I’m thinking of starting a limited series called “dirty secrets” of finance and investing. ?If anyone wants to toss me some ideas you can contact me here. ?I know that since starting this blog, I have used the phrase “dirty secret” at least ten times.

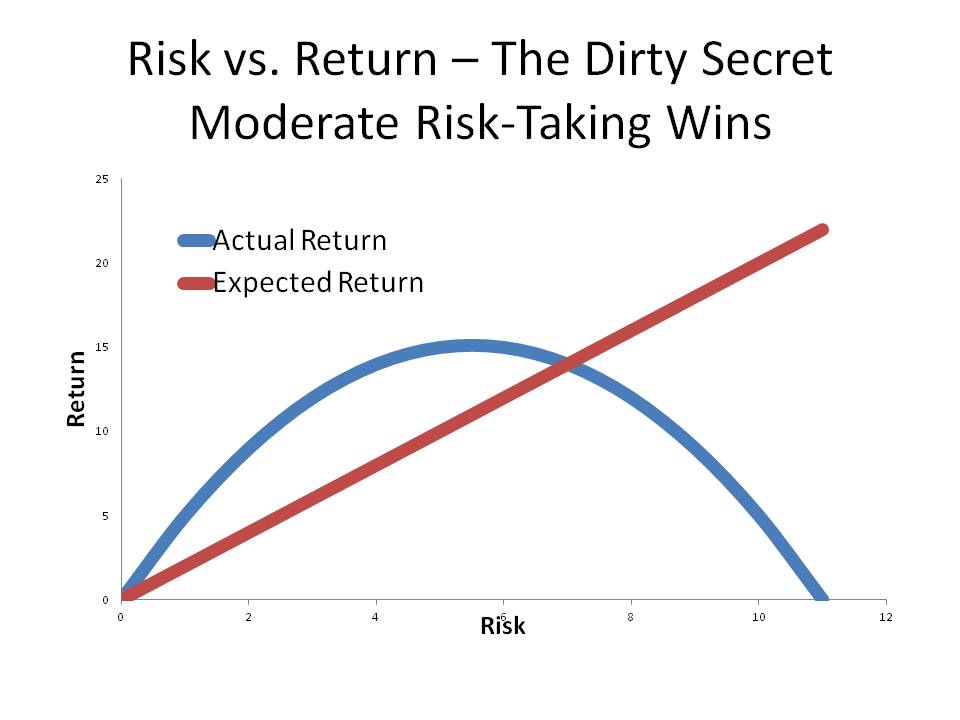

Tonight’s dirty secret is a simple one, and it derives mostly from investor behavior. ?You don’t always get more return on average if you take more risk. ?The amount of added return declines with each unit of additional risk, and eventually turns negative at high levels of risk. ?The graph above is a vague approximate representation of how this process works.

Why is this so? ?Two related reasons:

People are not very good at estimating the probability of success for ventures, and it gets worse as the probability of success gets lower. ?People overpay for chancy lottery ticket-like investments, because they would like to strike it rich. ?This malady affect men more than women, on average.

People get to investment ideas late. ?They buy closer to tops than bottoms, and they sell closer to bottoms than tops. ?As a result, the more volatile the investment, the more money they lose in their buying and selling. ?This malady also affects men more than women, on average.

Put another way, this is choosing your investments based on your circle of competence, such that your probability of choosing a good investment goes up, and second, having the fortitude to hold a good investment through good and bad times. ?From my series on dollar-weighted returns you know that the more volatile the investment is, the more average people lose in their buying and selling of the investment, versus being a buy-and-hold investor.

Since stocks are a long duration investment, don’t buy them unless you are going to hold them long enough for your thesis to work out. ?Things don’t always go right in the short run, even with good ideas. ?(And occasionally, things go right in the short run with bad ideas.)

For more on this topic, you can look at my creative piece,?Volatility Analogy. ?It explains the intuition behind how volatility affects the results that investors receive as they get greedy, panic, and hold on for dear life.

In closing, the dirty secret is this: size your risk level to what you can live with without getting greedy or panicking. ?You will do better than other investors who get tempted to make rash moves, and act on that temptation. ?On average, the world belongs to moderate risk-takers.

Photo Credit: Kathryn || Truly, I sympathize. ?I try to be strong for others when internally I am broken.

