One of my clients asked me what I think is a hard question: When should I deploy capital? ?I?ll try to answer that here.

There are three?main things to consider in using cash to buy or sell assets:

What is your time horizon? ?When will you likely need the money for spending purposes?

How promising is the asset in question? ?What do you think it might return vs alternatives, including holding cash?

How safe is the asset in question? ?Will it survive to the end of your time horizon under almost all circumstances and at least preserve value while you wait?

Other questions like ?Should I dollar cost average, or invest the lump?? are lesser questions, because what will make the most difference in ultimate returns comes from ?the above three questions. ?Putting it another way, the?results of dollar cost averaging depend on returns after you put in the last dollar of the lump, as does investing the lump sum all at once.

Thinking about price momentum and mean-reversion are also lesser matters, because if your time horizon is a long one, the initial results will have a modest effect on the ultimate results.

Now, if you care about price momentum, you may as well ignore the rest of the piece, and start trading in and out with the waves of the market, assuming you can do it. ?If you care about mean reversion, you can wait in cash until we get ?the mother of all selloffs? and then invest. ?That has its problems as well: what?s a big enough selloff? ?There are a lot of bears waiting for rock bottom valuations, but the promised bargain valuations don?t materialize because others invest at higher prices than you would, and the prices?never get as low as you would like. ?Ask?John Hussman.

Investing has to be done on a ?good enough? basis. ?The optimal return in hindsight is never achieved. ?Thus, at least for value investors like me, we focus on what we can figure out:

How long can I set aside this capital?

Is this a promising investment at a relatively attractive price?

Do I have a margin of safety buying this?

Those are the same questions as the first three, just phrased differently.

Now, I?m not saying that there is never a time to sit on cash, but decisions like that are typically limited to times where valuations are utterly nuts, like 1964-5, 1968, 1972, 1999-2000 ? basically parts of the go-go years and the dot-com bubble. ?Those situations don?t last more than a decade, and are typically much shorter.

Beyond that, if you have the capital to spare, and the opportunity is safe and cheap, then deploy the capital. ?You?ll never get it perfect. ?The price may fall after you buy. ?Those are the breaks. ?If that really bothers you, then maybe?do half?of what you would ultimately do, but set a time limit for investment of the other half. ?Remember, the opposite can happen, and the price could run away from you.

A better idea might show up later. ?If there is enough liquidity,?trade into the new idea.

Since perfection is not achievable, if you have something good enough, I recommend that you execute and deploy the capital. ?Over the long haul, given relative peace, the advantage belongs to the one who is invested.

If you still wonder about this question you can read the following two articles:

The following may be controversial. It also may be dull to the point that you might not care. Here’s why you should care: quarterly reporting is a useful and productive use of corporate resources, and it would be a shame to lose it because some people with a patina of intelligence think it is harmful. Who knows? Losing it might even make you poorer.

Influential law firm Wachtell, Lipton, Rosen & Katz has an idea that may be music to the ears of its big corporate clients and a nightmare for some investors and analysts: end quarterly earnings reports.

Wachtell on Tuesday called on the Securities and Exchange Commission to consider allowing U.S. companies to do away with the obligatory updates, one of the most important rituals on Wall Street and in corporate America, suggesting that they distract executives from long-term goals.

The basic case is that quarterly earnings lead companies to behave in a short-term manner, and underinvest for longer-term growth, thus hurting the US economy. ?I disagree. There are at least four?things that are false in the arguments made in the article, and in books like?Saving Capitalism from Short-Termism:

Quarterly earnings don’t produce value in and of themselves

Quarterly earnings cause most corporations to ignore the long-term.

Ending quarterly earnings will end activism, buybacks, and dividends.

Buybacks and dividends are bad uses of capital, and more capital investment, especially for long-dated projects, is necessarily a good thing.

Most of the value of a Corporation on a going concern basis stems from the future earnings of the company.? Investors want to have an estimate of forward earnings so that they can gauge whether the company is growing at an appropriate rate.

Now, it wouldn?t matter if the system were set up by third-party sell side analysts, by buyside analysts, by companies themselves, or by a combination thereof.? The thing is investors are forward-looking, and they want a forward-looking estimate to allow them to estimate whether the companies are doing well with their current earnings or not.

Don’t think of the quarterly earnings in isolation. ?A good or bad quarterly earnings number conveys information not about the current period only, but about all future periods. ?A bad earnings number?lowers the estimates of all future earnings, telling market players that the long-term efforts of the company are not going to be so great. ?Vice-versa for a good number.

Now, in some cases, that might not be true, and the management team will say, “But we still expect our future earnings to reach the levels that we expected before this quarter.” ?That still leaves the problem of getting to the high future earnings, which if missed will lead the market to reprice the stock down.

They might also use a non-GAAP measure of earnings to explain that earnings are not as bad as they might seem. ?In the short-run the market may accept that, but if you do that often enough, eventually the markets factor in the many “one-time” adjustments, and lower the earnings multiple on the stock to reflect the reduced quality of earnings.

