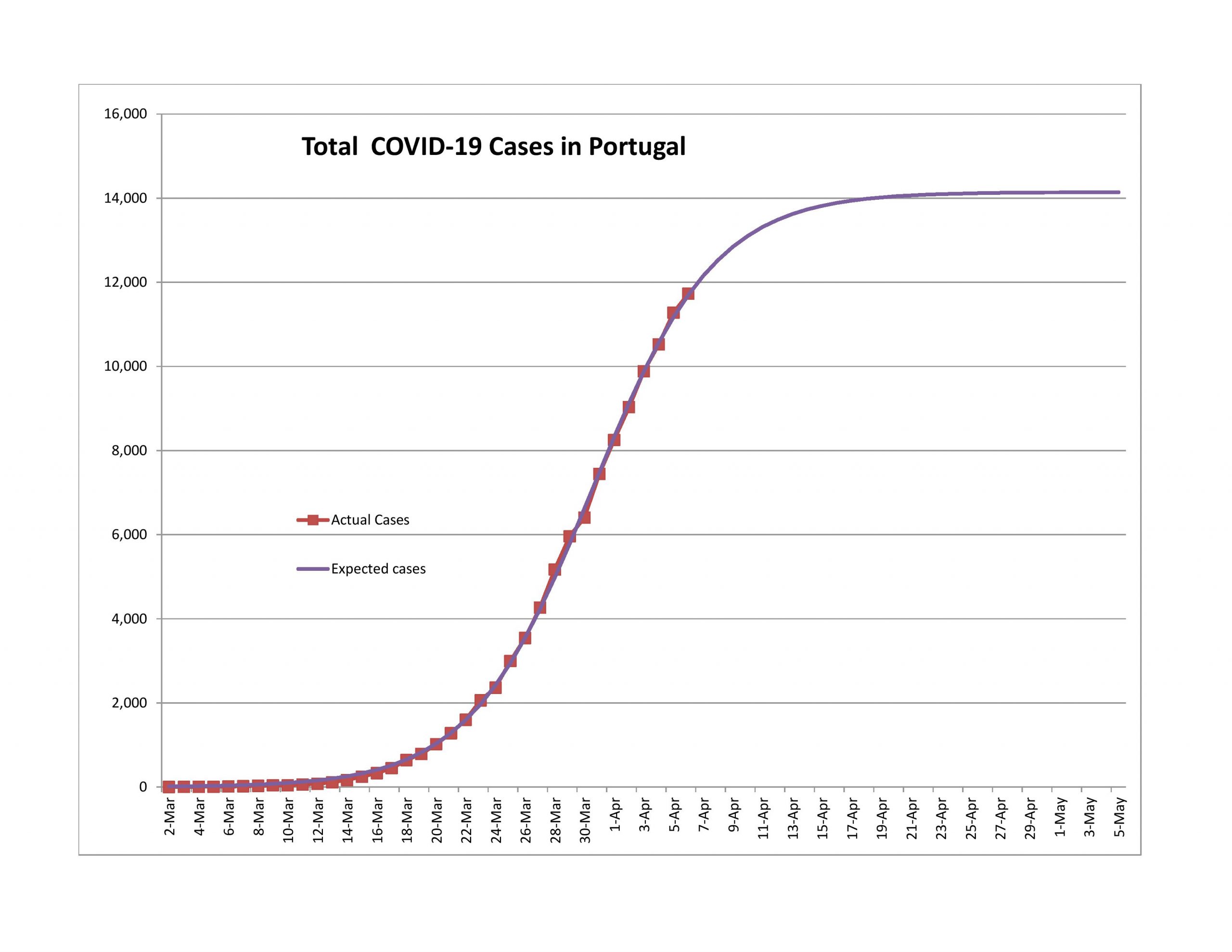

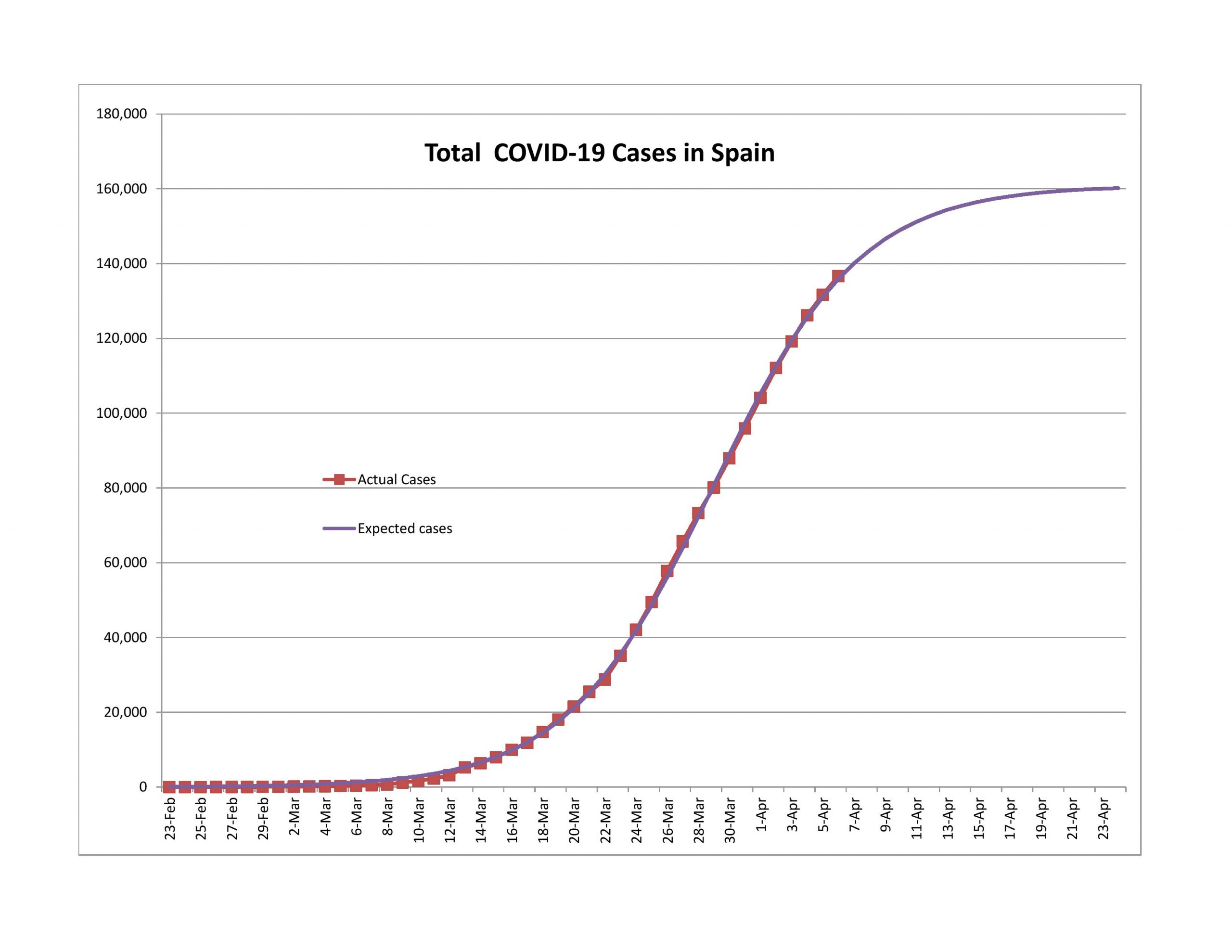

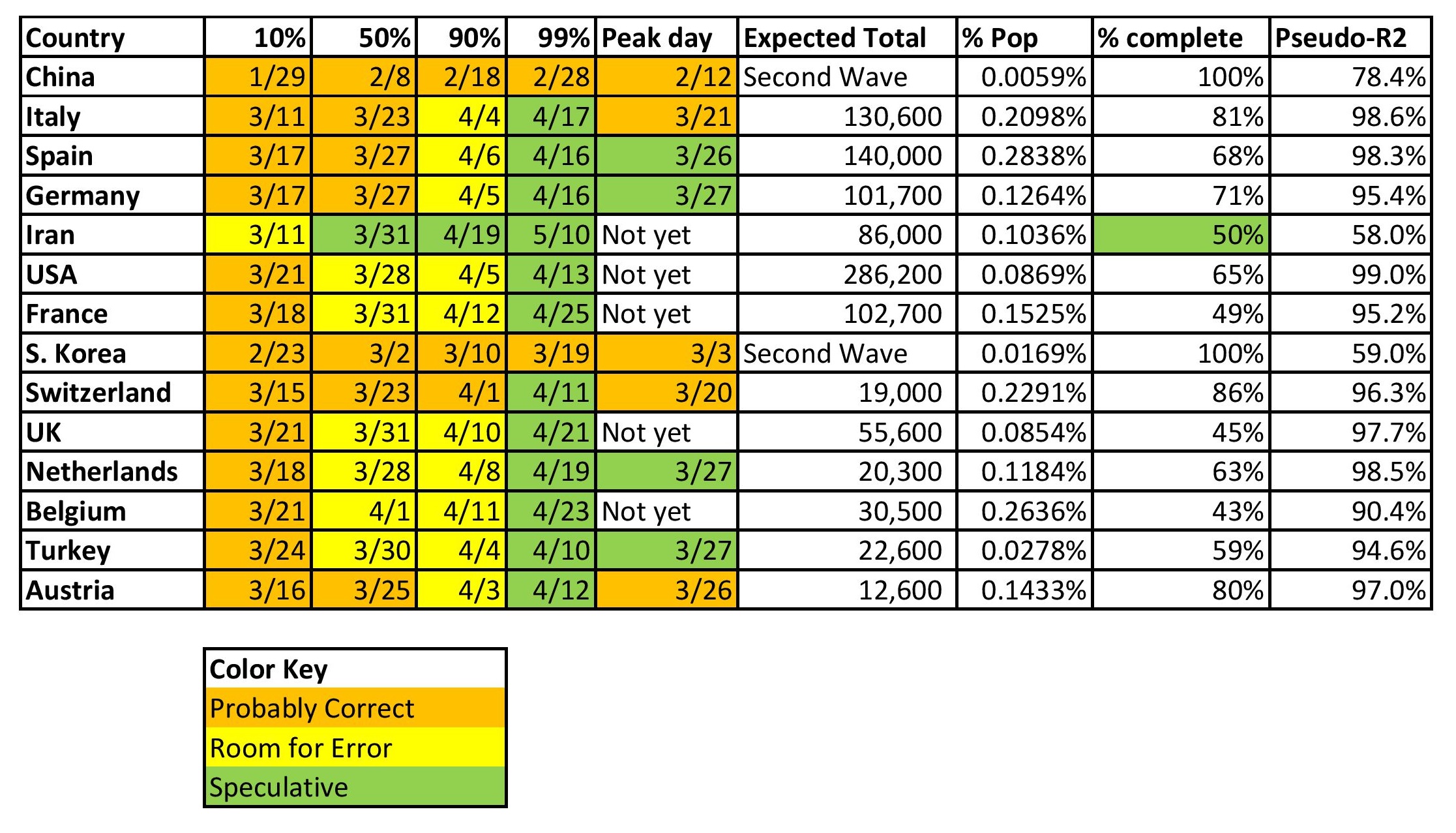

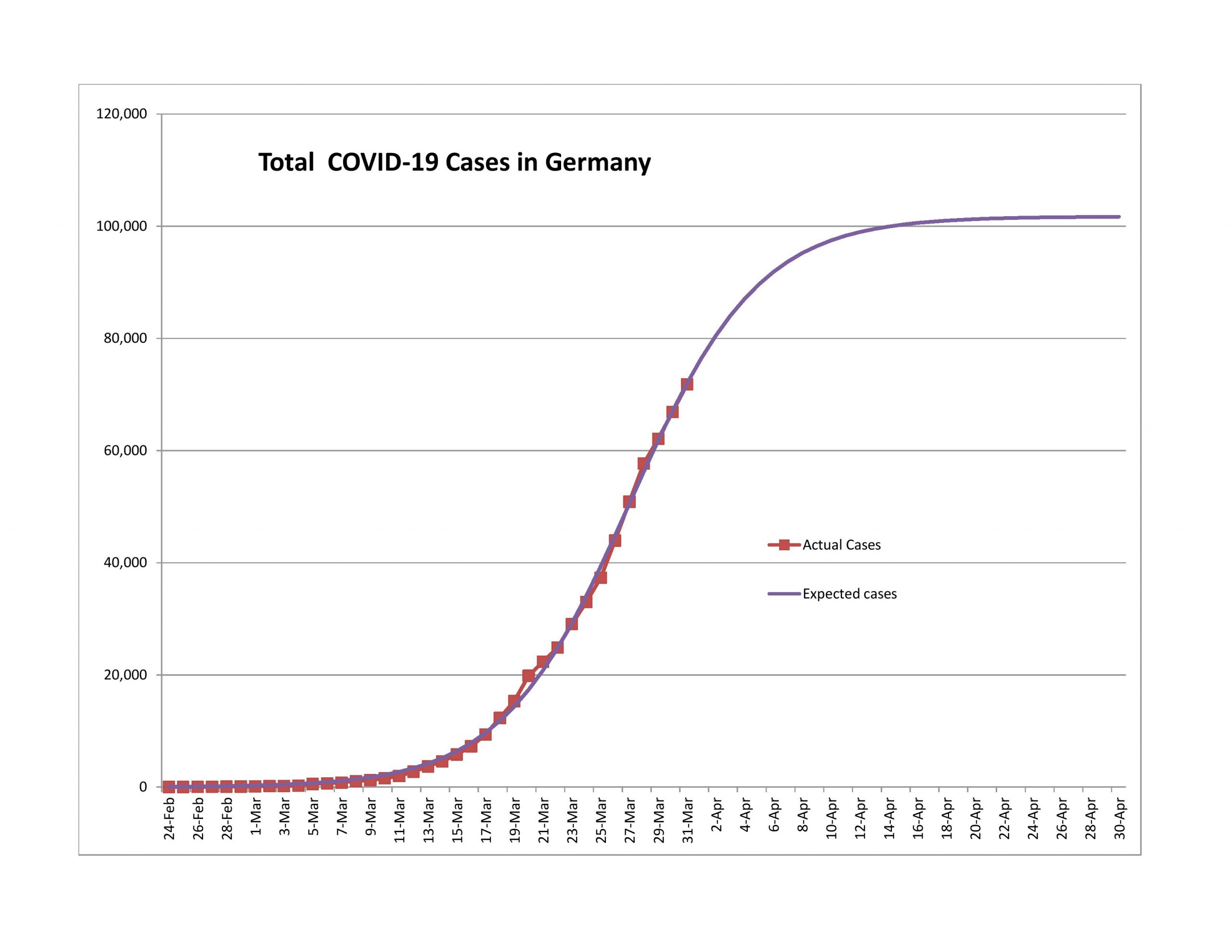

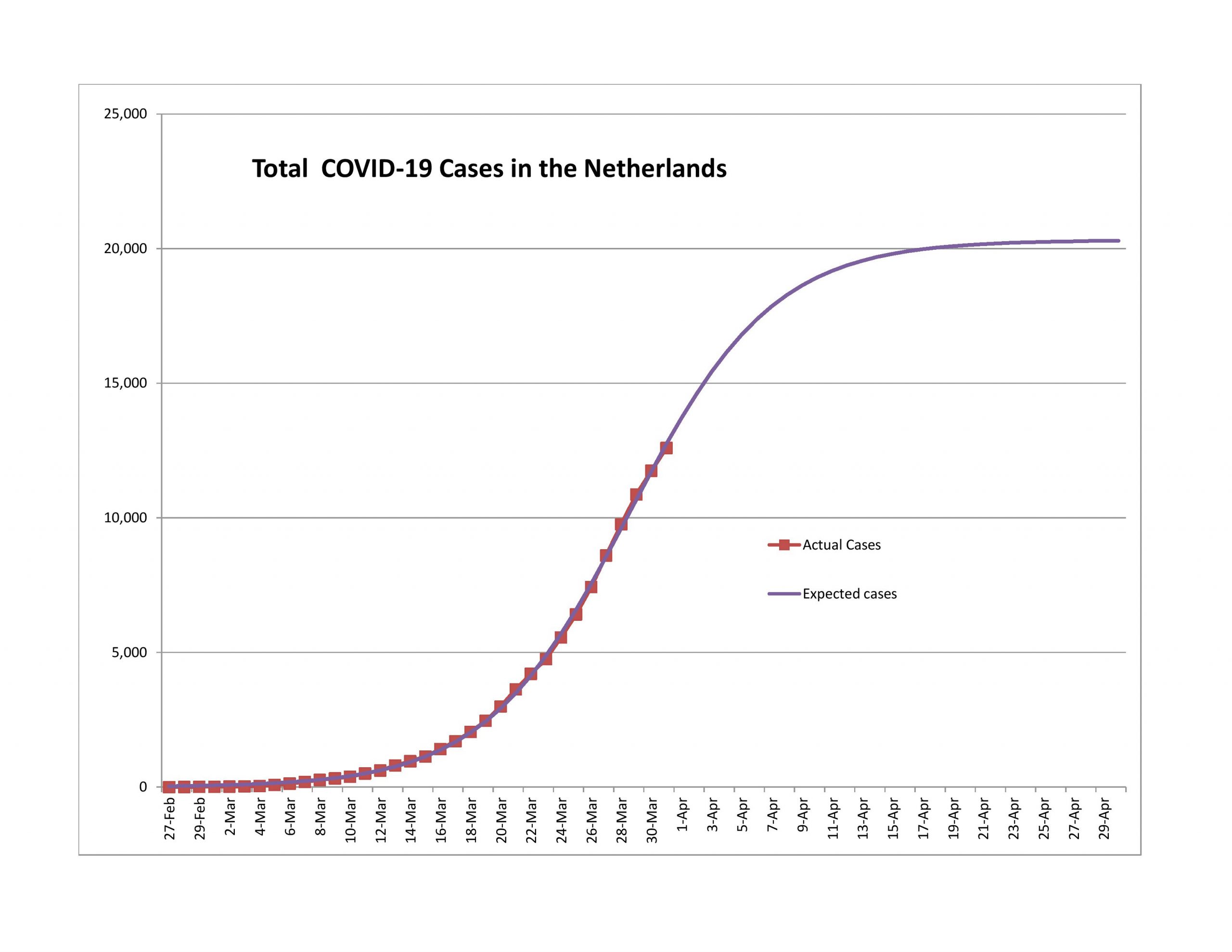

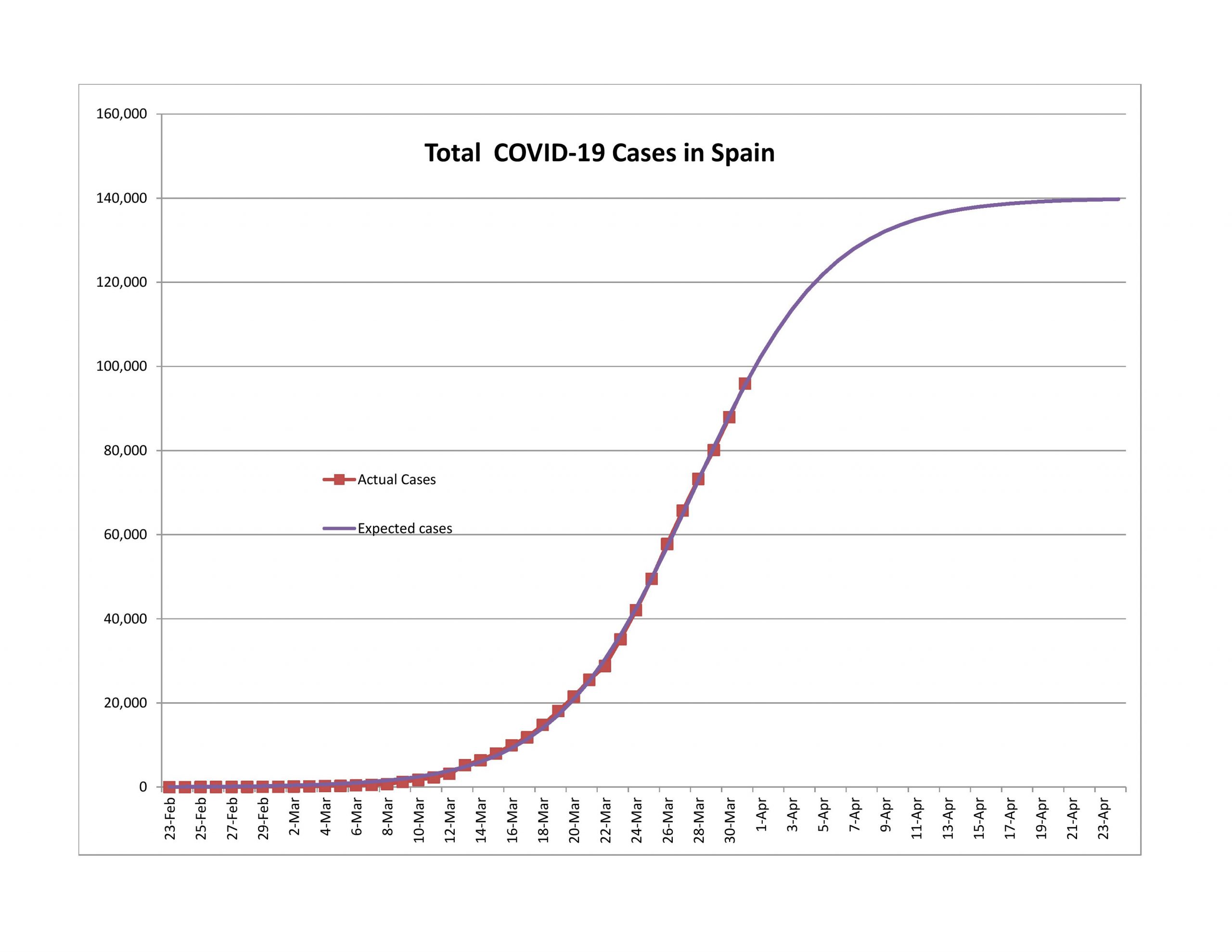

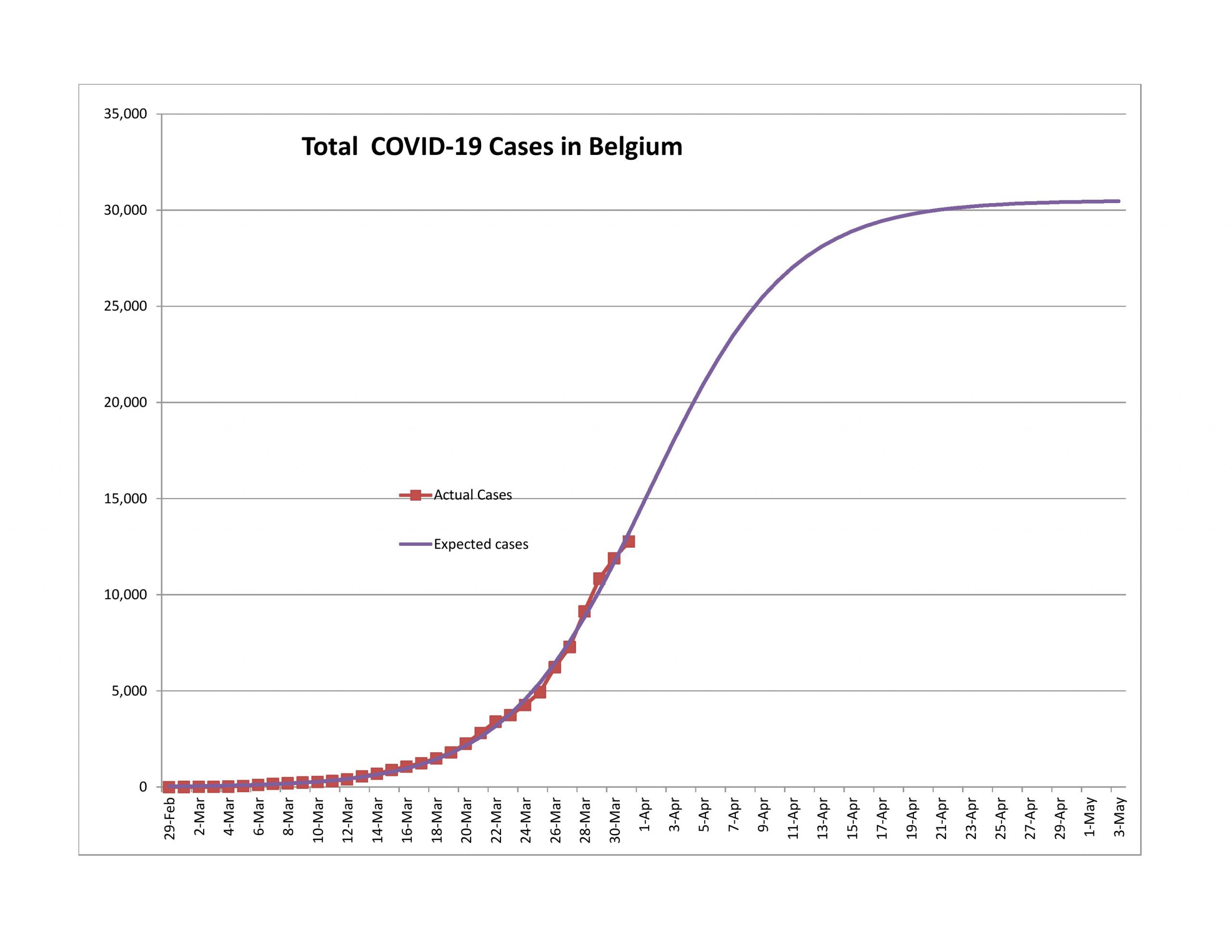

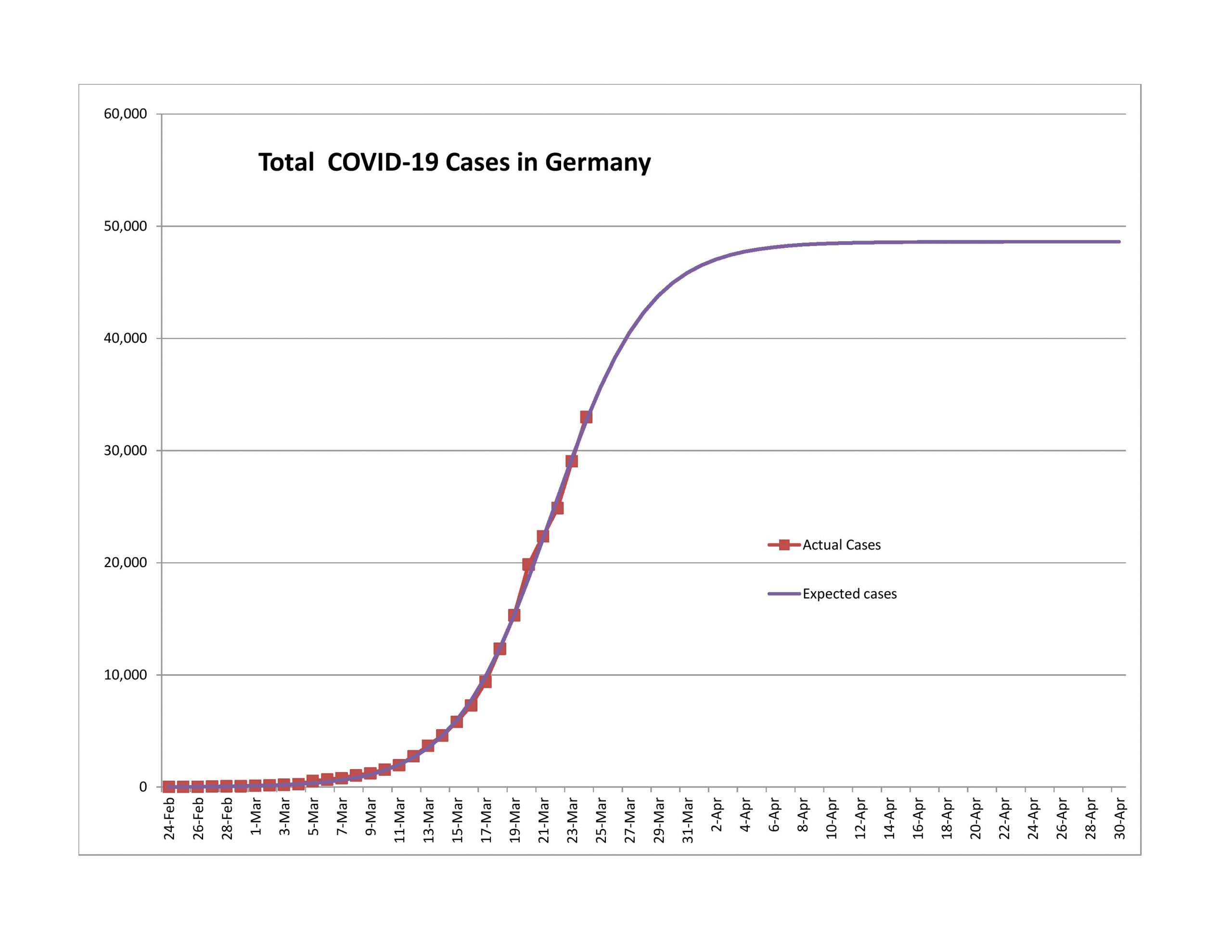

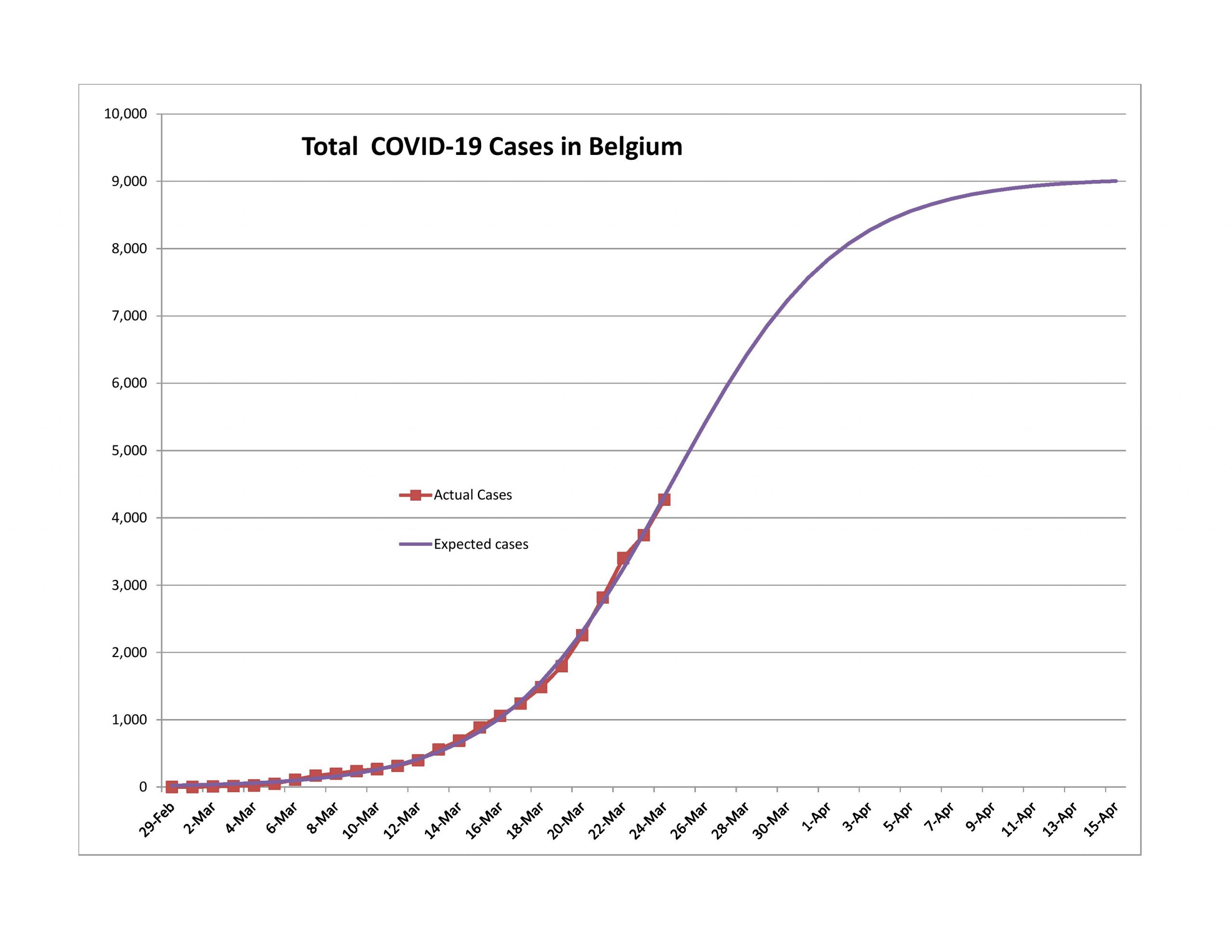

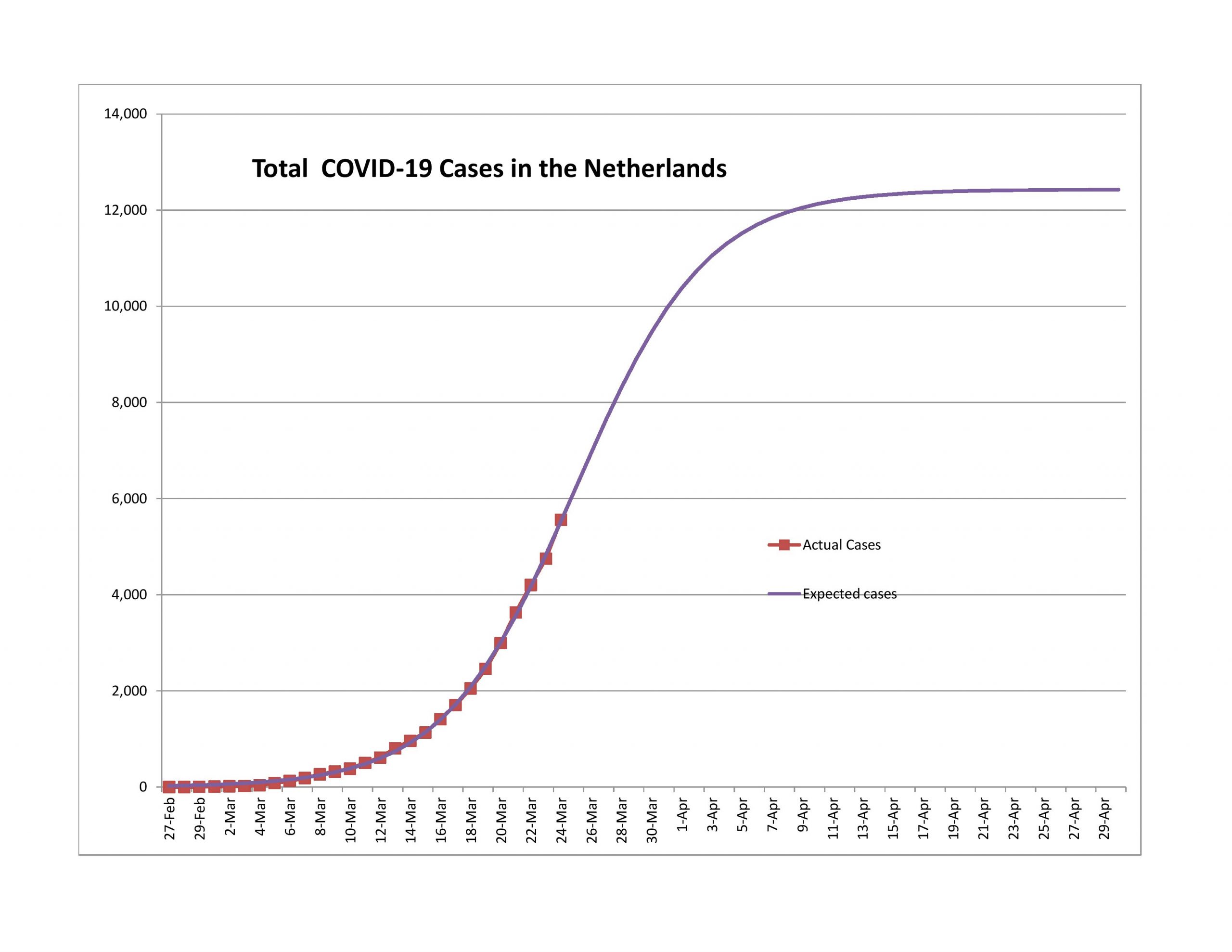

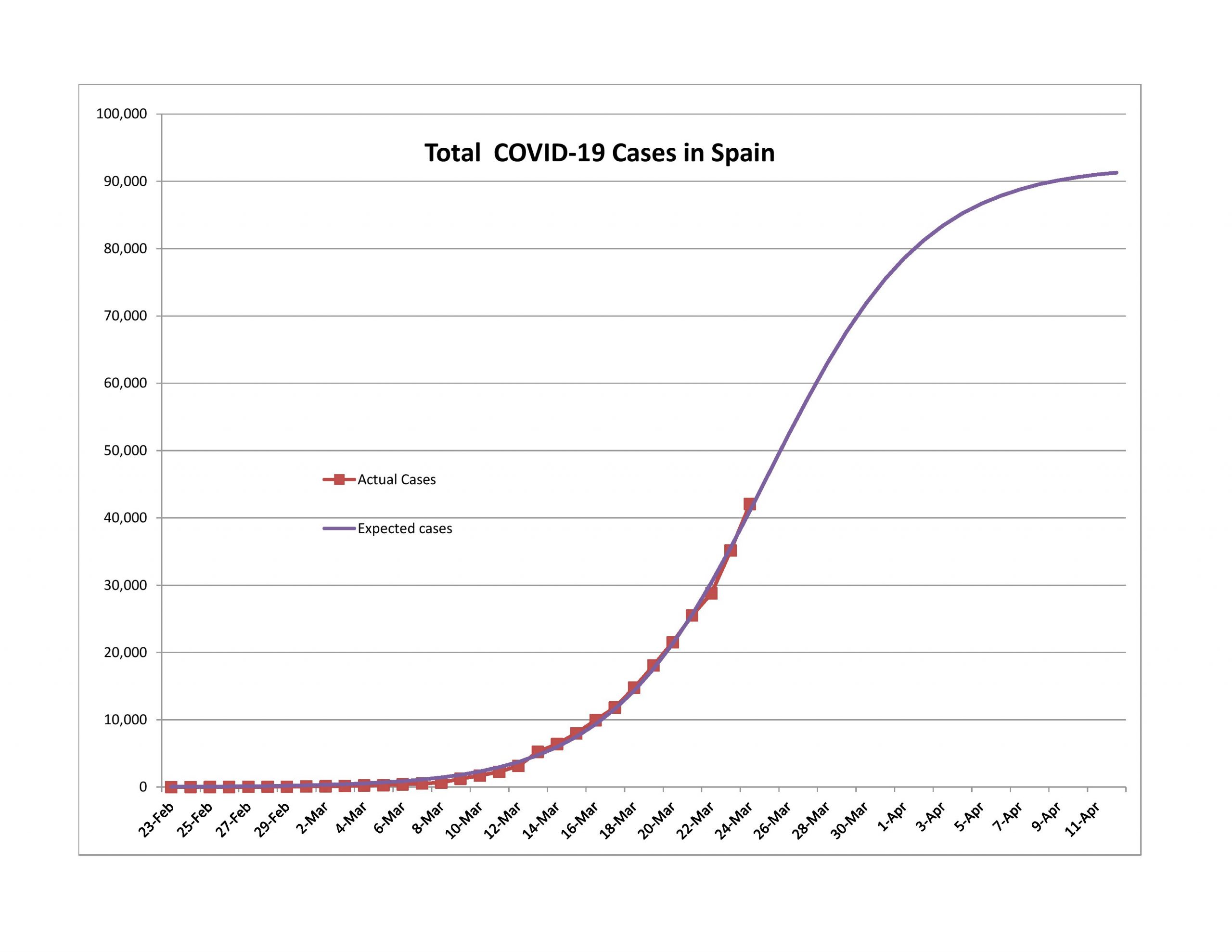

