I write about this every now and then, because human fertility is falling faster then most demographers expect. Using the CIA Factbook for data, the present total fertility rate for the world is 2.407 births per woman that survives childbearing. That is down from 2.425 in 2014, 2.467 in 2012, and 2.489 in 2010.? At this rate, the world will be at replacement rate (2.1), somewhere between 2035 and 2040. That?s a lot earlier than most expect, and it makes me suggest that global population will top out somewhat below 9?Billion in 2050, lower and earlier than most expect.

Have a look at the Total Fertility Rate by group in the graph above. The largest nations for each cell are listed below the graph. Note Asian nations to the left, and African nations to the right.

Africa is so small, that the high birth rates have little global impact. Also, AIDS consumes their population, as do wars, malnutrition, etc.

The Arab world is also slowing in population growth. When Saudi Arabia at?replacement rate (2.11), you can tell that the women are gaining the upper hand there, which is notable given the polygamy is permitted.

In the Developed world, who leads in fertility? Israel at 2.66. Next is France at 2.07 (Arabs), New Zealand at 2.03, Iceland at 2.01, Ireland at 1.98 (up considerably), UK at 1.89, Sweden at 1.88, and the US at 1.87, which is below replacement. The US?still grows from immigration, as does France.

Most of the above is a quick update of my prior pieces, which have some additional crunchy insights. ?When I look at the new data, I wonder if developed nations might not finally be waking up to the birth dearth. ?Take a look at this graph:

Now, the bottom left is a little crammed. ?What if I expand it?

I did the second graph in order to make the point that nations with fertility below 1.76 in 2010 tended to increase their fertility, while those above 1.76 tended to decrease it. ?Not that you should trust any statistical analysis, but if you could, this is statistically significant at a level well above 99%. ?(Note: this is an ordinary least squares regression. ?Every “nation” is weighted equally. ?If I get asked nicely, I could do a weighted least squares regression which gives heavy weight to China, India and the US, and less weight to Somalia, the West Bank, and Tonga. ?I don’t think the result would change much.)

I’m chuckling a little bit as I write this, because this is an interesting result, and one that I never thought I would be writing when I started this project. ?Interesting, huh? ?My guess is that there is a limit to how much you can get people to reduce family sizes before they begin to question the idea. ?Older parents may say, “What was that all about?” but children are usually fun and cute when they are little if they are reasonably disciplined.

One final note: I’ve been running into a lot of demographic articles of late, but this was the one that got me to write this:?The World’s Most Populous Country Is Turning Gray. ?The barbaric “One Child Policy” of China is having its impact; demography is often destiny. ?That said, over the last six years China’s total fertility rate has moved from 1.54 to 1.60.

As it says in the article:

Births in 2016 reached 17.86 million, the most since 2000, rising by 1.91 million from 2015, the National Health and Family Planning Commission said this month. That still falls short of the official projection. Last June, the ministry estimated there would be an increase of 4 million new births every year until 2020. China will continue to implement the two-child policy to promote a balanced population, the plan said.

Fertility doesn’t turn on a dime. ?When women conclude that the rewards of society (money, power, approval of peers) go to those with fewer children, that’s a tough cultural idea to overcome. ?I would conclude that it will take a lot longer than a single five-year plan to turn around birthrates in China… if they can be turned around at all. ?All across Asia, marriages happen at lesser rates, happen later, and produce fewer children. ?China is one of the more notable examples.

PS — Picky note: the two-child policy in China is only available to a husband and wife where at least one is an “only child.” ?It won’t create a balanced population near replacement rate, as everyone else must have only one child (with exceptions).

I was driving to a meeting of the Baltimore CFA Society, and listening to Bloomberg Radio, which was carrying President-Elect Trump’s Press Conference. I didn’t think too much about what I heard until Sheri Dillon talk about what was being done to eliminate conflicts of interest. Here is an excerpt:

Some have asked questions. Why not divest? Why not just sell everything? Form of blind trust. And I?d like to turn to addressing some of those questions now.

Selling, first and foremost, would not eliminate possibilities of conflicts of interest. In fact, it would exacerbate them. The Trump brand is key to the value of the Trump Organization?s assets. If President-elect Trump sold his brand, he would be entitled to royalties for the use of it, and this would result in the trust retaining an interest in the brand without the ability to assure that it does not exploit the office of the presidency.

[snip]

Some people have suggested that the Trump ? that President-elect Trump could bundle the assets and turn the Trump Organization into a public company. Anyone who has ever gone through this extraordinarily cumbersome and complicated process knows that it is a non-starter. It is not realistic and it would be inappropriate for the Trump Organization.

It went on from there, but I choked on the last paragraph that I quoted above. (Credit: New York Times, not all accounts carried the remarks of Ms. Dillon, a prominent attorney with the firm Morgan Lewis who structured the agreements for Trump) ?As I said before:

Trump to Outline Plans for ?Leaving My Great Business? Dec. 15 https://t.co/iIwweP2LcN Time to IPO and sell off the Trump Organization $$

An IPO of the Trump Organization was?realistic. ?I’m not saying it could have been done by the inauguration, but certainly by the end of 2017, and likely a lot earlier. ?I’ve seen insurance companies go through IPO processes that took a matter of months, a few because they had to sell the company to raise liquidity quickly for some reason.

In an IPO, Trump, all of Trump’s children and anyone else with an equity interest would have gotten their proportionate share of the new public company. ?Trump could have provided a lot of shares for the IPO, and instructed the trustee for his assets to sell it off?the remainder over the next year or so.

While difficult, this would not have been impossible or imprudent. ?Trump?might lose some value in the process, but hey, that should be part of the cost for a very wealthy man who becomes President of the US. ?There would be the countervailing advantage that all capital gains are eliminated, and who knows, that might settle his existing negotiations with the IRS.

Ending the counterfactual, though conflict of interest rules don’t apply to the President, Trump had?an opportunity to eliminate all conflicts of interest, and did not take it.

PS — Many major hotels are in the “name licensing” business — I also don’t buy the argument that Trump could not sell off the organization in entire, with no future payments for the rights of using the name. ?A bright businessman could create a new brand easily. ?It’s been done before.