Entire societies and nations have been wiped out in the past. ?Sometimes this has been in spite of the best efforts of leading citizens to avoid it, and sometimes it has been because of their efforts. ?In human terms, this is as bad as it gets on Earth. ?In virtually all of these cases, the optimal strategy was to run, and hope that wherever you ended up would be kind to foreigners. ?Also, most common methods of preserving value don’t work in the worst situations… flight capital stashed early in the place of refuge?and?gold might work, if you can get there.

There. ?That’s the worst survivable scenario I can think of. ?What does it take to get there?

Total government and?market breakdown, or

A lost war on your home soil, with the victors considerably less kind than the USA and its allies

The odds of these are very low in most of the developed world. ?In the developing world, most of the wealthy have “flight capital” stashed away in the USA or someplace equally reliable.

Most nations, societies and economies are more durable than most people would expect. ?There is a cynical reason for this: the wealthy and the powerful have a distinct interest in not letting things break. ?As Solomon observed a little less than 3000 years ago:

If you see the oppression of the poor, and the violent perversion of justice and righteousness in a province, do not marvel at the matter; for high official watches over high official, and higher officials are over them. Moreover the profit of the land is for all; even the king is served from the field. — Ecclesiastes 5:8-9 [NKJV]

In general, I think there is?no value in preparing for the “total disaster” scenario if you live in the developed world. ?No one wants to poison their own prosperity, and so the?rich and powerful?hold back from being too rapacious.

If you don’t have a copy, it would?be a good idea to get a copy of?Triumph of the Optimists. ?[TOTO] ?As I commented in my review of TOTO:

TOTO points out a number of things that should bias investors toward risk-bearing in the equity markets:

Over the period 1900-2000, equities beat bonds, which beat cash in returns. (Note: time weighted returns. If the study had been done with dollar-weighted returns, the order would be the same, but the differences would not be so big.)

This was true regardless of what presently developed nation you looked at. (Note: survivor bias? what of all the developing markets that looked bigger in 1900, like Russia and India, that amounted to little?)

Relative importance of industries shifts, but the aggregate market tended to do well regardless. (Note: some industries are manias when they are new)

Returns were higher globally in the last quarter of the 20th century.

Downdrafts can be severe. Consider the US 1929-1932, UK 1973-74, Germany 1945-48, or Japan 1944-47. Amazing what losing a war on your home soil can do, or, even a severe recession.

Real cash returns tend to be positive but small.

Long bonds returned more than short bonds, but with a lot more risk. High grade corporate bonds returned more on average, but again, with some severe downdrafts.

Purchasing power parity seems to work for currencies in the long run. (Note: estimates of forward interest rates work in the short run, but they are noisy.)

International diversification may give risk reduction. During times of global stress, such as wartime, it may not diversify much. Global markets are more correlated now than before, reducing diversification benefits.

Small caps may or may not outperform large caps on average.

Value tends to beat growth over the long run.

Higher dividends tend to beat lower dividends.

Forward-looking equity risk premia are lower than most estimates stemming from historical results. (Note: I agree, and the low returns of the 2000s so far in the US are a partial demonstration of that. My estimates are a little lower, even?)

Stocks will beat bonds over the long run, but in the short run, having some bonds makes sense.

Returns in the latter part of the 20th century were artificially high.

Capitalist republics/democracies tend to be very resilient. ?This should make us willing to be long term bullish.

Now, many people look at their societies and shake their heads, wondering if things won’t keep getting worse. ?This typically falls into three?non-exclusive buckets:

The rich are getting richer, and the middle class is getting destroyed ?(toss in comments about robotics, immigrants, unfair trade, education problems with children, etc. ?Most such comments are bogus.)

The dependency class is getting larger and larger versus the productive elements of society. ?(Add in comments related to demographics… those comments are not bogus, but there is a deal that could be driven here. ?A painful deal…)

Looking at moral decay, and wondering at it.

You can add to the list. ?I don’t discount that there are challenges/troubles. ?Even modestly healthy society can deal with these without falling apart.

