He’s arguing that monetary policy has been too loose for too long, though a zero percent policy was needed for a time. ?Cites this paper here. ?Gives a confusing neo-Fisherian model — simple models don’t do justice to a complex economy. ?Argues that low rates lead to low price inflation. ?(Personally, all of this neglects demographics, and the relative propensity of monetary policy to funnel marginal money into asset or goods markets.)

Monetary policy near the zero bound creates its own demand for abnormal policy tools. ?Thinks that economy is pretty normal now, and there is no need for excess stimulus now. ?Thinks that current policy will lead to bad results if maintained.

Q&A — Selgin of Cato — Says Fisher would spin in his grave, that public natively facilitates Fed policy, which is not natural.

Fisher argues that you have to have an equilibrium concept in economics. ?How than to explain low rates and low inflation.

Q2 — Politics and the Fed — what does he think of GOP candidate comments?

Information received since the Federal Open Market Committee met in July suggests that economic activity is expanding at a moderate pace.

Information received since the Federal Open Market Committee met in September suggests that economic activity has been expanding at a moderate pace.

Shows less certainty about current GDP.

Household spending and business fixed investment have been increasing moderately, and the housing sector has improved further; however, net exports have been soft.

Household spending and business fixed investment have been increasing at solid rates in recent months, and the housing sector has improved further; however, net exports have been soft.

Shades up household spending.

The labor market continued to improve, with solid job gains and declining unemployment. On balance, labor market indicators show that underutilization of labor resources has diminished since early this year.

The pace of job gains slowed and the unemployment rate held steady. Nonetheless, labor market indicators, on balance, show that underutilization of labor resources has diminished since early this year.

Shades labor employment down a little.

Inflation has continued to run below the Committee’s longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports.

Inflation has continued to run below the Committee’s longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports.

No change.

Market-based measures of inflation compensation moved lower; survey-based measures of longer-term inflation expectations have remained stable.

Market-based measures of inflation compensation moved slightly lower; survey-based measures of longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy.

Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.

Well, that sentence lasted for one meeting.? Would that more got chopped out of the statement.

Nonetheless, the Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate.

The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate.

No real change.

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced but is monitoring developments abroad. Inflation is anticipated to remain near its recent low level in the near term but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely.

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced but is monitoring global economic and financial developments. Inflation is anticipated to remain near its recent low level in the near term but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely.

CPI is at +0.0% now, yoy.? States that they have a global view of what they need to watch.? Good luck with that.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining whether it will be appropriate to raise the target range at its next meeting, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Gives the impression that a change might be coming at the next meeting, but the way the FOMC thinks about monetary policy is currently scattered, to say the least.

I wouldn?t make too much of this change.? The FOMC is big on their newfound flexibility, and isn?t going to be very predictable for some time.

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

No change.

No rules, just guesswork from academics and bureaucrats with bad theories on economics.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

No change.? Changing that would be a cheap way to effect a tightening.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

No Change.

?Balanced? means they don?t know what they will do, and want flexibility.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

Still a majority of doves.

We need some people in the Fed and in the government who realize that balance sheets matter ? for households, corporations, governments, and central banks.? Remove anyone who is a neoclassical economist ? they missed the last crisis; they will miss the next one.

Voting against the action was Jeffrey M. Lacker, who preferred to raise the target range for the federal funds rate by 25 basis points at this meeting.

Voting against the action was Jeffrey M. Lacker, who preferred to raise the target range for the federal funds rate by 25 basis points at this meeting.

No change.? Lacker dissents, arguing policy has been too loose for too long.

Comments

This FOMC statement was yet another great big nothing. Only notable changes were shading household spending up, and employment and GDP down.

Don?t expect tightening in December. People should conclude that the FOMC has no idea of when the FOMC will tighten policy, if ever.? The FOMC says that any future change to policy is contingent on almost everything.

On the new phrase, ?whether it will be appropriate to raise the target range at its next meeting,? I would not make much of it. It gives the impression that a change might be coming at the next meeting, but the way the FOMC thinks about monetary policy is currently scattered, to say the least.? I wouldn?t make too much of this change.? The FOMC is big on their newfound flexibility, and isn?t going to be very predictable for some time.

Despite lower unemployment levels, labor market conditions are still pretty punk. Much of the unemployment rate improvement comes more from discouraged workers, and part-time workers.? Wage growth is weak also.

Equities fall and bonds rise. Commodity prices fall and the dollar rises.? This is a sign that the markets anticipate more economic weakness.