I wrote about this last in October 2009 in a piece lovingly entitled:?At Last, Death!?(speaking of the holding company, not the insurance subsidiaries). ?I’m going to quote the whole piece here, because it says most of the things that I wanted to say when I heard the most recent news about Penn Treaty, where the underlying insurance subsidiaries are finally getting liquidated. ?It will be the largest health insurer insolvency ever, and second largest overall behind Executive Life.

Alas, but all good things in the human sphere come to an end.? Penn Treaty is the biggest insurer failure since 2004.? Now, don?t cry too much.? The state guaranty funds will pick up the slack.? The banks are jealous of an industry that has so few insolvencies.? Conservative state regulation works better than federal regulation.

Or does it?? In this case, no.? The state insurance regulator allowed a reinsurance treaty to give reserve credit where no risk was passed.? The GAAP auditor flagged the treaty and did not allow credit on a GAAP basis, because no risk was passed.? No risk passed? No additional surplus; instead it is a loan.? I do not get how the state regulators in Pennsylvania could have done this.? Yes, they want companies to survive, but it is better to take losses early, than let them develop and fester.

A prior employer asked me about this company as a long idea, because it was trading at a significant discount to book.? I told him, ?Gun to the head: I would short this.? Long-term care is not an underwritable contingency.? Those insured have more knowledge over their situation than the insurance company does.?? He did nothing.? He could not see shorting a company that was less than 50% of book value.

It was not as if I did not have some trust in the management team.? I knew the CEO and the Chief Actuary from my days at Provident Mutual.? Working against that was when I called each of them, they did not return my calls.? That made me more skeptical.? It is one thing not to return the call of a buyside analyst, but another thing not to return the call of one who was once a friend.

Aside from Penn Treaty, the only other company that I can think of as being at risk in the long term care arena is Genworth.? Be wary there.? What is worse is that they also underwrite mortgage insurance.? I can?t think of a worse combo: long term care and mortgage insurance.

The troubles at Penn Treaty are indicative of the future for those who fund long term care.? Be wary, because the troubles of the graying of the Baby Boomers will overwhelm those that try to provide long term care.? That includes government institutions.

Note that Genworth is down 60% since I wrote that, against a market that has less than tripled. ?If their acquirer doesn’t follow through, it too may go the way of Penn Treaty. ?(Give GE credit for kicking that “bad boy” out. ?They bring good things to “life.” 😉 )

Okay, enough snark. ?My main point this evening is that Pennsylvania should have had Penn Treaty stop writing new business by 2004 or so. ?As I wrote to a reporter at Crain’s back in 2008:

On your recent article on PennTreaty, one little known aspect of their treaty with Imagine Re is that it doesn’t pass risk.? Their GAAP auditors objected, but the State of Pennsylvania went along, which is the opposite of how it ordinarily works. ? Now Imagine Re takes advantage of the situation and doesn’t pay, knowing that PennTreaty is in a weak position and can’t fight back, partially because of the accounting shenanigans. ? It is my opinion that PennTreaty has been effectively insolvent for the past four years.? I don’t have any economic interest here, but I had to investigate it as an equity analyst one year ago.? Things are playing out as I predicted then.? What I don’t get is why Pennsylvania hasn’t taken them into conservation.

Another matter was that Imagine Re was an Irish reinsurer, and they have weak reserving rules. ?That also should have been a “red flag” to Pennsylvania. ?The deal with Imagine Re was struck in late 2005, leading to upgrades from AM Best that were reversed by mid-2006.

It was as if the state of Pennsylvania did not want to take the company over for some political reason. ?Lesser companies have been taken over over far less. ?Pennsylvania itself had worked out Fidelity Mutual a number of years earlier, so it’s not as if they had never done it before.

Had they acted sooner, the losses would never have been as large. ?I remember looking through the claim tables in the statutory books for Penn Treaty because the GAAP statements weren’t filed, and concluding that the firm was insolvent back in 2005 or so. ?Insurance regulators are supposed to be more conservative than equity analysts, because they don’t want companies to go broke, harming customers, and bringing stress to the industry through the guaranty funds.

The legal troubles post-2009 probably?had a small effect on the eventual outcome — raising premiums might have lowered the eventual shortfall of $2.6 billion a little. ?But raising premiums would make some healthy folks surrender, and those on benefit are not affected. ?It would likely not have much impact. ?Maybe some expenses could have been saved if the companies had been liquidated in 2009, 2012, or 2015 — still, that would not have been much either.

Some policyholders get soaked as well, as most state guaranty funds limit covered payments to $300,000. ?About 10% of all current Penn Treaty policyholders will lose some?benefits as a result.

Regulatory Policy Recommendations

Often regulators only care that premiums not be too high for the insurance, but this is a case where the company clearly undercharged, particularly on the pre-2003 policies. ?For contingencies that are long-lived, where payments could be made for a long time, regulators need to spend time looking at premium adequacy. ?This is especially important where the company is a monoline and in a line of business that is difficult to underwrite, like long-term care.

The regulators also need to review early claim experience in those situations (unusual business in a monoline), and even look at claim files to get some idea as to whether a company is likely to go insolvent if practices continue. ?A review like that might have shut off Penn Treaty’s ability to write business early, maybe prior to 2002. ?Qualitative indicators of underpricing show up in the types of claims that arrive early, and the regulators might have been able to reduce the size of this failure.

But wave goodbye to Penn Treaty, not that it will be missed except by policyholders that don’t get full payment.

Information received since the Federal Open Market Committee met in September indicates that the labor market has continued to strengthen and growth of economic activity has picked up from the modest pace seen in the first half of this year.

Information received since the Federal Open Market Committee met in November indicates that the labor market has continued to strengthen and that economic activity has been expanding at a moderate pace since mid-year.

FOMC shades GDP up.

Although the unemployment rate is little changed in recent months, job gains have been solid.

Job gains have been solid in recent months and the unemployment rate has declined.

Shades up their view on labor.