For Belgium, Germany, Netherlands, Portugal and Spain, new cases are declining, though not as rapidly as the model would predict. Even with that, it seems likely to me that all will pass the 90% point within a week.

Problem Children

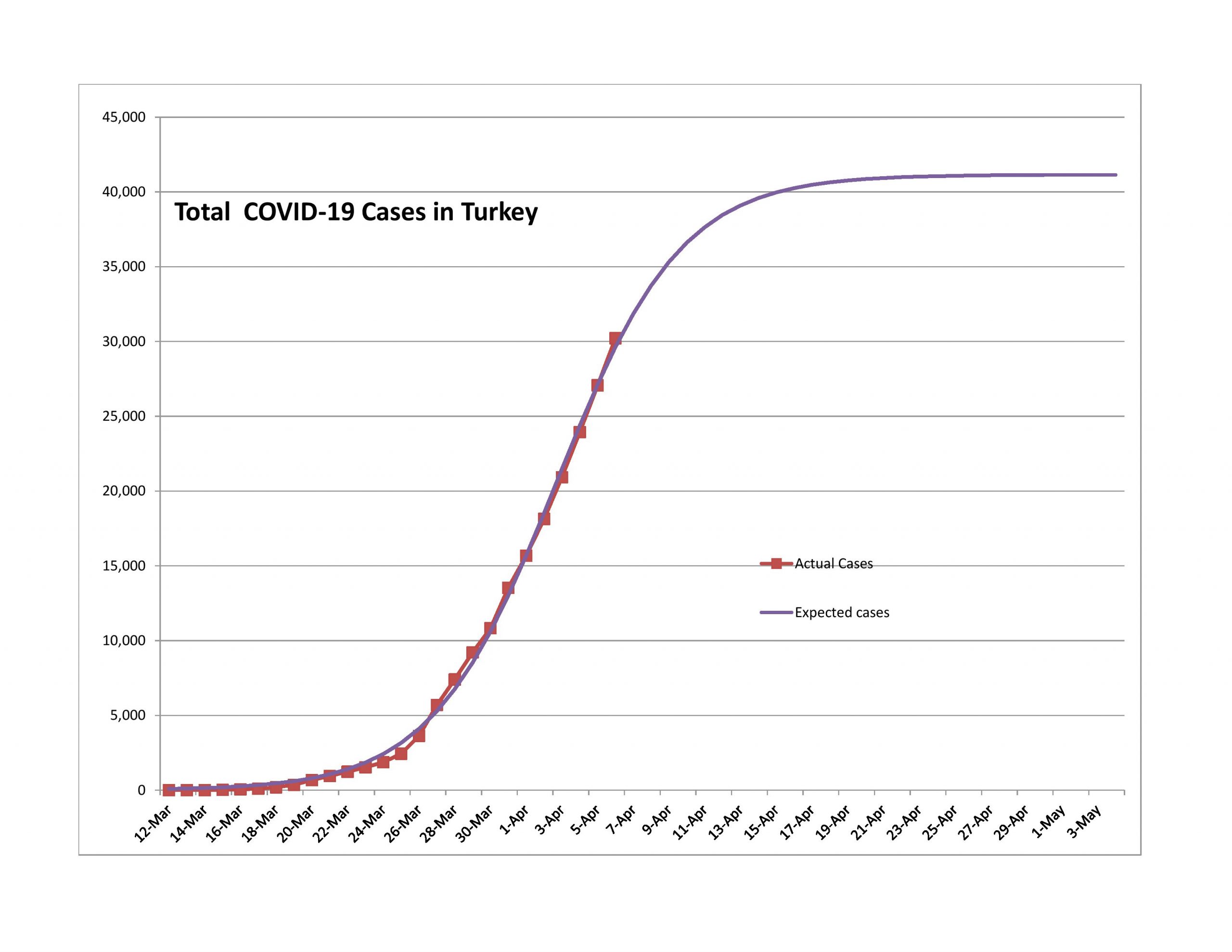

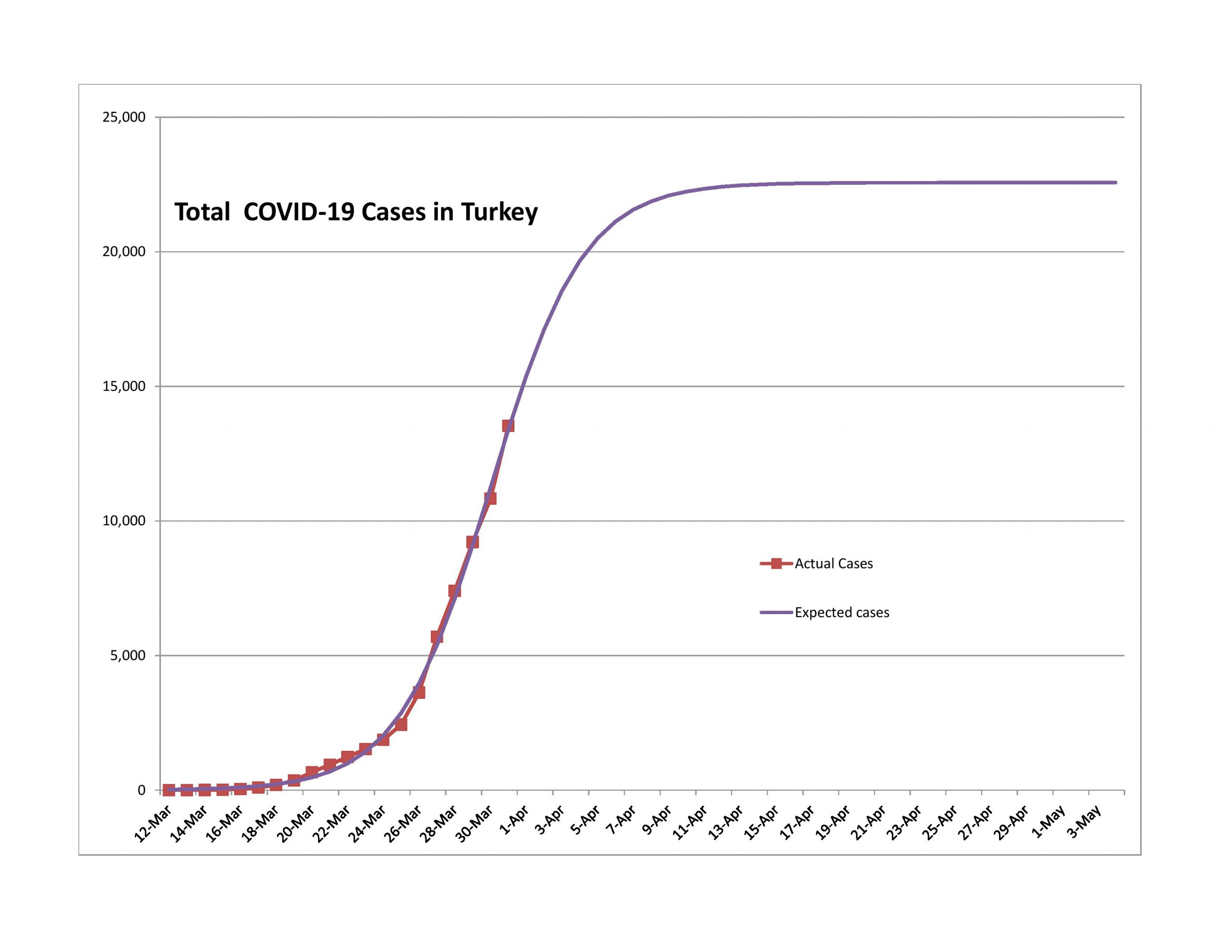

Turkey

My problem with Turkey is that the expected total population infected is too low. They got to the game late, and the curve looks too sharp. I would expect this to not turn as quickly as the model says.

