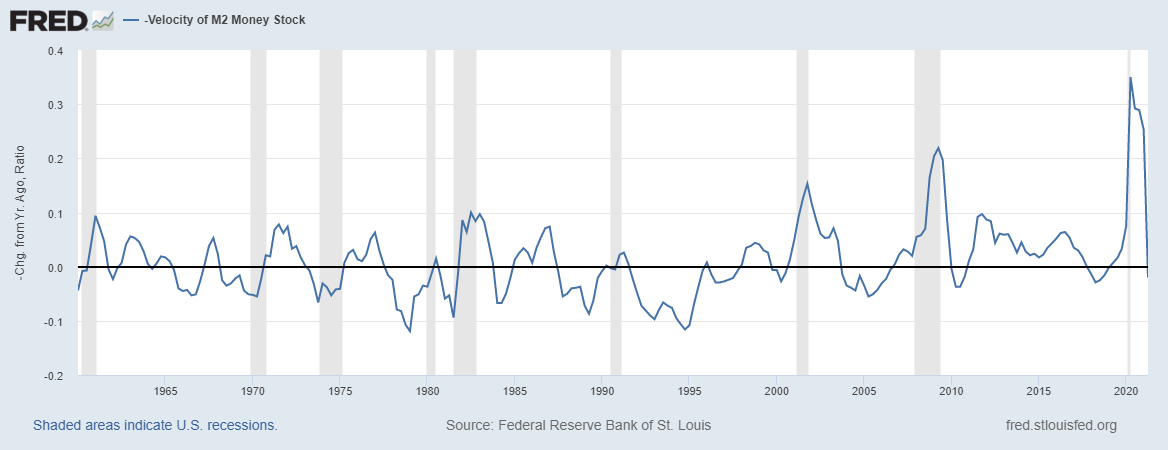

Picture Credit: FRED and Aleph Blog || The above is the negative of the year over year change in the velocity of M2. GDP is now growing faster than M2

There was an Interesting article on Bloomberg yesterday: Liquidity Is Evaporating Even Before Fed Taper Hits Markets. It makes the case that over the last 20+ years the stock market has fallen once GDP starts growing faster than M2. More money goes to production, and less to financing assets.

As the article says:

�Put another way, the recovering economy is now drinking from a punch bowl that the stock market once had all to itself,� Doug Ramsey, Leuthold Group�s chief investment officer, wrote in a note last week.

Liquidity Is Evaporating Even Before Fed Taper Hits Markets

Looking over the last 60 years, there seems to be a weak correlation that supports this idea. Now, for those that follow my S&P 500 valuation model, we are very close to the all-time peak valuation level. The peak was a -1.87%/year expected nominal return over the next 10 years. We are at -1.81%/year now. (Again, not adjusted for inflation.)

Anybody else noticing that interest rates have been rising recently? The 30-year Treasury bond yields 2.00%! (I remember my first boss saying to me in 1987, “Interest rates will never go below 10%.”)

In the Bloomberg article, Ed Yardeni is skeptical and said the following:

Ed Yardeni, the president and founder of Yardeni Research Inc., says he prefers to plot not the growth rates but the absolute level of M2 against GDP to measure liquidity. Based on that, liquidity stood near a record high. �Some people start to freak out about the M2 growth rate,� he said in an interview on Bloomberg TV and Radio. �What they don�t really appreciate is M2 today is $5 trillion higher than it was before the pandemic. There is just a tremendous liquidity sitting there.�

Liquidity Is Evaporating Even Before Fed Taper Hits Markets

I disagree with Yardeni here, but that doesn’t mean that I fully believe that danger is imminent. Economics has always improved by analyzing in terms of how marginal values are affected, not absolute values. Ben Bernanke uttered the word “taper” and forward interest rates roared higher as he protested that monetary policy was “accommodative.” Monetary policy is as loose as what economic actors can borrow money at. Rates are rising — tight. Rates are falling — loose. Yellen and Fischer made the same errors.

The Fed is tightening as they reduce QE, and begin raising the Fed Funds rate in 2022. It will end in a market meltdown in late 2022 as an overly indebted economy cannot tolerate the increase in the financing rate. The Fed will find itself trapped and interest rates will remain low.

My confidence level on this idea is only 70%. But valuations are high, and the Fed is tightening, even if they say they are not doing so. There will be far worse times to speculate on a fall in the market. It can’t go much higher. It can go a lot lower. Short bonds and cash are alternatives.