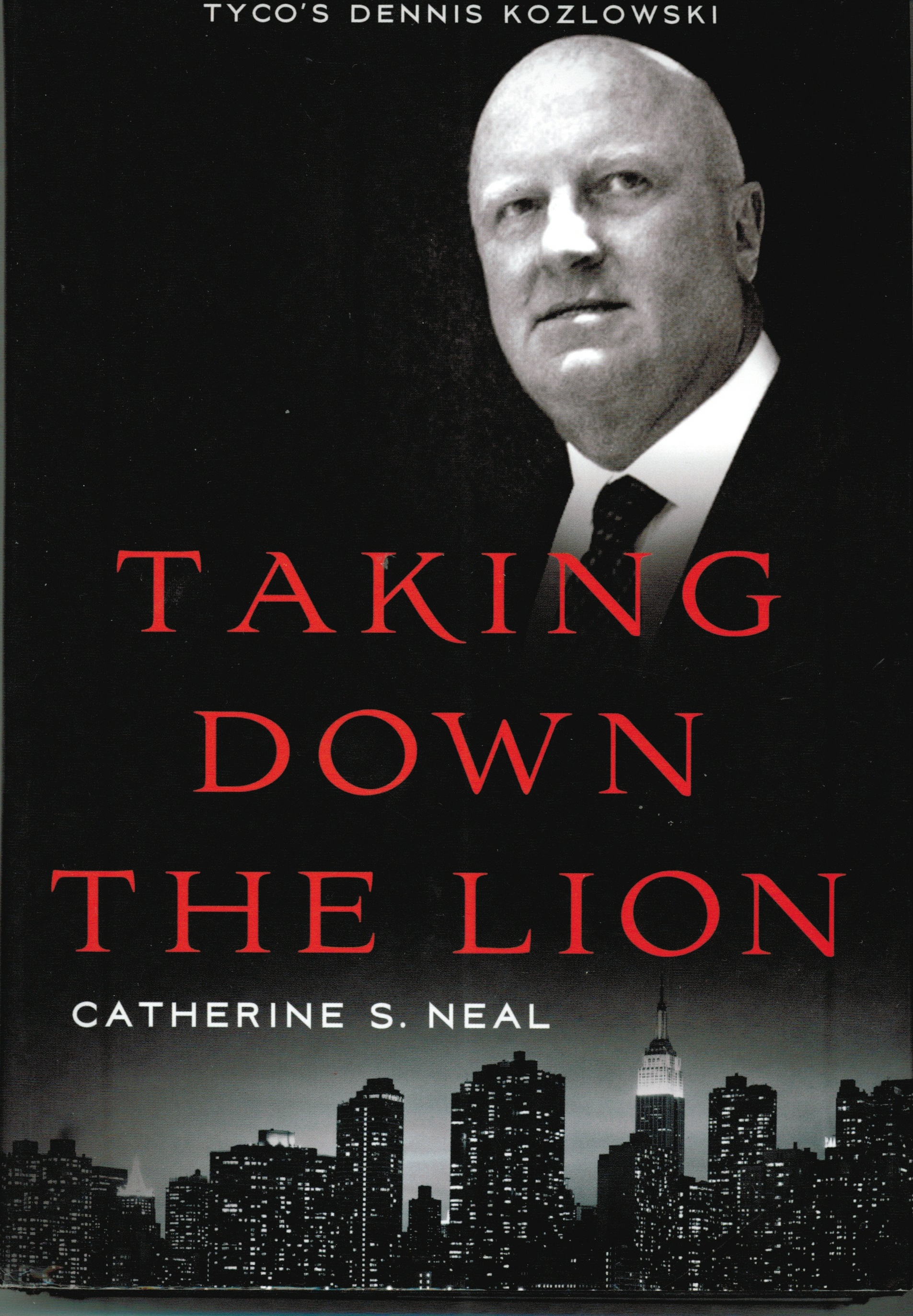

Book Review: Taking Down the Lion

This is a tough book for me to review. ?The credit distress of Tyco caused me considerable stress, and let me explain to you how that was.

This is a tough book for me to review. ?The credit distress of Tyco caused me considerable stress, and let me explain to you how that was.

I was the leading corporate bond manager at the fastest growing life insurance company 2001-2003. ?We had a significant position in Tyco bonds, and as thy fell, we were concerned. ?As a new corporate bond manager, I drew upon all of my analysts and portfolio managers, and asked them, “Who can give me the bear case here?” ?I did my own analysis as well. ?No one could come up with a way that Tyco could go broke.

So I asked the next question: Is there anyone on Wall who thinks Tyco could go broke? ?We found one. ?We read the analysis. ?We thought the argument was ridiculous, and so we wanted to buy more. ?We had a problem: our client was under pressure from the rating agencies to decrease our exposure to Tyco.

We had a large block of two-year Tyco bonds that were trading near par, and I sold them, and reinvested into a smaller market value of 30-year Tyco bonds. ?Problem solved, but we were now taking more risk in Tyco debt, a bet that we would win.

The Book

Taking Down the Lion takes the view that Kozlowski had a subpar legal team which made many blunders in representing him. ?It also notes how the informal management culture played against Kozlowski as things that were formal at many other corporations, and thus could not be argued, were not so at Tyco.

If the book is correct, this was a perfect storm for Kozlowski, leading to an unjust conviction and sentence. ?Having worked at firms that were informal, I can believe that Kozlowski was framed during a witch-hunt era that produced the dreadful Sarbox law. ?Few legislators think of what the side-effects will be from their legislation.

My Thoughts

Tyco as a corporation was not a fraud. ?Yes, Kozlowski was tone-deaf regarding some conspicuous consumption that he did, or was done on his behalf. ?There is no crime for being a vulgar consumer. ?Supposedly Kozlowski paid for it all, but still he got judged for it in court.

Truth, ?don’t know whether Kozlowski was guilty or not, but the company was well-run, and what company could you not find a few things that have some taint?

Summary

I think it is a good book, and I lean toward the idea that Kozlowski should not have been convicted, ?If you want to, you can buy it here:Taking Down the Lion: The Triumphant Rise and Tragic Fall of Tyco’s Dennis Kozlowski.

Full disclosure:?The PR flack asked me if I would like a copy, and I said yes.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

{kind=link}