The FOMC says that any future change to policy is contingent on almost everything.

Don?t know they keep an optimistic view of GDP growth, especially amid falling monetary velocity.

The key variables on Fed Policy are capacity utilization, labor market indicators, inflation trends, and inflation expectations. As a result, the FOMC ain?t moving rates up, absent improvement in labor market indicators, much higher inflation, or a US Dollar crisis.

We have a congress of doves for 2015 on the FOMC. Things will continue to be boring as far as dissents go.? We need some people in the Fed and in the government who realize that balance sheets matter ? for households, corporations, governments, and central banks.? Remove anyone who is a neoclassical economist ? they missed the last crisis; they will miss the next one.

I have my list of concerns for the economy and the markets:

Unexpected Global Macroeconomic Surprises, including more from China

Student Loans, Agricultural Loans, Auto Loans — too much

Exchange Traded Products — the tail is wagging the dog in some places, and ETPs are very liquid, but at a cost of reducing liquidity to the rest of the market

Low risk margins — valuations for equity and debt are high-ish

Demographics — mostly negative as populations across the globe age

Wages in the “developed world” are getting pushed to the levels of the “developing world,” largely due to the influence of information technology. ?Also, technology is temporarily displacing people from current careers.

This is worth watching. ?It seems like there isn’t that much advantage to corporate borrowing now — the arbitrage of borrowing to buy back stock seems thin, as does borrowing to buy up competitors. ?That doesn’t mean it is not being done –?people imitate the recent past as a useful shortcut to avoid thinking. ?Momentum carries markets beyond equilibrium as a result.

If the Federal Reserve stimulates by duping getting economic actors to accelerate current growth by taking on more debt, it has worked here. ?Now where is leverage low? ?Across the board, debt levels aren’t far from where they were in 2008:

As such, I’m not sure where we go from here, but I would suggest the following:

Start lightening up on bonds and stocks that would concern you if it were difficult to get financing. ?How well would they do if they had to self-finance for three years?

Fiscal policy will remain riven by disagreements, and hamstrung by rising entitlement spending.

Long Treasuries don’t look bad with inflation so low.

Leave a little liquidity on the side in case of a negative surprise. ?When everyone else has high debt levels, it is time to reduce leverage.

Better safe than sorry. ?This isn’t saying that the equity markets can’t go higher from here, that corporate issuance can’t grow, or that corporate spreads can’t tighten. ?This is saying that in 2004-2006, a lot of the troubles that were going to come were already baked into the cake. ?Consider your current positions carefully, and develop your plan for your future portfolio defense.

Here are two ideas for the Fed, not that they care much about what I think:

1) Stop holding regular press conferences and holding regular meetings. ?Only meet when a supermajority of your members are calling for a change in policy. ?Don’t announce that you are holding a meeting — perhaps do it via private video conference.

Part of the reason for this is that it is useless to listen to commentary about why you did nothing. ?You may as well have not held a meeting. ?Another reason is that governors could act more independently if a meeting can’t be called unless a supermajority of voting members calls for it.

Yet another reason is that the frequent and long communication has not eliminated the Kremlinology that exists to interpret the Fed. ?When changes to the FOMC statement are small, they get over-interpreted — remember the “taper” comment? ?Far better to say nothing than to repeat yourself with small meaningless variations.

Along with that, you could eliminate issuing statements altogether, and go back to the way things were done pre-Greenspan. ?Need it be mentioned that monetary was executed better under Volcker and Martin? ?We don’t need words, we need to feel the actions of the Fed. ?That brings me to:

2) Stop trying to support risky asset markets. ?It is not your job to give equity or corporate bond investors what they want. ?If you do that, too much liquidity gets injected into the system, creating the financial bubbles of 2000 and 2007-9.

Instead, give the risk markets some negative surprises. ?Don’t follow Fed funds futures; make them follow you. ?Show them that you are the boss, not the slave. ?Let recessions do their good work of clearing out bad debts, and then the economy can grow on a better basis. ?Be like Martin, and take away the punchbowl when the party gets exciting.

Do these things and guess what? ?Monetary policy will have more punch. ?When you make a decision, it will actually do something.

If were going to have fiat money, do it in such a way that bubbles do not develop, which means not caring about the effects of policy on risky asset markets. ?This might not be popular, but it would be good for the economy in the long run.

-==-=–==–==–=-=-=-=-=-=-=-=-=-=-=-=-=-=-=–=-=

As a final note let me end with one chart from the recent data from FOMC participants:

I?suspect the FOMC will tighten in December, but remember that the FOMC doesn’t have a roadmap for the environment they are in, and they are acting like slaves to the risky asset markets. ?Another burp in the markets, and lessening policy accommodation will be further delayed.

