I was writing to potential clients when I realized that I don’t have so much to write about my bond track record as I do my track record with stocks. ?I jotted down a note to formalize what I say about my bond portfolios.

One person I was writing to asked some detailed questions, and I told him that the stock market was likely to return about 4.5%/yr (not adjusted for inflation) over the next ten years. ?The model I use is the same one as this one used by pseudonymous Philosophical Economist. ?I don’t always agree with him, but he’s a bright guy, what can I say? ?That’s not a very high return — the historical average is around 9.5%. ?The market is in the 85th-90th percentiles of valuation, which is pretty high. ?That said, I am not taking any defensive action yet.

Yet.

But then it hit me. ?The yield on my bond portfolio is around 4.5% also. ?Now, it’s not a riskless bond portfolio, as you can tell by the yield. ?I’m no longer running the portfolio described in Fire and Ice. ?I sold the long Treasuries about 30 basis points ago. ?Right now, I am only running the Credit sensitive portion of the portfolio, with a bit of foreign bonds mixed in.

Why am I doing this? ?I think it has a good balance of risks. ?Remember that there is no such thing as generic risk. ?There are many risks. ?At this point this portfolio has a decent amount of credit risk, some foreign exchange risk, and is low in interest rate risk. ?The duration of the portfolio is less than?2, so I am not concerned about rising rates, should the FOMC ever do such a thing as raise rates. ?(Who knows? ?The economy might actually grow faster if they did that. ?Savers will eventually spend more.)

But 10 years is a long time for a bond portfolio with a duration of less than 2 years. ?I’m clipping coupons in the short run, running credit risk while I don’t see any major credit risks on the horizon aside from weak sovereigns (think the PIIGS), student loans, and weak junk (ratings starting with a “C”). ?The risks on bank loans are possibly overdone here, even with weakened covenants. ?Aside from that, if we really do see a lot of credit risk crop up, stocks will get hit a lot harder than this portfolio. ?Dollar weakness and US inflation (should we see any) would also not be a risk.

I’ve set a kind of a mental stop loss at losing 5% of portfolio value. ?Bad credit is the only significant factor that could harm the portfolio. ?If credit problems got that bad, it would be time to exit because credit problems come in bundles, not dribs and drabs.

I’m not doing it yet, but it is?tempting to reposition some of my IRA assets presently in stocks into the bond strategy. ?I’m not sure I would lose that much in terms of profit potential, and it would increase the overall safety of the portfolio.

I’ll keep you posted. ?That is, after I would tell my clients what I am doing, and give them a chance to act, should they want to.

Finally, do you have a different opinion? ?You can email me, or, you can share it with all of the readers in the comments. ?Please do.

I had the fun today of taping a segment with Ameera David on RT Boom/Bust. The above video covers the first half of the session, and lasts about seven minutes. We covered the following topics (with links to articles of mine, if any are applicable):

My last piece on this topic, On Bond Market Illiquidity (and more), drew a few good comments. ?I would like to feature them and answer them. ?Here’s the first one:

Hello David,

One issue you don’t address in your post, which is excellent as usual, is the impact of what I’ll call “vaulted” high quality bonds. The explosion and manufacturing of fixed income derivatives has continued to explode while the menu of collateral has been steady or declining. A lot of paper is locked down for collateral reasons.

That’s a good point. ?When I was a bond manager, I often had to deal with bonds that were salted away in the vaults of insurance companies, which tend to be long-term holders of long-term bonds, as they should be. ?They need them in order to properly fund the promises that they make, while minimizing cash flow risk.

Also, as you mention, some bonds can’t be sold for collateral reasons. ?That can happen due to reinsurance treaties, collateralized debt obligations, accounting reasons (marked “held to maturity”),?and some?other reasons.

But if the bonds are technically?available for sale, it takes a certain talent to get an insurance company to sell some of those bonds without offering a?steamy?price. ?You can’t sound anxious, rushed, etc. My approach was, “I’d be interested in buying a million or two of XYZ (mention coupon rate and maturity) bonds in the right price context. ?No hurry, just get back to me with any interest.” ?I would entrust this to one mid-tier broker familiar with the deal, who had previously had some skill in prying bonds out of the accounts of long-term holders before. ?I might have two or three brokers doing this at a time, but all working on separate issues. ?No overlap allowed, or it looks like there is a lot of demand for what is likely a sleepy security. ?No sense in driving up the price.

Because it is difficult to get the actual cash bonds, it is tempting for some managers to buy synthetic versions of those bonds, or synthetic collateralized debt obligations of them instead. ?Aside from counterparty risk, the derivatives exist as “side bets” in the credit of the underlying securities, and don’t provide any additional liquidity to the market.