Household spending has been rising moderately but business fixed investment has remained soft.

Household spending has been rising moderately but business fixed investment has remained soft.

No change.

Inflation has increased somewhat since earlier this year but is still below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports.

Inflation has increased since earlier this year but is still below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports.

Shades their view of inflation up.

Market-based measures of inflation compensation have moved up but remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Market-based measures of inflation compensation have moved up considerably but still are low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy.

The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will strengthen somewhat further.

The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will strengthen somewhat further.

No change.

Inflation is expected to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further.

Inflation is expected to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further.

Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

No change.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1/2 to 3/4 percent.

Builds in the idea that they are reacting at least partially to expected future conditions in inflation and labor.

The Committee judges that the case for an increase in the federal funds rate has continued to strengthen but decided, for the time being, to wait for some further evidence of continued progress toward its objectives.

?

Sentence dropped.

The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a return to 2 percent inflation.

Shades down their view of how accommodative monetary policy is.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

No change.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

No change.? Gives the FOMC flexibility in decision-making, because they really don?t know what matters, and whether they can truly do anything with monetary policy.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal.

No change.

The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

No change.? Says that they will go slowly, and react to new data.? Big surprises, those.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

No change.? Says it will keep reinvesting maturing proceeds of agency debt and MBS, which blunts any tightening.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Esther L. George; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo.

Full agreement

Voting against the action were: Esther L. George and Loretta J. Mester, each of whom preferred at this meeting to raise the target range for the federal funds rate to 1/2 to 3/4 percent.

Prior dissenters are now happy, but was a 0.25% increase enough?? Or, as Steve Hanke has said, has monetary policy had to be loose to fight lower bank leverage?

Comments

The FOMC tightens 1/4%, but deludes itself that it is still accommodative.

The economy is growing well now, and in general, those who want to work can find work.

Maybe policy should be tighter. The key question to me is whether lower leverage at the banks was a reason for ultra-loose policy.

The change of the FOMC?s view is that inflation is higher. Equities and bonds fall. Commodity prices fall and the dollar strengthens.

The FOMC says that any future change to policy is contingent on almost everything.

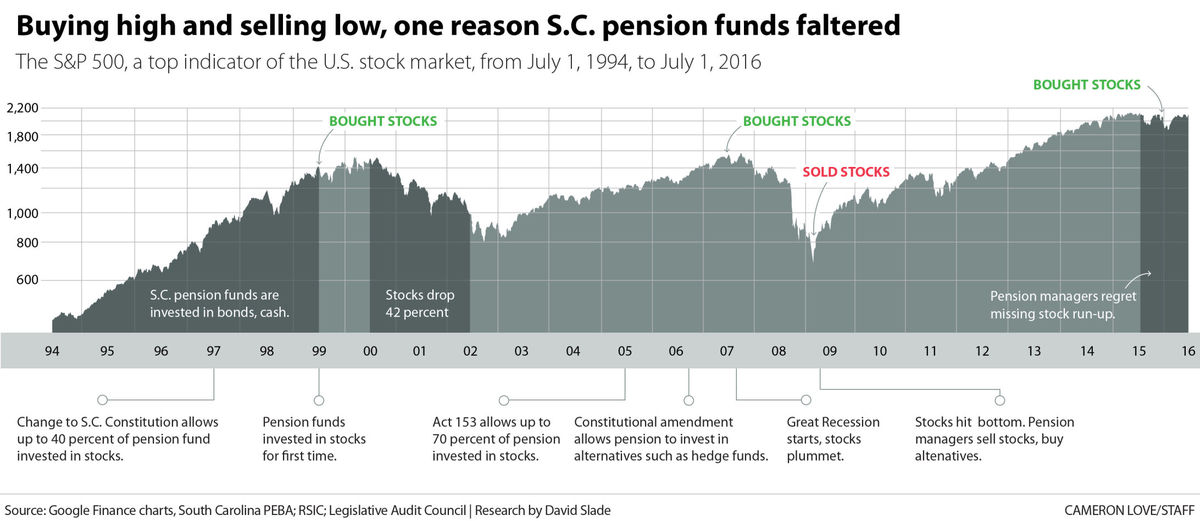

If you want a full view of what I am writing about today, look at this article from The Post and Courier, “South Carolina’s looming pension crisis.” ?I want to give you some perspective on this, so that you can understand better what went wrong, and what is likely to go wrong in the future.

Before I start, remember that the rich get richer, and the poor poorer even among states. ?Unlike what many will tell you though, it is not any conspiracy. ?It happens for very natural reasons that are endemic in human behavior. ?The so-called experts in this story are not truly experts, but sourcerer’s apprentices who know a few tricks, but don’t truly understand pensions and investing. ?And from what little I can tell from here, they still haven’t learned. ?I would fire them all, and replace all of the boards in question, and turn the politicians who are responsible out of office. ?Let the people of South Carolina figure out what they must do here — I’m a foreigner to them, but they might want to hear my opinion.

Let’s start here with:

Central Error 1: Chasing the Markets

Credit: The Courier and Post

Much as inexperienced individuals did, the South Carolina?Retirement System Investment Commission [SCRSIC] chased the markets in an effort to earn returns when they seemed easy to get in hindsight. ?As the article said:

It used to be different, before the high-octane investment strategies began. South Carolina?s pension plans were considered 99 percent funded in 1999, and on track to pay all promised benefits for decades to come.

That was the year the pension funds started investing in stocks, in hopes of pulling in even more income. A change to the state constitution and action by the General Assembly allowed those investments. In the previous five years, U.S. stock prices had nearly tripled.

Prior to that time, the pension funds were largely invested in bonds and cash, which actually yielded something back then. ?If the pension funds were invested in bonds that were long, the returns might not have been so bad versus stocks. ?But in the late ’90s the market went up aggressively, and the money looked easy, and it was easy, partly due to loose monetary policy, and a mania in technology and internet stocks.

Here’s the real problem. ?It’s okay to invest in only bonds. It’s okay to invest in bonds and stocks in a fixed proportion. ?It’s okay even to invest only in stocks. ?Whatever you do, keep the same policy over the long haul, and don’t adjust it. ?Also, the more nonguaranteed your investments become (anything but high quality bonds), the larger your provision against bear markets must become.