In addition, having shorter-term targets causes corporations to not get lazy in managing expenses and capital. ?When the measurement periods get too long, discipline can be lost.

Quarterly Earnings Don’t Cause Most Firms to Neglect the Long-Term

Firms aren’t interested in only the current period’s earnings, but about the entire future path of earnings. ?Even if?the current period’s earnings meet the estimates, the job is not done. ?If there aren’t plans to grow earnings for the next 3-5 years, eventually earnings won’t meet the expectations of investors, and the price of the stock will fall. ?The short-term is just the beginning of the long-term. ?It is not either/or but both/and. ?A company has to try to explain to investors how it is?growing the value of the firm — if present targets aren’t being met, why should there be any confidence that the future will be good?

Think of corporate earnings like a long-term project which has a variety of things that have to be done en route to a significant goal. ?The quarterly earnings measure?whether the progress toward completing the goal is adequate or not. ?Now, the measure is not perfect, but who can think of a better one?

Ending Quarterly Earnings Would Not?End Activism, Buybacks, and Dividends

I can think of an area in business where earnings estimates don’t play a role — private equity. ?Are the owners long-term oriented? Yes. ?Are they short-term oriented? ?Yes. ?Is?capital managed tightly? ?Very tightly. ?All excess capital is dividended back — it as if activists run the firms permanently.

If there were no quarterly earnings in the public equity markets, firms would still be under pressure to return excess capital to shareholders. ?Activists would still analyze companies to see if they are badly managed, and in need of change. ?If anything, when companies would release their earnings less frequently, the adjustments to the market price of the stock would be more severe. ?Companies that disappoint would find the activists arriving regardless of the periodicity of the release of earnings.

On the Use of Excess Capital

Investing, particularly for the long-term, is not risk-free. ?In an environment where there is rapid technological change, like there is today, it is difficult to tell what investments will not be made obsolete. ?In such an environment, it can make a lot of sense to focus on shorter-term?investments that are more certain as to the success of the project. ?It is also a reason why dividends and buybacks are done, as capital returned to shareholders is associated with higher stock prices, because the capital is used more efficiently. ?Companies that shrink their balance sheets tend to outperform those that grow them.

As an example, large acquisitions tend not to benefit shareholders, while small acquisitions that lead to greater organic growth do tend to benefit investors. ?The same is true of large versus small investments for organic growth away from M&A. ?Most management teams can adequately estimate and plan for the growth that stems from incremental action. Large revolutionary investments are another thing. ?There is usually no way to estimate how those will work out, and whether the prospects are reasonable or not.

In one sense, it’s best to leave those kinds of investment projects to highly focused firms that do only that. ?That’s how biotech firms work, and it is why so many of them fail. ?The few winners are astounding.

Or, think about how progressive Japanese firms were viewed to be in the 1980s, as they pursued long-term projects that had very low returns on equity. ?All of that failed, to a first approximation, while the derided American model of shareholder capitalism prospered, as capital was used efficiently on projects with high risk-adjusted?returns, and not wasted on speculative projects with uncertain returns. ?The same will prove true of China over the next 20 years as they choke on all of their bad investments that yield low returns, if indeed the returns are positive.

Remember, bad investments are just expenses in fancy garb — it just takes the accounting longer to recognize the losses. ?Think of Enron if you need an example, which brings up one more point: good investing focuses on accounting quality. ?Accrual items on the asset side of the balance sheets of corporations get higher valuations the shorter the accrual is, and the more likely it is to produce cash. ?Most long term projects tend to be speculative, and as such, drag down the valuation of the stock, because in most cases, it lowers the long-term earnings of the company.

Conclusion

If quarterly earnings are abolished, intelligent corporations won’t change much. ?Investment won’t go up much, and the time horizon of most management teams will not rise much. ?If you need any proof of that, look at how private equity and large mutual insurers manage their firms — they still analyze quarterly results, and are conservative in how they deploy capital.

The only great change of eliminating quarterly earnings will be a loss of quality information for equity investors. ?Bond investors and banks will still require more frequent financial updates, and equity investors may try to find ways to get that data, perhaps through the rating agencies.