My point here would be that these conditions have existed before, and I think what we have here is a repeat of bull market conditions in bond credit. ?This isn’t that unusual, and it will eventually change when the bull market ends.

Here’s the next comment:

Hi David,

I hope you?re doing well.? I?ve been reading your blog for about a year now and really appreciate your perspective and original content.? Just wanted to ask a quick question regarding your most recent post on bond market liquidity.?

Our investment committee often talk about the idea of bond liquidity (and discusses it with every bond manager who walks in our doors), and specifically how there are systematic issues now which limit liquidity and considerably push the burden onto money managers to make markets vs. the past, when banks themselves were free to make more of a market with their own balance sheets.

My (limited) understanding is that legislation since 2008 has changed the way that investment banks are permitted to trade on their own books, and this is a big part of the significantly decreased liquidity which has thus far been a relative non-issue but which could rear its head quickly in the face of a sharp correction in bonds.

Do you have any thoughts about this newer paradigm of limited market-making at the big banks?? You didn?t seem to mention it at all in your article and I?m wondering if my thoughts here are either inaccurate or not impactful to the bottom line of the liquidity conversation.

I?m sure you?re a busy guy so I won?t presume upon a direct response but it may be worthwhile to post an update if you think these questions are pertinent.

Another very good comment. ?I thought about adding this to the first piece, but in my experience, the large investment banks only kept some of the highest liquidity corporates in inventory, and the dregs of mortgage- and asset-backed bonds that they could not otherwise sell. ?The smaller investment banks would keep little-to-no-inventory. ?Many salesmen might have liked the flexibility of their bank to hold positions overnight, or buying bonds to “reposition” them, but the experiences of their risk control desks put the kibosh on that.

As a result, I think that the willingness of investment banks to make a market rely on:

The natural liquidity of the securities (which comes from the size of the issue, market knowledge of the issue, and composition of the ownership base), and

How much capital the investment bank has to put against the position.

The second is a much smaller factor. ?Insurance companies have to deal with variations in capital charges in the bonds that they hold, and that is not a decisive factor in whether they hold a bond or not. ?It is a factor in who will hold a bond and what yield spread the bond will trade at. ?Bonds tend to gravitate to the holders that:

Like the issuer

Like the cash flow profile

Have low costs for holding the bonds

Yes, the changed laws and regulations have raised the costs for investment banks to hold bonds in inventory. ?They are not a preferred habitat for most bonds. ?Therefore, if an investment bank buys a bond in order to sell it (or vice-versa) in the present environment, the bid-ask spread must be wider to compensate for the incremental costs, thus reducing liquidity.

To close this evening, one more letter on bonds from a reader:

First off, thank you for taking the time to share your knowledge via your blog.? It is much appreciated.

Now for a bond question from someone learning the fixed income ropes…

What is the advantage/reasoning behind a company co-issuing notes with a finance subsidiary?? Even with reading the prospectus/indenture I can’t understand why a finance sub (essentially just set up to be a co-issuer of debt) would be necessary especially since the company is an issuer anyway and they also may have?other subs guarantee the debt also.? I’m probably missing something obvious.

The answer here can vary.? Some companies guarantee their finance subsidiaries, and some don?t.? Those that don?t are willing to pay more to borrow, while bondholders live with the risk that in a crisis, the company might step away from its lending subsidiary.? They would never let the subsidiary fail, right?

Well, that depends on how easy it is to get financing alternatives, and how easy it might be for the parent company to borrow, post-subsidiary default.

If things go well, perhaps the subsidiary could be spun off as a separate company, or sold to another finance company for a gain.? After all, it has had separate accounting done for a number of years.

Beyond that, it can be useful to manage lending separately from sales.? They are different businesses, and require different skills.? Granted, it could be done as two divisions in the same company, but doing it in separate companies would force separate accountability if done right.

There may be other reasons, but they aren?t coming to my mind right now.? If you think of one, please note it in the comments.

I’ve read a lot of articles about bond market illiquidity, and I don’t think it is as big of an issue as many are making it out to be. ?The bond market often runs hot and cold, and when prices and yields are moving, it is difficult to get off trades at levels you might like unless you are resisting the trend. ?And if you are resisting the trend, will you like the trade one week later, when the trade might look poor in hindsight?

