One of my clients asked me what I think is a hard question: When should I deploy capital? ?I?ll try to answer that here.

There are three?main things to consider in using cash to buy or sell assets:

What is your time horizon? ?When will you likely need the money for spending purposes?

How promising is the asset in question? ?What do you think it might return vs alternatives, including holding cash?

How safe is the asset in question? ?Will it survive to the end of your time horizon under almost all circumstances and at least preserve value while you wait?

Other questions like ?Should I dollar cost average, or invest the lump?? are lesser questions, because what will make the most difference in ultimate returns comes from ?the above three questions. ?Putting it another way, the?results of dollar cost averaging depend on returns after you put in the last dollar of the lump, as does investing the lump sum all at once.

Thinking about price momentum and mean-reversion are also lesser matters, because if your time horizon is a long one, the initial results will have a modest effect on the ultimate results.

Now, if you care about price momentum, you may as well ignore the rest of the piece, and start trading in and out with the waves of the market, assuming you can do it. ?If you care about mean reversion, you can wait in cash until we get ?the mother of all selloffs? and then invest. ?That has its problems as well: what?s a big enough selloff? ?There are a lot of bears waiting for rock bottom valuations, but the promised bargain valuations don?t materialize because others invest at higher prices than you would, and the prices?never get as low as you would like. ?Ask John Hussman.

Investing has to be done on a ?good enough? basis. ?The optimal return in hindsight is never achieved. ?Thus, at least for value investors like me, we focus on what we can figure out:

How long can I set aside this capital?

Is this a promising investment at a relatively attractive price?

Do I have a margin of safety buying this?

Those are the same questions as the first three, just phrased differently.

Now, I?m not saying that there is never a time to sit on cash, but decisions like that are typically limited to times where valuations are utterly nuts, like 1964-5, 1968, 1972, 1999-2000 ? basically parts of the go-go years and the dot-com bubble. ?Those situations don?t last more than a decade, and are typically much shorter.

Beyond that, if you have the capital to spare, and the opportunity is safe and cheap, then deploy the capital. ?You?ll never get it perfect. ?The price may fall after you buy. ?Those are the breaks. ?If that really bothers you, then maybe do half of what you would ultimately do, but set a time limit for investment of the other half. ?Remember, the opposite can happen, and the price could run away from you.

A better idea might show up later. ?If there is enough liquidity,?trade into the new idea.

Since perfection is not achievable, if you have something good enough, I recommend that you execute and deploy the capital. ?Over the long haul, given relative peace, the advantage belongs to the one who is invested.

If you still wonder about this question you can read the following two articles:

One of my clients asked me what I think is a hard question: When should I deploy capital? ?I?ll try to answer that here.

There are three?main things to consider in using cash to buy or sell assets:

What is your time horizon? ?When will you likely need the money for spending purposes?

How promising is the asset in question? ?What do you think it might return vs alternatives, including holding cash?

How safe is the asset in question? ?Will it survive to the end of your time horizon under almost all circumstances and at least preserve value while you wait?

Other questions like ?Should I dollar cost average, or invest the lump?? are lesser questions, because what will make the most difference in ultimate returns comes from ?the above three questions. ?Putting it another way, the?results of dollar cost averaging depend on returns after you put in the last dollar of the lump, as does investing the lump sum all at once.

Thinking about price momentum and mean-reversion are also lesser matters, because if your time horizon is a long one, the initial results will have a modest effect on the ultimate results.

Now, if you care about price momentum, you may as well ignore the rest of the piece, and start trading in and out with the waves of the market, assuming you can do it. ?If you care about mean reversion, you can wait in cash until we get ?the mother of all selloffs? and then invest. ?That has its problems as well: what?s a big enough selloff? ?There are a lot of bears waiting for rock bottom valuations, but the promised bargain valuations don?t materialize because others invest at higher prices than you would, and the prices?never get as low as you would like. ?Ask?John Hussman.

Investing has to be done on a ?good enough? basis. ?The optimal return in hindsight is never achieved. ?Thus, at least for value investors like me, we focus on what we can figure out:

How long can I set aside this capital?

Is this a promising investment at a relatively attractive price?

Do I have a margin of safety buying this?

Those are the same questions as the first three, just phrased differently.