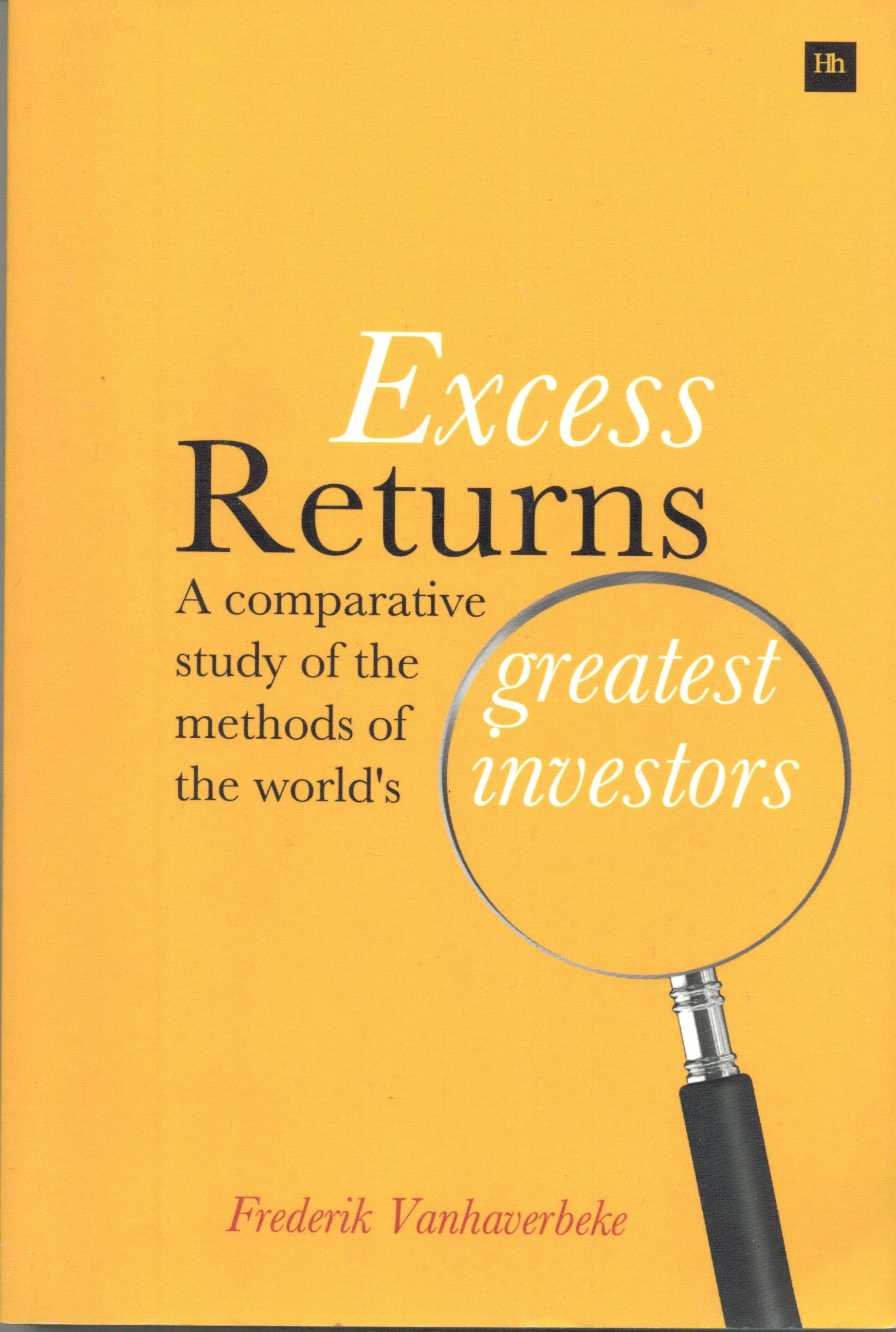

Suppose you wanted a comprehensive book on all of the ways that there are to get excess returns from the stock market as a type of value investor (as of year-end 2013), and you wanted it in one slim volume. ?This is that book. ?As with most desires there is the “be careful what you wish for, you just might get it” effect. ?This book is not immune.

At Aleph Blog, I try to write book reviews that always include what sort of reader might benefit from a given book. ?Because this book packs so much into such a small space, it is not a?book for beginners unless they are?prodigies. ?If you are a beginner, better to warm up with something like The Intelligent Investor, by Ben Graham. ?Beginners need time to see concepts described in greater detail, and more slowly.

Though it is a book on value investing, it is expansive in what it considers value investing. ?It includes topics as varied as:

Behavioral Economics

Market-timing from a valuation standpoint

Growth at a reasonable price [GARP] investing

Private investing

Shorting

Event-driven investing

Barriers to considering investments that keep others from buying them at attractive prices

In a book of around 300 pages, this is ambitious. ?It gives you one or two passes over important topics, so you are only getting a taste of the ideas involved. ?This is also predominantly a book on qualitative investing. ?Pure quantitative value investing doesn’t get much play. ?Non-value anomalies don’t get much coverage.

The other?thing the book lacks is a way to pull it all together in a practical way. ?Yes, the last chapter tries to pull it all together, but given the breadth of the material, it gets pulled together in terms of the attitudes you need to do this right, but less of a “how do you structure an overall investment process to put these principles into practical action.” ?Providing more examples could have been useful, and really, the whole book could have benefited from that.

Additional Resources

Now, if you want a greater taste of the book without buying it, I’ve got a deal for you: this is a medium-sized slide presentation that summarizes the book. ?Pretty sweet, huh? ?It represents the book well, so if you are on the fence, I would look at it — after that you would know if you want to buy it.

Full disclosure:?I?received a?copy from the author.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

I’m not going to argue for any particular strategy here. My main point is this: every valid strategy is going to have some periods of underperformance. ?Don’t give up on your strategy because of that; you are likely to give up near?the point of maximum pain, and miss the great returns in the?bull phase of the strategy.