Information received since the Federal Open Market Committee met in June indicates that economic activity has been expanding moderately in recent months.

Information received since the Federal Open Market Committee met in July suggests that economic activity is expanding at a moderate pace.

No real change.

Growth in household spending has been moderate and the housing sector has shown additional improvement; however, business fixed investment and net exports stayed soft.

Household spending and business fixed investment have been increasing moderately, and the housing sector has improved further; however, net exports have been soft.

No real change. Swapped places with the following sentence.

The labor market continued to improve, with solid job gains and declining unemployment. On balance, a range of labor market indicators suggests that underutilization of labor resources has diminished since early this year.

The labor market continued to improve, with solid job gains and declining unemployment. On balance, labor market indicators show that underutilization of labor resources has diminished since early this year.

No real change. Swapped places with the previous sentence.

Inflation continued to run below the Committee’s longer-run objective, partly reflecting earlier declines in energy prices and decreasing prices of non-energy imports.

Inflation has continued to run below the Committee’s longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports.

No real change.

Market-based measures of inflation compensation remain low; survey?based measures of longer-term inflation expectations have remained stable.

Market-based measures of inflation compensation moved lower; survey-based measures of longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy.

Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.

New sentence.? Nods at the recent volatility in risky asset markets here and abroad.

The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate.

Nonetheless, the Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate.

No real change.

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of earlier declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely.

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced but is monitoring developments abroad. Inflation is anticipated to remain near its recent low level in the near term but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

No change.

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen some further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

No change.

No rules, just guesswork from academics and bureaucrats with bad theories on economics.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

No change.? Changing that would be a cheap way to effect a tightening.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

No Change.

?Balanced? means they don?t know what they will do, and want flexibility.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Jeffrey M. Lacker; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

Still a majority of doves.

We need some people in the Fed and in the government who realize that balance sheets matter ? for households, corporations, governments, and central banks.? Remove anyone who is a neoclassical economist ? they missed the last crisis; they will miss the next one.

Voting against the action was Jeffrey M. Lacker, who preferred to raise the target range for the federal funds rate by 25 basis points at this meeting.

Lacker dissents, arguing policy has been too loose for too long.

Comments

This FOMC statement was another great big nothing. Only notable change was the influence of risky asset markets and foreign markets on the decision-making process on the FOMC.

Don?t expect tightening in October. People should conclude that the FOMC has no idea of when the FOMC will tighten policy, if ever.? This is the sort of statement they issue when things are ?steady as you go.?? There is no hint of imminent policy change.

Despite lower unemployment levels, labor market conditions are still pretty punk. Much of the unemployment rate improvement comes more from discouraged workers, and part-time workers.? Wage growth is weak also.

Equities flat and long bonds rise. Commodity prices rise and the dollar falls.

The FOMC says that any future change to policy is contingent on almost everything.

Don?t know they keep an optimistic view of GDP growth, especially amid falling monetary velocity.

The key variables on Fed Policy are capacity utilization, labor market indicators, inflation trends, and inflation expectations. As a result, the FOMC ain?t moving rates up, absent improvement in labor market indicators, much higher inflation, or a US Dollar crisis.

We have a congress of doves for 2015 on the FOMC. Things will continue to be boring as far as dissents go.? We need some people in the Fed and in the government who realize that balance sheets matter ? for households, corporations, governments, and central banks.? Remove anyone who is a neoclassical economist ? they missed the last crisis; they will miss the next one.

Today, I happened to stumble across an old article of mine: Easy In, Hard Out (Updated). ?It’s kind of long, but goes into the changes that have happened at the Fed since the crisis, and points out why tightening policy might be tough. ?Nothing has changed in the 2.4 years since I wrote it, so I am going to reprint the end of the article. ?Let me know what you think.

-==-=-=–==-=–=-==-=-=-=-=-

In normal times, central banks buy only government debt, and keeps the assets relatively short, at longest attempting to mimic the existing supply of government debt.? Think of it this way, purchases/sales of longer debt injects/removes liquidity for longer periods of time.? Staying short maintains flexibility.

Yes, the Fed does not mark its securities or gold to market.? Under most scenarios, it is impossible for a central bank which can issue its own currency to go broke.? Rare exceptions ? home soil wars that fail, or political repudiation of the bank, where the government might create a new monetary standard, or closes the bank because of inflation.? (Hey, the central bank has been eliminated twice before.? It could happen again.)