Now, I?m not saying that there is never a time to sit on cash, but decisions like that are typically limited to times where valuations are utterly nuts, like 1964-5, 1968, 1972, 1999-2000 ? basically parts of the go-go years and the dot-com bubble. ?Those situations don?t last more than a decade, and are typically much shorter.

Beyond that, if you have the capital to spare, and the opportunity is safe and cheap, then deploy the capital. ?You?ll never get it perfect. ?The price may fall after you buy. ?Those are the breaks. ?If that really bothers you, then maybe?do half?of what you would ultimately do, but set a time limit for investment of the other half. ?Remember, the opposite can happen, and the price could run away from you.

A better idea might show up later. ?If there is enough liquidity,?trade into the new idea.

Since perfection is not achievable, if you have something good enough, I recommend that you execute and deploy the capital. ?Over the long haul, given relative peace, the advantage belongs to the one who is invested.

If you still wonder about this question you can read the following two articles:

I try not to be an ideologue, and I often fail. One bias of mine is that most macroeconomic policy actions of the government or central bank either don’t help, or merely shift the problem to another place.

Tonight’s issue is the wealth effect, which tends to be favored more by conservatives. ?The wealth effect is the tendency to spend more as the market value of the assets of a person rises. ?I don’t think the wealth effect is zero, but I don’t think can be?very big, and tonight, I will explain why.

Now, imagine that you own some assets and the value of them has grown. ?You’re feeling richer, and you would like to live richer as a consequence. ?How are you going to do it? ?You could:

Sell some of the assets.

Borrow against the assets.

If you control the assets, you could increase the stream of dividends, or pay yourself a higher salary.

Trade the assets for assets that pay a higher income.

Do more exotic things, like sell call options — but let’s ignore those possibilities for now. ?Those are just contingent forms of selling.

Let’s take these in order:

Sell Assets

Selling appreciated assets in most cases means incurring a capital gain and paying taxes. ?It can be an effective way of raising your purchasing power on a one-time basis. ?It also means that someone like you, or, one of their representatives, is going to have to part with money so that you can receive cash for your money. ?The net effect for the economy is not likely to be an increase of cash spent on consumption as a result.

As an aside, some people might be averse to selling assets in a big way because they don’t want to consume capital. ?They may not believe that the remainder of their assets will continue to rise in value, and as such might not be willing to spend from realized capital gains. ?That said, many older people *will* have to consume capital in old age, but they aren’t well-enough off to produce a wealth effect — they worry whether their assets will last.

Borrow Against Assets

I think this is dangerous if done in a big way, though I have seen some crackpots advocating that. ?We should have learned from the financial crisis that if borrowing against stable assets like a home in order to spend can result in disaster, it does not make sense to do it against more volatile assets like stocks or a private business. ?Your home is not an ATM. ?That same logic should apply to a brokerage account.

If you do borrow against an appreciated asset in order to spend, that may increase your spending one time, but unless the value of your assets continually increases, you won’t be able to do it forever. ?And, if asset values fall dramatically, you may find that if your debts are greater than your assets, that your spending may go down considerably as you pay back debt to hold onto your assets.

Now, if a lot of people are inverted in their borrowing, an increase in the overall price level of assets could make some?people un-invert and breathe easier, and after a while, spend more from their incomes. ?But the rise there will likely be offset by others whose savings aren’t worth as much being reticent to spend.

Pay Yourself a Greater Dividend or Salary

If you own all of a given asset, this?becomes a question of taking income versus spending on capital expenditures to grow or maintain the business. ?Greater personal spending is offset by lesser business spending. ?Oh, and you have to pay tax on the income you receive. ?If you own part of the business, but still control it, receiving a higher salary disproportionately helps you versus your minority shareholders. ?You might be able to spend more, but it comes out of their pockets.

Trade Your Assets for Assets that Pay a Higher Income

First, it’s a simple trade. ?You might have more income to spend, but someone else has less on average. ?Beyond that, it makes more sense to pursue investments that give you the best returns regardless of how much income they pay. ?You can decide on the income you need via dividends, selling bits of the investment, etc.

Income is not an inherent aspect of an asset. ?Within bounds, it is arbitrary, as noted in the two articles to which?I linked. ?As a result, choosing a higher income set of assets may not give you more to spend over time. ?Even if Congress passed a law tomorrow saying that all companies, public and private, have to pay a dividend equal to 3% of market value (or fair value, however determined), it might increase personal taxable income, but many would reinvest it while some would spend. ?As for the corporations, they would have to spend less on capital expenditures, or borrow more to fund them. ?A great increase in spending would be unlikely.