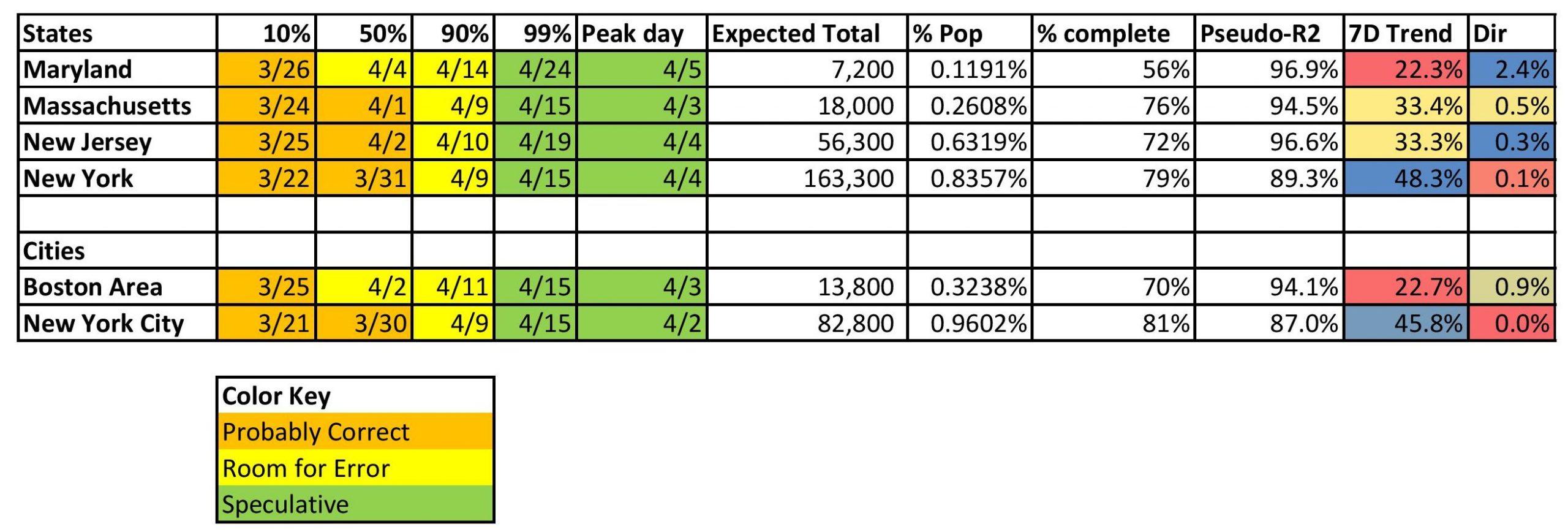

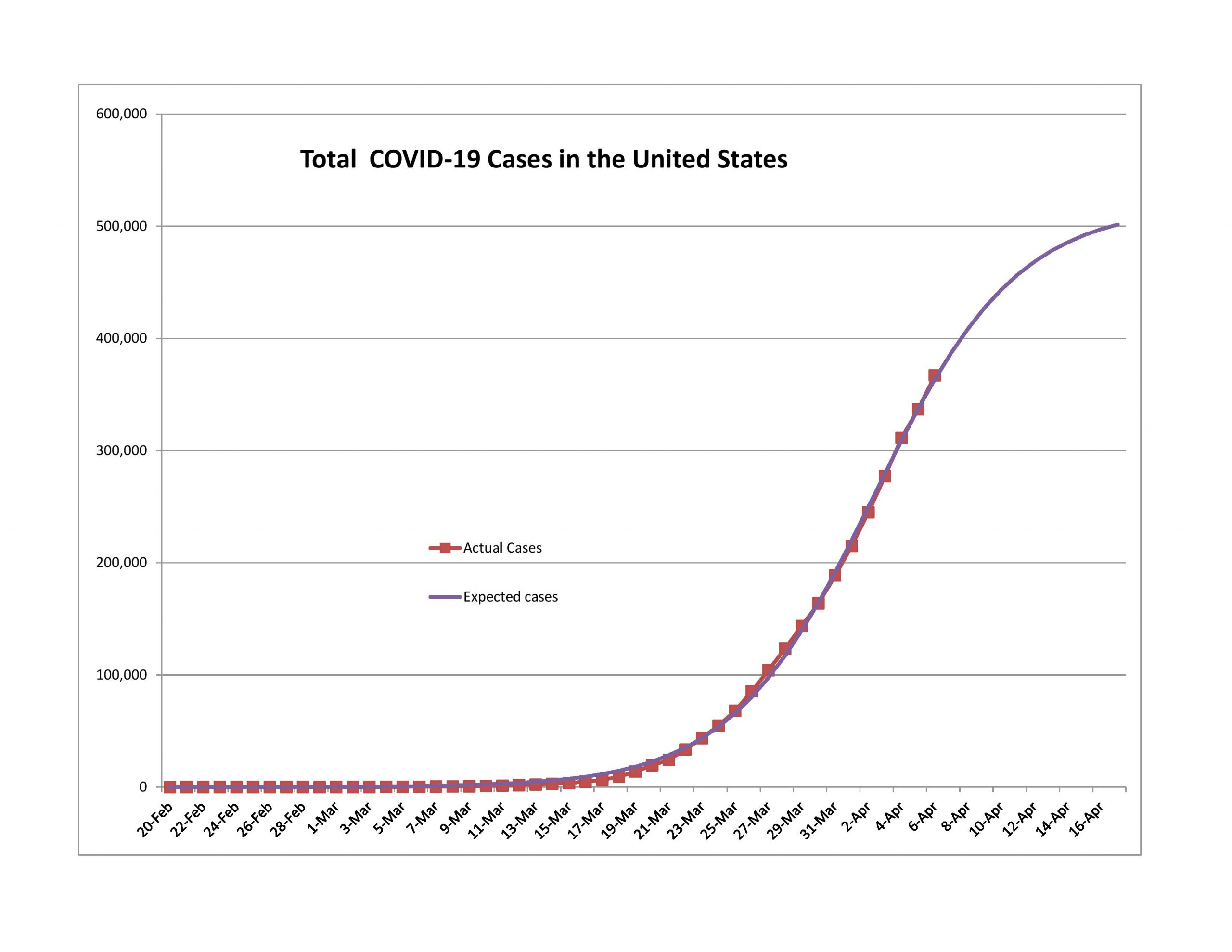

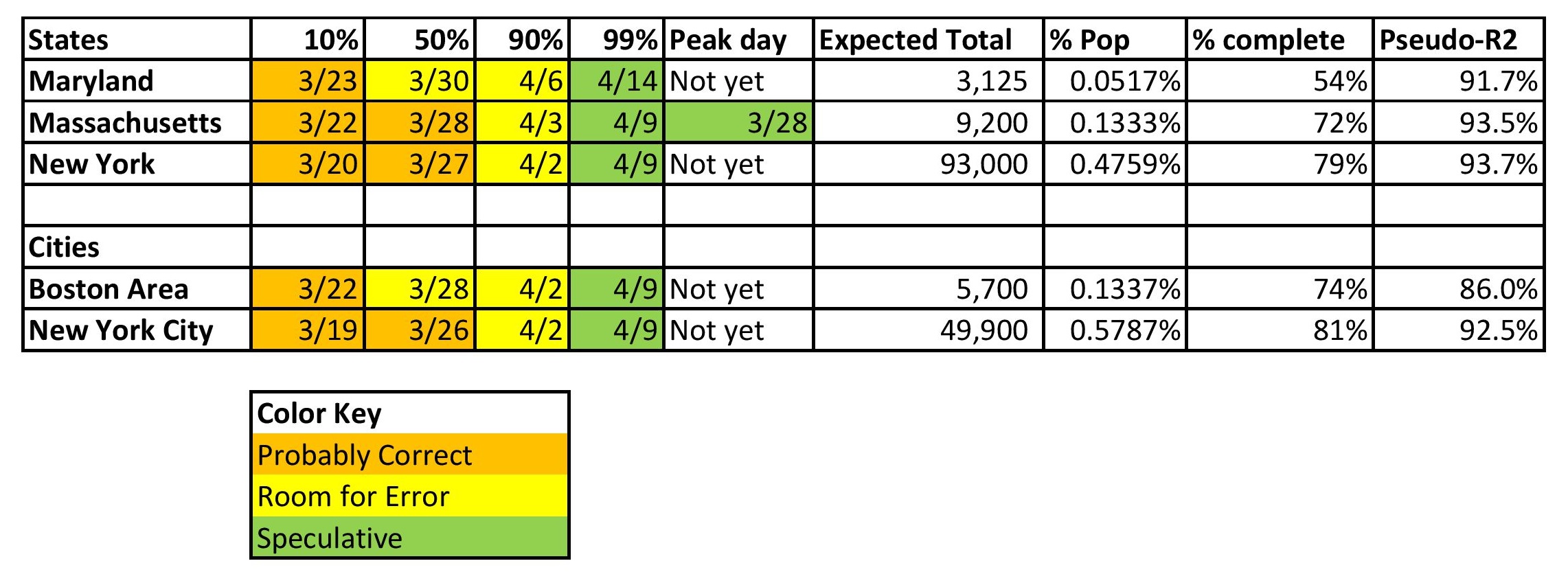

United States of America with some States and Cities

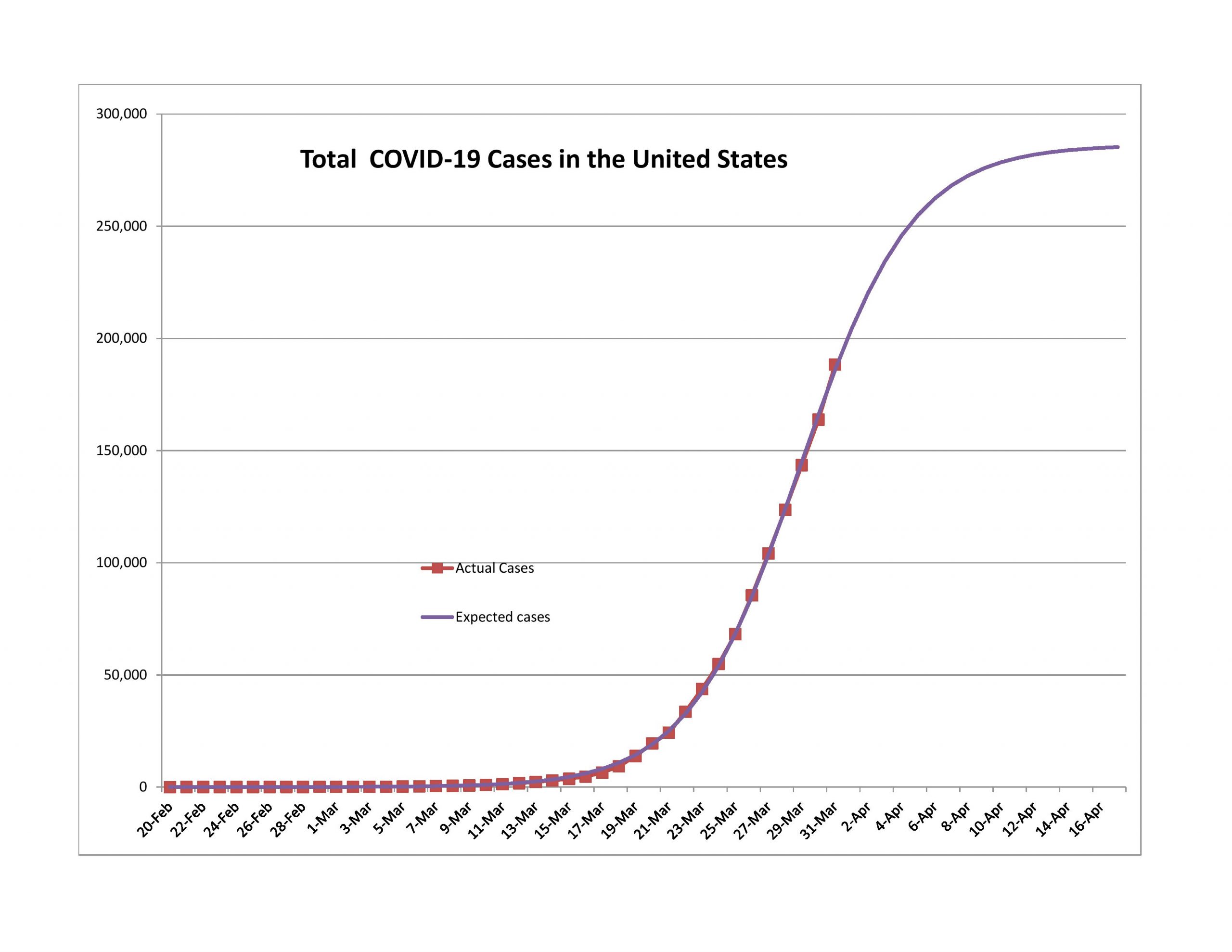

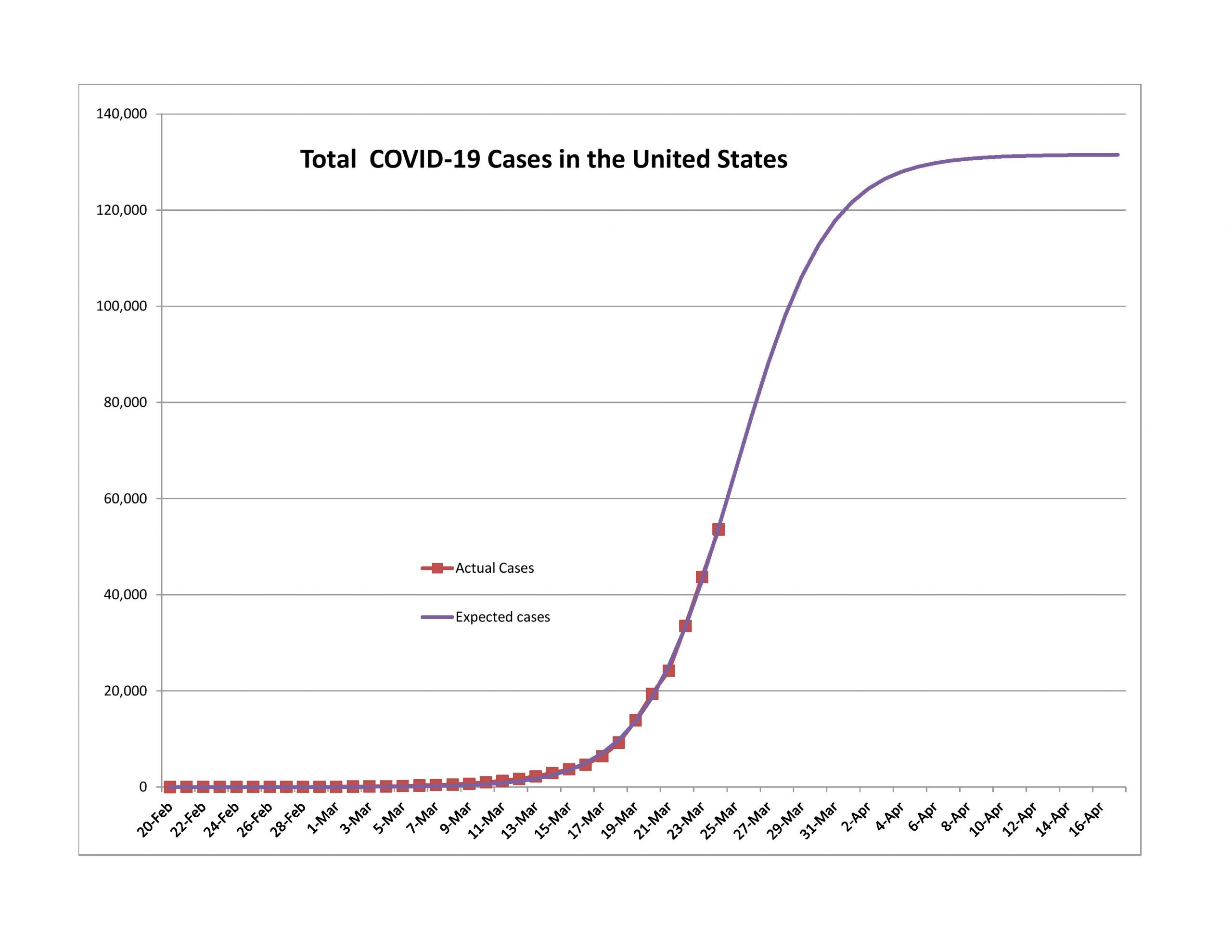

Yes, the USA has been slower than I expected, and I think I have a good reason for it. I gained the reason while trying to model the world as a whole for the COVID-19 pandemic. Using the logistic equation as my functional form, I could not even in the slightest achieve a positive pseudo-R-squared. Why?

If you add together a bunch of logistic curves with varying timing, height and sharpness, there is no guarantee that you will end up with a logistic curve. The US is a big place, and the population is spread out, with many different large population centers. Much as would have killed me timewise unless I had better software, I think it would have made more sense to model the US as a bunch of logistic curves state-by-state, and add them up.

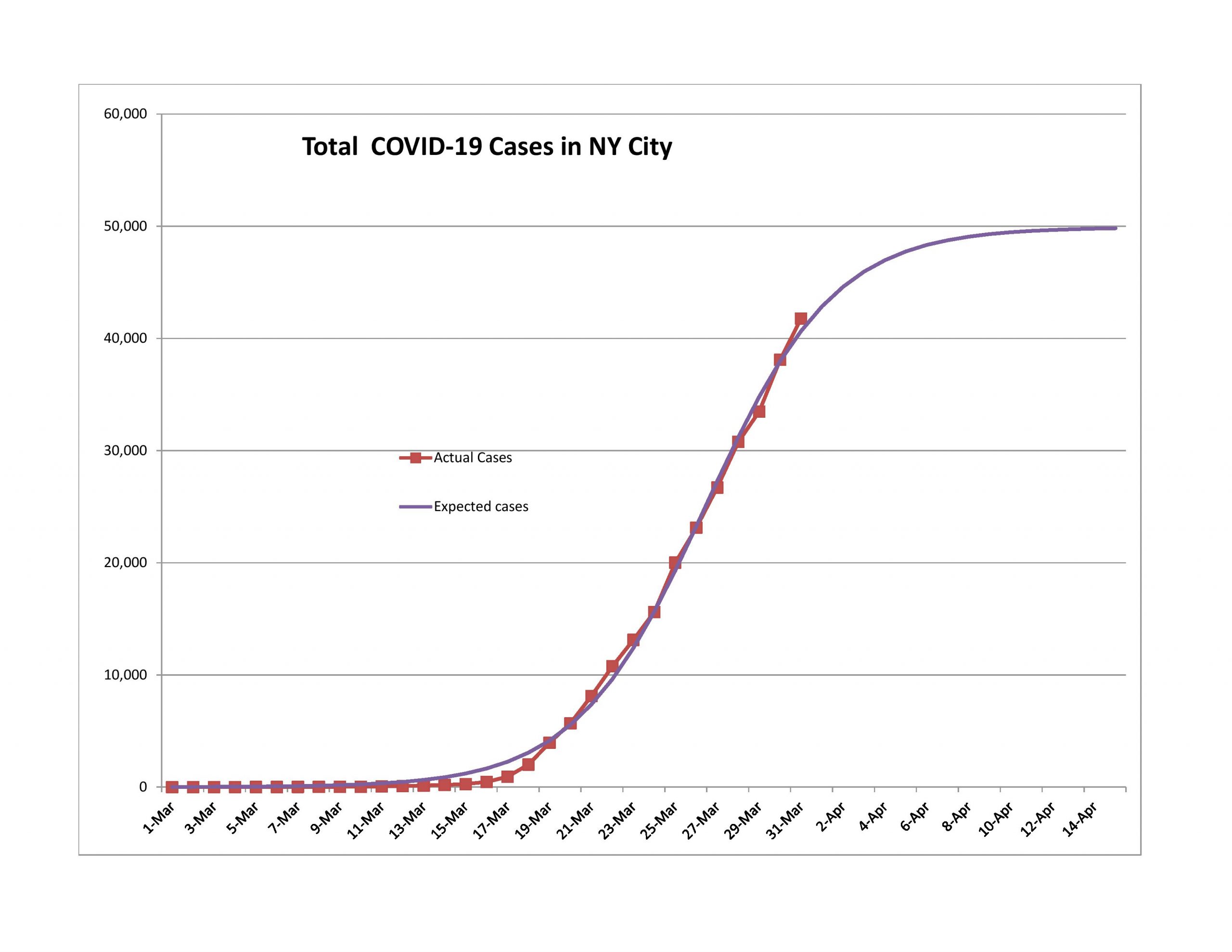

Here’s a demonstration for the past week: if I take the forecast errors of New York State and New Jersey, they are roughly 65% of the forecast errors for the US as a whole. Together they have 47% of all reported COVID-19 cases.