The only real effect is on how much?seigniorage the Fed remits to the Treasury, or, if things go bad, how much the Treasury would have to lend/send to the central bank in order to avoid the bad optics of negative capital, perhaps via the Supplemental Financing Account.? This isn?t trivial; when people hear the central bank is ?broke,? they will do weird things.? To avoid that, the Fed?s gold will be revalued to market at minimum; hey maybe the Fed at that time will be the vanguard of market value accounting, and revalue everything.? Can you imagine what the replacement cost of the NY Fed building is?? The temple in DC?

Or, maybe the bank would be recapitalized by its member banks, if they are capable of doing so, with the reward being the preferred dividend they receive.

Back to the main point.? What effect will this abnormal monetary policy have in the future?

Scenarios

1) Growth strengthens and inflation remains low.? In this unusual combo, it will be easy?for the Fed to collapse its balance sheet, and raise rates.? This is the dream scenario; and I don?t think it is likely.? Look at the global economy; there is a lot of slack capacity.

2) Growth strengthens and inflation rises.? The Fed will likely raise the interest on reserves rate, but not sell bonds.? If they do sell bonds, the market will back up, and their losses will be horrible.? If don?t take the losses,?seigniorage could be considerably reduced, or even vanish, as the Fed funds rate rises, but because of the long duration asset portfolio, asset income rises slowly.? This is where the asset-liability mismatch bites.

If the Fed doesn?t raise the interest on reserves rate, I suspect banks would be willing to lend more, leaving fewer excess reserves at the Fed, which could stimulate more inflation. Now, there are some aspects of inflation that remain a mystery ? because sometimes inflationary conditions affect assets, rather than goods, I think depending on demographics.

3) Growth weakens and inflation remains low.? This would be the main scenario for QE4, QE5, etc.? We don?t care much about the Fed?s balance sheet until the Fed wants to raise rates, which is mainly a problem in Scenario 2.

4) Growth weakens and inflation rises, i.e. stagflation.? There?s no good set of policy options here. The Fed could engage in further financial repression, keeping short rates low, and let inflation reduce the nominal value of debts.? If it doesn?t run wild, it could play a role in reducing the indebtedness of the whole economy, though again, it will favor debtors over savers.? (As I?ve said before, in a situation like this, or like the Eurozone, all creditors want to be paid back at par on the bad loans that they have made, and it can?t be done.? The pains of bad debt have to go somewhere, where it goes is the argument.)

I?ve kept this deliberately simple, partially because with all of the flows going back and forth, and trying to think of the whole system, rather than effects on just one part, I know that I have glossed over a lot.? I accept that, and I could be dead wrong, as I sometimes am.? Comment as you like, with grace and dignity, and let us grow together in our knowledge.? I?ve been spending some time reading documents at the Fed, trying to understand their mechanisms, but I could always learn more.

Summary

During older times, the end of a Fed loosening cycle would end with the Fed funds rate rising.? In this cycle, it will end with interest of reserves rising, and/or, the sale of bonds, which I find less likely (they will probably be held to maturity, absent some crisis that we can?t imagine, or non-inflationary growth).? But when the tightening cycle comes, the Fed will find that its actions will be far harder to take than when they made the ?policy accommodation.?? That has always been true, which is why the Fed during its better times limited the amount of stimulus that it would deliver, and would tighten sooner than it needed to.

Far better to be like McChesney Martin or Volcker, and be tough, letting recessions do their necessary work of eliminating bad debt.? Under Greenspan, and Bernanke to a lesser extent (though he persists in pushing the canard that the Fed was not too loose 2003-2004, ask John Taylor for more), there were many missed opportunities to stop the buildup of bad debts, but the promise of the ?Great Moderation? beguiled so many.

Removing policy accommodation is always tougher than imagined, and carries new risks, particularly when new tools have been used.? Bernanke can go to his carefully chosen venues and speak to his carefully chosen audiences, and try to exonerate the Fed from well-deserved blame for their looseness in the late 80s, 90s, and 2000s.? Please, Mr. Bernanke, take some blame there on behalf of the Fed ? the credit boom could never have happened without the Fed.? Painting the Fed as blameless is wrong; the ?Greenspan put? landed us in an overleveraged bust.

I?m not primarily blaming the Fed for its current conduct; we are still in the aftermath of a lending bust ? too much bad mortgage debt, with a government whose budget is out of balance.? (In the bust, there are no good solutions.)? I am blaming the Fed for loose policies 1984-2007, monetary policy should have been a lot tighter on average.? But now we live with the results of prior bad policy, and may the current Fed not compound it.