Part of the difficulty is that the buy side has gotten more concentrated. ?Bigger players by their nature can’t move in and out of positions without moving the market against their interests. ?Illiquidity is a rule of life for them. ?They may as well become market makers to some degree — offering bonds they want to keep at prices at which only the desperate would want to buy. ? Also, they could bid for bonds at levels at which only the desperate would want to sell.

Add into that the amount of bonds tucked away in ETFs. ?The ETFs may seem to offer liquidity at no cost, but retail investors tend to panic more rapidly than institutional investors. ?If retail investors run away from any part of the market, the ETFs in that part of the market will be among the managers selling into a falling market, and there is a cost to that, at least for those slower to sell the ETFs in question.

But away from that, current monetary policy leaves many on pins and needles waiting for short rates to rise. ?Now, there is no guarantee that short rates will rise in 2015. ?The Fed has shown itself to be extra slow to act in this cycle, and the current FOMC has no hawks — not that the hawks matter — their views are not a part of current monetary policy.

But even if short rates rise, there is no guarantee that long rates will follow. ?In the last tightening cycle, long rates stayed the same with a lot of noise that included falling long yields in the early phases. ?The global economy isn’t that strong, and interest rates in the middle of the curve tend to track nominal GDP growth (with a lot of noise).

You can position yourself for rising short rates, but you have to give up a lot of income (carry) to do so. ?How long can you bear to earn very little, particularly if you are earning a management fee?that eats up a lot of the income?

Situations like this are naturally twitchy, because things are unclear, but as things clarify, there may?be many who will want to sell longer bonds to buy?shorter bonds where rates will rise. ?If long rates do rise along with short rates, who pray tell will be the philanthropist that holds onto the long bonds and eats losses for clients that want positive (or at least small?negative) total returns?

There is a price for almost every asset, but there is no guarantee of being able to sell a lot of long bonds if rates are rising, and certainly not without offering a large price concession. ?That’s illiquidity, which naturally happens if you try to trade against a large trend in the bond market.

That brings me to my main point:

Bonds should be illiquid now. ?Why should you expect otherwise?

No one is out to do you voluntary favors in the markets. ?Why should markets have narrow bid-ask spreads when there is significant policy uncertainty, and large players that hold a large fraction of the total bond market? ?At a time like this, I would?only?want to make a market if the compensation was significant.

Two unrelated notes before I sign off. ?First, I sold my position in long Treasuries about a month ago, when 30-year yields crossed 2.80%. ?I had owned the long bonds for quite a while and had decent profits on them. ?I felt the current selloff might have legs, which may be true (or not). ?So, I am below market duration at present, and earning ~4% off of a variety of short investment grade corporates, bank loans, junk bonds, TIPS, and foreign bonds… so far so good, but I can’t express any significant confidence that this strategy will be a winner. ?It’s my best guess for now, as I don’t see many immediate credit risks. ?After all, look how little damage the energy sector took on even with oil prices that fell hard. ?There is a lot of money looking around for bargains.

Second, if I were a large corporate bond issuer, I would look to form a consortium with my fellow large issuers to set up an auction market for the new issuance of bonds, and bypass Wall Street. ?Why? ?Because the new issue yield premiums are large. ?Why should large money managers benefit from the new issue market? ?Yes, I know that offering liquidity should receive some reward, but not as large as it is at present.

This is a modern era, and the need for intermediaries in the IPO market for bonds is less needed. ?Let the buy side, which is starved for new bonds and yield, pay up for the privilege of receiving the bonds. ?Who knows? ?Maybe the issuers might borrow a little more as a result.

Hey, CFOs of large bond issuers! ?This is your chance to become a hero. ?Grab the opportunity, and issue your bonds with your peers through a mutually owned central auction house. ?Who knows? ?One day you could spin it off, and it could become… an investment bank. 😉

Recently I ran across an academic journal article where they posited one dozen or so risk premiums that were durable, could be taken advantage of in the markets. ?In the past, if you had done so, you could have earned incredible returns.

What were some of the risk premiums? ?I don’t have the article in front of me but I’ll toss out a few.

Many were Credit-oriented. ?Lend and make money.

Some were volatility-oriented. ?Sell options on high volatility assets and make money.

Some were currency-oriented. ?Buy government bonds where they yield more, and short those that yield less.

Some had you act like a bank. ?Borrow short, lend long.

Some were like value investors. ?Buy cheap assets and hold.

Some were akin to arbitrage. ?Take illiquidity risk or deal/credit risk.

Others were akin to momentum investing. ?Ride the fastest pony you can find.

After I glanced through the paper, I said a few things to myself:

Someone will start a hedge fund off this.

Many of these are correlated; with enough leverage behind it, the hedge fund?could leave a very large hole when it blows up.