And, when you start a new policy, do what is not greedy. ?1999-2000 was the right time to buy long bonds and sell stocks, and I did that for a small trust that I managed at the time. ?It looked dumb on current performance, but if you look at investing as a business asking what level of surplus?cash flows the underlying investments will throw off, it was an easy choice, because bonds were offering a much higher future yield than stocks. ?But the natural tendency is to chase returns, because most people don’t think, they imitate. ?And that was true for the SCRSIC,?bigtime.

Central Error 2:?Bad Data

The above quote said that “South Carolina?s pension plans were considered 99 percent funded in 1999.” ?That was during an era when government accounting standards were weak. ?The?standards are still weak, but they are stronger than they were. ?South Carolina was NOT 99% funded in 1999 — I don’t know what the right answer would have been, but it would have been considerably lower, like 80% or so.

Central Error 3: Unintelligent Diversification into “Alternatives”

In 2009, I had the fun of writing a small report for CALPERS. ?One of my main points was that they allocated money to alternative investments too late. ?With all new classes of investments the best deals get done early, and as more money flows into the new class returns surge because the flood of buyers drives prices up. ?Pricing is relatively undifferentiated, because experience is early, and there have been few failures. ?After significant failures happen, differentiation occurs, and players realize that there are sponsors with genuine skill, and “also rans.” ?Those with genuine skill also limit the amount of money they manage, because they know that good-returning ideas are hard to come by.

The second aspect of this foolishness comes from the consultants who use historical statistics and put them into brain-dead mean-variance models which spit out an asset allocation. ?Good asset allocation work comes from analyzing what economic return the underlying business activities will throw off, and adjusting for risk qualitatively. ?Then allocate funds assuming they will never be able to trade something once bought. ?Maybe you will be able to?trade, but never assume there will be future liquidity.

The article kvetches about the expenses, which are bad, but the strategy is worse. ?The returns from all of the non-standard investments were poor, and so was their timing — why invest in something not geared much to stock returns when the market is at low valuations? ?This is the same as the timing problem in point one.

Alternatives might make sense at market peaks, or providing liquidity in distressed situations, but for the most part they are as saturated now as public market investments, but with more expenses and less liquidity.

Central Error 4: Caring about 7.5% rather than doing your best

Part of the justification for buying the alternatives rather than stocks and bonds is that you have more of a chance of beating the target return of the plan, which in this case was 7.5%/yr. ?Far better to go for the best risk-adjusted return, and tell the State of South Carolina to pony up to meet the promises that their forbears made. ?That brings us to:

Central Error 5: Foolish politicians who would not allocate more money to pensions, and who gave?pension increases rather than wage hikes

The biggest error belongs to the politicians and bureaucrats who voted for and negotiated higher pension promises instead of higher wages. ?The cowards wanted to hand over an economic benefit without raising taxes, because the rise in pension benefits does not have any immediate cash outlay if one can bend the will of the actuary to assume that there will be even higher investment earnings in the future to make up the additional benefits.

[Which brings me to a related pet peeve. ?The original framers of the pension accounting rules assumed that everyone would be angels, and so they left a lot of flexibility in the accounting rules to encourage the creation of defined benefit plans, expecting that men of good will would go out of their way to fund them fully and soon.

The last 30 years have taught us that plan sponsors are nothing like angels, playing for their own advantage, with the IRS doing its bit to keep corporate plans from being fully funded so that taxes will be higher. ?It would have been far better to not let defined benefit plans assume any rate of return greater than the rate on Treasuries that would mimic their liability profile, and require immediate relatively quick funding of deficits. ?Then if plans outperform Treasuries, they can reduce their contributions by that much.]

Error 5 is likely the biggest error, and will lead to most of the tax increases of the future in many states and municipalities.

Central Error 6: Insufficient Investment Expertise

Those in charge of making the investment decisions proved themselves to be as bad as amateurs, and worse. ?As one of my brighter friends at RealMoney, Howard Simons, used to say (something like), “On Wall Street, to those that are expert, we give them super-advanced tools that they can use to destroy themselves.” ? The trustees of?SCRSIC received those tools and allowed themselves to be swayed by those who said these magic strategies will work, possibly without doing any analysis to challenge the strategies that would enrich many third parties. ?Always distrust those receiving commissions.

Central Error 7: Intergenerational Equity of Employee Contributions

The last problem is that the wrong people will bear the brunt of the problems created. ?Those that received the benefit of services from those expecting pensions will not be the prime taxpayers to pay those pensions. ?Rather, it will be their children paying for the sins of the parents who voted foolish people into office who voted for the good of current taxpayers, and against the good of future taxpayers. ?Thank you, Silent Generation and Baby Boomers, you really sank things for Generation X, the Millennials, and those who will follow.

Conclusion

Could this have been done worse? ?Well, there is Illinois and Kentucky. ?Puerto Rico also. ?Many cities are in similar straits — Chicago, Detroit, Dallas, and more.

Take note of the situation in your state and city, and if the problem is big enough, you might consider moving sooner rather than later. ?Those that move soonest will do best selling at?higher real estate prices, and not suffer the soaring taxes and likely?diminution of city services. ?Don’t kid yourself by thinking that everyone will stay there, that there will be a bailout, etc. ?Maybe clever ways will be found to default on pensions (often constitutionally guaranteed, but politicians don’t always honor Constitutions) and municipal obligations.

Forewarned is forearmed. ?South Carolina is a harbinger of future problems, in their case made worse by opportunists who sold the idea of high-yielding investments to trustees that proved to be a bunch of rubes. ?But the high returns were only needed because of the overly high promises made to state employees, and the unwillingness to levy taxes sufficient to fund them.