Postscript

The main difference between this time and the last time I wrote on this is QE3.? What has been the practical impact since then?? The Fed owns more MBS and long maturity Treasuries, financed by more reserve balances at the Fed.

Banks use this cheap funding to finance other assets.? But if they want to make money, the banks have to take credit risk (something the Fed is trying to stimulate), and/or interest rate rate risk (borrow short, lend long, negative convexity, etc).? The longer low rates go on through interest on reserves, the greater the tendency to build up imbalances in the banking system through credit and interest rate risks. 1992-1993 where Fed funds rates were held at 3%, was followed by the residential mortgage backed security market melting down in 1994, not to mention Mexico.? Sub-2% Fed funds rates from 2002 through mid-2004 led to massive overinvestment in residential housing, leading to the present crisis.

Fed tightening cycles often start with a small explosion where short-dated financing for thinly capitalized speculators evaporates, because of the anticipation of higher financing rates.? Fed tightening cycles often end with a large explosion, where a large levered asset class that was better financed, was not financed well-enough.? Think of commercial property in 1989, the stock market in 2000 (particularly the NASDAQ), or housing/banks in 2008.? And yet, that is part of what Fed policy is supposed to do: reveal parts of the economy that are running too hot, so that capital can flow from misallocated areas to areas that are more sound.? At present, my suspicion is that we still have more trouble to come in banking sector.? Here?s why:

We?ve just been through 4.5 years of Fed funds / Interest on reserves being below 0.5% ? this is a far greater period of loose policy than that of 1992-1993 and 2002 to mid-2004 together, and there is no apparent end in sight.? This is why I believe that any removal of policy accommodation will prove very difficult.? The greater the amount of policy accommodation, the greater the difficulties of removal.? Watch the fireworks, if/when they try to remove it.? And while you have the opportunity now, take some risk off the table.

This should be short. There are a lot of good reasons not to worry about the FOMC raising Fed funds or not. ?If they raise Fed funds:

First, savers deserve a return. ?Economies work better when savers get rewarded.

Second, investors do better on the whole when there is a risk free asset earning something to allocate money to, because otherwise investors take too much risk in an effort to generate income.

Third, the FOMC should never have let Fed funds rates go below 1% anyway — the marginal stimulus is limited once the yield curve gets slope enough for the banks to lend. ?They don’t really need more than that.

Fourth, it’s not as if monetary policy has been doing that much. ? Outside of the government and corporations, most entities have not shown a lot of desire to lever up after the financial crisis.

Fifth, long Treasury yields will do what they want to do — they won’t necessarily go up… it all depends on how strong the economy is.

But if the they don’t raise Fed funds, no big deal. ?We wait a little longer. ?What’s the difference between having zero interest rates for 6.5 years and 7.5 years? ?Either one would build up enough leverage if the economy had the oomph to absorb it.

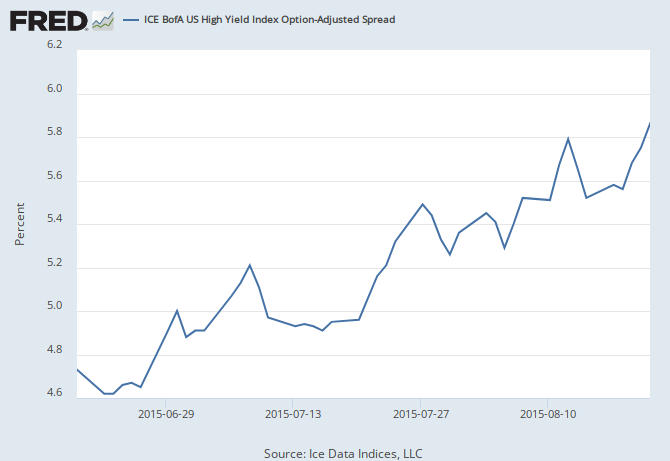

As it is, corporate borrowing has been the major place of debt expansion through both loans and bonds. ?Watch the debt of energy firms that are allergic to low crude oil prices. ?Honorable mention goes to auto, student, and agricultural lending. ?May as well mention that underwriting standards are slipping in some areas for consumers, but things aren’t nuts yet.

I’ve often said that the FOMC stops tightening rates when something big blows up. ?Can’t see what it will be this time — the energy sector will be hurt, but it isn’t big enough to impair financials as a group. ?Subprime lending is light at present outside of autos.