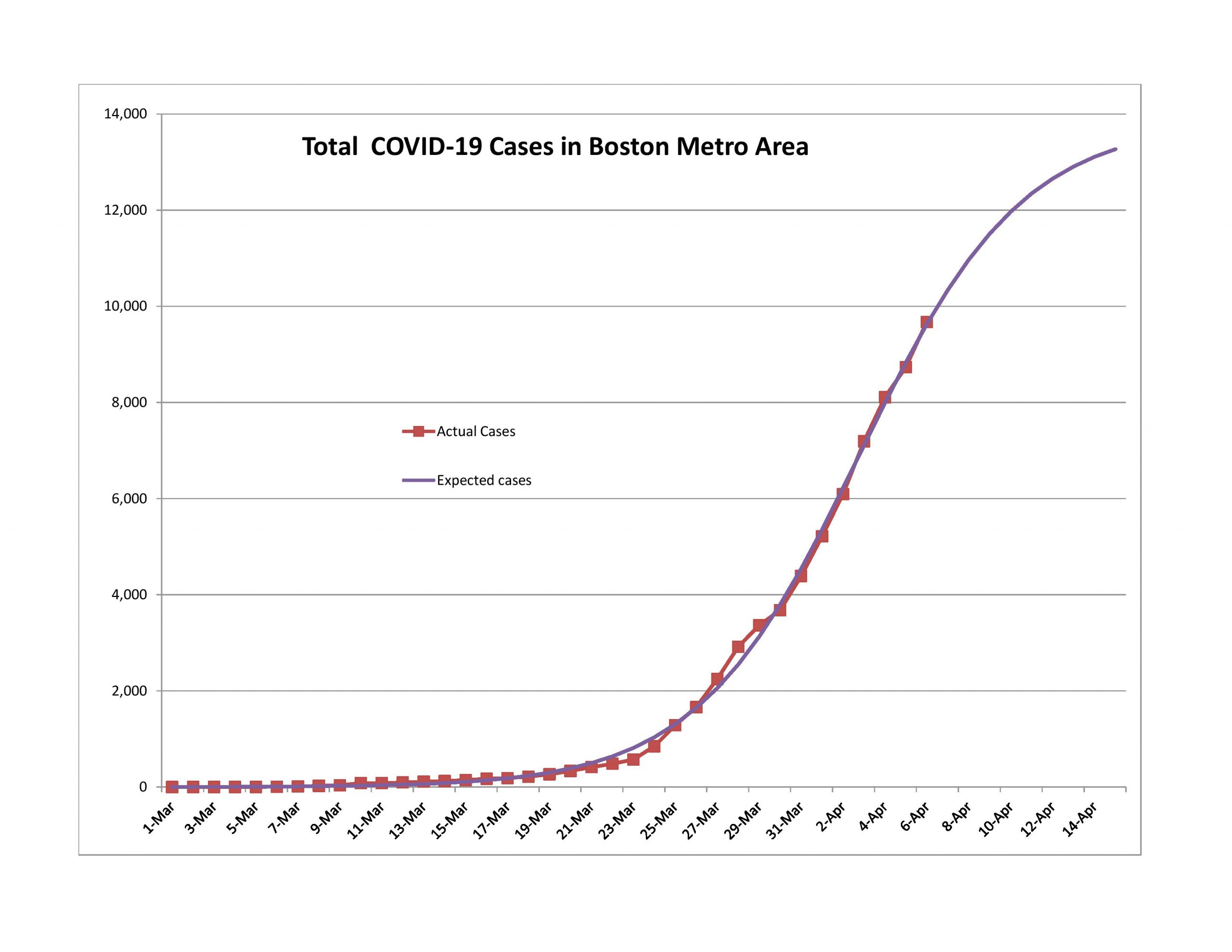

There have been statements by some politicians that there will be a lot of new “hotspots” across the US, it’s a tempest in a teapot. The dense and large cities like New York City and Boston have a lot harder of a time preventing the spread of an epidemic. Areas that are smaller and less dense won’t have the same impact, not even proportionate to their sizes.

The US has been making progress, just not as fast the model predicted. I would be surprised if the US weren’t at the 90% point by what is normally tax day. It takes three weeks or so to get from 10% to 90% and another week or two to get to 99%. We will likely see the practical end of this in April. It’s just a question of when.

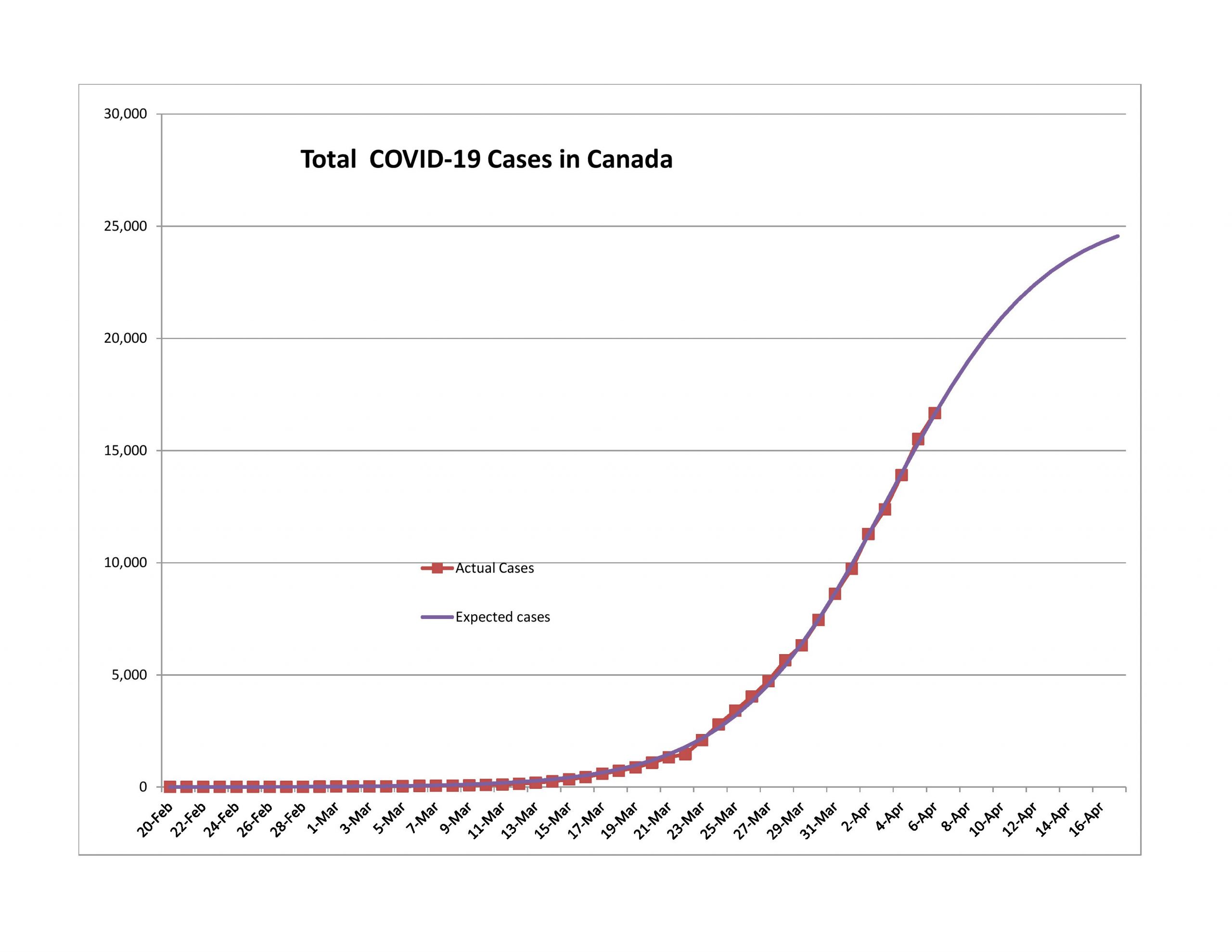

Canada

I place Canada in the same boat as Turkey. Too few ultimate cases. It will likely revise upward. That said, their population is more spread out, so it will likely have fewer cases per capita than the US.

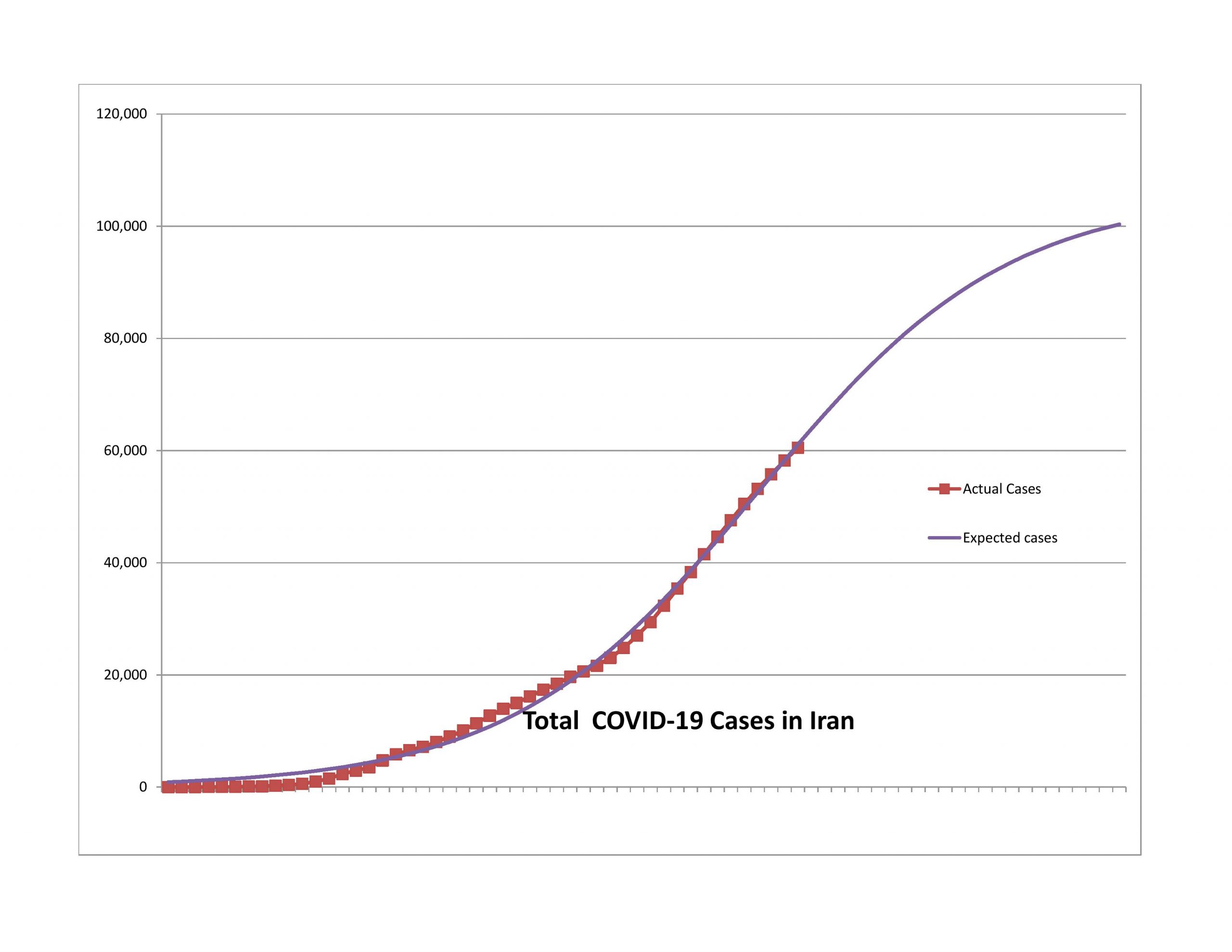

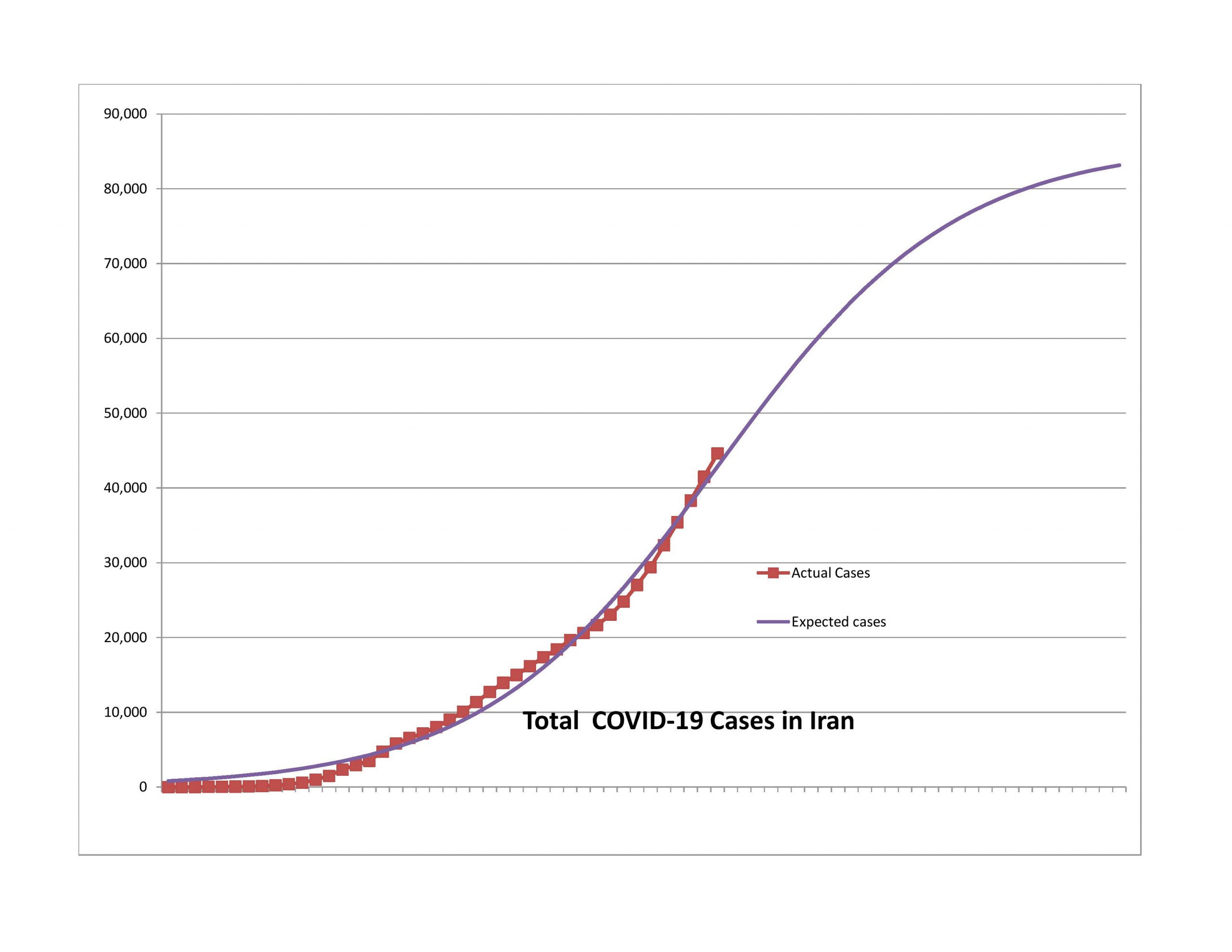

Iran

After several weeks of having claims far higher than the model would predict, the curve for Iran has regained a normal shape. The expected ultimate number of reported cases is on the low side of reasonable, and the model is finally tracking well. This is a watch and see sort of thing because of the instability in Iranian society, particularly amid the epidemic.

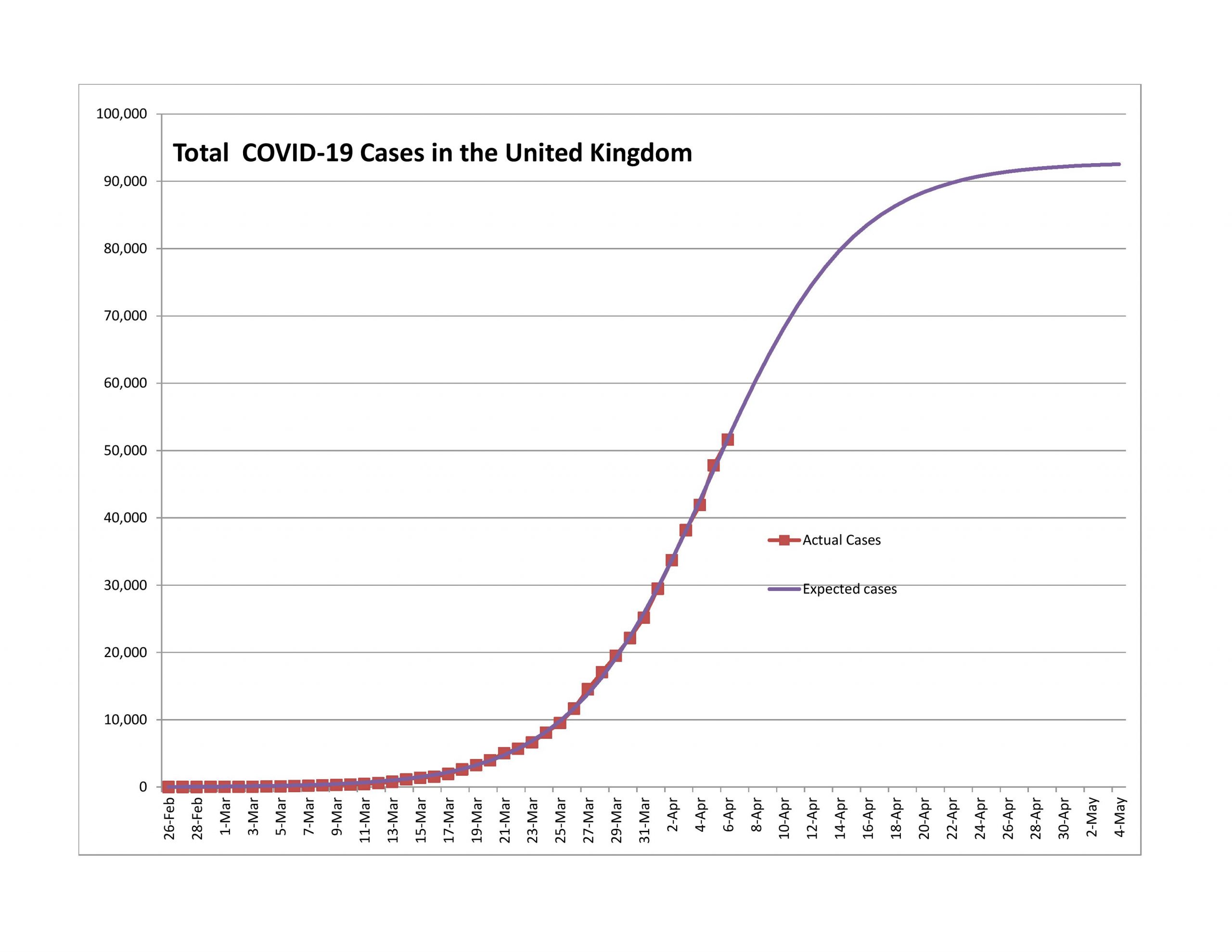

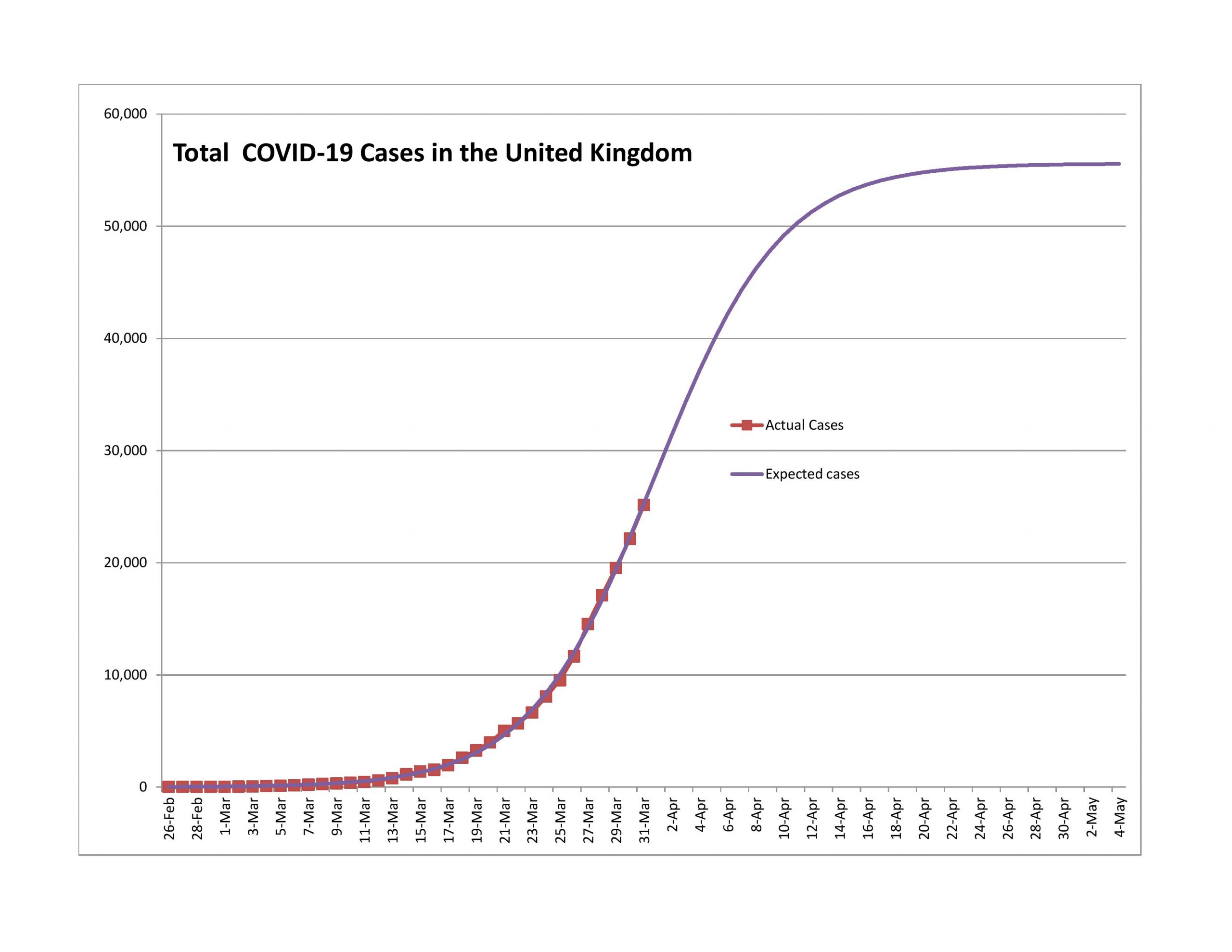

United Kingdom

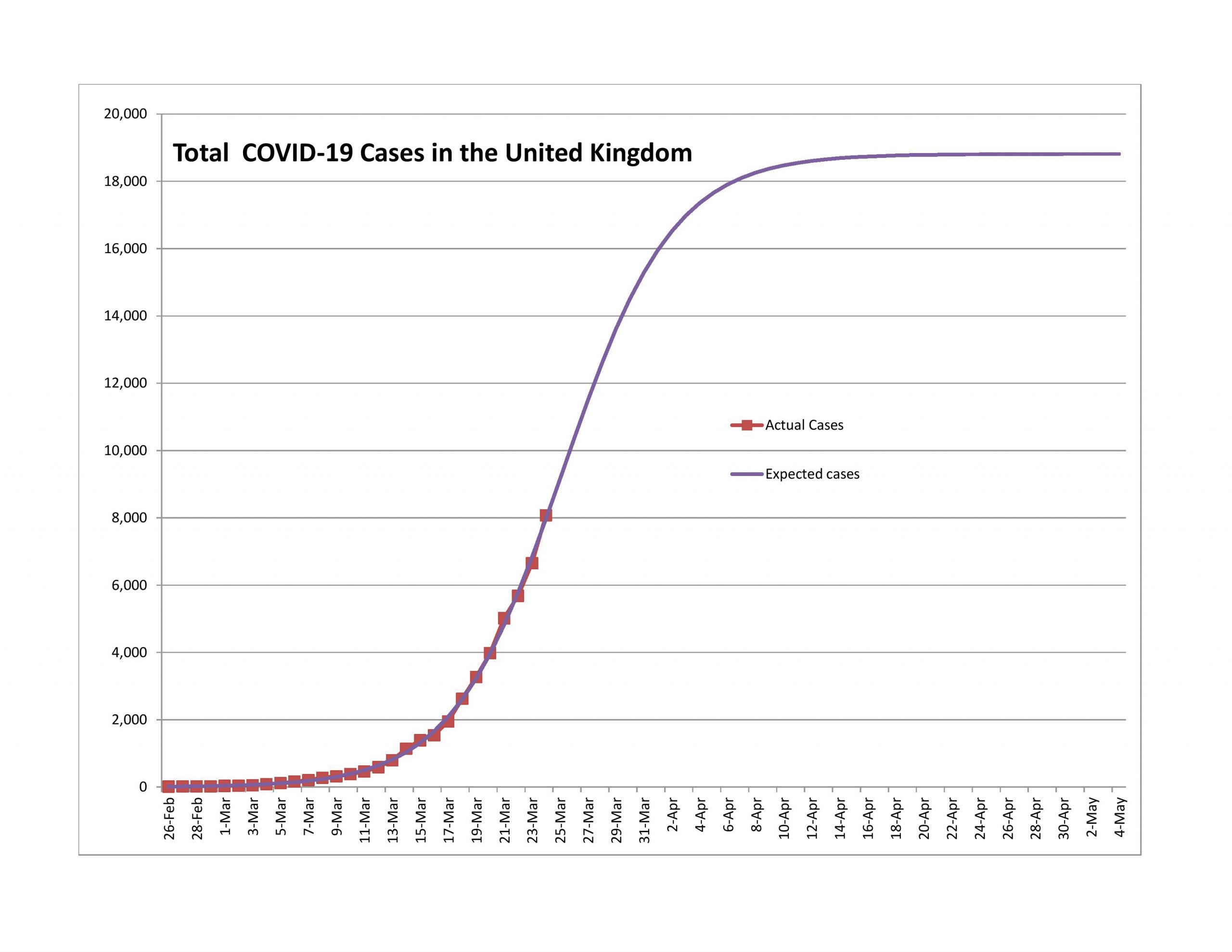

The UK is on the same path as the USA, only 5-11 days behind. Their new case rate is decelerating slowly, but it is decelerating.