Here?are three?simple bits of advice that I hand out to average people regarding asset allocation:

Figure out what the maximum loss is that you are willing to take in a year, and then size your allocation to risky assets such that the likelihood of exceeding that loss level is remote.

If you have any doubts on bit of advice #1, reduce the amount of risky assets a bit more. ?You’d be surprised how little you give up in performance from doing so. ?The loss from not allocating to risky assets that return better on average is partly mitigated by a bigger payoff from rebalancing from risky assets to safe, and back again.

Use additional money slated for investing?to rebalance the portfolio. ?Feed your losers.

The first rule is most important, because the most important thing here is avoiding panic, leading to selling risky assets when prices are depressed. ?That is the number one cause of underperformance for average investors. ?The second rule is important, because it is better to earn less and be able to avoid panic than to risk losing your nerve. ?Rule three just makes it easier to maintain your portfolio; it may not be applicable if you follow a momentum strategy.

Now, about momentum strategies — if you’re going to pursue strategies where you are always buying the assets that are presently behaving strong, well, keep doing it. ?Don’t give up during the periods where it doesn’t seem to work, or when it occasionally blows up. ?The best time for any strategy typically come after a lot of marginal players give up because losses exceed their pain point.

That brings me back to rule #1 above — even for a momentum strategy, maybe it would be nice to have some safe assets?on the side to turn down the total level of risk. ?It would also give you some money to toss into the strategy after the bad times.

If you want to try a new strategy, consider doing it when your present strategy has been doing well for a while, and you see new players entering the strategy who think it is magic. ?No strategy is magic; none work all the time. ?But if you “harvest” your strategy when it is mature, that would be the time to do it. ?It would be similar to a bond manager reducing exposure to risky bonds when the additional yield over safe bonds is thin, and waiting for a better opportunity to take risk.

But if you do things like that, be disciplined in how you do it. ?I’ve seen people violate their strategies, and reinvest in the hot asset when the bull phase lasts too long, just in time for the cycle to turn. ?Greed got the better of them.

Markets are perverse. ?They deliver surprises to all, and you can be prepared to react to volatility by having some safe assets to tone things down, or, you can roll with the volatility fully invested and hopefully not panic. ?When too many unprepared people are fully invested in risky assets, there’s a nasty tendency for the market to have a significant decline. ?Similarly, when people swear off investing in risky assets, markets tend to perform really well.

It all looks like a conspiracy, and so you get a variety of wags in comment streams alleging that the markets are rigged. ?The markets aren’t rigged. ?If you are a soldier heading off for war, you have to mentally prepare for it. ?The same applies to investors, because investing isn’t perfectly easy, but a lot of players say that it is easy.

We can make investing easier by restricting the choices that you have to make to a few key ones. ?Index funds. ?Allocation funds that use index funds that give people a single fund to buy that are?continually rebalanced. ?But you would still have to exercise discipline to avoid fear and greed — and thus my three example rules above.

If you need more confirmation on this, re-read my articles on dollar-weighted returns versus time-weighted returns. ?Most trading that average people do loses money versus buying and holding. ?As a result, the best thing to do with any strategy is to structure it so that you never take actions out of a sense of regret for past performance.

That’s easy to say, but hard to do. ?I’m subject to the same difficulties that everyone else is, but I worked to create rules to limit my behavior during times of investment pain.

Your personality, your strategy may differ from mine, but the successful meta-strategy is that you should be disciplined in your investing, and not give into greed or panic. ?Pursue that, whether you invest like me or not.

One of the constants in investing is that average investors show up late to the party or to the crisis. ?Unlike many gatherings where it may be cool to be fashionably late, in investing it tends to mean you earn less and lose more, which is definitely not cool.

One reason why this happens is that information gets distributed in lumps. ?We don’t notice things in real time, partly because we’re not paying attention to the small changes that are happening. ?But after enough time passes, a few people notice a trend. ?After a while longer, still more people notice the trend, and it might get mentioned in some special purpose publications, blogs, etc. ?More time elapses and it becomes a topic of conversation, and articles make it into the broad financial press. ?The final phase is when?general interest magazines put it onto the cover, and get rich quick articles and books point at how great fortunes have been made, and you can do it too!

That slow dissemination and?gathering of information is paralleled by a similar flow of money, and just as the audience gets wider, the flow of money gets bigger. ?As the flow of money in or out gets bigger, prices tend to overshoot fair value, leaving those who arrived last with subpar returns.

There is another aspect to this, and that stems from the way that people commonly evaluate managers. ?We use past returns as a prologue to what is assumed to be still?greater returns in the future. ?This not only applies to retail investors but also many institutional investors. ?Somme institutional investors will balk at this conclusion, but my experience in talking with institutional investors has been that though they look at many of the right forward looking indicators of manager quality, almost none of them will hire a manager that has the right people, process, etc., and has below average returns relative to peers or indexes. ?(This also happens with hedge funds… there is nothing special in fund analysis there.)