If you give into fears like these, you can become prey to a variety of investment “experts” who counsel radical strategies that will only succeed with very low probability. ?Examples:

Strategies that neglect investing in risk assets at all, or pursue shorting them. ?(Even with hedge funds you have to be careful, we passed the limits to arbitrage back in the late ’90s, and since then aggregate returns have been poor. ?A few niche hedge funds make sense, but they limit their size.)

Gold, odd commodities — trend following CTAs can sometimes make sense as a diversifier, but finding one with skill is tough.

Anything that smacks of being part of a “secret club.” ?There are no secrets in investing. ?THERE ARE NO SECRETS IN INVESTING!!! ?If you think that con men in investing is not a problem, read?On Avoiding Con Men. ?I spend lots of time trying to take apart investment pitches that are bogus, and yet I feel that I am barely scraping the surface.

Things are rarely as bad as they seem. ?Be willing to be a modest bull most of the time. ?I’m not saying don’t be cautious — of course be cautious! ?Just don’t let that keep you from taking some risk. ?Size your risks to your time horizon for needing cash back, and your ability to sleep at night. ?The biggest risk may not be taking no risk, but that might be the most common risk economically for those who have some assets.

To close, here is a personal comment that might help: I am natively a pessimist, and would easily give into disaster scenarios. ?I had to train myself to realize that even in the worst situations there was some reason for optimism. ?That served me well as I invested spare assets at the bottoms in 2002-3 and 2008-9. ?The sun will rise tomorrow, Lord helping us… so?diversify and take moderate risks most of time.

Photo Credit: Paw Paw || The excitement of anticipating our friend’s arrival is overcoming our dignity

While perusing Barron’s on Saturday, I wondered if I had picked up a?publication entitled, “Hope for Broken-hearted Value Investors.” ?Note the articles, most of which should be behind a paywall:

Two things: First, this could just be a bounce off of the recent run-up in oil prices. ?Lots of value investors are hiding there, and I think they are early. ?Also, many people are hoping for a bounce in global growth, but there isn’t a lot to commend that in the short run.

Second, there are too many people hoping for this. ?Lots of money is flowing out of value strategies, and the stocks are cheap. ?I’ve lost several clients, and may lose some more.

Oddly, it is the losing of clients that gives me the most hope. ?You need people to leave a strategy when it is down and out for the strategy to bottom. ?These are the sorts of people that create the difference between time-weighted and dollar-weighted returns. ?They will move to strategies that have outperformed, so they can lose money again.

As for me, I’m not changing. ?I like my stocks more than ever, and I think I’ve got good ideas throughout?the portfolio. ?But I am not?depending on value investing as a strategy turning upward now. ?I think we still need and will get more pain before it turns.

Both articles are exercises in understanding the time horizon over which you invest. ?If you are older, you may not have the time to recover from market shortfalls, so advice to buy dips may sound hollow when you are nearer to drawing on your assets.

Thus the idea that volatility, presumably negative, doesn’t hurt unless you sell. ?Some people don’t have much choice in the matter. ?They have retired, and they have a lump sum of money that they are managing for long-term income. ?No more money is going in, money is only going out. ?What can you do?

You have to plan before volatility strikes. ?My equity only clients had 14% cash before the recent volatility hit. ?Over the past week I opportunistically brought that down to 10% in names that I would like to own even if the “crisis” deepened. ?That flexibility was built into my management. ?(If the market recovers enough, I will rebuild the buffer. ?Around 1300 on the S&P, I would put all cash to work, and move to the alternative portfolio management strategy where I sell the most marginal ideas one at a time to raise cash and reinvest into the best ideas.)

If an older investor would be?hurt by a drawdown in the stock market, he needs to invest less in stocks now, even if that means having a lower income on average over the longer-term. ?With a higher level of bonds in the portfolio, he could more than?proportionately draw down on bonds during a crisis, which would rebalance his portfolio. ?If and when the stock market recovered, for a time, he could draw on has stock positions more than proportionately then. ?That also would rebalance the portfolio.

Again, plans like that need to be made in advance. ?If you have no plans for defense, you will lose most wars.

One more note: often when we talk about time horizon, it sounds like we are talking about a single future point in time. ?When the time for converting assets to cash is far distant, using a single point may be a decent approximation. ?When the time for converting assets to cash is near, it must be viewed as a stream of payments, and whatever scenario testing, (quasi)?Monte Carlo simulations, and sensitivity analyses are done must reflect that.