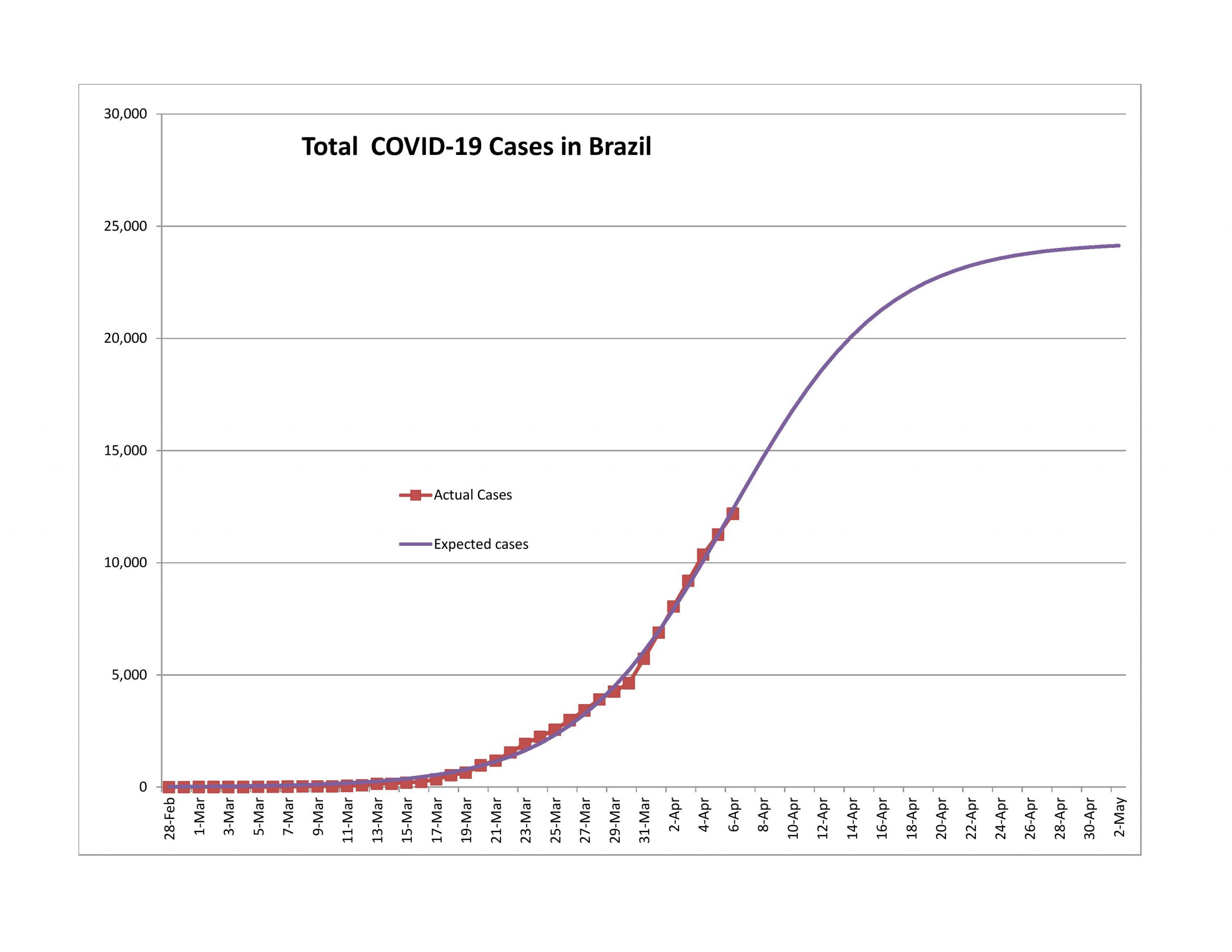

Brazil

The expected ultimate number of reported cases is too low, and the model is too new. Conditions in Brazil are less than orderly, so I would expect this model to revise significantly upward.

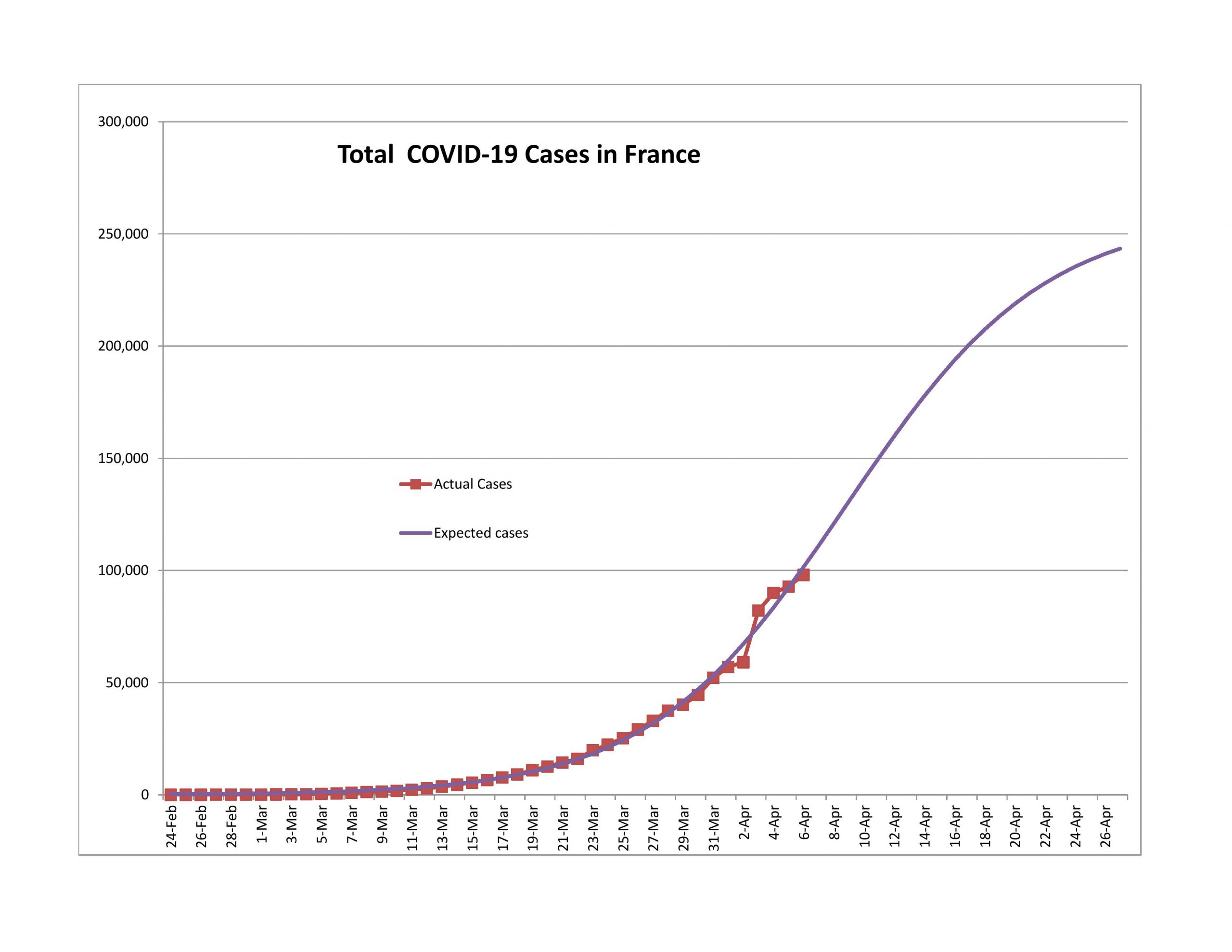

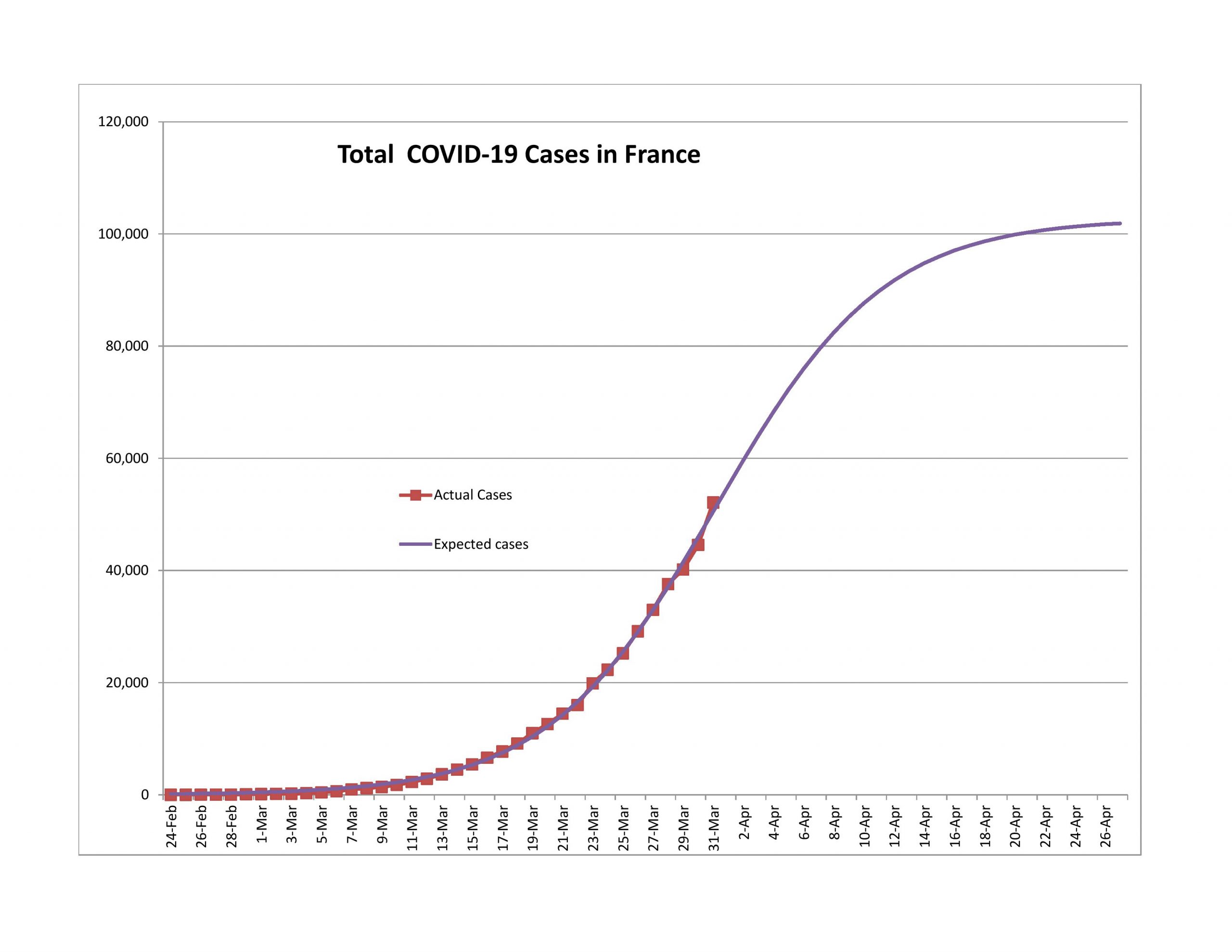

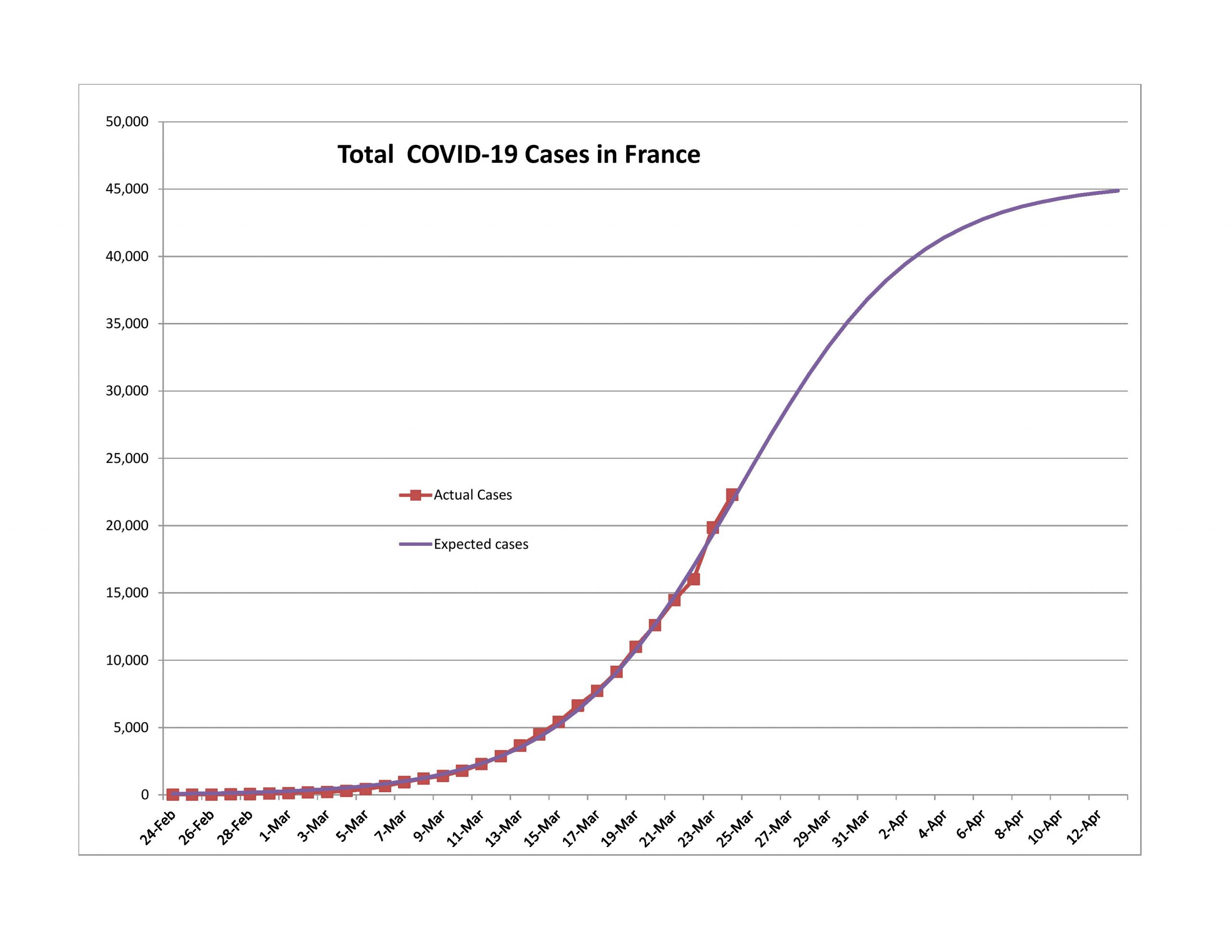

France

On 4/3 of the French government announced that they had only been counting deaths in hospitals and as such reported 23,000 new cases. Since that time the model for France has been posting negative forecast errors, and is slowly returning to a normal shape. I would expect in a week that the curve will look normal, and that the crisis in France would end about the same time as for the US.

Closing

That’s all for now. For those talking about these posts on Facebook, please note that I don’t interact there much. It’s best to comment at my blog or email me if you want my attention.

PIcture credit: Aleph Blog, and the same for all the graphs and charts in this post. All liability for mistakes here is mine.

Recommendations and Comments

To the National Governments and Central Banks: don’t create a lot of policies that you might need to reverse. This crisis is coming to an end faster than most are reporting/proclaiming. If a policy is easily reversible, get ready. Start planning for dealing with the second wave of the pandemic.

To US State Governments and city/county governments: start figuring out how you will targetedly let up on the restrictions that you have imposed before you realize that you are behind the curve (again). Start planning for dealing with the second wave of the pandemic. It would be better to let younger people go back to work, and shelter those more likely to get a deadly case of COVID-19. (Aside: if this ends early, note the people who told you that it would long and big, and remove them as advisors.)

To the media: please calm down. This is one of those situations where it gets worse before it gets better. We are through most of the worse, but to the average observer, they don’t see the better, even though the point of maximum pessimism has passed.

To individuals: if you don’t have a lot, take heart that this first wave likely won’t be here much longer. Use your money carefully. To those who do have money, as a nation moves from 50% to 75% complete in the first wave of the virus, it might be a good time to own a little more stock. I don’t usually encourage speculation, but it might be warranted here. Remember, don’t invest anything you can’t afford to lose.

Last, my models last week were too optimistic, but not by much. The growth rate of total cases is generally dropping pretty quickly, but you couldn’t tell that from what you are hearing from politicians and the media.

Introduction

Before I start, I want to explain what the tables above and below mean.

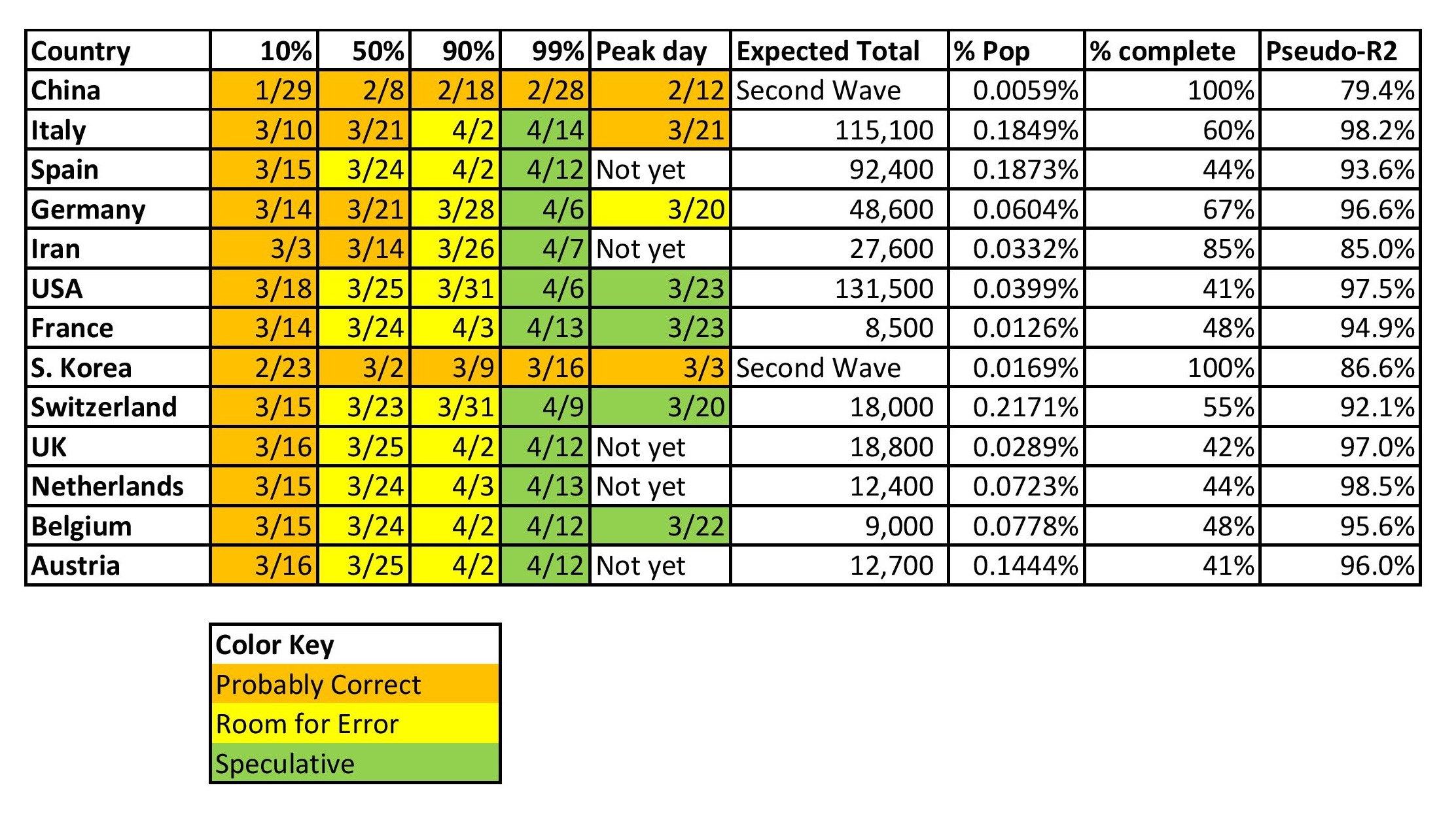

The figures underneath the percentages are dates. The dates are estimates of when the country, state or city will have experienced 10%, 50%, 90%, and 99% of the total COVID-19 cases that they will experience in the first wave.

The peak day is the day each has the most new claims.

“Expected Total” is my estimate for the total number of reported COVID-19 claims in the first wave.

“% pop” is the percentage of each population that will be reported as infected with COVID-19.

“% complete” is the ratio of estimated current total cases to estimated final total cases fo the first wave.

Pseudo-R2 is the percentage of the total variation in the total cases explained by my three-parameter nonlinear regression. Because the regression is nonlinear, it is not an F-statistic, and gives us only a spit-in-the-wind sense for how good the regression is. Some have asked if I could add error bands to my models and the answer is no, because the nonlinearity of the equation makes that difficult. I’m only working with Excel, and looking through my old Econometrics texts, they don’t have an answer for this one. Maybe I should start modeling in R.

You’ll note that I added six additional models to this post.

One country: Turkey (I am modeling any country that gets more total cases than S. Korea.)