Watch and see, but in my opinion, it is a sideshow. ?Watch how the long end behaves, and see if the market reflates. ?We need more confusion and less concern over what the next crisis is, before any significant crisis comes.

I try not to be an ideologue, and I often fail. One bias of mine is that most macroeconomic policy actions of the government or central bank either don’t help, or merely shift the problem to another place.

Tonight’s issue is the wealth effect, which tends to be favored more by conservatives. ?The wealth effect is the tendency to spend more as the market value of the assets of a person rises. ?I don’t think the wealth effect is zero, but I don’t think can be?very big, and tonight, I will explain why.

Now, imagine that you own some assets and the value of them has grown. ?You’re feeling richer, and you would like to live richer as a consequence. ?How are you going to do it? ?You could:

Sell some of the assets.

Borrow against the assets.

If you control the assets, you could increase the stream of dividends, or pay yourself a higher salary.

Trade the assets for assets that pay a higher income.

Do more exotic things, like sell call options — but let’s ignore those possibilities for now. ?Those are just contingent forms of selling.

Let’s take these in order:

Sell Assets

Selling appreciated assets in most cases means incurring a capital gain and paying taxes. ?It can be an effective way of raising your purchasing power on a one-time basis. ?It also means that someone like you, or, one of their representatives, is going to have to part with money so that you can receive cash for your money. ?The net effect for the economy is not likely to be an increase of cash spent on consumption as a result.

As an aside, some people might be averse to selling assets in a big way because they don’t want to consume capital. ?They may not believe that the remainder of their assets will continue to rise in value, and as such might not be willing to spend from realized capital gains. ?That said, many older people *will* have to consume capital in old age, but they aren’t well-enough off to produce a wealth effect — they worry whether their assets will last.

Borrow Against Assets

I think this is dangerous if done in a big way, though I have seen some crackpots advocating that. ?We should have learned from the financial crisis that if borrowing against stable assets like a home in order to spend can result in disaster, it does not make sense to do it against more volatile assets like stocks or a private business. ?Your home is not an ATM. ?That same logic should apply to a brokerage account.

If you do borrow against an appreciated asset in order to spend, that may increase your spending one time, but unless the value of your assets continually increases, you won’t be able to do it forever. ?And, if asset values fall dramatically, you may find that if your debts are greater than your assets, that your spending may go down considerably as you pay back debt to hold onto your assets.

Now, if a lot of people are inverted in their borrowing, an increase in the overall price level of assets could make some?people un-invert and breathe easier, and after a while, spend more from their incomes. ?But the rise there will likely be offset by others whose savings aren’t worth as much being reticent to spend.

Pay Yourself a Greater Dividend or Salary

If you own all of a given asset, this?becomes a question of taking income versus spending on capital expenditures to grow or maintain the business. ?Greater personal spending is offset by lesser business spending. ?Oh, and you have to pay tax on the income you receive. ?If you own part of the business, but still control it, receiving a higher salary disproportionately helps you versus your minority shareholders. ?You might be able to spend more, but it comes out of their pockets.

Trade Your Assets for Assets that Pay a Higher Income

First, it’s a simple trade. ?You might have more income to spend, but someone else has less on average. ?Beyond that, it makes more sense to pursue investments that give you the best returns regardless of how much income they pay. ?You can decide on the income you need via dividends, selling bits of the investment, etc.

Income is not an inherent aspect of an asset. ?Within bounds, it is arbitrary, as noted in the two articles to which?I linked. ?As a result, choosing a higher income set of assets may not give you more to spend over time. ?Even if Congress passed a law tomorrow saying that all companies, public and private, have to pay a dividend equal to 3% of market value (or fair value, however determined), it might increase personal taxable income, but many would reinvest it while some would spend. ?As for the corporations, they would have to spend less on capital expenditures, or borrow more to fund them. ?A great increase in spending would be unlikely.

Summary

None of the ways I mentioned for getting more money for spending out of investments is likely to produce a lot of additional spending in aggregate across the economy. ?As a result, I think that the Executive Branch, the Congress, and the Federal Reserve should be cautious of trying to make asset values rise, or encourage more borrowing against assets. ?It will likely not have any significant effect to grow the economy over the intermediate -to-long term.

There is the temptation when market prices move fast after they have been at recent highs to assume that things are going to fall apart. ?Well, guess what? ?That could happen.

I don’t think it is likely though, if falling apart means a scenario like 2008-9,?2000-2 or 1973-4. ?In order to have a significant drawdown in the market, you have to have a lot of leverage collapse, whether that is financial or operating leverage.