For the retail crowd it is worse, because?most investors look at past returns when evaluating managers. ?Much as Morningstar is trying to do the right thing, and have forward looking analyst ratings (gold, silver, bronze, neutral and negative), yet much of the investing public will not touch a fund unless it has four or five stars from Morningstar, which is a backward looking rating. ?This not only applies to individuals, but also committees that choose funds for defined contribution plans. ?If they don’t choose the funds with four or five stars, they get complaints, or participants don’t use the funds.

Another Exercise in Dollar-Weighted Returns

One of the ways this investing shortfall gets expressed is looking at the difference between time-weighted (buy-and-hold) and dollar-weighted (weighted geometric average/IRR) returns. ?The first reveals what an investor who bought and held from the beginning earned, versus what the average dollar invested earned. ?Since money tends to come after good returns have been achieved, and money tends to leave after bad returns have been realized, the time-weighted returns are typically higher then the dollar-weighted returns. ?Generally, the more volatile the performance of the investment vehicle the larger the difference between time- and dollar-weighted returns gets. ?The greed and fear cycle is bigger when there is more volatility, and people buy and sell at the wrong times to a greater degree.

(An aside: much as some pooh-pooh buy-and-hold investing, it generally beats those who trade. ?There may be intelligent ways to trade, but they are always a minority among market actors.)

HSGFX Dollar and Time Weighted Returns

That brings me to tonight’s fund for analysis: Hussman Strategic Growth [HSGFX]. John Hussman, a very bright guy, has been trying to do something very difficult — time the markets. ?The results started out promising, attracting assets in the process, and then didn’t do so well, and assets have slowly left. ?For my calculation this evening, I run the calculation on his fund with the longest track record from inception to 30 June 2014. ?The fund’s fiscal years end on June 30th, and so I assume cash flows occur at mid-year as a simplifying assumption. ?At the end of the scenario, 30 June 2014, I assume that all of the funds remaining get paid out.

To run this calculation, I do what I have always done, gone to the SEC EDGAR website and look at the annual reports, particularly the section called “Statements of Changes in Net Assets.” ?The cash flow for each fiscal year is equal to the?net increase in net assets from capital share transactions plus the net decrease in net assets from distributions to shareholders. ?Once I have?the amount of money moving in or out of the fund in each fiscal year, I can then run an internal rate of return calculation to get the dollar-weighted rate of return.

In my table, the cash flows into/(out of) the fund are in millions of dollars, and the column titled Accumulated PV is the?accumulated present value calculated at an annualized rate of -2.56% per year, which is the dollar-weighted rate of return. ?The zero figure at the top shows that a discount rate -2.56% makes the cash inflows and outflows net to zero.

From the beginning of the Annual Report for the fiscal year ended in June 2014, they helpfully provide the buy-and-hold return since inception, which was +3.68%. ?That gives a difference of 6.24% of how much average investors earned less than the buy-and-hold investors. ?This is not meant to be a criticism of Hussman’s performance or methods, but simply a demonstration that a lot of people invested money after the fund’s good years, and then removed money after years of underperformance. ?They timed their investment in a market-timing fund poorly.

Now, Hussman’s fund may do better when the boom/bust cycle turns if his system makes the right move?somewhere near the bottom of the cycle. ?That didn’t happen in 2009, and thus the present state of affairs. ?I am reluctant to criticize, though, because I tried running a strategy like this for some of my own clients and did not do well at it. ?But when I realized that I did not have the personal ability/willingness to?buy when valuations were high even though the model said to do so because of momentum, rather than compound an error, I shut down the product, and refunded some fees.

One thing I can say with reasonable confidence, though: the low returns of the past by themselves are not a reason to not invest in Mr. Hussman’s funds. ?Past returns by themselves tell you almost nothing about future returns. ?The hard questions with a fund like this are: when will the cycle turn from bullish to bearish? ?(So that you can decide how long you are willing to sit on the sidelines), and when the cycle turns from bearish to bullish, will Mr. Hussman make the right decision then?

Those questions are impossible to answer with any precision, but at least those are the right questions to ask. ?What, you’d rather have the answer to a simple question like how did it return?in the past, that has no bearing on how the fund will do in the future? ?Sadly, that is the answer that propels more investment decisions than any other, and it is what leads to bad overall investment returns on average.

PS — In future articles in this irregular series, I will apply this to the Financial Sector Spider [XLF], and perhaps some fund of Kenneth Heebner’s. ?Till then.

When you analyze?a manager, look at the repeatability of his processes. ?It’s possible that you could get “the Big Short” right once, and never have another good investment idea in your life. ?Same for investors who are the clever ones who picked the most recent top or bottom… they are probably one-trick ponies.

When a manager does well and begins to pick up a lot of new client assets, watch for the period where the growth slows to almost zero. ?It is quite possible that some of the great performance during the high growth period stemmed from asset prices rising due to the purchases of the manager himself. ?It might be a good time to exit, or, for shorts to consider the assets with the highest percentage of market cap owned as targets for shorting.