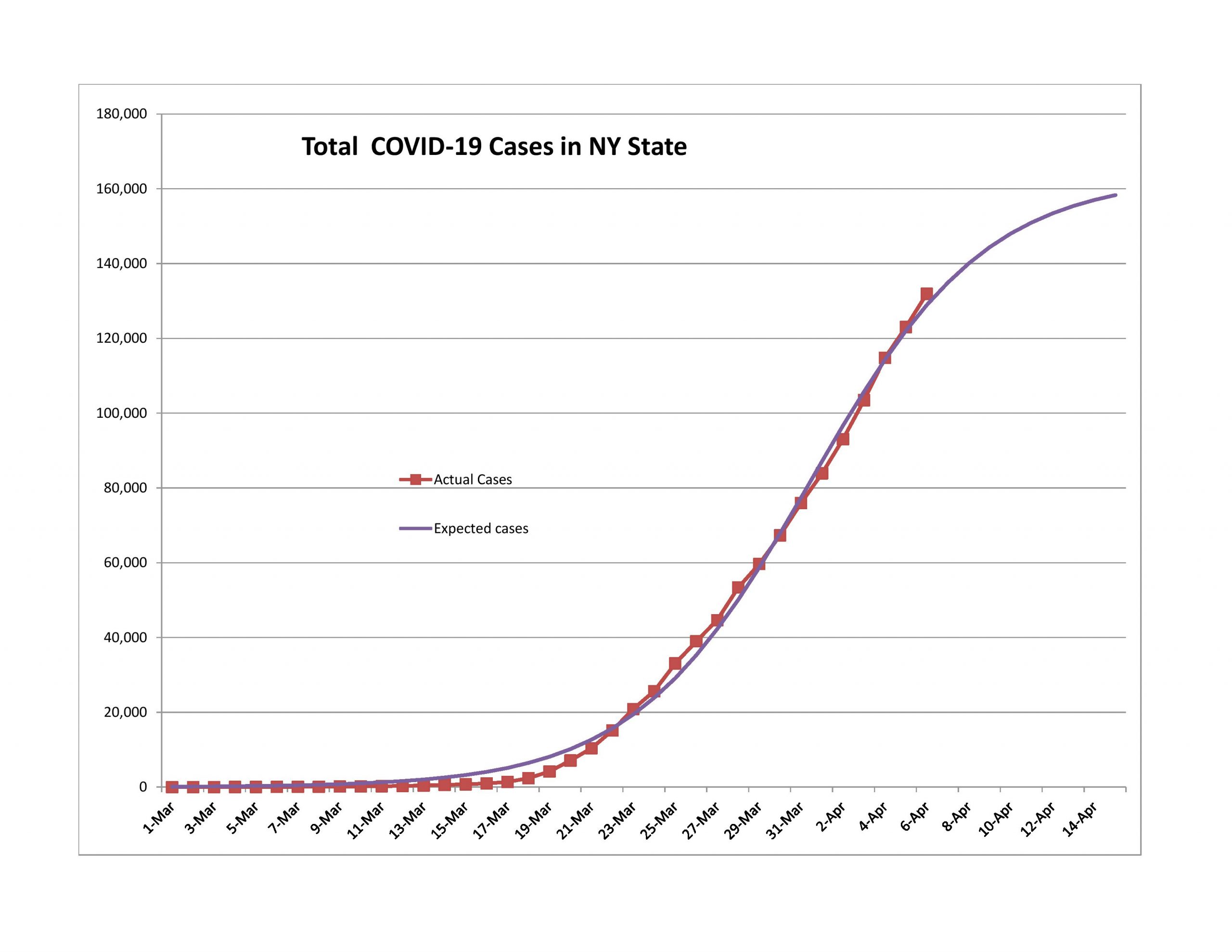

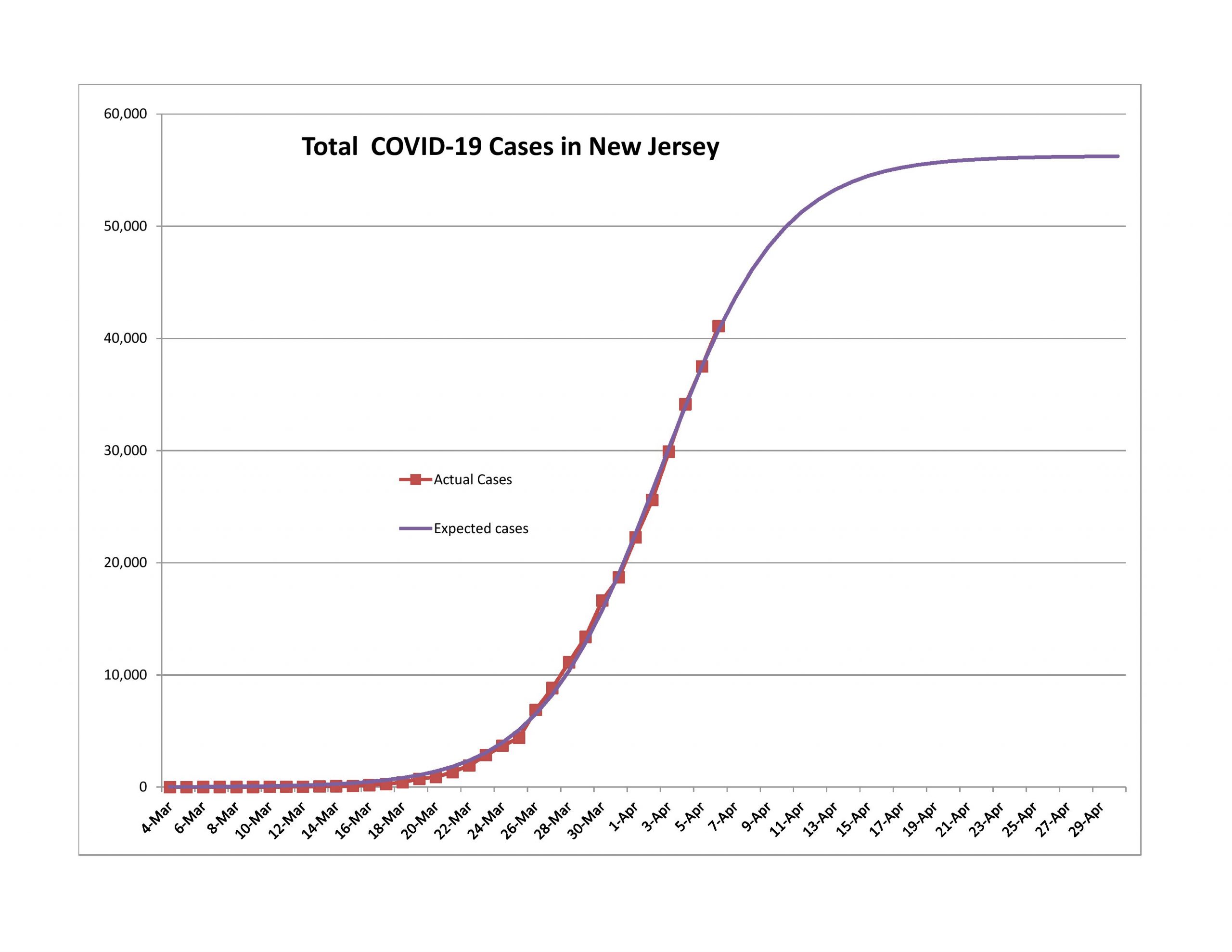

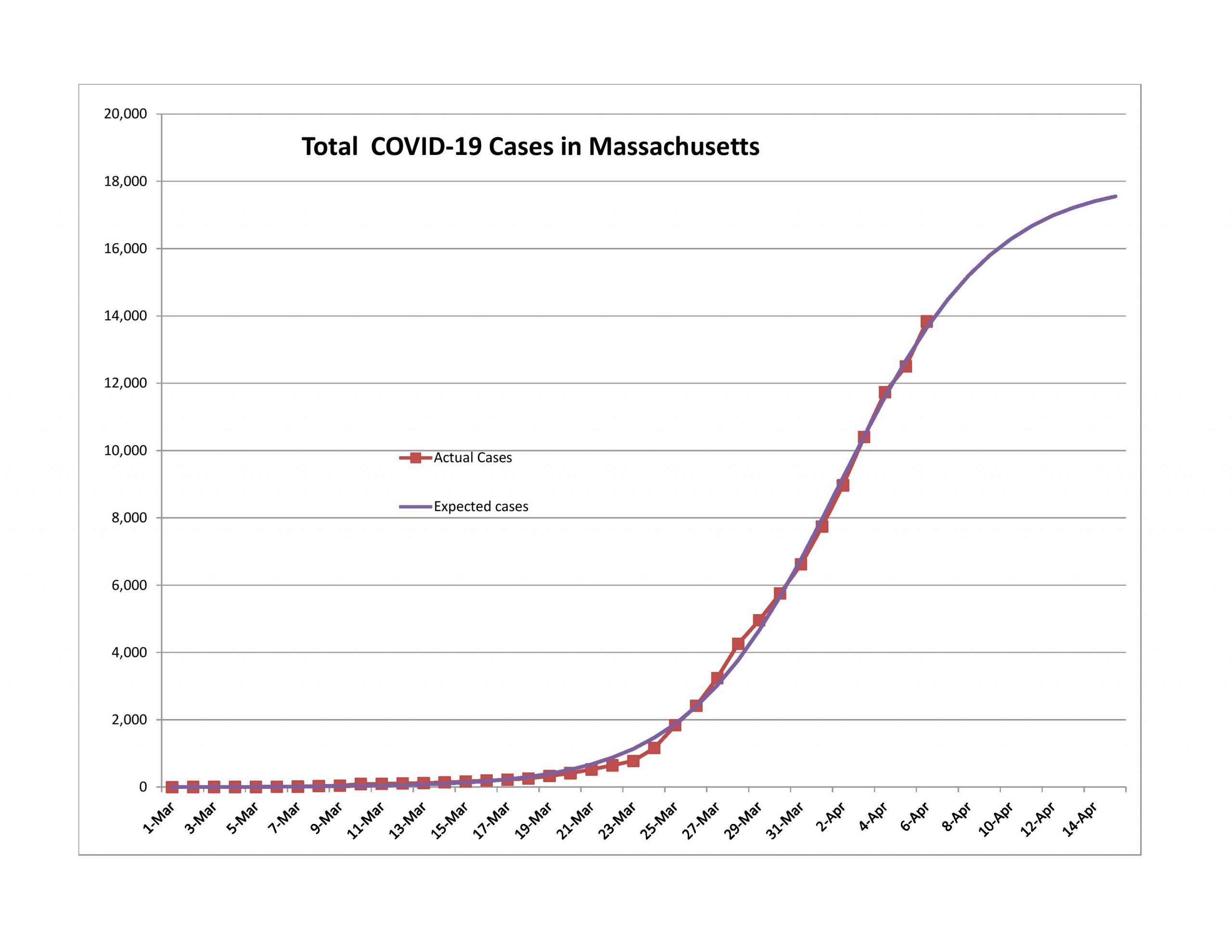

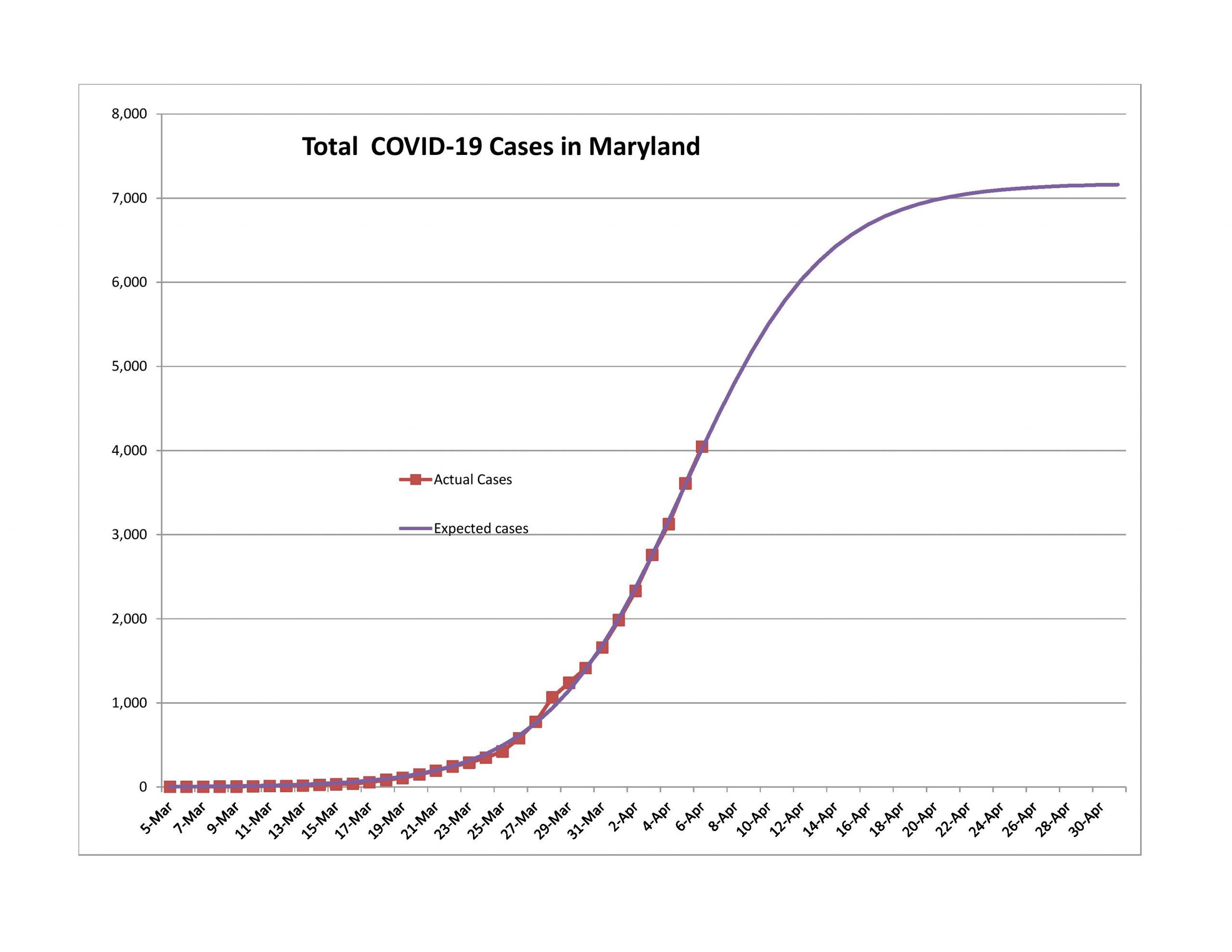

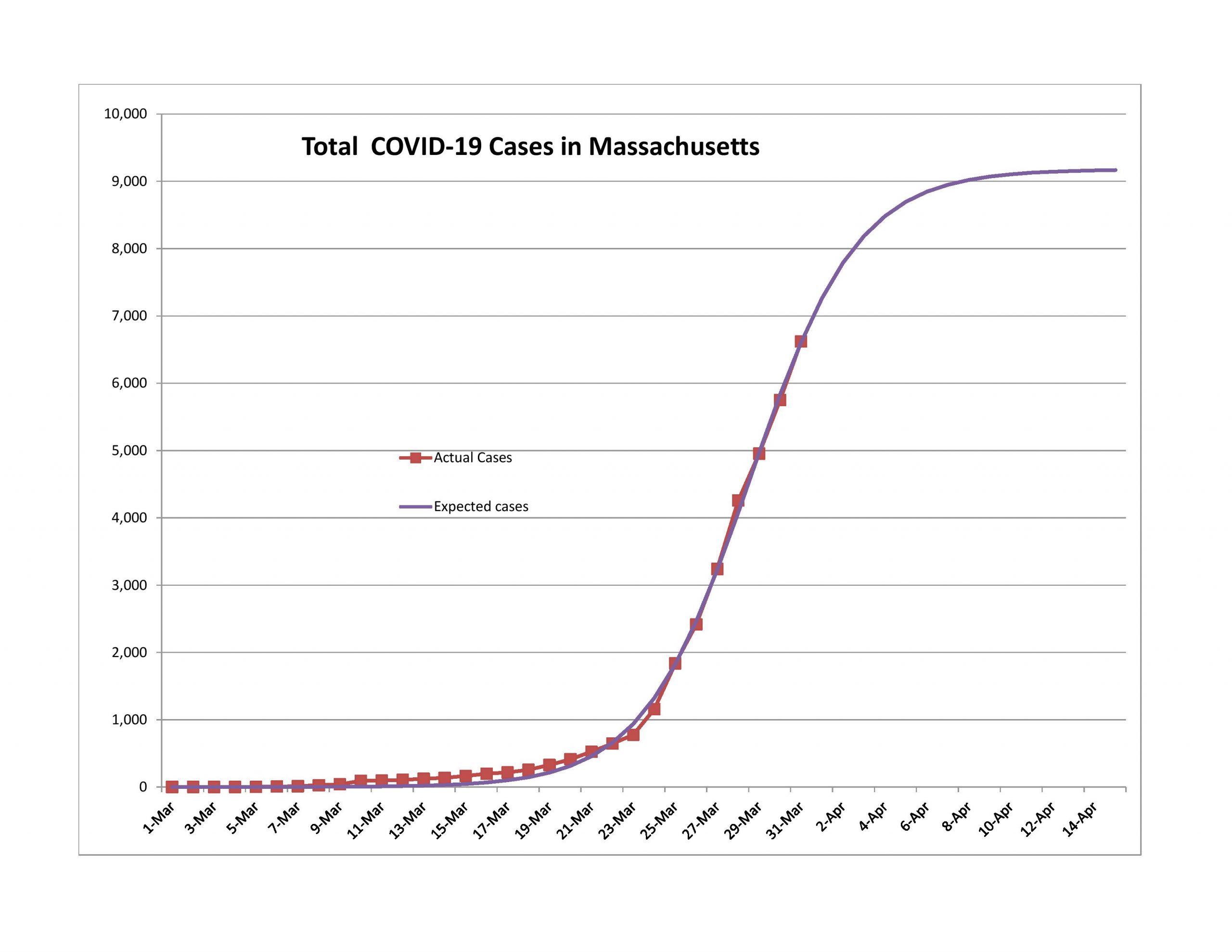

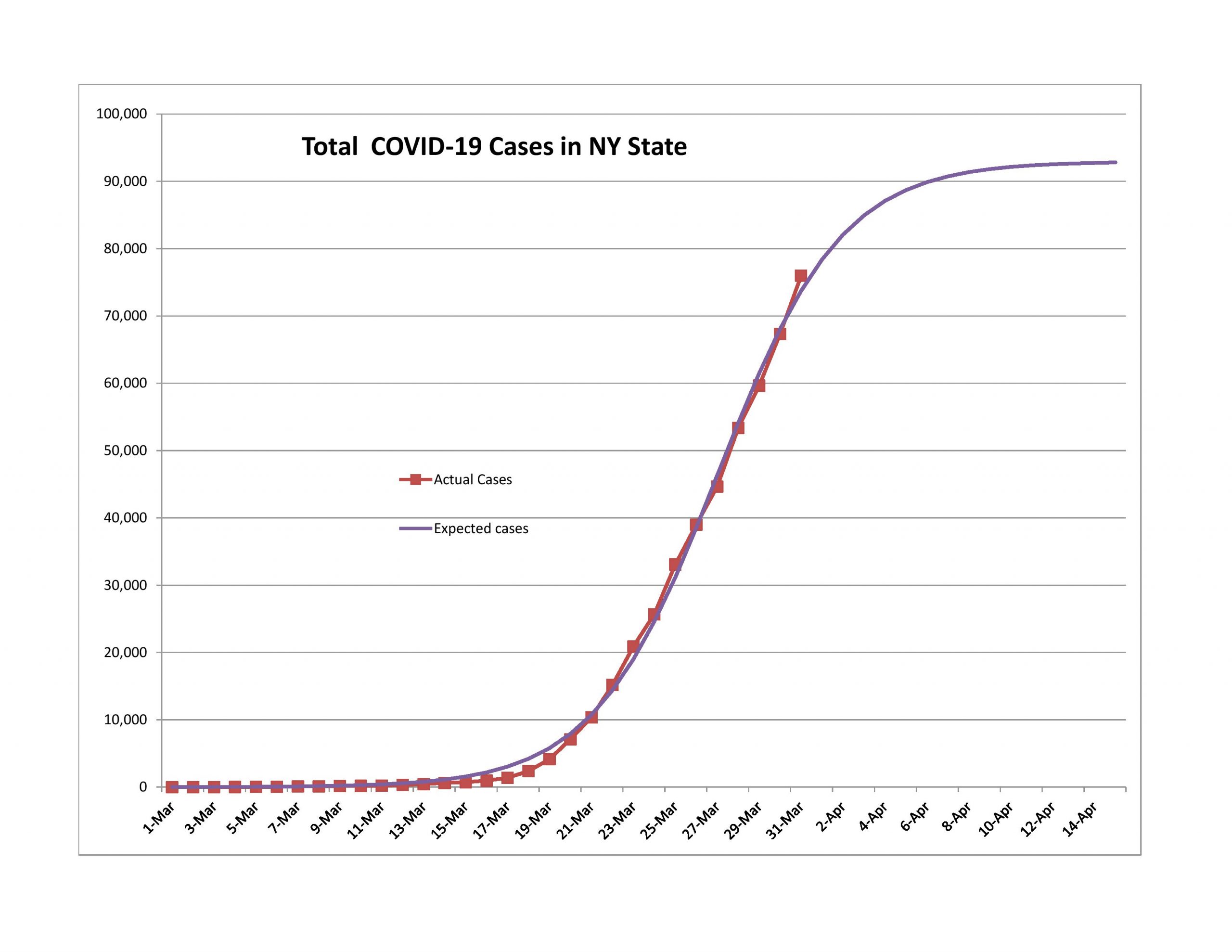

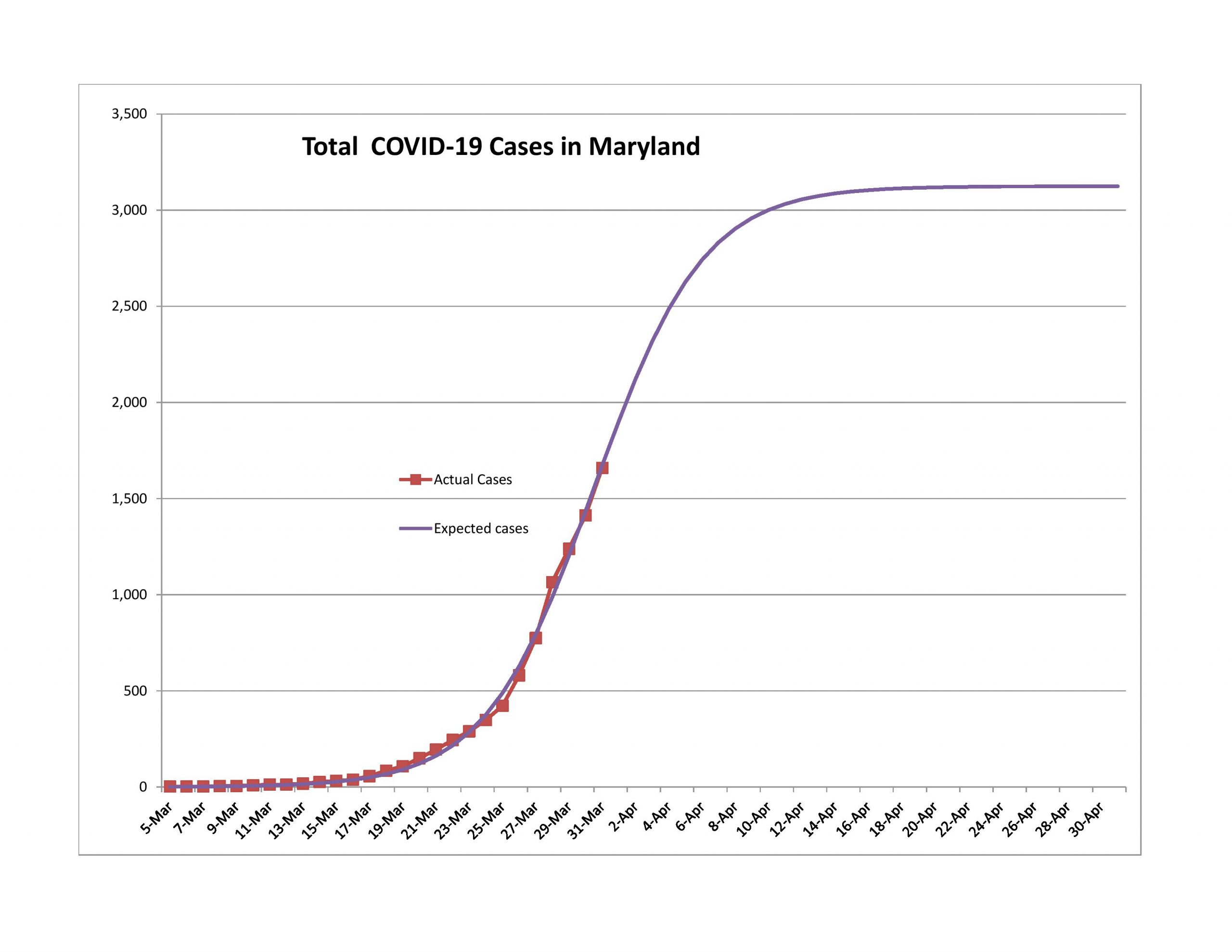

Three states: Maryland, Massachusetts, and New York. I’m modeling my home state, Maryland, Massachusetts for a friend, and New York because it has the most cases of any state.