Financial leverage is bad debt. ?We have areas of that — student loans, agricultural loans, a modest amount of subprime lending for autos, and a decent amount of lending to junk-rated corporations, but not enough to create a self-reinforcing situation where bad debts can’t be borne by lenders, and lenders then collapse.

Operating leverage is bad assets — building up too much productive capacity such that there will not be enough demand to absorb it for the foreseeable future. ?Or, building capacity that isn’t productive… either way, assets will have to be written down.

There have been a number of parties kvetching about a lack of investment from US corporations, but let’s take this a different direction. ?There hasn’t been a lot of bad investment from US corporations… and part of that may be due to dividend and buyback policies. ?Yes, there are some IPOs that have come out that look marginal. ?I’ve looked at a variety of spin-offs where the underlying business is attractive, but they loaded the spin-off with a sizable slug of debt in order to pay a final dividend to the parent company saying farewell. ?But on the whole, I don’t see a lot of money being wasted by corporations on investments. ?That is another reason why profit margins are high.

Now, a lot of the furor in the markets stems from China, and the effects that slowing growth and/or bad debts in China will have on the US economy. ?Personally, I don’t think this is an issue to worry about, unless you have a lot of investments in China and other emerging markets. ?In general, US markets don’t get deeply hurt by slowdowns or even crises in other countries. ?Even if it means a slowdown in revenue growth for large US corporations, it would also likely mean that US interest rates might fall, which would often make equities fall less as bonds rally.

Also, for foreign affairs to affect the US in a big way, the US would have to have a lot of lending exposure to those nations that are struggling. ?(Think of the LDC nations in the early ’80s.) ?Maybe this is one of the benefits of running current account?deficits — we don’t have money to lend to foreign countries from our net export earnings.

Think of all the significant foreign crises of the last 30 years. ?LDC crisis, Plaza Accords leading to Japan’s lost decades, Mexico, Asian Crisis, European Union difficulties with their fringe nations, Iceland, Greece, Greece, Greece, China, etc. ?There was always temporary indigestion in US markets, but when did it ever weigh on the US markets for a long period? ?Really, it never did. ?So why are we concerned over China?

Regarding the Fed, I abstract from this old post, which quoted a 2005?piece on Fed policy at RealMoney.com, and what blew up at the end of each tightening cycle. ?I list blow-ups up to that point, and mention that I think US Housing is next:

2000 ? Nasdaq

1997-98 ? Asia/Russia/LTCM, though that was a small move for the Fed

1994 ? Mortgages/Mexico

1989 ? Banks/Commercial Real Estate

1987 ? Stock Market

1984 ? Continental Illinois

Early ?80s ? LDC debt crisis

So it moves in baby steps, wondering if the next straw will break some camel?s back where lending has been going on terms that were too favorable. The odds of this 1/4% move creating such a nonlinear change is small, but not zero.

But on the bright side, the odds of a 50 basis point tightening at any point in the next year are even smaller. The markets can?t afford it.

Some worry now about future Fed policy — what will blow up when the Fed tightens too much? ?I would encourage everyone to relax. ?First, we don’t know that the Fed will do anything soon. ?Second, we don’t know if they will do anything much. ?Third, we don’t even know if the Fed has a coherent theory of monetary policy anymore. ?Face it: Yellen has never tightened rates once. ?Bernanke never tightened rates aside from finishing out Greenspan’s plan to invert the yield curve at the beginning of his Chairmanship. ?Almost no one on the FOMC has any significant practical experience with tightening rates. ?What will guide them out of their zero interest rate policy? ?What will be enough?

Even so, tightening cycles usually end with something blowing up. ?Maybe this time it is the emerging markets. ?I don’t see a large concentration of US-based bad debt that the Fed might inadvertently blow up, at least not yet. ?(Maybe the day will come when the US Treasury might complain about rising financing rates. ?After all, debt is high, but affordable while rates are low.)

Valuation is the main issue as I see it at present, as I commented in my recent piece “Stocks or Bonds?” ?When stocks are priced at a level that discounts 4.5%/year returns over the next 10 years, you don’t have a lot of margin for error, especially when you can create a safer bond portfolio that yields the same.

Now, since I wrote that piece, the S&P 500 is down around 10.5%. ?The bond portfolio is down around 4.5% (it was a risky portfolio, and some of the emerging markets bonds hurt), while the Barclays’ Aggregate is up 1%. ?High-yield bond spreads have widened over that time by ~1.2%.