Yes, who wouldn’t want to be a bank without regulations?

What an exercise in data-mining and overfitting. ?The data only existed for a short time, and most of these are well-recognized now, but few do all of them, and no one does them all well.

Hubris, and not sufficiently skeptical of the limits of quantitative finance.

Risk premiums aren’t free money — eggs from a chicken, a cow to be milked, etc. ?(Even those are not truly free; animals have to be fed and cared for.) ?They exist because there comes a point in each risk cycle when bad investments are revealed to not be “money good,” and even good investments are revealed to be overpriced.

Risk premiums exist to compensate good investors for bearing risk on “money good” investments through the risk cycle, and occasionally taking a loss on an investment that proves to not be “money good.”

(Note: “money good” is a bond market term for a bond that?pays all of its interest and principal. ?Usage: “Is it ‘money good?'” ?”Yes, it is ‘money good.'”)

In general, it is best to take advantage of wide risk premiums during times of panic, if you have the free cash or a strong balance sheet behind you. ?There are a few problems though:

Typically, few have free cash at that time, because people make bad investment commitments near the end of booms.

Many come late to the party, when risk premiums dwindle, because the past performance looks so good, and they would like some “free money.”

These are the same problems experienced by almost all institutional investors in one form or another. ?What bank wouldn’t want to sell off their highest risk loan book prior to the end of the credit cycle? ?What insurance company wouldn’t want to sell off its junk bonds at that time as well? ?And what lemmings will buy then, and run over the cliff?

This is just a more sophisticated form of market timing. ?Also, like many quantitative studies, I’m not sure it takes into account the market impact of trying to move into and out of the risk premiums, which could be significant, and change the nature of the markets.

One more note: I have seen a number of investment books take these approaches — the track records look phenomenal, but implementation will be more difficult than the books make it out to be. ?Just be wary, as an intelligent businessman should, ask what could go wrong, and how risk could be mitigated, if at all.

This is a difficult book to review. ?Let me tell you what it is not, and then let me tell you what it is more easily as a result.

1) The book?does not give you detailed biographies of the people that it features. ?Indeed, the writing on each person is less than the amount that Ken Fisher wrote in his book, 100 Minds That Made the Market. ?If you are looking for detailed biographical sketches, you will be disappointed.

2) The book does not give detailed and comparable reviews of the portfolio performance of those that it features. ?There’s no way from what is written to tell really how good many of the investors are. ?I mean, I would want to see dollar-weighted rates of return, and perhaps, measures of dollar alpha. ?The truly best managers have expansive strategies that can perform well managing a large amount of money.

3) The book admits that the managers selected may not be the greatest, but are some of the “greats.” ?Okay, fair enough, but I would argue that a few of the managers don’t deserve to be featured even as that if you review their dollar-weighted performance. ?A few of them showed that they did not pay adequate attention to margin of safety in the recent financial crisis, and lost a lot of money for people at the time that they should have been the most careful.

What do you get in this book? ?You get beautiful black and white photos of 33 managers, and vignettes of each of them written by six authors. ?The author writes two-thirds of the vignettes.

Do I recommend this book? ?Yes, if you understand what it is good for. ?It is a well-done coffee table book on thick glossy paper, with truly beautiful photographs.?It is well-suited for people waiting in a reception area, who want to read something light and short about several?notable investment managers.

But if you are looking for anything involved in my five points above, you will not be satisfied by this book.

One final note on the side — I would have somehow reworked the layout of Bill Miller’s photograph. ?Splitting his face down the middle of the gutter does not?represent him to be the handsome guy that he is.

Full disclosure:?I?received a?copy from the author. ?He was most helpful.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

This will be the post where I cover the biggest mistakes that I made as an institutional bond and stock investor. In general, in my career, my results were very good for those who employed me as a manager or analyst of investments, but I had three significant blunders over a fifteen-year period that cost my employers and their clients a lot of money. ?Put on your peril-sensitive sunglasses, and let’s take a learning expedition through my failures.

Manufactured Housing Asset Back Securities — Mezzanine and Subordinated Certificates

In 2001, I lost my boss. ?In the midst of a merger, he?figured his opportunities in the merged firm were poor, and so he jumped to another firm. ?In the process, I temporarily became the Chief Investment Officer, and felt that we could take some chances that the boss would not take that in my opinion were safe propositions. ?All of them worked out well, except for one: The?– Mezzanine and Subordinated Certificates of?Manufactured Housing Asset Back Securities [MHABS]. ?What were those beasts?

