The Financial Report of the United States Government 2016

=================================================

The last time I wrote about this was four years ago. ?I have covered this topic off and on for the last 25 years. ?As usual, the report got released during a relatively dead time, January 12th, where most people were listening to the preparations for the inauguration. ?I’ll give them some credit though — not as much of a dead time as usual; it was in the middle of a work week, AND earlier than usual. ?(It would be nice to know when it’s coming, though.)

I have two main messages to go with my two graphs. ?The first message is one I have been saying before — beware some of the estimates that you hear, should you hear them at all. ?No one wants to talk about this, but what few that do will look at a few headline numbers and leave it there. ?Really you have to look at it for years, and look at the footnotes and other explanatory sections in the back when things seemingly change for no good reason. ?Also, you have to add all the bits up. ?No one will do that for you. ?Even with that, you are relying on the assumptions that the government uses, and they are not biased toward making the estimates sound larger. ?They tend to make them smaller.

Thus you will see two things that adjust the headline figures. ?In 2004, when Medicare part D was created, the Financial Report of the US Government began mentioning the Infinite Horizon Increment. ?Now, that liability always existed, but the actuaries began calculating how solvent is the system as a whole if it were permanent, as opposed to lasting 75 years.

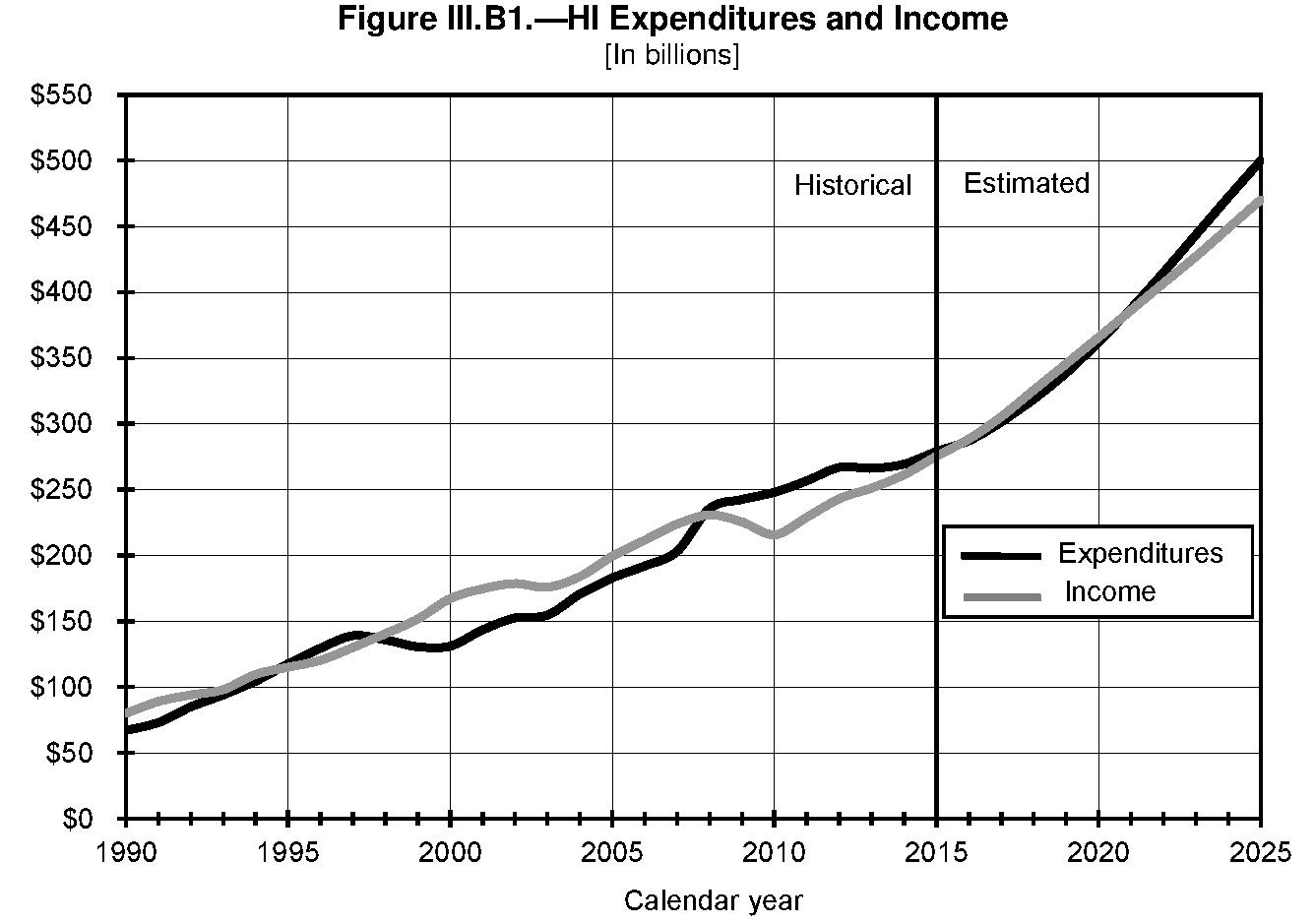

The second is the Alternative Medicare Scenario. ?When the PPACA (Obamacare) was created in 2010, there was considerable chicanery in the cost estimates. ?The biggest part was that they assumed Medicare Part A (HI) would cost a lot less because they would reduce the amount that they would reimburse. ?They legislated away costs by assuming them away, and then each year Congress would restore the funding so that there wouldn’t be a firestorm when doctors stopped taking Medicare. ?But they left it in for budget and forecast purposes, and showed what the projections would be like if these cuts never took place in what they called the?Alternative Medicare Scenario.

So, did the cuts to Medicare part A take place? No.

As you can see they have gone up almost every year since 2010. The liability should not have gone down. If you think the?Alternative Medicare Scenario is conservative enough, the liability has remained relatively constant since 2010, not diminished dramatically.

How is the load relative to GDP? ?It keeps growing, but since 2010 at a less frantic clip. ?The adjusted ratio below includes the?Alternative Medicare Scenario.

Final Notes

Remember that we have had a recovery since 2009. ?The statistics never assume that we will have another recession, much less a full fledged crisis like 2008-9. ?Without adjustment, the Medicare part A trust fund will run out in 2028. ?There is no provision for what the reimbursements will be made if the trust fund runs dry. ?Social Security’s trust fund will run out a few years after that, and instead of getting 12 checks a year, people will only get 9 of that same amount. ?If there is a significant recession, those statistics will move forward by an unknown number of years. ?Without congressional action, because there will be a recession, I would expect that both will run out somewhere in the middle of the 2020s, and then the real political fun will begin.

The tendency has been over time to turn these from entitlements to old age welfare schemes. ?FDR always wanted them to be self funded entitlements with everybody getting roughly the same treatment by formula, because he wanted the program to have widespread legitimacy across all classes, and no sense of stigma for being a poor old person on the dole.

Given the strategies that exist around qualifying for Medicaid, those days are gone, so I would expect that benefits will be limited for those better off, inflation adjustments eliminated, taxes raised to some degree, eligibility ages quickly raised a few more years, with elimination of strategies that allow people to get more out of the system by being clever. ?(As an example, expect the favorable late retirement factors to get reduced, and the early retirement factors to go down even more.)

Does this sound fun? ?Of course not, but remember that cultures are larger than economies, which are larger than governments. ?The cultural need for supporting poor elderly people will lead funding to continue, unless it makes the government, and the culture as a whole fail in the process, and that would never happen, right?

{kind=link}