The anticipated return on the S&P 500 has maybe risen by 1%/year over the next 10 years, to 5.5%. ?That said, so has the yield on the risky bond portfolio. ?I see the selloff as being in-line with the yields of risky debt, which at some higher level of spread, will attract buyers, given that there have been no significant defaults recently.

The US stock market could go down another 20% from here, but I think it will be less. ?My main point is that we shouldn’t get a big washout, but just a correction of valuation levels that got too high relative to other risky assets, like junk bonds.

So don’t panic. ?You could still move some assets from stocks to bonds if you want to sleep better, but don’t do anything severe.

Too often in debates regarding the recent financial crisis, the event was regarded as a surprise that no one could have anticipated, conveniently forgetting those who pointed out sloppy banking, lending and borrowing practices in advance of the crisis. ?There is a need for a well-developed model of how a financial crisis works, so that the wrong cures are not applied to the financial system.

All that said, any correct cure will bring about a predictable response from the banks and other lending institutions. ?They will argue that borrower choice is reduced, and that the flow of credit and liquidity to the financial system is also reduced. ?That is not a big problem in the boom?phase of the financial cycle, because those same measures help to avoid a loss of liquidity and credit availability in the bust phase of the cycle. ?Too much liquidity and credit is what fuels eventual financial crises.

To get to a place where we could have a decent model of the state of overall financial credit, we would have to have models that work like this:

The models would have to have both a cash flow and a balance sheet component to them — it’s not enough to look at present measures of creditworthiness only, particularly if loans do not fully amortize debts at the current interest rate. ?Regulatory solvency tests should not automatically assume that borrowers will always be able to refinance.

The models should try to go loan-by-loan, and forecast the ability of each loan to service debts. ?Where updated financial data is available on borrowers, that should be included.

The models should try to forecast the fair market prices of assets/collateral, off of estimated future lending conditions, so that at the end of the loan, estimates can be made as to whether loans would be refinanced, extended, or default.

As asset prices?rise, there has to be a feedback effect into lowered ability to finance new loans, unless purchasing power is increasing as much or more than asset prices. ?It should be assumed that if loans are made at lower underwriting standards than a given threshold, there will be increasing levels of default.

A close eye would have to look for situations where if the property were rented out, it would not earn enough to pay for normalized interest, taxes and maintenance. ?When asset prices are that high, the system is out of whack, and invites future defaults. ?The margin of implied rents over?normalized interest, taxes and maintenance would be the key measure, and the regulators would have to have a function that attributes future losses off of the margin of that calculation.

The cash flows from the loans/mortgages would have to feed through the securitization vehicles, if any, and then to the regulated financial institutions, after which, how they would fund their future liabilities would?have to be estimated.

The models would have to include the repo markets, because when the prices of collateral get too high, runs on the repo market can happen. ?The same applies to portfolio margining agreements for derivatives, futures, and other types of wholesale lending.

There should be scenarios for ordinary recessions. ?There should also be some way of increasing the Ds at that time: death, disability, divorce, disaster, dis-employment, etc. ?They mysteriously?tend to increase in bad economic times.

What a monster. ?I’ve worked with stripped-down versions of this that analyze the Commercial Mortgage Backed Securities [CMBS] market, but the demands of a model like this would be considerable, and probably impossible. ?Getting the data, scrubbing it, running the cash flows, calculating the asset price functions, implied margin on borrowing, etc., would be pretty tough for angels to do, much less mere men.

Thus if I were watching over the banks, I would probably rely on analyzing:

what areas of credit have grown the quickest.

where have collateral prices risen the fastest.

where are underwriting standards declining.

what assets are being financed that do not fully amortize, including all repo markets, margin agreements, etc.

The one semi-practical thing i would strip out of this model would be for regulators to score loans using a model like point 5 suggests. ?Even that would be tough, but even getting that approximately right could highlight lending institutions that are taking undue chances with underwriting.

On a slightly different note, I would be skeptical of models that don’t try to at least mimic the approach of a cash flow based model with some adjustments for market-like pricing of collateral and loans. ?The degree of financing long assets with short liabilities is the key aspect of how financial crises develop. ?If models don’t reflect that, they aren’t realistic, and somehow, I expect that non-realistic models of lending risk will eventually be the rule, because it helps financial institutions make loans in the short run. ?After all, it is virtually impossible to fight loosening financial standards piece-by-piece, because the changes seem immaterial, and everyone favors a boom in the short-run. ?So it goes.

{kind=link}