[bctt tweet=”Seven central errors committed by the South Carolina Retirement System and politicians” username=”alephblog”]

Should a credit?analyst care about financial?leverage? ?Of course, the amount and types of financial claims against a firm are material to the ability of a firm to avoid defaulting on its debts. ?What about operating leverage? ?Should the credit?analyst care? ?Of course, if a firm has high fixed costs and low variable costs (high operating leverage), its financial position is less stable than that of a company that has low fixed costs and high variable costs. ?Changes in demand don’t affect a firm as much if they have low operating leverage.

That might be fine for industrials and utilities, but what about financials? ?Aren’t financials different? ?Yes, financials are different as far as operating leverage goes because for financial companies, operating leverage is the degree of credit risk that financials take on in their assets. Different types of lending have different propensities for loss, both in terms of likelihood and severity, which are usually correlated.

A simple example would be two groups of corporate bonds — ?one can argue over new classes of bond?ratings, but on average, lower rated corporate bonds default more frequently than higher rated bonds, and when they default, the losses are typically greater on the lower rated bonds.

As such the amount of operating risk, that is, unlevered credit risk, is material to the riskiness of financial companies.

Credit analysis gets done on financial companies by many parties: the rating agencies, private credit analysts, and implicitly by financial regulators. ?They all do the same sorts of analyses using similar underlying theory, though the details vary.

Regulators typically codify their analyses through what they call risk-based capital. ?Given all of the risks a financial institution takes — credit, asset-liability mismatch, and other liability risks, how much capital does a financial institution need in order to stay solvent? ?Along with this usually also comes cash flow testing to make sure that?the financial companies can withstand runs on their capital structure.

When done in a rigorous way, this lowers the probability and severity of financial failures, including the remote possibility that taxpayers could be tagged in a crisis to cover losses. ?In the life insurance industry, actuaries have worked together with regulators to put together a fair system that is hard to game, and as such, few life and P&C insurance companies went under during the financial crisis. ?(Note: AIG went under due to its derivative subsidiary and that they messed with securities lending agreements. ?The only failures in life and P&C insurance were small.)

Banks have risk-based capital standards, but they are less well-designed than those of the US insurance industry, and for the big banks they are more flexible than those for insurers. ?If I were regulating banks, I would get a small army of actuaries to study bank solvency, and craft regulations together with a single banking regulator that covers all depositary financials (or, state regulators like in insurance which would be better) using methods similar to those for the insurance industry. ?Then every five years or so, adjust the regulations because as they get used, problems appear. ?After a while, the methods would work well. ?Oh, I left one thing out — all banks would have a valuation actuary reporting to the board and the regulators who would do the cash flow testing and the risk-based capital calculations. ?Their positions would be funded with a very small portion of money that currently goes to the FDIC.

This would be a very good system for avoiding excessive financial risk. ?Dreaming aside, I write this this evening because there are other dreamers proposing a radically simple system for regulating banks which would allow them to write business with no constraint at all with respect to credit risk. ?All banks would face a simple 10% leverage ratio regardless of how risky their loan books are. ?This would in the short run constrain the big banks because they would need to raise capital levels, though after that happened, they would probably write riskier loans to get their return on equity back to where it was.

My main point here is that you don’t want to incent banks to write a lot of risky loans. ?It would be better for banks to put aside the right amount of capital versus varying classes of risk, and size the amount of capital such that it is not prohibitive to the banking system.

As such, a simple leverage ratio will not cut it. ?Thinking people and their politicians should reject the current proposal being put out by the Republicans and instead embrace a more successful regulatory system manned by intelligent and reasonably risk-averse actuaries.

If you knew me when I was young, you might not have liked me much. ?I was the know-it-all who talked a lot in the classroom, but was quieter outside of it. ?I loved learning. ?I mostly liked my teachers. ?I liked and I didn’t like my fellow students. ?If the option of being home schooled had been offered to me, I would have jumped at it in an instant, because then I could learn with no one slowing me down, and no kids picking on me.

I read a lot. A LOT. ?Even when young I spent my time on the adult side of the library. ?The librarians typically liked me, and helped me find stuff.

I became curious about investing for two reasons. 1) my mother did it, and it was difficult not to bump into it. ?She would watch Wall Street Week, and often, I would watch it with her. ?2) Relatives gave me gifts of stock, and my Mom taught me where to look up the price in the newspaper.

Now, if you knew the stocks that they gave me, you would wonder at how I still retained interest. ?The two were the conglomerate Litton Industries, and the home electronics company?Magnavox. ?Magnavox was bought out by Philips in 1974 for a price that was 25% of the original cost basis of my shares. ?We did worse on Litton. ?Bought in the mid-to-late ’60s and sold in the mid-’70s for a 80%+ loss. ?Don’t blame my mother for any of this, though. ?She rarely bought highfliers, and told me that she would have picked different stocks. ?Gifts are gifts, and I didn’t need the money as a kid, so it didn’t bother me much.

At the library, sometimes I would look through some of the research volumes that were there for stocks. ?There are a few things that stuck with me from that era.

1) All bonds traded at discounts. ?It’s not that I understood it well, but I remember looking at bond guides, and noted that none of the bonds traded over $100 — and not surprisingly, they all had low coupons.

In those days, some people owned individual bonds for income. ?I remember my Grandma on my mother’s side talking about how little one of her bonds paid in interest, given that inflation was perking up in the 1970s. ?Though I didn’t hear it in that era, bonds were sometimes called “certificates of confiscation” by professionals ?in the mid-to-late ’70s. ?My Grandpa on my father’s side thought he was clever investing in short-term CDs, but he never changed on that, and forever missed the rally in stocks and long bonds that kicked off in 1982.

When I became a professional bond investor at the ripe old age of 38 in 1998, it was the opposite — almost all bonds traded at premiums, and had relatively high coupons. ?Now, at that time I knew a few firms that were choking because they had a rule that said you can never buy premium bonds, because in a bankruptcy, the premium will be automatically lost. ?Any recoveries will be off the par value of the bond, which is usually $100.

2) Many stocks paid dividends that were higher than their earnings. ?I first noticed that while reading through Value Line, and wondered how that could be maintained. ?The phrase “borrowing the dividend” was bandied about.