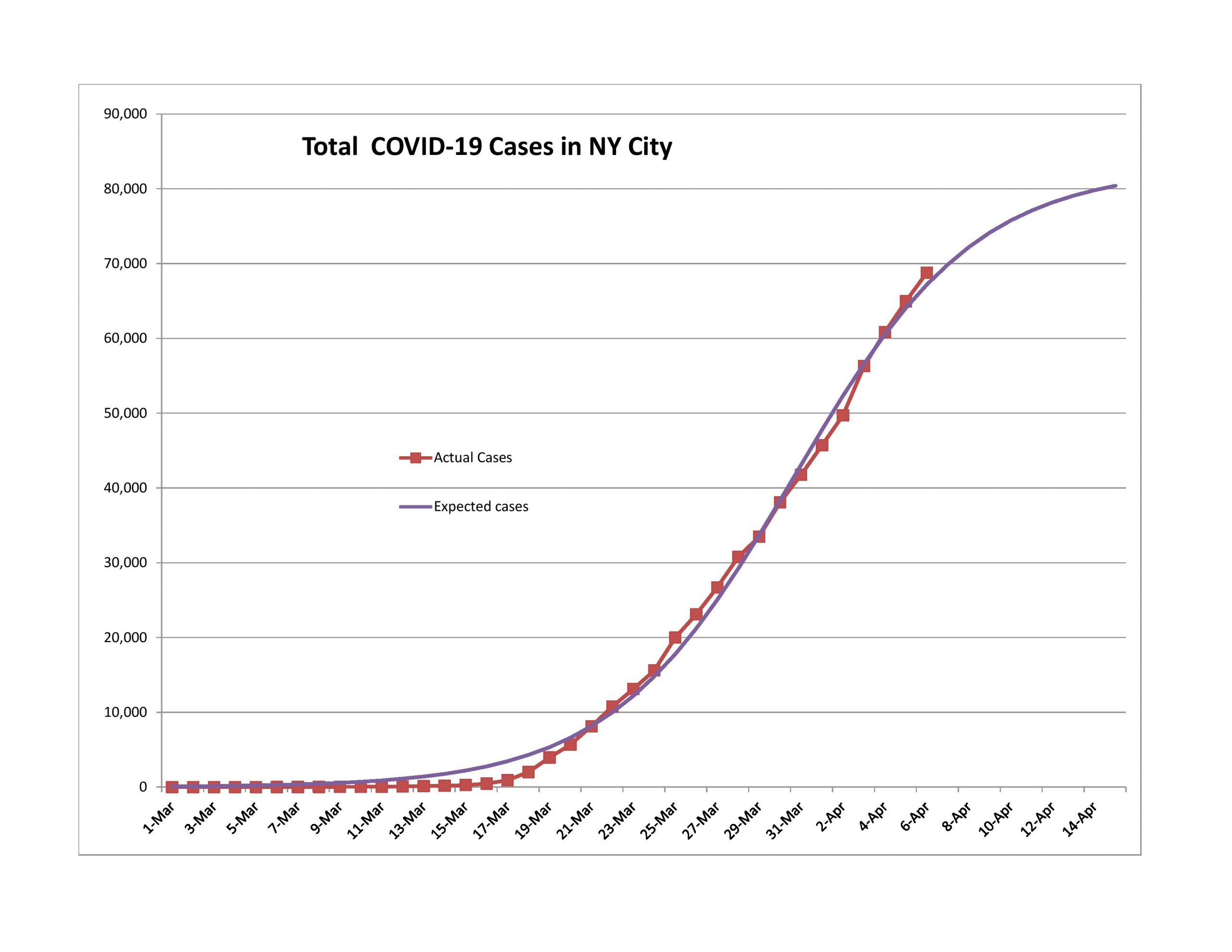

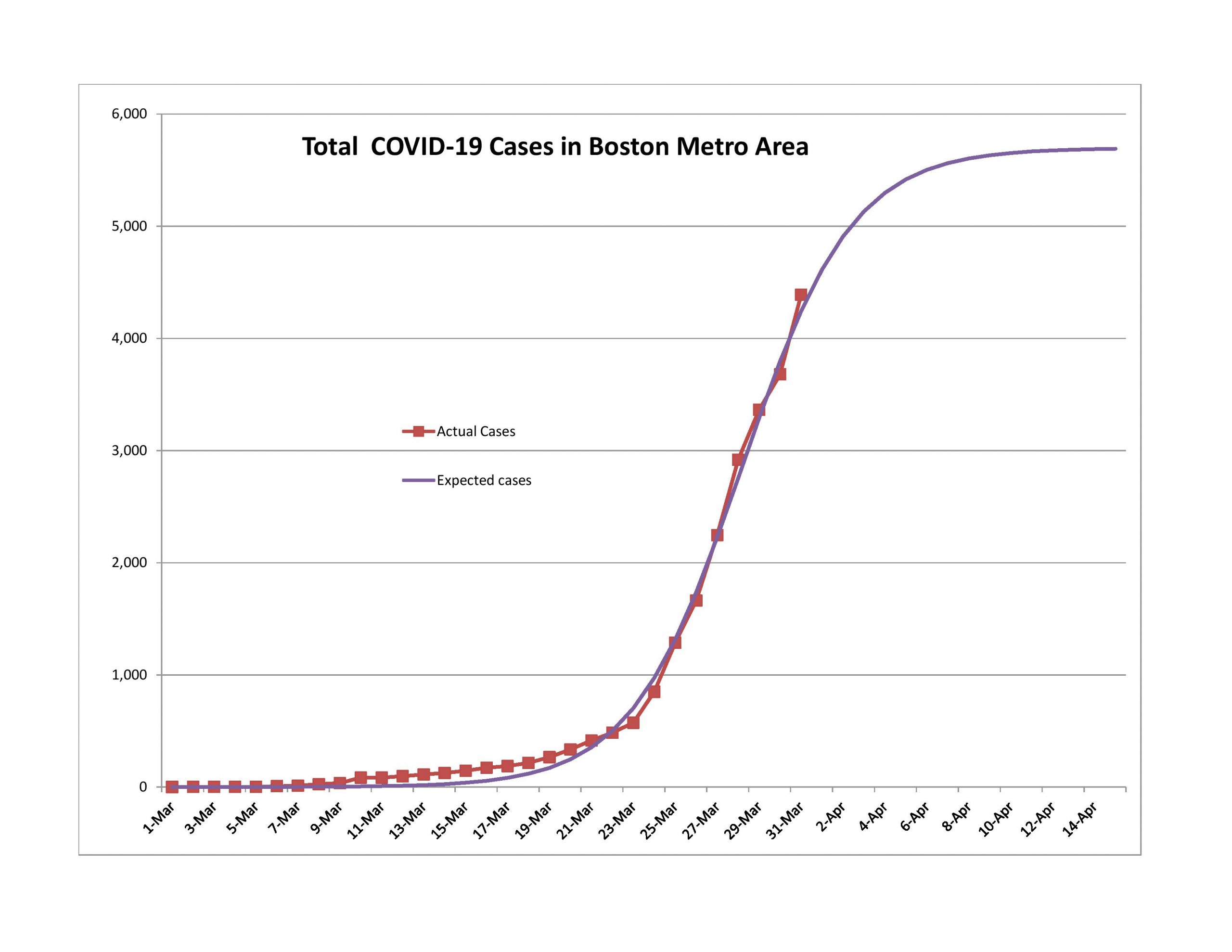

Two cities: New York City and the Boston Area, which is the five counties near Boston (Essex, Middlesex, Plymouth, Suffolk and Worcester). New York City, because it has the most cases of any city, and Boston, because of the aforementioned friend.

Data and Resources

Before I go on, I want to point out some useful sites for getting data and resources. If you think you have other useful resources, please post them in the comments.

Courtesy of the New York Times, you can get state and county total cases and deaths on a day-by-day basis. (Main page) (state data) (county data) Data is in a Comma Separated Values [CSV] file format.

Finally, you can look at my models if you like. Here’s the country model. Here is the states and cities model. Now you can look at what I am doing, and play with it yourselves. Note that you will have to activate the Solver application inside of Excel.

Limitations of what I am Writing About

I am forecasting one variable in each geographic area — reported total claims as of a given date. I am forecasting this for several reasons.

It is relatively easy to do. If I tried to estimate medical resource usage or even deaths, I would need more data that I don’t have access to in order to do reasonable models in that area. (Now that said, a hidden assumption of the analyses is that there is some regularity to how cases get reported. If that changes, the models will be less accurate.)

Reported total claims is a leading indicator for other variables of interest. In addition to those mentioned in the first point, total reported claims is a leading indicator for the economy, lifting of government restrictions, and the financial markets.

It’s not as if there aren’t complexities that could mess with an analysis like this. When testing becomes common, you might see total cases go up a lot from all of the asymptomatic or low symptomatic people who are suddenly found and are no longer infected. That sort of shift would give the appearance of COVID-19 taking off, when we realize that that data belongs to the past, even though it is reported in the present.

No one wants to say it, but there are tradeoffs involved in having governments be too ham-fisted in their regulations. Those regulations are impoverishing a lot of people, and many of the restrictions are not needed in order to have the same level of societal safety.

There are also tradeoffs of life and money… and this is not new. Life is precious, no doubt, and money can often be replaced, but where does the money come from? Would it be right to be Robin Hood and push 100 unrelated people out of work in order to save a life? Perhaps it would be better ask for volunteers. It would be more ethical for the government to raise taxes, than to put on restrictions that harm the economy a lot, with few additional lives saved.

This is an economics, investing and finance blog. I focus on those matters. It’s not a healthcare blog. When I think of my average reader, that person is not thinking a lot about the problems from medical resource shortages, except perhaps the lack of ability to test for COVID-19. It’s different if you are in the medical profession or if you are sick. You would care a lot about these issues then, and my heart goes out to you, because you are having a challenging time with short resources.

As an aside, when you think of medical efforts in the US generally, with the emphasis on trying to manage costs, hospitals and inventories of supplies and equipment are light because in normal times, those were easy places to save money. Few would complain much (except closing rural hospitals) because there would be enough resources under 99%+ of all circumstances. This is fine, until you experience the low probability and high severity event. This is common to other disaster scenarios as well — there is often a complaint over lack of redundancy or robustness of some resource. (Not enough policemen, firefighters, ice, electricity, phone connectivity, emergency shelter, etc.)

I am not saying my analysis is the whole enchilada, but it is an important part of it. And with that, on to the graphs:

Past the First Wave, in the Second Wave

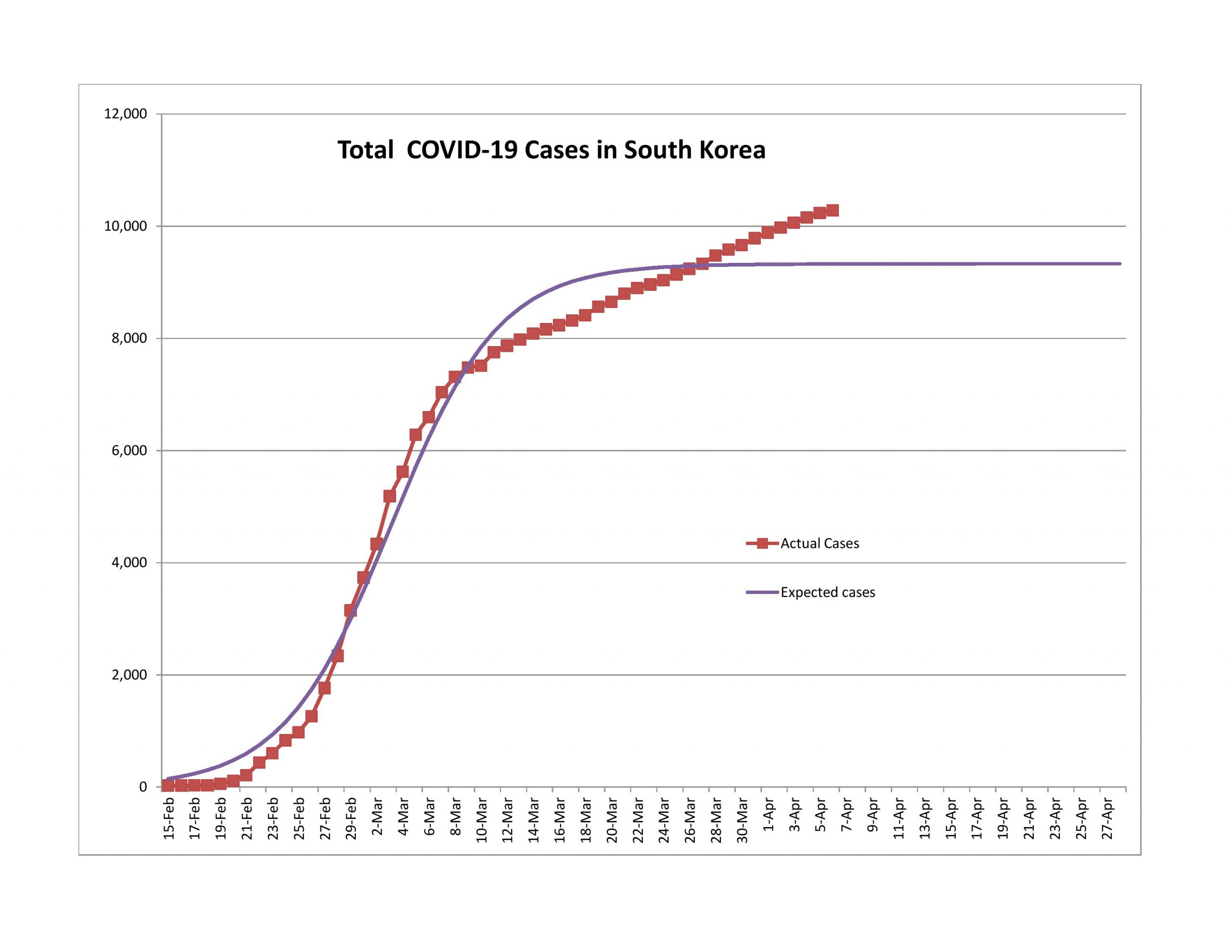

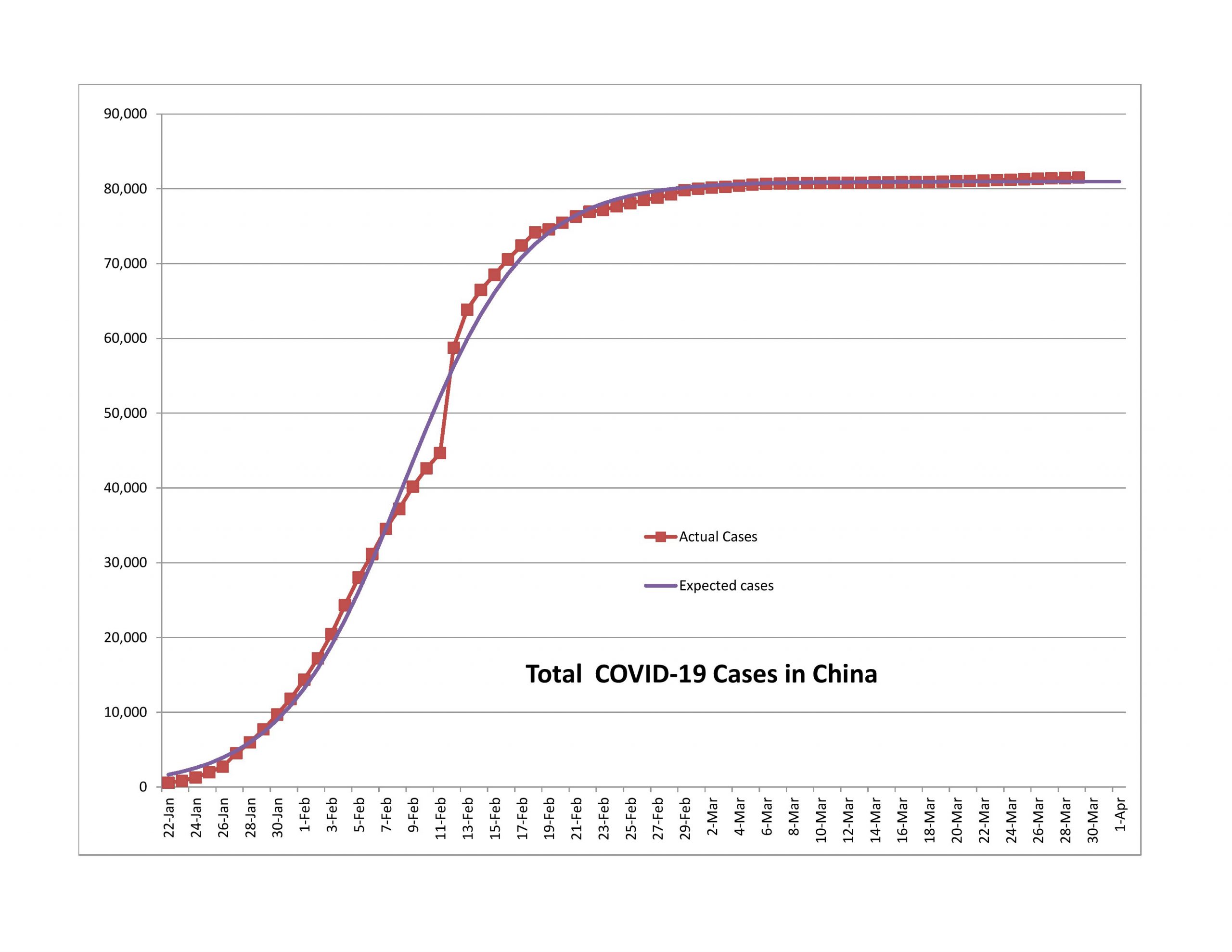

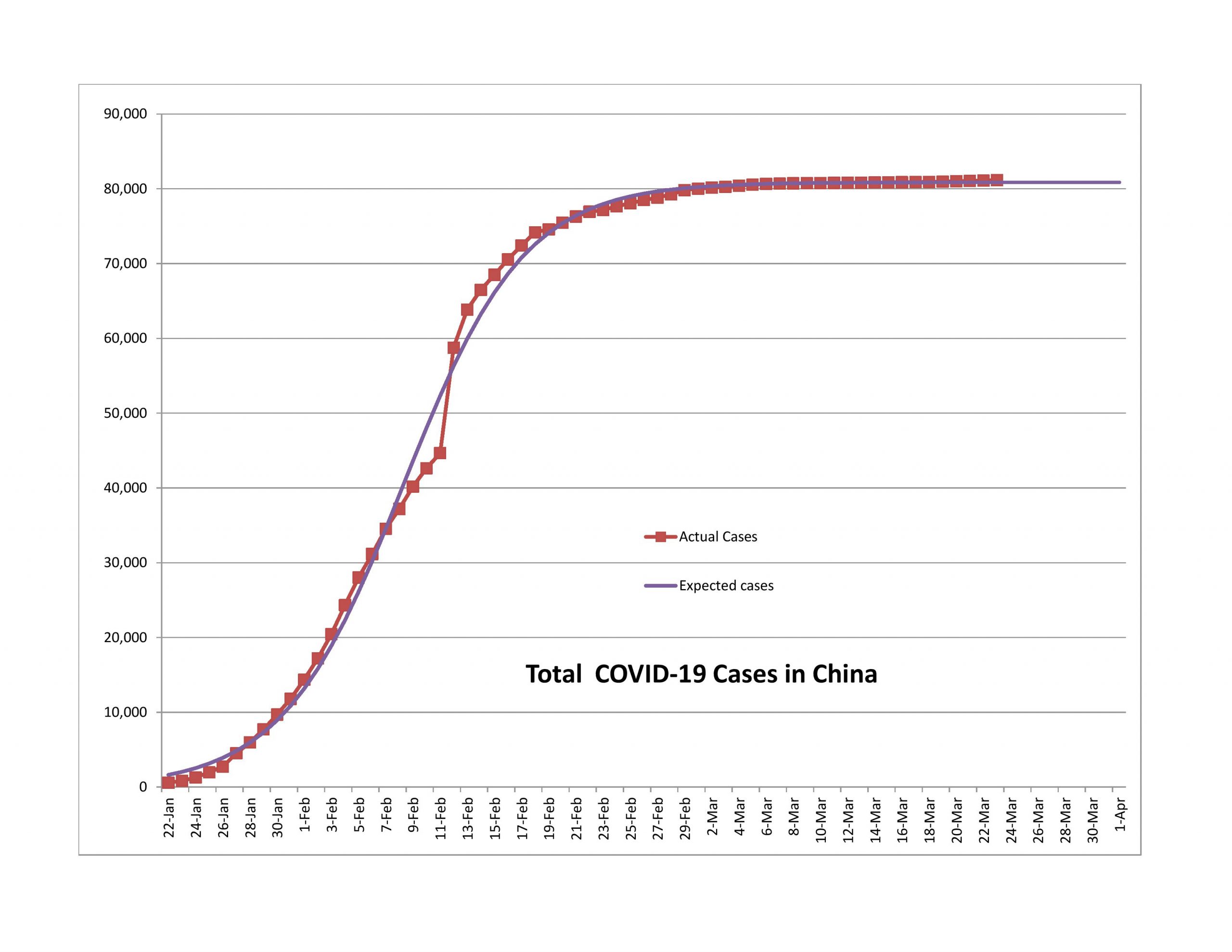

China has averaged 55 new cases of the past 10 days, and South Korea that figure is 99. The trend seems to be up, but with a lot of variability. I liken the second wave to what needs to be done after the main battle with a forest fire is done. You still have to put out some minor fires before they turn into something major. Eventually, like say in a month or two, most nations will be dealing with this.