Often when countries open up to foreign investment, valuations are relatively low. ?The initial flood of money in often pushes up valuations, leads to momentum buyers, and a still greater flow of money. ?Eventually an adjustment comes, and shakes out the undisciplined investors. ?But, when you look at the return series analyze potential future investment, ignore the early years — they aren’t representative of the future.

Before an academic paper showing a way to invest that would been clever to use in the past gets published, the excess returns are typically described as coming from valuation, momentum, manager skill, etc. ?After the paper is published, money starts getting applied to the idea, and the strategy will do well initially. ?Again, too much money can get applied to a limited factor (or other) anomaly, because no one knows how far it can get pushed before the market rebels. ?Be careful when you apply the research — if you are late, you could get to hold the bag of overvalued companies. ?Aside for that, don’t assume that performance from the academic paper’s era or the 2-3 years after that will persist. ?Those are almost always the best years for a factor (or other) anomaly strategy.

During a credit boom, almost every new type of fixed income security, dodgy or not, will look like genius by?the early purchasers. ?During a credit bust, it is rare for a new security type to fare well.

Anytime you take a large position in an obscure security, it must jump through extra hoops to assure a margin of safety. ?Don’t assume that merely because you are off the beaten path that you are a clever contrarian, smarter than most.

Always think about the carrying capacity of a strategy when you look at an academic paper. ?It might be clever, but it might not be able to handle a lot of money. ?Examples would include trying to do exactly what Ben Graham did in the early days today, and things like Piotroski’s methods, because typically only a few small and obscure stocks survive the screen.

Also look at how an academic paper models trading and liquidity, if they give it any real thought at all. ?Many papers embed the idea that liquidity is free, and large trades can happen where prices closed previously.

Hedge funds and other manager databases should reflect that some managers have closed their funds, and put them in a separate category, because new money can’t be applied to those funds. ?I.e., there should be “new money allowed” indexes.

Max Heine, who started the Mutual Series funds (now part of Franklin), was a genius when he thought of the strategy 20% distressed investing, 20% arbitrage/event-driven investing and 60% value investing. ?It produced great returns 9 years out of 10. ?but once distressed investing and event-driven because heavily done, the idea lost its punch. ?Michael Price was clever enough to sell the firm to Franklin before that was realized, and thus capitalizing the past track record that would not?do as well in the future.

The same applies to a lot of clever managers. ?They have a very good sense of when their edge is getting dulled by too much competition, and where the future will not be as good as the past. ?If they have the opportunity to sell, they will disproportionately do so then.

Corporate management teams are like rock bands. ?Most of them never have a hit song. ?(For managements, a period where a strategy improves profitability far more than most would have expected.) ?The next-most are one-hit wonders. ?Few have multiple hits, and rare are those that create a culture of hits. ?Applying this to management teams — the problem is if they get multiple bright ideas, or a culture of success, it is often too late to invest, because the valuation multiple adjusts to reflect it. ?Thus, advantages accrue to those who can spot clever managements before the rest of the market. ?More often this happens in dull industries, because no one would think to look there.

It probably doesn’t make sense to run from hot investment idea to hot investment idea as a result of all of this. ?You will end up getting there once the period of genius is over, and valuations have adjusted. ?It might be better to buy the burned out stuff and see if a positive surprise might come. ?(Watch margin of safety…)

Macroeconomics and the effect that it has on investment returns is overanalyzed, though many get the effects wrong anyway. ?Also, when central bankers and politicians take cues from the prices of risky assets, the feedback loop confuses matters considerably. ?if you must pay attention to macro in investing, always ask, “Is it priced in or not? ?How much of it is priced in?”

Most asset allocation work that relies on past returns is easy to do and bogus. ?Good asset allocation is forward-looking and ignores past returns.

Finally, remember that some ideas seem?right by accident — they aren’t actually right. ?Many academic papers don’t get published. ?Many different methods of investing get tried. ?Many managements try new business ideas. ?Those that succeed get air time, whether it was due to intelligence or luck. ?Use your business sense to analyze which it might be, or, if it is a combination.

There’s more that could be said here. ?Just be cautious with new investment strategies, whatever form they may take. ?Make sure that you maintain a margin of safety; you will likely need it.

Factors like Valuation, Sentiment, Momentum, Size, Neglect…

New technologies

New financing methods and security types

Changes in government policies will have effects, cultural change, or other top-down macro ideas

New countries to invest in

Events where value might be discovered, like recapitalizations, mergers, acquisitions, spinoffs, etc.

New asset classes or subclasses

Durable competitive advantage of marketing, technology, cultural, or other corporate practices

Now, before an idea is discovered, the economics behind the idea still exist, but the returns happen in a way that no one yet perceives. ?When an idea is discovered, the discovery might be made public early, or the discoverer might keep it to himself until it slowly leaks out.