Today as a professional I know that we should look at free cash flow as a limit for dividends (and today, buybacks, which were unusual to unheard of when I was a boy), but earnings still aren’t a bad initial proxy for dividend viability. ?Even if you don’t have a cash flow statement nearby, if debt is expanding and earnings don’t cover the dividend, I would be concerned enough to analyze the situation.

3) A lot of people were down on stocks and bonds — there was a kind of malaise, and it did not just emanate from Jimmy Carter’s mind. [Cue the sad Country Music] Some concluded that inflation hedges like homes, short CDs, and gold/silver were the only way to go. ?I remember meeting some goldbugs in 1982 just as the market was starting to take off, and they disdained the idea of stocks, saying that history was their proof.

The “Death of Equities” came and went, but that reminds me of one more thing:

4) There was a decent amount of pessimism about defined benefit plan pension funding levels and life insurer solvency. ?Inflation and high interest rates made life insurers look shaky if you marked the assets alone to market (the idea of marking liabilities to market was at least 10 years off in concept, and still hasn’t really arrived, though cash flow testing accomplishes most of the same things). ?Low stock and bond prices made pension plans look shaky. ?A few insurance companies experimented with buying gold and other commodities, just in time for the grand shift that started in 1982.

Takeaways

The biggest takeaway is to remember that as a fish you don’t notice the water that you swim in. ?We are so absorbed in the zeitgeist (Spirit of the Times)?that we usually miss that other eras are different. ?We miss the possibility of turning points. ?We miss the possibility of things that we would have not thought possible, like negative interest rates.

In the mid-2000s, few thought about the possibility of debt deflation having a serious impact on the US economy. ?Many still feared the return of inflation, though the peacetime inflation of the late ’60s through mid-’80s was historically unusual.

The Soviet Union will bury us.

Japan will bury us. ?(I’m listening to some Japanese rock as I write this.) 😉

China will bury us.

Few people can see past the zeitgeist. ?Many can’t remember the past.

Should we?be concerned about companies not being able pay their dividends and fulfill their buybacks? ?Yes, it’s worth analyzing.

Should we be concerned about defined benefit plan funding levels? Yes, even if interest rates rise, and percentage deficits narrow. ?Stocks will likely fall with bonds if real interest rates rise. ?And, interest rates may not rise much soon. ?Are you ready for both possibilities?

Average people don’t seem that excited about any asset class today. ?The stock market is at new highs, and there isn’t really a mania feel now. ?That said, the ’60s had their highfliers, and the P/Es eventually collapsed amid inflation and higher real interest rates. ?Those that held onto the Nifty Fifty may not have lost money, but few had the courage. ?Will there be a correction for the highfliers of this era, or, is it different this time?

It’s never different.

It’s always different.

Separating the transitory from the permanent is tough. ?I would be lying to you if I said I could do it consistently or easily, but I spend time thinking about it. ?As Buffett has said, (something like)?”We’re paid to think about things that can’t happen.”

Ending Thoughts

Now, lest the above seem airy-fairy, here are my biases at present as I try to separate the transitory from the permanent:

The US is in better shape than most of the rest of the world, but its securities are relatively priced for that reality.

Before the US has problems, Japan, China, OPEC, and the EU will have problems, in about that order. ?Sovereign default used to be a large problem. ?It is a problem that is returning. ?As I have said before — this era reminds me of the 1840s — huge debts and deficits, with continued currency debasement. ?Hopefully we don’t get a lot of wars as they did in that decade.

I am treating long duration bonds as a place to speculate — I’m dubious as to how much Trump can truly change things. ?I’m flat there now. ?I think you almost have to be a trend follower there.

The yield curve will probably flatten quickly if the Fed tightens more than once more.

The internet and global demographics are both forces for deflationary pressure. ?That said, virtually the whole world has overpromised to their older populations. ?How that gets solved without inflation or defaults is a tough problem.

Stocks are somewhat overvalued, but the attitude isn’t frothy.

DIvidend stocks are kind of a cult right now, and will suffer some significant setback, particularly if interest rates rise.

Eventually emerging markets and their stocks will dominate over developed markets.

Value investing will do relatively better than growth investing for a while.

That’s all for now. ?You may conclude very differently than I have, but I would encourage you to try to think about the hard problems of our world today in a systematic way. ?The past teaches us some things, but not enough, which should tell all of us to do risk control first, because you don’t know the future, and neither do I. 🙂

I’ve thought about this problem before, but always thought it was more of a curiosity until I read this on page 66 of Jeff Gramm’s very good book, Dear Chairman: Boardroom Battles and the Rise of Shareholder Activism. ?(Note: anyone entering through this link and buying something at Amazon, I get a small commission.)

I saw Eddie Lampert, a hedge fund manager who is chairman of Sears Holdings, make some interesting points at a New York Public Library event in 2006. When he was discussing the challenges of managing a public company, he raised a question few people in the room had considered. How do you run a company well when the stock is overvalued? What happens when management can’t meet investors’ unrealistic expectations without taking more risk? And what happens to employee morale if everyone does a good job but the stock declines? Lampert, of course, knew what he was talking about. Sears closed that day at $175 per share versus today’s price of around $35. In an efficient market, it’s easy to develop tidy theories about optimal corporate governance. Once you realize stock prices can be totally crazy, the dogma needs to go out the window.

The price of Sears Holding is around $13 now, though there have been a lot of spinoffs. ?Could Eddie have done better for shareholders? ?Before answering that, let’s take a simpler example: what should a the managers/board of a closed end fund do if it persistently trades at a large premium to its net asset value [NAV]? ?I can think of three ideas:

1) Conclude that the best course of action is to?minimize the eventual price crash that will happen. ?Therefore issue stock as near the current price level as possible, and use it to buy non-inflated assets, bringing down the discount. ?What’s that, you say? ?The act of announcing a stock offering will crater the price? ?Okay, good point, which brings us to:

2) Merge with another closed end fund, trading at a discount, but offering them a premium to their NAV, hopefully a closed end fund?related to the type of closed end fund that you are. ?What’s that, you say? ?Those that manage other closed end funds are financial experts, and would never agree to that? ?Uhh, maybe. ?Let me say that not all financial experts are equal, and who knows what you might be able to do. ?Also, they do have a duty to their investors to maximize value, and for those that?sell above net asset value this is a big win. ?In the meantime, you have reduced your effective economic discount for those that continue to hold your fund.