Many people in the lower middle class live in prefabricated housing in predominantly in trailer parks around the US. ?You get a type of inexpensive independent living that is lower density than an apartment building, and?the rent you have to pay is lower than renting an apartment. ?What costs some money is paying for the loan to buy the prefabricated housing.

Those loans would get gathered into bunches, put into a securitization trust, and certificates would get sold allocating cash flows with different probabilities of default. ?Essentially there were four levels (in order of increasing riskiness) — Senior, Mezzanine, Subordinated, and Residual. ?I focused on the middle two classes because they seemed to offer a very favorable risk/reward trade-off if you selected carefully.

In 2001, it was obvious that there was too much competition for lending to borrowers in Manufactured Housing [MH] — too many manufacturers were trying to sell their product to a saturated market, and underwriting suffered. ?But, if you looked at older deals, lending standards were a lot higher, but the yields on those bonds were similar to those on the badly underwritten newer deals. ?That was the key insight.

One day, I was able to confirm that insight by talking with my rep at Lehman Brothers. ?I talked to him about the idea, and he said, “Did you know we have a database on the loss stats of all of the Green Tree (the earliest lender on MH) deals since inception?” ?After the conversation was over, I had that database, and after one day of analysis — the analysis was clear: underwriting standards had slipped dramatically in 1998, and much further in 1999 and following.

That said, the losses by deal and duration since issuance followed a very predictable pattern: a slow ramp-up of losses over 30 months, and then losses tailing off gradually after about 60 months. ?The loss statistics of all other MH lenders aside from Vanderbilt (now owned by Berkshire Hathaway) was worse than Green Tree losses. ?The investment idea was as follows:

Buy AA-rated mezzanine and BBB-rated subordinated MHABS originated by Green Tree in 1997 and before that. ?The yield spreads over Treasuries are compelling for the rating, and the loss rates would have to jump and stick by a factor of three to impair the subordinated bonds, and by a factor of six to impair the mezzanine bonds. ?These bonds have at least four years of seasoning, so the loss rates are very predictable, and are very unlikely to spike by that much.

That was the thesis, and I began quietly acquiring $200 million of these bonds in the last half of 2001. ?I did it for several reasons:

The yields were compelling.

The company that I was investing for was growing way too rapidly, and we needed places to put money.

The cash flow profile of?these securities matched very well the annuities that the company was selling.

The amount of capital needed to carry the position was small.

By the end of 2001, two things happened. ?The opportunity dried up, because I had acquired enough of the bonds on the secondary market to make a difference, and prices rose. ?Second, I was made the corporate bond manager, and another member of our team took over the trade. ?He didn’t much like the trade, and I told my boss that it was his portfolio now, he can do what he wanted.

He kept the positions on, but did not add to them. ?I was told he looked at the bonds, noticed that they were all trading at gains, and stuck with the positions.

Can You Make It Through the Valley of the Shadow of Death?

I left the firm about 14 months later, and around?that time, the prices for MHABS fell apart. ?Increasing defaults on MH loans, and failures of companies that made MH, made many people exceptionally bearish and led rating agencies to downgrade almost all MHABS bonds.

The effects of the losses were similar to that of the Housing Bubble in 2007-9. ?As people defaulted, the value of existing prefabricated houses fell, because of the glut of unsold houses, both new and used. ?This had an effect, even on older deals, and temporarily, loss rates spiked above the levels that would impair the bonds that I bought if the levels stayed that high.

With the ratings lowered, more capital had to be put up against the positions, which the insurance company did not want to do, because they always levered themselves up more highly than most companies — they never had capital to spare, so any loss on bonds was a disaster to them.

They feared the worst, and sold the bonds at a considerable loss, and blamed me.

[sigh]

Easy to demonize the one that is gone, and forget the good that he did, and that others had charge of it during the critical period. ?So what happened to the MHABS bonds that I bought?

Every single one of those bonds paid off in full. ?Held to maturity, not one of them lost a dime.

What was my error?

Part of being a good investor is knowing your client. ?In my case, the client was an impossible one, demanding high yields, low capital employed, and no losses. ?I should have realized that at some later date, under a horrific scenario, that the client would not be capable of holding onto the securities. ?For that reason, I should have never bought them in the first place. ?Then again, I should have never bought anything with any risk for them under those conditions, because in a large enough portfolio, you will have some areas where the risk will surprise you. ?This was less than 2% of the consolidated assets of the firm, and they can’t hold onto securities that would likely be money good amid a panic?!

Sadly, no. ?As their corporate bond manager, before I left, I sold down positions like that that my replacement might not understand, but I did not control the MHABS portfolio then, and so I could?not do that.