Many different scenarios may have the same average rate of return, but the ones with early losses and late gains are pure poison to the person trying to manage a lump sum in retirement. ?The same would apply to an early spike in inflation rates followed by deflation.

The time to plan is now for all contingencies, and please realize that this is an art and not a science, so if someone comes to you with glitzy simulation?analyses, ask them to run the following scenarios: run every 30-year period back as far as the data goes. ?If it doesn’t include the Great Depression, it is not realistic enough. ?Run them forwards, backwards, upside-down forwards, and upside-down backwards. ?(For the upside-down scenarios normalize the return levels to the right side up levels.) ?The idea here is to use real volatility levels in the analyses, because reality is almost always more volatile than models using normal distributions. ?History is meaner, much meaner than models, and will likely be meaner in the future… we just don’t know how it will be meaner.

You will then be surprised at how much caution the models will indicate, and hopefully those who can will save more, run safer asset allocations, and plan to withdraw less over time. ?Reality is a lot more stingy than the models of most financial Dr. Feelgoods out there.

One more note: and I know how to model this, but most won’t — in the Great Depression, the returns after 1931 weren’t bad. ?Trouble is, few were able to take advantage of them because they had already drawn down on their investments. ?The many bankruptcies meant there was a smaller market available to invest in, so the dollar-weighted returns in the Great Depression were lower than the buy-and-hold returns. ?They had to be lower, because many people could not hold their investments for the eventual recovery. ?Part of that was margin loans, part of it was liquidating assets to help tide over unemployment.

It would be wonky, but simulation models would have to have an uptick in need for withdrawals at the very time that markets are low. ?That’s not all that much different than some had to do in the recent financial crisis. ?Now, who is willing to throw *that* into financial planning models?

The simple answer is to be more conservative. ?Expect less from your investments, and maybe you will get positive surprises. ?Better that than being negatively surprised when older, when flexibility is limited.

One of my clients asked me what I think is a hard question: When should I deploy capital? ?I?ll try to answer that here.

There are three?main things to consider in using cash to buy or sell assets:

What is your time horizon? ?When will you likely need the money for spending purposes?

How promising is the asset in question? ?What do you think it might return vs alternatives, including holding cash?

How safe is the asset in question? ?Will it survive to the end of your time horizon under almost all circumstances and at least preserve value while you wait?

Other questions like ?Should I dollar cost average, or invest the lump?? are lesser questions, because what will make the most difference in ultimate returns comes from ?the above three questions. ?Putting it another way, the?results of dollar cost averaging depend on returns after you put in the last dollar of the lump, as does investing the lump sum all at once.

Thinking about price momentum and mean-reversion are also lesser matters, because if your time horizon is a long one, the initial results will have a modest effect on the ultimate results.

Now, if you care about price momentum, you may as well ignore the rest of the piece, and start trading in and out with the waves of the market, assuming you can do it. ?If you care about mean reversion, you can wait in cash until we get ?the mother of all selloffs? and then invest. ?That has its problems as well: what?s a big enough selloff? ?There are a lot of bears waiting for rock bottom valuations, but the promised bargain valuations don?t materialize because others invest at higher prices than you would, and the prices?never get as low as you would like. ?Ask John Hussman.

Investing has to be done on a ?good enough? basis. ?The optimal return in hindsight is never achieved. ?Thus, at least for value investors like me, we focus on what we can figure out:

How long can I set aside this capital?

Is this a promising investment at a relatively attractive price?

Do I have a margin of safety buying this?

Those are the same questions as the first three, just phrased differently.

Now, I?m not saying that there is never a time to sit on cash, but decisions like that are typically limited to times where valuations are utterly nuts, like 1964-5, 1968, 1972, 1999-2000 ? basically parts of the go-go years and the dot-com bubble. ?Those situations don?t last more than a decade, and are typically much shorter.

Beyond that, if you have the capital to spare, and the opportunity is safe and cheap, then deploy the capital. ?You?ll never get it perfect. ?The price may fall after you buy. ?Those are the breaks. ?If that really bothers you, then maybe do half of what you would ultimately do, but set a time limit for investment of the other half. ?Remember, the opposite can happen, and the price could run away from you.

A better idea might show up later. ?If there is enough liquidity,?trade into the new idea.