3) Issue bonds or preferred stock convertible into common stock at a level that virtually guarantees conversion. ?Use the proceeds to invest in your ordinary investment strategy, bringing down the effective discount as dilution slowly takes place.

Of all the ideas, I think 3 might work best, because it would have the best chance of allowing you to issue equity near the overvalued level. ?If the overvaluation was 50%, maybe you could get it down to 25% by doubling the asset base, in which case you did your holders a big favor. ?If it works, maybe repeat it in two years if the premium persists.

A closed end fund is simple compared to a company — but that added complexity may allow strategies one or two to work better. ?Before we go there, let’s take one more detour — PENNY STOCKS!

Okay, I haven’t written about those in a while, but what do penny stock managements with no revenues do to keep their firm alive? ?They trade stock at discount levels in order to source goods and services. ?This creates dilution, but they don’t care, they are waiting for the day when they can exit, possibly after a promotion. ?Also, they could issue their stock to buy up a small firm,?adding some value behind the worthless shares. ?One guy wrote me after my penny stock articles, telling me of how he foolishly did that, with the stock being restricted, and he watched in horror as the ?price sank 60% before he was allowed to sell any shares. ?He lost most of what he worked for in life, took the company to court, and I suspect that he lost… it was his responsibility to do “due diligence.”

So with that, strategy one can be to issue as much stock as possible as quietly as possible. ?Offer your employees stock in order to reduce wages. ?Give them options. ?Where possible, pay for real assets and services with stock. ?Issue stock, saying that you have big plans for organic growth, then, try to grow the company. ?In this case, strategy three can make more sense, as the set of buyers taking the convertible stock and bonds don’t see the dilution. ?That said, the hard critical element is the organic growth strategy — what great thing can you do? ?Maybe this strategy would apply to a cash hungry firm like Tesla.

In strategy two, merge with other companies either to achieve diversification or vertical integration. ?Issue stock at a premium to the value received, but not not as great as the premium underlying your current stock price. ?Ordinarily, I would argue against dilutive acquisitions, but this is a special case where you are trying to reduce the premium valuation without reducing the share price.

This brings us to another set of examples: conglomerates and roll-ups. ?Think of the go-go years in the ’60s where conglomerates bought up low P/E stocks using?their high P/E stocks as currency. ?Initially, the process produces earnings growth. ?It works until the eventual bloat of the businesses is difficult to manage, and?the P/Es fall. ?Final acquisitions are sometimes ugly, leading to failure. ?The law of decreasing returns to scale eventually catches up.

With roll-ups an aggressive management team buys up peers. ?The acquirer is a faster growing company, and so its stock trades at a premium. ?If the acquirer is clever, it can shed costs in the target, and continue to show earnings growth for some time until it finally slows down and has to rationalize the mess of peer companies that have been bought.

This brings up one more area for overvalued companies: frauds. ?This past evening, my wife and I watched The Billion Dollar Bubble, which was the largest financial fraud up until Madoff. ?One thing Equity Funding?did was use the funds that they had generated to buy other insurers. (That’s not in the movie, which kept things simple, and compressed the time it took for the fraud to take place.)

Enron is another example of a fraudulent company that used its inflated share price to buy up other companies. ?Not everything Enron did was fraudulent, but having a highly valued stock allowed it to buy up companies with assets which reduced some of its valuation premium, though not enough for the stock to go out at a positive figure.

Summary

It is an unusual situation, but the best strategy for a company with an overvalued stock is to try to grow their way out of it, usually through mergers and acquisitions. ? The twist I offer you at the end of my piece is this: thus, watch highly acquisitive firms. Not all of them are overvalued or fraudulent, but some will be. Avoid the shares of those firms.

[bctt tweet=”watch highly acquisitive firms. Not all of them are overvalued or fraudulent, but some will be. Avoid the shares of those firms.” username=”alephblog”]

Well, I’m back in suburban Baltimore after the struggle of getting to the the center of DC and back. ?It takes a lot of energy to write 4000 or so words, tweet 26 times, meet new people, old friends, etc. ?Here are some thoughts after the sip from the firehose:

1) There was almost no media there this time. ?Maybe it’s all the action associated with a new president being elected. ?All the same, I see almost nothing on the web right now aside from the Twitter hashtag #CatoMC16?and my posts echoed at ValueWalk.

2) I came out of the conference thinking that I need to read three of the papers, the ones by:

Hanke & Sekerke — color me dull, but it finally dawned on me the potential degree to which structural regulatory change has been fighting ZIRP.

Jordan — his idea on how to sop up excess liquidity sounds interesting.

Goodspeed — I am a sucker for economic history — it broadens the categories that you think in. ?His presentation was very data-oriented, and I thought the methodology was clever for analyzing alternative deposit guarantee methods back in a time when the states regulated the banks. ?(Please bring back state regulation of banks; it works better. ?Many more failures, but they are all small.)

3) Jim Grant is always educational to listen to. ?I also appreciated O’Driscoll, Thornton, Orphanides, and Hoenig.

4) I would not invite back Spitznagel (irrelevant), Allison, Todd, and Gramm (three living in fantasyland).

5) That brings me to the fantasies of the conference as I see them. ?This is what I think is true:

The Community Reinvestment Act [CRA] was not a big factor in the crisis, aside from the GSEs. ?Intelligent banks make decent CRA loans; I’ve seen it done.

Subprime lending was the leading edge of of bad lending on residential real estate, but regulators did not do their jobs well in supervising lending.

Tangible bank leverage was way too high, and was a large part of the crisis. ?So was a lack of liquidity from losing the wholesale funding markets, which disproportionately hit the big banks.

The big banks were disproportionately insolvent, though a few of them did not need more capital, like US Bancorp BB&T, and Wells Fargo. ?Many more small banks were insolvent also, but they weren’t big enough to move the systemic risk needle.