Maybe $50 million went down the drain here. ?On the bright side, it helped teach me what would happen in the housing bubble, and my next employer benefited from those insights.

Thus the lesson is: only choose investments that your client will be capable of holding even during horrible times, because the worst losses come from panic selling.

Next time, my two worst stock losses from my hedge fund days.

Information received since the Federal Open Market Committee met in January suggests that economic growth has moderated somewhat.

Information received since the Federal Open Market Committee met in March suggests that economic growth slowed during the winter months, in part reflecting transitory factors.

Shades GDP down. ?Why can?t the FOMC accept that the economy is structurally weak?

Labor market conditions have improved further, with strong job gains and a lower unemployment rate. A range of labor market indicators suggests that underutilization of labor resources continues to diminish.

The pace of job gains moderated, and the unemployment rate remained steady. A range of labor market indicators suggests that underutilization of labor resources was little changed.

Shades labor use down.

Household spending is rising moderately; declines in energy prices have boosted household purchasing power. Business fixed investment is advancing, while the recovery in the housing sector remains slow and export growth has weakened.

Growth in household spending declined; households’ real incomes rose strongly, partly reflecting earlier declines in energy prices, and consumer sentiment remains high. Business fixed investment softened, the recovery in the housing sector remained slow, and exports declined.

Shades down their view of household spending.? Adds a comment on consumer sentiment.

Also shades down business fixed investment and exports.

Inflation has declined further below the Committee’s longer-run objective, largely reflecting declines in energy prices. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations have remained stable.

Inflation continued to run below the Committee’s longer-run objective, partly reflecting earlier declines in energy prices and decreasing prices of non-energy imports. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy.

The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate.

Although growth in output and employment slowed during the first quarter, the Committee continues to expect that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate.

No real change. They are fitting Einstein?s definition of insanity ? doing the same thing, and expecting a different outcome.

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of energy price declines and other factors dissipate. The Committee continues to monitor inflation developments closely.

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

No change.

Consistent with its previous statement, the Committee judges that an increase in the target range for the federal funds rate remains unlikely at the April FOMC meeting.

Deleted

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

No change.

No rules, just guesswork from academics and bureaucrats with bad theories on economics.

This change in the forward guidance does not indicate that the Committee has decided on the timing of the initial increase in the target range.

Deleted

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

No change.? Changing that would be a cheap way to effect a tightening.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

?Balanced? means they don?t know what they will do, and want flexibility.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Jeffrey M. Lacker; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Jeffrey M. Lacker; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

No change, sadly.

We need some people in the Fed and in the government who realize that balance sheets matter ? for households, corporations, governments, and central banks.? Remove anyone who is a neoclassical economist ? they missed the last crisis; they will miss the next one.

Comments

With this FOMC statement, people should conclude that they have no idea of when the FOMC will tighten policy, if ever. This is the sort of statement they issue when things are ?steady as you go.?? There is no hint of imminent policy change.

The FOMC has a weaker view of GDP, labor use, household spending, business fixed investment and exports.

Despite lower unemployment levels, labor market conditions are still pretty punk. Much of the unemployment rate improvement comes more from discouraged workers, and part-time workers.? Wage growth is weak also.

Forward inflation expectations have reversed direction and are rising, and the twitchy FOMC did not note it.

Equities rise and long bonds rise. Commodity prices fall and the dollar rises.? The FOMC says that any future change to policy is contingent on almost everything.

Don?t know they keep an optimistic view of GDP growth, especially amid falling monetary velocity.

The key variables on Fed Policy are capacity utilization, labor market indicators, inflation trends, and inflation expectations. As a result, the FOMC ain?t moving rates up, absent improvement in labor market indicators, much higher inflation, or a US Dollar crisis.

We have a congress of doves for 2015 on the FOMC. Things will be boring as far as dissents go.? We need some people in the Fed and in the government who realize that balance sheets matter ? for households, corporations, governments, and central banks.? Remove anyone who is a neoclassical economist ? they missed the last crisis; they will miss the next one.

Saving unicorns from themselves? There was an interesting piece last week from Martin Peers in The Information?(sub req), arguing that the private markets need some sort of shorting mechanism so that there is a check on unreasonable valuation inflation. It would make the market more efficient, Peers argues, even though implementation would require several structural changes (particularly to stock transfer rules). He writes:

“Private companies will probably resist the development of a short-selling market, given it would hurt valuations, which in turn can undermine the value of employee option programs, and give them less control over their shareholder group. But those risks are likely to be outweighed by the long term benefits of bringing more buyers into the market and ensuring the company’s valuation can be sustained outside of the constraints of the private market.”