Since perfection is not achievable, if you have something good enough, I recommend that you execute and deploy the capital. ?Over the long haul, given relative peace, the advantage belongs to the one who is invested.

If you still wonder about this question you can read the following two articles:

One of my clients asked me what I think is a hard question: When should I deploy capital? ?I?ll try to answer that here.

There are three?main things to consider in using cash to buy or sell assets:

What is your time horizon? ?When will you likely need the money for spending purposes?

How promising is the asset in question? ?What do you think it might return vs alternatives, including holding cash?

How safe is the asset in question? ?Will it survive to the end of your time horizon under almost all circumstances and at least preserve value while you wait?

Other questions like ?Should I dollar cost average, or invest the lump?? are lesser questions, because what will make the most difference in ultimate returns comes from ?the above three questions. ?Putting it another way, the?results of dollar cost averaging depend on returns after you put in the last dollar of the lump, as does investing the lump sum all at once.

Thinking about price momentum and mean-reversion are also lesser matters, because if your time horizon is a long one, the initial results will have a modest effect on the ultimate results.

Now, if you care about price momentum, you may as well ignore the rest of the piece, and start trading in and out with the waves of the market, assuming you can do it. ?If you care about mean reversion, you can wait in cash until we get ?the mother of all selloffs? and then invest. ?That has its problems as well: what?s a big enough selloff? ?There are a lot of bears waiting for rock bottom valuations, but the promised bargain valuations don?t materialize because others invest at higher prices than you would, and the prices?never get as low as you would like. ?Ask?John Hussman.

Investing has to be done on a ?good enough? basis. ?The optimal return in hindsight is never achieved. ?Thus, at least for value investors like me, we focus on what we can figure out:

How long can I set aside this capital?

Is this a promising investment at a relatively attractive price?

Do I have a margin of safety buying this?

Those are the same questions as the first three, just phrased differently.

Now, I?m not saying that there is never a time to sit on cash, but decisions like that are typically limited to times where valuations are utterly nuts, like 1964-5, 1968, 1972, 1999-2000 ? basically parts of the go-go years and the dot-com bubble. ?Those situations don?t last more than a decade, and are typically much shorter.

Beyond that, if you have the capital to spare, and the opportunity is safe and cheap, then deploy the capital. ?You?ll never get it perfect. ?The price may fall after you buy. ?Those are the breaks. ?If that really bothers you, then maybe?do half?of what you would ultimately do, but set a time limit for investment of the other half. ?Remember, the opposite can happen, and the price could run away from you.

A better idea might show up later. ?If there is enough liquidity,?trade into the new idea.

Since perfection is not achievable, if you have something good enough, I recommend that you execute and deploy the capital. ?Over the long haul, given relative peace, the advantage belongs to the one who is invested.

If you still wonder about this question you can read the following two articles:

I’m not going to argue for any particular strategy here. My main point is this: every valid strategy is going to have some periods of underperformance. ?Don’t give up on your strategy because of that; you are likely to give up near?the point of maximum pain, and miss the great returns in the?bull phase of the strategy.

Here?are three?simple bits of advice that I hand out to average people regarding asset allocation:

Figure out what the maximum loss is that you are willing to take in a year, and then size your allocation to risky assets such that the likelihood of exceeding that loss level is remote.

If you have any doubts on bit of advice #1, reduce the amount of risky assets a bit more. ?You’d be surprised how little you give up in performance from doing so. ?The loss from not allocating to risky assets that return better on average is partly mitigated by a bigger payoff from rebalancing from risky assets to safe, and back again.

Use additional money slated for investing?to rebalance the portfolio. ?Feed your losers.

The first rule is most important, because the most important thing here is avoiding panic, leading to selling risky assets when prices are depressed. ?That is the number one cause of underperformance for average investors. ?The second rule is important, because it is better to earn less and be able to avoid panic than to risk losing your nerve. ?Rule three just makes it easier to maintain your portfolio; it may not be applicable if you follow a momentum strategy.

Now, about momentum strategies — if you’re going to pursue strategies where you are always buying the assets that are presently behaving strong, well, keep doing it. ?Don’t give up during the periods where it doesn’t seem to work, or when it occasionally blows up. ?The best time for any strategy typically come after a lot of marginal players give up because losses exceed their pain point.