For an example, think of Ben Graham in the early days. ?He taught openly at Columbia, but few followed his ideas within the investing public because everyone was still shell-shocked from the trauma of the Great Depression. ?As a result, there was a large amount of companies trading for less than the value of their current assets minus their total liabilities.

As Graham gained disciples, both known and unknown, they chipped away at the companies that were so priced, until by the late ’60s there were few opportunities of that sort left. ?Graham had long since retired; Buffett winds up his partnerships, and manages the textile firm he took over as a means of creating a nascent conglomerate.

The returns generated during its era were phenomenal, but for the most part, they were never to be repeated. ?Toward the end of the era, many of the practitioners made their own mistakes as they violated “margin of safety” principles. ?It was a hard way of learning that the vein of financial ore they were mining was finite, and trying to expand to mine a type of “fool’s gold” was not a winning idea.

Value investing principles, rather than dying there, broadened out to consider?other ways that securities could be undervalued, and the analysis process began again.

My main point this evening is this: when a valid new investing idea is discovered, a lot of returns are generated in the initial phase. For the most part they will never be repeated because there will likely never be another time when that investment idea is totally forgotten.

Now think of the technologies that led to the dot-com bubble. ?The idealism, and the “follow the leader” price momentum that it created lasted until enough cash was sucked into unproductive enterprises, where the value was destroyed. ?The current economic value of investment ideas can overshoot or undershoot the fundamental value of the idea, seen in hindsight.

My second point is that often the price performance of an investment idea overshoots. ?Then the cash flows of the assets can’t justify the prices, and the prices fall dramatically, sometimes undershooting. ?It might happen because of expected?demand that does not occur, or too much short-term leverage applied to long-term assets.

Later, when the returns for the investment idea are calculated, how do you characterize the value of the investment idea? ?A new investment factor is discovered:

it earns great returns on a small amount of assets applied to it.

More assets get applied, and more people use the factor.

The factor develops its own price momentum, but few?think about it that way

The factor exceeds the “carrying capacity”?that it should have in the market, overshoots, and burns out or crashes.

It may be downplayed, but it lives on to some degree as an aspect of investing.

On a time-weighted rate of return basis, the factor will show that it had great performance, but a lot of the excess returns will be in the early era where very little money was applied to the factor. ?By the time a lot of money was applied to the factor, the future excess returns were either small or even negative. ?On a dollar-weighted basis, the verdict on the factor might not be so hot.

So, how useful is the time-weighted rate of return series for the factor/idea in question for making judgments about the future? ?Not very useful. ?Dollar weighted? ?Better, but still of limited use, because the discovery era will likely never be repeated.

What should we do then to make decisions about any factor/idea for purposes of future decisions? ?We have to look at the degree to which the factor or idea is presently neglected, and estimate future potential returns if the neglect is eliminated. ?That’s not easy to do, but it will give us a better sense of future potential than looking at historical statistics that bear the marks of an unusual period that is little like the present.

It leaves us with a mess, and few?firm statistics to work from, but it is better to be approximately right and somewhat uncertain, than to be precisely wrong with tidy statistical anomalies bearing the overglorified title “facts.”

That’s all for now. ?As always, be careful with your statistics, and use sound business judgment to analyze their validity in?the present situation.

I was writing to potential clients when I realized that I don’t have so much to write about my bond track record as I do my track record with stocks. ?I jotted down a note to formalize what I say about my bond portfolios.

One person I was writing to asked some detailed questions, and I told him that the stock market was likely to return about 4.5%/yr (not adjusted for inflation) over the next ten years. ?The model I use is the same one as this one used by pseudonymous Philosophical Economist. ?I don’t always agree with him, but he’s a bright guy, what can I say? ?That’s not a very high return — the historical average is around 9.5%. ?The market is in the 85th-90th percentiles of valuation, which is pretty high. ?That said, I am not taking any defensive action yet.

Yet.

But then it hit me. ?The yield on my bond portfolio is around 4.5% also. ?Now, it’s not a riskless bond portfolio, as you can tell by the yield. ?I’m no longer running the portfolio described in Fire and Ice. ?I sold the long Treasuries about 30 basis points ago. ?Right now, I am only running the Credit sensitive portion of the portfolio, with a bit of foreign bonds mixed in.

Why am I doing this? ?I think it has a good balance of risks. ?Remember that there is no such thing as generic risk. ?There are many risks. ?At this point this portfolio has a decent amount of credit risk, some foreign exchange risk, and is low in interest rate risk. ?The duration of the portfolio is less than?2, so I am not concerned about rising rates, should the FOMC ever do such a thing as raise rates. ?(Who knows? ?The economy might actually grow faster if they did that. ?Savers will eventually spend more.)

But 10 years is a long time for a bond portfolio with a duration of less than 2 years. ?I’m clipping coupons in the short run, running credit risk while I don’t see any major credit risks on the horizon aside from weak sovereigns (think the PIIGS), student loans, and weak junk (ratings starting with a “C”). ?The risks on bank loans are possibly overdone here, even with weakened covenants. ?Aside from that, if we really do see a lot of credit risk crop up, stocks will get hit a lot harder than this portfolio. ?Dollar weakness and US inflation (should we see any) would also not be a risk.