Because of this situation, the models fit less and less well. I could add in a second logistic curve that starts where the first one ends… though it seems like overkill from a modeling standpoint. It wouldn’t be difficult to do.

Approaching the End of the First Wave

Austria, Switzerland and Italy are most likely past the 80% point. By that point reported new cases are declining quickly, and total cases are growing at around a 4% daily rate, and the growth rate is falling quickly.

As an aside, this is a good time to talk of how the media, and sometimes even policy makers who should know better, are practically innumerate in terms of the verbs that they use. They look at the raw increase in cases and say that they are soaring. It varies by geographic area, but the daily percentage growth in total cases and daily percentage growth in new cases is like this:

Percentage Completed

Daily % Growth in Total Cases

Daily % Growth in New Cases

0-10%

18-35% nearly constant daily growth, but absolute numbers are low.

Exceptionally high and erratic, 30-50%/day , but absolute numbers are low.

10-50%

Rate of growth falls into the teens of percentages. If the starting percentage is lower in this interval, so will the ending percentage. Absolute numbers sound large, especially nearing the halfway mark.

Rate of growth falls rapidly to zero by the end of this period

50-90%

Rate of growth continues to fall to the low single digits of percentages, say 2-4%. Absolute numbers sound large but rapidly get smaller toward the end of this interval.

Rate of growth is negative, and gets more negative as the interval gets to the 90% mark.

90-100%

Growth is very low. Absolute numbers are low.

Growth is negative and erratic. Absolute numbers are low.

It’s in the middle two zones where the absolute numbers are high that the rhetoric gets shrill. Compare that to me where at 8PM Eastern Time, I sit down and update my models and comment on how close they came to the modelled estimates. The absolute numbers of total cases, new cases, total deaths and new deaths make great headline fodder, but the real news should be looking at the percentage rates of growth of total cases and new cases. But I suspect that would be a tough thing to see change.

Middle of the Pack

Germany, the Netherlands, Spain, and the US are the next group. New cases are either rising at a low rate or declining. Growth in total cases is in the high single digits of percentage. These countries aren’t out of the woods yet, but are likely past the halfway point.

Some of these had high new case surprises over the last week, but on the whole showed improvement.

Bringing up the Rear

Each of these had significant upward surprises in terms of new cases reported. The growth rate of reported total cases is in the mid-to-high teens.

Too Early to Tell

I did not model Turkey in the last article. It has a really sharp takeoff and deceleration of growth that looks too good to be true. (The US is that way to a lesser extent.) I need more data before I can be definite about this.

Problem Child

Compared to last week, Iran has gone backward. New cases have been growing more rapidly, and the growth in total cases shows no sign of slowing. It will be interesting to see how this develops — it doesn’t fit the model well, unless….

Unless you think of it as several logistic curves in different areas that have taken off and leveled at different points in time. Now that said, from what little I have read, there seems to be a lot of disagreement in Iran over what to do. And to some degree, a populace that doesn’t trust the government much… so it’s not a recipe for constructive collective action.

States and Cities

Massachusetts and Boston Area

New York State and New York CIty

Maryland

The logistic curves for smaller, more homogeneous areas tend to be shorter and sharper than those for broader areas. The data also tends to be more noisy, but that’s what the regression analysis is for — smoothing out the data in a theoretically consistent way, and allowing tracking to be done so that a policymaker could estimate if they are doing better or worse than expected. It would certainly calm some politicians down if they had an idea of how things are likely to develop, and if a deviation happened, they could try to explain why, allowing for the level of uncertainty in analyses like this.

And so at the end, can I offer a happy surprise to New Yorkers, both those in the city, and those that are upstate? There will still be problems for a while, but it really seems like you are getting to the end of the trail. In two weeks, you should be a lot happier. And the same will likely be true in Massachusetts and Boston, and in my adopted home state, Maryland.

But here’s the key question. How ready will the politicians and policymakers be to accept the good news? I fear they will not be happy with it at all, but will remain cautious in the wrong way too long. There is kill, and there is overkill. Kill is enough.

I would encourage the politicians to have us continue to do social distancing, but to reopen businesses, requiring them to follow certain sanitary and distancing procedures. Perhaps those who are infirm, or are over 60, 65, 70, or so should continue remain at home, or only go to necessary places a while longer.

There is a price to everyone staying home. There is a political price to politicians that maintain it too long. Better to modify policy such that it is a sniper rifle, and no longer a blunderbuss.

PIcture credit: Aleph Blog, and the same for all the graphs and charts in this post. All liability for mistakes here is mine.

This post is different than any other I have done at Aleph Blog. I will try to write this in a nice way even though it is a strong and out-of-consensus opinion on a topic that many are edgy about.

I realize I might be wrong here, but I will present to you what I think, along with what I think are the limitations of my analysis. Part of my reason for writing this is that I think that most of the reporting on COVID-19 is subject to a bias common in our culture among politicians, lawyers, bureaucrats, and the media: an extreme bias toward safety because the costs of being wrong on the optimistic side are high than the rewards for being right. (Example: NOAA overpredicts disasters, and so do most hurricane forecasters.)

This post will be structured like this:

Summary of findings and recommendations

Limitations of the analysis

Breaking down the results by groups of countries

A discussion of the “Second Wave,” with policy recommendations

Closing comments

Appendix for math nerds

Summary of findings and recommendations

The First Wave of the crisis will pass more quickly than most expect. Most countries with a large number of COVID-19 cases will have 99% of their First Wave cases reported by mid-April.

Of the 13 countries with the most cases of COVID-19, the least of them has reported 41% of their likely First Wave cases. Of those same nations, none are expected to have more than 0.3% infected with COVID-19.

The real challenge will come in dealing with the Second Wave of the crisis. How do governments deal with a smallish number of new cases, and keep them from growing into a new epidemic?

In the Second Wave, governments should selectively tell some to stay home, while telling most people to get about their normal work.

Quarantine those who are sick with COVID-19 and those who have been with them, until they are tested and have a negative result. Continue to disallow international travel, or insist on a two week quarantine upon returning.

Let healthy people return to their work. All businesses are necessary businesses.

Avoid bizarre stimulus programs that are harmful in the long run. Tell the Fed that monetary policy can’t solve everything, and not to play favorites.

Limitations of the analysis

I am not a public health specialist. I am a statistician with a background in econometrics, which has its similarities with biometrics.

My analysis assumes that processes for finding new cases of COVID-19 are constant, or mostly so. That is not always true — an example is when China announced a large amount of new cases all at once.

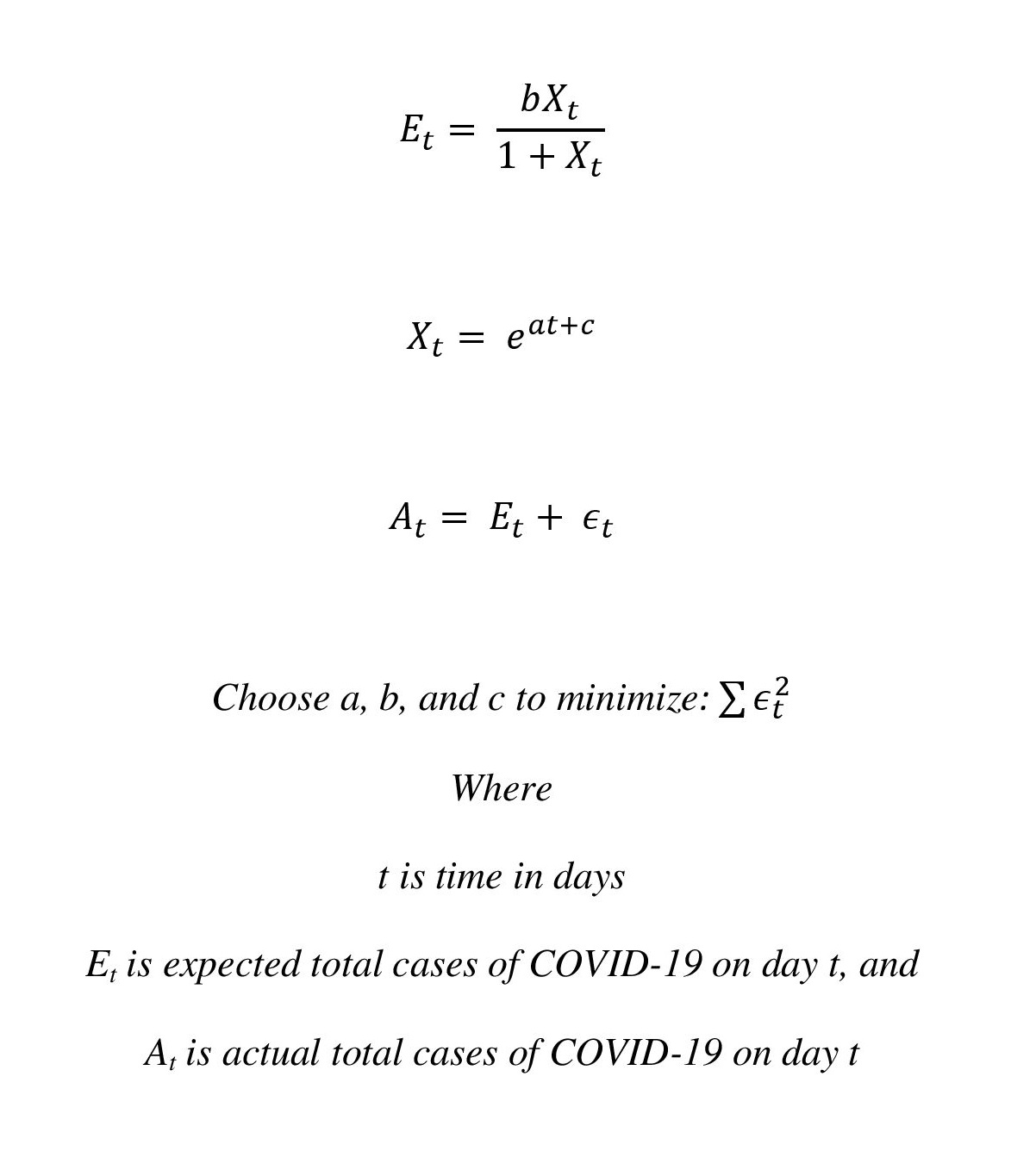

I use an inverse logistic curve for my analysis. All functional forms have their limitations, and for the nations analyzed as of this date, the minimum pseudo-R-squared is 79.4%, and the highest is 98.5%. That said, this is a common functional form for epidemics.

The model assumes that there is one wave. That will not prove to be true, as can be seen from China and South Korea.

All sorts of things can go wrong that are not in the data now — mutations, civil disobedience, large bureaucratic errors, large policy errors, etc.

Analysis By Group

Those that are though the First Wave

We have two in this group: South Korea and China. I don’t trust China’s data. In each case, though, you have the First Wave go through their nation and burn out, followed by an excess number of new cases where the public health authorities may not be catching up with what could be the Second Wave. I’ll talk more about the Second wave below.

The unusual case of Iran

Really, I don’t know what is going on in Iran on COVID-19 but it looks like the initial new cases started to slow down, and then they let up on restrictions too soon. New cases hit a new high yesterday, which doesn’t fit the paradigm of a consistent response the the crisis. COVID-19 seem to be out of control in Iran.

Those that are close to done

Italy and Germany are past the halfway mark in the epidemic, and are having lower new cases on average daily.

In general, the policy responses of a nation influence the amount of the population subject to infection, and the ability of the infected to interact with the broader society.

The rest

These are the nations that have not certainly passed the 50% mark as of today as I estimate the infection. As I have watched this develop over the last week, the most difficult aspect of estimation comes when you are near the halfway point. Small changes in actual new cases make a big difference in estimated new cases. An example is the United States, who has had significantly lower new cases than expected for a preponderance of the last week. The US got off to a slow start in its reaction to the crisis, but seemingly has caught up and then some.

WIth these countries, the odds of being wrong is the highest. Thus all conclusions with them must be considered tentative. But with so many of them following nearly the same pattern, despite very different responses to the crisis, gives more certainty to this analysis.

A discussion of the “Second Wave,” with policy recommendations

When you look at the data of CHina and South Korea, you see how the epidemic went through the s-curve, and then has persistently high new cases thereafter. I call this the “Second Wave.” Iran seems to be a case where their society inadequately stops transmission, and so instead of following an s-curve of an exponential, it seems to keep increasing in a way that is almost quadratic — slow but steady.

This will be the grand problem for most countries. How do you eradicate the virus after you have had large success in interrupting its transmission? Looking at the relative success of South Korea in the First Wave I would say that you do the following:

Test and quarantine aggressively.

Of those who test positive for COVID-19, quarantine all of their contacts, and test them. Continue quarantine for those who test positive, and quarantine/test their contacts as well. Repeat as needed.

But don’t quarantine everyone. Let those who are healthy work. Encourage those who are old or have compromised immune systems to stay home for the duration of the crisis, and give some assistance to them.

Don’t assist all of society because that is way too expensive and not needed — get them back to work. Don’t give into the idea of denying people work and then offering meager assistance. It is an inferior idea for those who are healthy.

This applies to the actions of the Federal Reserve as well — don’t harm the value of capital by artificially creating more capital that has no earnings capacity.

Closing comments

This analysis shows the the slowest of the nations written about here is passing the middle of the crisis quite rapidly, and the practical end of the crisis is in mid-April, when 99% of all First Wave new cases will have been realized. The real challenge will come in dealing with the cases after that, which will be sporadic and localized. How do we keep that from becoming a semi-permanent bother to the world, because the cost of putting life on hold is high, as is the cost of losing lives.

Quarantining and testing aggressively is the best solution, together with letting the healthy work. This should be the guiding star for all policymakers, because we need to strike the right balance between breaking the social connections that lead to disease transmission, and allowing people to labor to support themselves. We are not trying to save the financial markets; we are trying to protect people who work.

Appendix for math nerds

The above was how I structured my analysis. It followed a logistic curve, which has the following benefit: infections begin exponentially, but get retarded by two factors: one is that even if people do almost nothing as in 1918, the uninfected population shrinks, which blunts further growth. Second, people act to blunt further growth. They separate themselves from each other, and particularly those who are infected. This is is akin to removing fuel from the fire.

The logistic curve has a number of advantages for estimation. It notices the slowing down of the percentage growth in total cases, while media and politicians continue to panic.

Remember that that the media and politicians selfishly like to maximize their influence, and try to create panics — it is good for them to maximize fear. The same is true for many in public health. Truly, we should spend more on public health, but it is one of those things that governments naturally neglect… because they are short-sighted, and will not spend money on something the lowers risk, but does not bring any present good. (Note to Christians: in the Old Testament public health was a function of their government via the priests. It should be a normal function of government to deal with contagion.)

Final note: I did not write this with Donald Trump in mind. I did not vote for him and will not vote for him. That said, he is on the right track when he says the cure should not be worse than the disease.

It is foolish to warp monetary policy and fiscal policy when healthy people are perfectly capable of working. Don’t destroy ordinary incentives and rack up tons of debt by keeping people idle. Test, quarantine, test, quarantine, etc. , but leave the main body of society alone, particularly for a virus that does not harm the healthy working population much.

To that end, I ask that Republicans be real Republicans, and not expand the deficit further. I ask that the Federal Reserve stop trying to be God, and be content with merely having a currency with a consistent value.

Government is best when it is small. We are not facing the Black Death, nor the Spanish Flu. We will get through this, God willing. We don’t need to panic.

Photo Credit: vldd || Relative to a complete bridge, what’s the value of a bridge that will never be completed?

Here’s number 65 in this irregular series:

The second-best plan that you can execute is better than the best plan that you can’t execute.

Rule LXV

It takes more than the right ideas to be an investor. It also takes the courage to make the hard decisions at the time when it hurts to do so.

Will you make more money if you allocate at least 80% of your assets to stocks and other risk assets? Yes. How will you hold on during a gut-wrenching bear market that gives you the feeling that you are losing everything?

You could just refuse to look at your statements, or listen to financial media. But most people will bump into that randomly during a bear market, because the level of chatter goes up so much. It may be better to take a second-best solution and reduce the portion of risky assets to 50-60%, and simply sleep better at night. Reduce until you won’t be nervous, and preferably, make this adjustment during the bull market.

Do you have a nifty trading strategy that you are tempted to overrule because it generates trades that you think don’t make sense, or come at times that seem too painful? Perhaps you need to abandon the strategy, or lower the size of the trades done. Maybe do half of what the strategy would tell you to do.

If you use the Kelly Criterion to size your trades, and the volatility drives you nuts, maybe size your trades to “half Kelly.”

Am I offering an opiate for underachievement? Well, no… maybe… yes… Look, personalities are not fixed, much as some say that they cannot change. If you have sufficient motivation, you can come up with ways to change your personality to be able to deal with more risk, or, conclude that you will do better if you take less risk.

Writing out a set of rules can useful, as is testing them to make sure they actually work. In general fewer rules are better.

An example of this in my life was when I was a corporate bond manager, I made an effort to forget prior prices of a bond, thus forcing me to be forward-looking in my management. When I was younger, I told myself that there would be losses, and they were a price of getting the gains on average.

But if you can’t make your personality change, then you have to adapt your investment strategy to let you be happy while still achieving most of your goals. As an example, if you like to sell stocks short, it would be wise to have some sort of limit as to how much you are willing to lose before closing out a trade — this applies more to shorting, as losses are unlimited as prices rise, but gains are capped.

Ordinarily, if a person or institution is close to even-keeled with respect to risk, the time horizon and uncertainty of the cash flows from the assets should be the main criteria for asset allocation. But when a person is overly timid or bold, that will become the dominant criterion for their asset allocation.

It is important not to be of two minds here. Admit your weaknesses, and either fix them, or live with them. The trouble comes when you think you are strong, but then give in when a bad event happens that was beyond your capacity to handle.

It’s also important to understand that the market can be more vicious than at any prior point in history. Yes, there are historical highs and lows for every variable — but both can be exceeded… the speed of the current bear market is an excellent reminder of that. Try to understand that there will be as Donald Rumsfeld once said “unknown unknowns.” Have you left enough slack in your strategy for some really bad scenarios? Have you considered that it’s not impossible to have a second Great Depression event, despite the best efforts of politicians, regulators and economists? Have you considered that it is possible to eclipse the valuation highs achieved in 2000?

And consider the phrase from my disclaimer “The market always has a new way to make a fool out of you.” Have you considered what scenario would be poison for what you currently do? Unlikely as it may be, can you live with that scenario? If not, scale down your strategy until you can live with it. Or, figure out what your coping strategy would be.

The first life insurer that I worked for had the strategy that if things went wrong with their investing, they would sell policies more aggressively and invest the proceeds to grow their way out of the problem. They ended up being the largest life insurance insolvency of the 1980s, as their worst case scenario arrived, and their capital was depleted. They would have done better to grow more slowly, and more soundly. The same would apply to Enron and other companies that try to grow too fast. This is another case where the second best is achievable, but the “best” is not.

So, know yourself, and know the markets well. Leave some slack in your strategy… don’t play it to or past the absolute maximum that you can handle. Have some humility, and live in reality. For most investors, that will pay off in a big way.

There are a pair of articles regarding the efforts of a few people posting at Reddit to make money in stocks as part of a perpetual motion machine. The articles are here: Businessweek, Matt Levine.

The idea is for a bunch of people to buy calls in the morning, which forces market makers to hedge by buying the underlying stock, which pushes the price up, giving automatic gains. Now, real hedgers hedge options using options, but the net effect should be the same regardless.

What the speculators mentioned in these articles don’t get is that they are violating rule XXXII:

Dynamic hedging only has the potential of working on deep markets.

Arbitrage pricing can reveal proper prices in smaller less liquid markets if there are larger, more liquid markets to compare against.? The process cannot work in reverse, except by accident.

The quick summary of this is that the tail can’t wag the dog. The amount of money in the options market is far smaller than the money in the stock market. As such, if speculators try to overwhelm the market for a given stock with call purchases, real money sellers will happily oblige them and provide them with stock. They will not win on average.

There are no simple magical money machines in the market. Those that think they have one have deceived themselves.

Photo Credit: Miles Nicholls || Actually, the bells get rung at the top, and quite frequently for the duration of the process. People hear it and they decide not to listen. Too many false alarms.

The stock market model is projecting a 3.06%/year return over the next ten years as of the close on 11/15/2019. That’s near where a 10-year mid-single-A rated bond would trade. That’s not offering a lot of compensation for putting your money at risk.

I’m planning on reducing my total risk level by 15% or so, moving my equity allocation from around 70% to 55%. That will be the lowest it has been in two decades. I’m not running to do this. I am still working out the details.

The Fundamentals of Equity Market Tops

You might recall an old piece of mine that I wrote for RealMoney back in January 2004 — The Fundamentals of Market Tops. In it, I gave a non-technical analysis approach to analyzing whether we might be near a market top. In 2004, I concluded that we were NOT near a market top. (This article also served as a partial template for the article at RealMoney in May 2005, which said that YES we were near a market top for Residential Real Estate. Two good calls.)

The article is longer than most, should not fit in the TL;DR bucket for most investors. I’m not going to reconstruct the article here, but just give some brief points that fit the frame of the article. Here I go:

Value investors have been sidelined. Growth is winning handily.

Valuation-sensitive investors are raising cash. Buffett sitting on $130 billion is quite statement. He’s not alone. More on that below.

Momentum is working.

There has been a decline in IPO quality.

Lots of money is getting attracted to private equity.

Corporate leverage is high, and covenants are weak.

Non-GAAP accounting gets more attention than it deserves.

Defined benefit plans are net sellers of stock, but not for the reasons I posit in my article — they are doing it to move to private equity and alternatives, and bonds as a part of liability-driven investing.

Cutting against my thesis:

More companies are committing to paying dividends, and growing them. I’m impressed with the degree that corporations are thinking through their use of free cash flow, even as they lever up.

Actual volatility isn’t that high.

The Fed is supportive.

On net, these conditions give some confirmation to what my quantitative model is saying… the market is near a top. Could it go higher still? You bet, with an emphasis on the word “bet.” The S&P 500 at 4500 would be where valuations were during the dot-com bubble.

The main idea as applied to the present is this: when you have “strong hands” (those with long time horizons and strong balance sheets) raising cash levels and those with “weak hands” (those with shorter time horizons and weaker balance sheets) staying highly invested in risk assets, it is a situation that is unstable. Those that have capability to “buy and hold” are sitting on their hands, whereas those who have to get returns or they will suffer (typically municipal defined benefit plans and older retail investor who didn’t save enough) are risking a great deal, and have little additional buying power.

This is unstable. This situation typically exists at market tops. Remember, it is what investors DO that is the consensus, not what they SAY.

With that, consider your risk positions, and if you think you should act, do so. If you are uncertain, you could ask an intelligent friend or do half.