That brings me back to rule #1 above — even for a momentum strategy, maybe it would be nice to have some safe assets?on the side to turn down the total level of risk. ?It would also give you some money to toss into the strategy after the bad times.

If you want to try a new strategy, consider doing it when your present strategy has been doing well for a while, and you see new players entering the strategy who think it is magic. ?No strategy is magic; none work all the time. ?But if you “harvest” your strategy when it is mature, that would be the time to do it. ?It would be similar to a bond manager reducing exposure to risky bonds when the additional yield over safe bonds is thin, and waiting for a better opportunity to take risk.

But if you do things like that, be disciplined in how you do it. ?I’ve seen people violate their strategies, and reinvest in the hot asset when the bull phase lasts too long, just in time for the cycle to turn. ?Greed got the better of them.

Markets are perverse. ?They deliver surprises to all, and you can be prepared to react to volatility by having some safe assets to tone things down, or, you can roll with the volatility fully invested and hopefully not panic. ?When too many unprepared people are fully invested in risky assets, there’s a nasty tendency for the market to have a significant decline. ?Similarly, when people swear off investing in risky assets, markets tend to perform really well.

It all looks like a conspiracy, and so you get a variety of wags in comment streams alleging that the markets are rigged. ?The markets aren’t rigged. ?If you are a soldier heading off for war, you have to mentally prepare for it. ?The same applies to investors, because investing isn’t perfectly easy, but a lot of players say that it is easy.

We can make investing easier by restricting the choices that you have to make to a few key ones. ?Index funds. ?Allocation funds that use index funds that give people a single fund to buy that are?continually rebalanced. ?But you would still have to exercise discipline to avoid fear and greed — and thus my three example rules above.

If you need more confirmation on this, re-read my articles on dollar-weighted returns versus time-weighted returns. ?Most trading that average people do loses money versus buying and holding. ?As a result, the best thing to do with any strategy is to structure it so that you never take actions out of a sense of regret for past performance.

That’s easy to say, but hard to do. ?I’m subject to the same difficulties that everyone else is, but I worked to create rules to limit my behavior during times of investment pain.

Your personality, your strategy may differ from mine, but the successful meta-strategy is that you should be disciplined in your investing, and not give into greed or panic. ?Pursue that, whether you invest like me or not.

Factors like Valuation, Sentiment, Momentum, Size, Neglect…

New technologies

New financing methods and security types

Changes in government policies will have effects, cultural change, or other top-down macro ideas

New countries to invest in

Events where value might be discovered, like recapitalizations, mergers, acquisitions, spinoffs, etc.

New asset classes or subclasses

Durable competitive advantage of marketing, technology, cultural, or other corporate practices

Now, before an idea is discovered, the economics behind the idea still exist, but the returns happen in a way that no one yet perceives. ?When an idea is discovered, the discovery might be made public early, or the discoverer might keep it to himself until it slowly leaks out.

For an example, think of Ben Graham in the early days. ?He taught openly at Columbia, but few followed his ideas within the investing public because everyone was still shell-shocked from the trauma of the Great Depression. ?As a result, there was a large amount of companies trading for less than the value of their current assets minus their total liabilities.

As Graham gained disciples, both known and unknown, they chipped away at the companies that were so priced, until by the late ’60s there were few opportunities of that sort left. ?Graham had long since retired; Buffett winds up his partnerships, and manages the textile firm he took over as a means of creating a nascent conglomerate.

The returns generated during its era were phenomenal, but for the most part, they were never to be repeated. ?Toward the end of the era, many of the practitioners made their own mistakes as they violated “margin of safety” principles. ?It was a hard way of learning that the vein of financial ore they were mining was finite, and trying to expand to mine a type of “fool’s gold” was not a winning idea.

Value investing principles, rather than dying there, broadened out to consider?other ways that securities could be undervalued, and the analysis process began again.

My main point this evening is this: when a valid new investing idea is discovered, a lot of returns are generated in the initial phase. For the most part they will never be repeated because there will likely never be another time when that investment idea is totally forgotten.

Now think of the technologies that led to the dot-com bubble. ?The idealism, and the “follow the leader” price momentum that it created lasted until enough cash was sucked into unproductive enterprises, where the value was destroyed. ?The current economic value of investment ideas can overshoot or undershoot the fundamental value of the idea, seen in hindsight.