I’ve set a kind of a mental stop loss at losing 5% of portfolio value. ?Bad credit is the only significant factor that could harm the portfolio. ?If credit problems got that bad, it would be time to exit because credit problems come in bundles, not dribs and drabs.

I’m not doing it yet, but it is?tempting to reposition some of my IRA assets presently in stocks into the bond strategy. ?I’m not sure I would lose that much in terms of profit potential, and it would increase the overall safety of the portfolio.

I’ll keep you posted. ?That is, after I would tell my clients what I am doing, and give them a chance to act, should they want to.

Finally, do you have a different opinion? ?You can email me, or, you can share it with all of the readers in the comments. ?Please do.

This is a difficult book to review. ?Let me tell you what it is not, and then let me tell you what it is more easily as a result.

1) The book?does not give you detailed biographies of the people that it features. ?Indeed, the writing on each person is less than the amount that Ken Fisher wrote in his book, 100 Minds That Made the Market. ?If you are looking for detailed biographical sketches, you will be disappointed.

2) The book does not give detailed and comparable reviews of the portfolio performance of those that it features. ?There’s no way from what is written to tell really how good many of the investors are. ?I mean, I would want to see dollar-weighted rates of return, and perhaps, measures of dollar alpha. ?The truly best managers have expansive strategies that can perform well managing a large amount of money.

3) The book admits that the managers selected may not be the greatest, but are some of the “greats.” ?Okay, fair enough, but I would argue that a few of the managers don’t deserve to be featured even as that if you review their dollar-weighted performance. ?A few of them showed that they did not pay adequate attention to margin of safety in the recent financial crisis, and lost a lot of money for people at the time that they should have been the most careful.

What do you get in this book? ?You get beautiful black and white photos of 33 managers, and vignettes of each of them written by six authors. ?The author writes two-thirds of the vignettes.

Do I recommend this book? ?Yes, if you understand what it is good for. ?It is a well-done coffee table book on thick glossy paper, with truly beautiful photographs.?It is well-suited for people waiting in a reception area, who want to read something light and short about several?notable investment managers.

But if you are looking for anything involved in my five points above, you will not be satisfied by this book.

One final note on the side — I would have somehow reworked the layout of Bill Miller’s photograph. ?Splitting his face down the middle of the gutter does not?represent him to be the handsome guy that he is.

Full disclosure:?I?received a?copy from the author. ?He was most helpful.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

Today I saw an article about a high school investing contest, and like most contests of that type, it does not teach investing, but speculation.

I’ve wanted to try this for about ten years or so. ?I’d like to try running a?stock picking contest, but only if I can offer decent prizes, and get enough participants. ?I’ve written about this before, these would be the rules:

No leverage and no shorting

No trading — buy & hold

No Exchange Traded Products, and only common stocks

Minimum market capitalization of $100 million

Only stocks traded on US exchanges

Forced diversification — a portfolio of ten stocks equally weighted

One stock from each of ten volatility buckets, to reduce speculation

Highest geometric mean return wins — this gives a bonus to consistency, which also reduces speculation. ?(Alternative rule: the best return on the?seventh best stock in each portfolio wins.)

Six month time frame.

One entry per person.

The most critical rules are seven and eight. ?The idea is to get people to think like investors, not speculators. ?By forcing investors to buy a broad range of companies from conservative to aggressive will force them to evaluate individual companies, with an eye to avoiding big losers. ?Rule number one, as many say, is don’t lose money. ?This would?honor the idea of avoiding losses while trying to make gains. ?It would be a lot like what intelligent investing in a portfolio of stocks is really like.

The idea is to promote stock-picking. ?Now lest you think I have taken all of the speculation out of this, let me tell you what my rules don’t stop:

Factor tilts — you can assemble a portfolio with price momentum

Industry and sector tilts

Foreign tilts

Size tilts

Valuation tilts

Investing in special situations

Copying famous investors

Now, Who Would Be Sponsors?

I can’t fund this on my own. ?Also, I don’t think registration fees could fund such a contest. ?Parties that could benefit from the branding and free advertising would include financial information companies and brokerages — they are some of the logical beneficiaries of promoting stock-picking. ?So, would the following consider sponsoring such a contest?

Wall Street Journal, Yahoo Finance, Bloomberg, Marketwatch, Reuters, Money, Value Line, theStreet.com, etc.

Nasdaq OMX, Intercontinental Exchange

Schwab, E-Trade, Scottrade, Interactive Brokers,?Ameritrade, Fidelity, ETrade, etc.

I don’t know, but I would want to have at least 1,000 entrants and $50,000 in prize money if were going to run a contest like this. ?I’m sure it would be a lot of fun, and would teach investors a lot about investing, as opposed to speculation.

Thoughts? ?Send them to me. ?(Especially if you are interested in sponsoring the event.)