Leaving out the technical difficulties — including?the lack of ongoing price discovery — one big counter could be that shorts didn’t so much to stop the earlier dotcom bubble (which largely took place in the public markets).

Adam D’Augelli of True Ventures pointed me to a 2002 academic paper (Princeton/London Biz School) that found “hedge funds during the time of the technology bubble on the Nasdaq… were heavily tilted towards overpriced technology stocks.” They add that “arbitrageurs are concerned about attacking the bubble too early without support from their peers,” and that they’re more likely to ride the bubble until just a few months before the end.

That would seem to be?too late to impose price discipline in private markets, but I’m curious in your thoughts. Does some sort of private shorting system make sense? And, if so, how would it be structured?

I’m going to take a stab at answering the final questions. ?There is often a reason why the financial world is set up the way it is, and why truly helpful financial innovations are rare. ?The answer is “no, we should not have any way of shorting private companies, and it is not a flaw in the system that we don’t have any easy way to do it.”

Two notes before I start: 1) I haven’t read the paper at The Information, because it is behind a paywall, but I don’t think I need to do so. ?I think the answer is obvious. ?2) I ran into this question answered at Quora. ?The answers are pretty good in aggregate, but what exists here are my own thoughts to present the answer in what I hope is a simple manner.

What is required to have an effective means of shorting assets

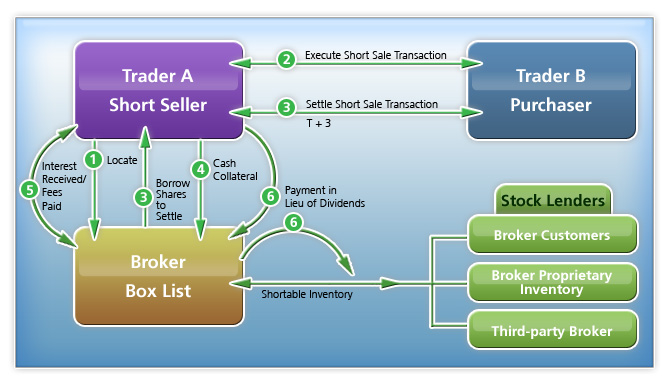

An asset must be capable of being easily transferred from one entity to another.

Entities willing to lend the asset in exchange for some compensation over a given lending term.

Entities willing to borrow the asset, put up collateral adequate to secure the asset, and then sell the asset to another entity.

An entity or entities to oversee the transaction, provide custody of the collateral, transmit payments, assure return of the asset at the end of the lending term, and gauge the adequacy of collateral relative to the value of the asset.

I’m leaving aside the concept of naked shorting, because there are a lot of bad implications to allowing a third party to create ownership interests in a firm, a power which is reserved for?the firm itself.

The Troubles Associated with Shorting Private Assets

I can think of four?troubles. ?Here they are:

The ability to sell, lend, or buy shares in a private company are limited by the private company.

Lending over long terms with no continuous?price mechanism to aid in the gradual adjustment of collateral could lead to losses for the lender if the borrower can’t put up additional capital.

The asset lender can decide only to lend over lending?terms that will likely be disadvantageous to the borrower. ?Getting the asset returned at the end of the lending term could be problematic.

It is difficult enough shorting relatively illiquid publicly traded assets. ?Liquidity is required for any regular?shorting to happen.

The first one is the killer. ?There are no advantages to a private company to allow for the?mechanisms needed to allow for shorting. That is one of the advantages of being private. ?Information is not shared openly, and you can use the secrecy to aid your competitive edge. ?Skeptical short-sellers would not be welcome.

The second problem is tough, because sometimes?successive capital rounds are at considerably higher prices. ?The borrower will likely not have enough slack assets to increase his collateral, and he will be forced to buy shares in the round to cover his short because of that. ?The lender could find that the borrower cannot make good on the loan, and so the lender loses a portion of the value his ownership stake.

But imagining the first two problems away, problem three would still be significant. ?If the term for lending were not all the way to the IPO, next capital round or dissolution/sale, at the end of the term, the borrower would have to look for someone to sell shares to him. ?It is quite possible that no one would sell them at any reasonable price. ?They know they have a forced buyer on their hands, and there could be informal collusion on the price of a sale.