My second point is that often the price performance of an investment idea overshoots. ?Then the cash flows of the assets can’t justify the prices, and the prices fall dramatically, sometimes undershooting. ?It might happen because of expected?demand that does not occur, or too much short-term leverage applied to long-term assets.

Later, when the returns for the investment idea are calculated, how do you characterize the value of the investment idea? ?A new investment factor is discovered:

it earns great returns on a small amount of assets applied to it.

More assets get applied, and more people use the factor.

The factor develops its own price momentum, but few?think about it that way

The factor exceeds the “carrying capacity”?that it should have in the market, overshoots, and burns out or crashes.

It may be downplayed, but it lives on to some degree as an aspect of investing.

On a time-weighted rate of return basis, the factor will show that it had great performance, but a lot of the excess returns will be in the early era where very little money was applied to the factor. ?By the time a lot of money was applied to the factor, the future excess returns were either small or even negative. ?On a dollar-weighted basis, the verdict on the factor might not be so hot.

So, how useful is the time-weighted rate of return series for the factor/idea in question for making judgments about the future? ?Not very useful. ?Dollar weighted? ?Better, but still of limited use, because the discovery era will likely never be repeated.

What should we do then to make decisions about any factor/idea for purposes of future decisions? ?We have to look at the degree to which the factor or idea is presently neglected, and estimate future potential returns if the neglect is eliminated. ?That’s not easy to do, but it will give us a better sense of future potential than looking at historical statistics that bear the marks of an unusual period that is little like the present.

It leaves us with a mess, and few?firm statistics to work from, but it is better to be approximately right and somewhat uncertain, than to be precisely wrong with tidy statistical anomalies bearing the overglorified title “facts.”

That’s all for now. ?As always, be careful with your statistics, and use sound business judgment to analyze their validity in?the present situation.

This is a difficult book to review. ?Let me tell you what it is not, and then let me tell you what it is more easily as a result.

1) The book?does not give you detailed biographies of the people that it features. ?Indeed, the writing on each person is less than the amount that Ken Fisher wrote in his book, 100 Minds That Made the Market. ?If you are looking for detailed biographical sketches, you will be disappointed.

2) The book does not give detailed and comparable reviews of the portfolio performance of those that it features. ?There’s no way from what is written to tell really how good many of the investors are. ?I mean, I would want to see dollar-weighted rates of return, and perhaps, measures of dollar alpha. ?The truly best managers have expansive strategies that can perform well managing a large amount of money.

3) The book admits that the managers selected may not be the greatest, but are some of the “greats.” ?Okay, fair enough, but I would argue that a few of the managers don’t deserve to be featured even as that if you review their dollar-weighted performance. ?A few of them showed that they did not pay adequate attention to margin of safety in the recent financial crisis, and lost a lot of money for people at the time that they should have been the most careful.

What do you get in this book? ?You get beautiful black and white photos of 33 managers, and vignettes of each of them written by six authors. ?The author writes two-thirds of the vignettes.

Do I recommend this book? ?Yes, if you understand what it is good for. ?It is a well-done coffee table book on thick glossy paper, with truly beautiful photographs.?It is well-suited for people waiting in a reception area, who want to read something light and short about several?notable investment managers.

But if you are looking for anything involved in my five points above, you will not be satisfied by this book.

One final note on the side — I would have somehow reworked the layout of Bill Miller’s photograph. ?Splitting his face down the middle of the gutter does not?represent him to be the handsome guy that he is.

Full disclosure:?I?received a?copy from the author. ?He was most helpful.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

15 years is a long time to wait for a 1%/yr return

The big news of the day is that the NASDAQ Composite hit a new high for the first time in 15 years. ?Nice, except as you note from the above graph, that if you adjusted for inflation, you still haven’t made a new high. ?By the time the NASDAQ Composite hits a new high, it will have to rack up at least another 2000 points, which is 40% or so away. ?Now if you add dividends back in since March 10th, 2000, you get to roughly a 1% return.