Banks are?a little over-regulated, but given the poor ways that they managed liquidity prior to the crisis, you can’t blame Dodd-Frank for trying to avoid that problem again.

The big bank stress tests are not real in the US or Europe; they exist to mollify politicians and bamboozle the public. ?If they ARE real, then publish the data, methods and results in detail.

Banks?need a strong risk based capital formula. ?The one for insurers works very well. ?Perhaps banks should imitate the stronger and smarter solvency regulations that insurers use. ?They might even find them looser than what they currently do, but be more accurate as to real risks.

Inverting the yield curve is?necessary in a fiat money system. ?You need to deflate and liquidate bad lending so that new lending in the next part of the credit cycle can recycle the capital to better projects.

6) That brings me to the realities of the conference as I see them. ?This is what I think is true:

Fannie/Freddie were a large part of the crisis. ?Undercapitalized relative to the amount of default risk they were taking.

Housing prices were pushed too high as a result of too much debt getting applied to finance them. ?Loose monetary policy aided the creation of this debt. ?Falling housing prices were the main cause of the crisis, as many loans became inverted, and a slowing economy led to many losing their ability to pay their mortgages.

We needed a different bailout where bank stockholders lost all, and debtholders lose also, only after that should the FDIC have been tapped to protect depositors.

Bank solvency is important for the long run for the economy. ?A crisis like the last one erases a lot of the growth that would occur from looser bank regulatory policy. ?Things may be tight now, but once the system adjusts, growth should resume.

A?healthier economy has lower debt and less debt leverage/complexity. ?Debt and layered debts make an economy inherently fragile.

A gold standard does not increase instability, unless banks are mis-regulated for solvency.

The wealth effect is tiny, and the Fed should stop pretending that it does much.

7) While at Cato, I noticed the area named for?Rose Wilder Lane, the same Rose in the “Little House on the Prairie” books (daughter of Laura and Almonzo Wilder). ?She was a libertarian later in life, and knew Ayn Rand. ?Their pictures are near each other in Cato’s basement. ?Just a little trivia.

8 ) There was a lot of sympathy for the idea of not paying interest on excess reserves, and certainly not same rate as on required reserves.

PANEL 4: RETHINKING THE MONETARY TRANSMISSION MECHANISM

Moderator: George Selgin?-?Director, Center for Monetary and Financial Alternatives, Cato Institute

Jerry L. Jordan -?Former President, Federal Reserve Bank of Cleveland

Steve Hanke -?Professor of Applied Economics, Johns Hopkins University

Walker F. Todd -?Trustee, American Institute for Economic Research

Selgin introduces the topic arguing how difficult it is to analyze things today

Jordan (get his paper)

Rules vs discretion — what are useful targets or indicators?

Buying/selling Treasuries; Fed funds targeting

Large balance sheets — no need for excess reserves. ?Large foreign banks buy deposits of FHLBs — positive fed funds rate.

Borrowing from the banking system — IOR, reverse repos.

Monetary base — currency plus reserves. ?Was close to accurate at the beginning, but not so now. ?When rates go up, it is a form of fiscal stimulus.

Monetary base has grown

Basel III massive cause for reserves. ?Foreign banks have been reducing activity in the US.

Hanke?Wrong things expected: hyperinflation, GDP growth, net private investment would soar, etc.

Money matters, and it dominates over fiscal policy

Money is a superior measure to interest rates

Divisia measures are superior — opportunity cost of converting a monetary asset into cash.

Center for Financial Stability takes care of Divisia measures.

Three measures: State money, Bank money and Nonbank private money.

State — M1 Currency, M4 T-bills

Nonbank private money — M2 Retail money funds, M3 Overnight & term repos, Institutional money funds, M4 commercial paper

Bank money — M1 Traveler’s Checks, M2 Non-interest bearing deposits. Savings Deposits, MM Dep accts, Small time deposits, M3 Large time deposits

Bank regulation has led to tight money, amid loose monetary policy w/QE.

Notes Kashkari’s recent proposal ?– would kill private money

Todd — have standard models failed?

Graph of Fed’s balance sheet — Assets, then shows money velocity/multiplier.

Government spending is up. ?QE not working, yet being adopted elsewhere. ?Suggests Jerry Jordan’s solution may work.

Swiss National Bank asked why the Fed is paying interest on excess reserves? ?Who knows?

With no velocity and no money multiplier how does monetary policy affect?GDP.

Central bank liquidity swaps are negligible now, though it was high as high as ~$600B. ?Should be limits on the Fed’s ability to enter into liquidity swaps.

Fed credited $558 Billion to US Treasury for a “security” at some point in the crisis. (??)

Suggests segmenting the Fed’s lending operations. ?Should be able to review any entity that would receive emergency funds.

Q1 Venezuelan guy — Can we trust the helicopter pilots? ?How to loosen bank regulations?

Hanke: Regulation important when it changes a lot. ?Not usually considered at monetary policy, but it is. ?Private money has shrunk since the crisis. ?Ultratight regulation plus loose policy — means relatively tight policy. ?Forget Basel IV and roll back Basel III.

Q2 Student at Southern Methodist University: When have central banks done it right?

Hanke: China has been an outlier by ignoring Basel — may have other effects later.

Jordan:?New Zealand often viewed as a successful Central Bank. ?Maybe Australia, Switzerland…

Q3 Joseph Marshall — How can things work well if we discourage savings?

Jordan: Savings glut = Investment glut (ex post). ?Lower rates often drive savers to save more to get to a target. ?Half-plus of US currency is held outside of the US. ?Investment spending 10-11% of GDP. ?Bailouts further consumption in bubble areas.

Q4 Gerry O’Driscoll — Todd: Blip in Treasury account balance may be drawdown in reserves. ?Promise to keep balance sheet constant until an exit is desired.

Jordan: Debt ceiling — large cash balance going into a debt ceiling period could be it.

Closing

Expresses gratitude to the speakers and Jim Dorn. ?Incident of some Russians printing their own currency. ?Top down central planning does not work, and threatens our liberties.

{kind=link}