Perhaps another way to put it is don’t play in a game where the other team has significant control over the rules of the game. ?One of the reasons I say this is from my days of a bond manager. ?There were a lot of games played in securities lending, and bonds?are?not the most liquid place to short assets. ?I remember it being very difficult to get a bond back from an entity that borrowed it, and the custodian and trustee did not help much. ?I also remember how we used to gauge the liquidity of bonds we lent out, and if one was particularly illiquid, we would always recall the bond before selling it, which would often make the price of the bond rise. ?Games, games, games…

What Might Be Better

Perhaps using collateralized options or another type of derivative could allow bets to be taken, if the term extended all the way to the IPO, the next capital round, or dissolution/sale of the company. ?The options would have to be limited to the posted collateral being the most the seller of the option could lose. ?Some of the above four issues would still be in play at various points, but aside from issue one, this would minimize the troubles.

What Might Be Better Still

The value of the shorts is that they share information with the rest of the market that there is a bearish opinion on an asset. ?Short-sellers are nice to have around, but not necessary for the asset pricing function. ?It is not unreasonable to live with the problem that some assets will be overvalued in the intermediate-term, rather than set up a complex method to try to enable shorting. ?As Ben Graham said:

?In the short run, the market is a voting machine but in the long run, it is a weighing machine.?

The weighing machine will do its job soon enough, showing that the overvalued asset will never produce free cash adequate to justify its current high price. ?Is it a trouble?to wait for that to happen? ?If you don’t own it, you shouldn’t care much.

If you want to short it, I’m not sure that will hasten the price adjustment process that much, unless you can convince the existing owners of the asset that it isn’t worth even the current price. ?Given that buyers have convinced themselves to own the asset, because they think it will be worth more in the future, intellectually, convincing them that it is worth less?is a tough sell.

In the end, only asset and liability cash flows count, regardless of what secondary buyers and sellers do. ?Secondary trading does not affect the value of assets, though it may affect the perception of value in the short run. ?Thus, you don’t need short sellers to aid in setting secondary market prices, but they are an aid there. ?In the primary markets, where whole companies are bought and sold, the perceived cash return is all that matters.

Conclusion

Ergo, live with short run overvaluation in private markets. ?It is a high quality problem. ?Sell overvalued assets?if you own them. ?Watch if you don’t own them. ?Shorting, even if possible, is not worth the bother.

Despite the large and seemingly meaty title, this will be a short piece. ?I class these types of investors together because most of them have long investment horizons. ?From an asset-liability management standpoint, that would mean they should invest similarly. ?That may be have been true for Defined Benefit [DB] pension plans and Endowments, but that has shifted over time, and is increasingly not true. ?In some ways, the DB plans are becoming more like life insurers in the way they invest, though not totally so. ?So, why do they invest differently? ?Two reasons: internal risk management goals, and the desires of insurance?regulators to preserve industry solvency.

Let’s start with life insurers. ?Regulators don’t want insolvent companies, so they constrain companies into safe assets using risk-based capital charges. ?The riskier the investment, the more capital the insurer has to put up against it. ?After that, there is cash-flow testing which tends to push life insurers to match assets and liabilities, or at least, not have a large mismatch. ?Also, accounting rules may lead insurers to buy assets where the income will show up on their financial statements regularly.

The result of this is that life insurers don’t invest much in risk assets — maybe they invest in stocks, junk bonds, etc. up to the amount of their surplus, but not much more than that.

DB plans don’t have regulators that care about investment risks. ?They do have plan sponsors that do care about investment risk, and that level of care has increased over the past 15?years. ?Back in?the late ’90s it was in vogue for DB plans to allocate more and more to risk assets, just in time for the market to correct. ?(Note to retail investors: professionals may deride your abilities, but the abilities of many professionals are questionable also.)

Over that time, the rate used to discount DB plan liabilities became standardized and attached to long high quality bonds. ?Together with a desire to minimize plan funding risks, and thus corporate risks for the plan sponsor, that led to more investments in bonds, and less in equities and other risk assets. ?Some plans try to cash flow match expected future plan payments out to a horizon.

Finally, endowments have no regulator, and don’t have a plan sponsor?that has to make future payments. ?They are free to invest as they like, and probably have the highest degree of variation in their assets as a group. ?There is some level of constraint from the spending rules employed by the endowments, particularly since 2008-9, when a number of famous endowments came to realize that there was a liability structure behind them when they ran low on liquidity amid the crisis. [Note: long article.] ?You might think it would be smart to have the present value of 3-5?years of expenditures on hand in bonds, but that is not always the case. ?In some ways, the quick recovery taught some endowment investors the wrong lesson — that they could wait out any crisis.

That’s my quick summary. ?If you have thoughts on the matter, you can share them in the comments.

{kind=link}