That’s a lot of pain for not much gain. ?That said, few if any rode out this storm in a fund like the NASDAQ composite. The pain would have been so great that most would have given up in 2002, and those that survived would have given up in 2008-9. ?We aren’t designed to take that much pain and hold on. ?I have a stronger financial pain tolerance than most, and I can’t think of a stock I hung on to past a 75% decline that ever came back in full. ?50%? ?Yes. ?75%? ?No.

I haven’t run the dollar-weighted return calculation for the QQQ, but I’ll try to run that calculation in a future blog post, and who knows, maybe I will run the calculation for John Hussman’s main fund at some future point also.

Look Elsewhere

Looking at the NASDAQ Composite is more a glimpse at the past rather than the future. ?But let me take two more glimpses at the past before I give you a guess at the future.

I remember March 10th, 2000, and the months around it. ?As the dot-com bubble expanded, what industry did the worst, and bounced back the hardest? ?Property/Casualty Insurance. ?I tell my story in detail in this post that I find amusing. ?To shorten this article, I can tell you that if you invested in undervalued industries in 2000-2001, you didn’t get hurt badly at all; you may even have made money like me. ?2002 was another matter — everything got smashed.

But many famous value investors never got to participate in that rally, because they got fired, or retired amid the furor of the dot-com bubble. ?This is yet another reason why it is so hard as an asset manager to hold onto promising assets that are out of favor… if your clients leave you because they?can’t take any more pain, you will be forced to liquidate because of them. ?If you are a big enough holder of those assets, the process may drive the price down further, adding insult to injury.

In my own case, I got derided by peers in early 2000 by owning a lot of property/casualty insurers, particularly my own company, The St. Paul (now part of the Travelers).

Here’s another glimpse: Sometime in 2005, I got introduced to a company called Industrias Bachoco [IBA]. ?It was a medium-sized chicken producer based in Celaya, Mexico. ?Today,?I believe?it is second to Tyson Foods in North America as far as chicken production goes.

It looked interesting and underfollowed, in an industry that I thought had good prospects, because in a world with a growing middle class, meat would be a?premium food product in demand. ?So I bought some, and mostly held on.

Yummy Chicken, no?

If you had bought IBA on March 10th, 2000, and held until today, you would have gotten a little more than a 17%/year return. ?4% of that came from dividends. ?Not quite a Peter Lynch 10-bagger from that point, but getting closer by the day.

Because I got there later, my returns haven’t been as good as that, but still well worth owning over the last ten years. ?I highlight IBA because I know it well, and it serves as a good example of a?winning?stock that few would have been likely to choose. ?Agriculture is not a sexy industry, whereas technology gets lots of admirers. ?But with an intelligent management team and conservative finances, IBA has done very well. ?Now, what will do well in the future?

This is why I tell you to look elsewhere for ideas, away from the crowds. ?Not that everything will do as well as IBA did, but where are the good assets that few are looking at?

Tough question. ?I’ll give you a few ideas, but then you have to work on it yourself.

1) Look at higher quality names in out-of-favor industries. ?The advantage of this approach is that your downside is likely to be limited, while the upside could be significant. ?I’ve seen it work many times. ?Note: avoid “buggy whip” industries where the decline is final; the internet is eating a lot of industries.

2) Look at companies outside the US that act in the best interests of outside, passive, minority investors like you and me. ?There is less competition there from analysts and clever US-focused investors. ?Note: spend extra time analyzing how they have used free cash flow in the past. ?Is management rational at allocating capital, or even clever?

3) Look at firms that can’t be taken over, where a control investor seems savvy, and acts in?the best interests of outside, passive, minority investors. ?Many won’t invest in those firms because they are less liquid, and a takeover is very unlikely.

4) Look at smaller firms pursuing a growing niche in an otherwise dull industry. ?Or smaller firms that have good finances, but have some taint that keeps investors from re-examining it.

5) Look through 13F filings for new names that look promising, before too many people learn about the company. ?Or, IPOs and spin-offs in industries that are dull.

6) Analyze stocks that are in the lowest quartile of performance over the last 3-5 years.

7) Or, go to Value Line, and look at the stocks with the highest appreciation potential, with an adequate safety rank.

Regardless, look forward from here, and look at assets that are cheap relative to future prospects that few others are looking at. ?There is little value in searching where everyone else does, such as the main stocks in the NASDAQ Composite.

Full Disclosure: long IBA and TRV for clients and me