Summary

None of the ways I mentioned for getting more money for spending out of investments is likely to produce a lot of additional spending in aggregate across the economy. ?As a result, I think that the Executive Branch, the Congress, and the Federal Reserve should be cautious of trying to make asset values rise, or encourage more borrowing against assets. ?It will likely not have any significant effect to grow the economy over the intermediate -to-long term.

There is the temptation when market prices move fast after they have been at recent highs to assume that things are going to fall apart. ?Well, guess what? ?That could happen.

I don’t think it is likely though, if falling apart means a scenario like 2008-9,?2000-2 or 1973-4. ?In order to have a significant drawdown in the market, you have to have a lot of leverage collapse, whether that is financial or operating leverage.

Financial leverage is bad debt. ?We have areas of that — student loans, agricultural loans, a modest amount of subprime lending for autos, and a decent amount of lending to junk-rated corporations, but not enough to create a self-reinforcing situation where bad debts can’t be borne by lenders, and lenders then collapse.

Operating leverage is bad assets — building up too much productive capacity such that there will not be enough demand to absorb it for the foreseeable future. ?Or, building capacity that isn’t productive… either way, assets will have to be written down.

There have been a number of parties kvetching about a lack of investment from US corporations, but let’s take this a different direction. ?There hasn’t been a lot of bad investment from US corporations… and part of that may be due to dividend and buyback policies. ?Yes, there are some IPOs that have come out that look marginal. ?I’ve looked at a variety of spin-offs where the underlying business is attractive, but they loaded the spin-off with a sizable slug of debt in order to pay a final dividend to the parent company saying farewell. ?But on the whole, I don’t see a lot of money being wasted by corporations on investments. ?That is another reason why profit margins are high.

Now, a lot of the furor in the markets stems from China, and the effects that slowing growth and/or bad debts in China will have on the US economy. ?Personally, I don’t think this is an issue to worry about, unless you have a lot of investments in China and other emerging markets. ?In general, US markets don’t get deeply hurt by slowdowns or even crises in other countries. ?Even if it means a slowdown in revenue growth for large US corporations, it would also likely mean that US interest rates might fall, which would often make equities fall less as bonds rally.

Also, for foreign affairs to affect the US in a big way, the US would have to have a lot of lending exposure to those nations that are struggling. ?(Think of the LDC nations in the early ’80s.) ?Maybe this is one of the benefits of running current account?deficits — we don’t have money to lend to foreign countries from our net export earnings.

Think of all the significant foreign crises of the last 30 years. ?LDC crisis, Plaza Accords leading to Japan’s lost decades, Mexico, Asian Crisis, European Union difficulties with their fringe nations, Iceland, Greece, Greece, Greece, China, etc. ?There was always temporary indigestion in US markets, but when did it ever weigh on the US markets for a long period? ?Really, it never did. ?So why are we concerned over China?

Regarding the Fed, I abstract from this old post, which quoted a 2005?piece on Fed policy at RealMoney.com, and what blew up at the end of each tightening cycle. ?I list blow-ups up to that point, and mention that I think US Housing is next:

2000 ? Nasdaq

1997-98 ? Asia/Russia/LTCM, though that was a small move for the Fed

1994 ? Mortgages/Mexico

1989 ? Banks/Commercial Real Estate

1987 ? Stock Market

1984 ? Continental Illinois

Early ?80s ? LDC debt crisis

So it moves in baby steps, wondering if the next straw will break some camel?s back where lending has been going on terms that were too favorable. The odds of this 1/4% move creating such a nonlinear change is small, but not zero.

But on the bright side, the odds of a 50 basis point tightening at any point in the next year are even smaller. The markets can?t afford it.

Some worry now about future Fed policy — what will blow up when the Fed tightens too much? ?I would encourage everyone to relax. ?First, we don’t know that the Fed will do anything soon. ?Second, we don’t know if they will do anything much. ?Third, we don’t even know if the Fed has a coherent theory of monetary policy anymore. ?Face it: Yellen has never tightened rates once. ?Bernanke never tightened rates aside from finishing out Greenspan’s plan to invert the yield curve at the beginning of his Chairmanship. ?Almost no one on the FOMC has any significant practical experience with tightening rates. ?What will guide them out of their zero interest rate policy? ?What will be enough?

Even so, tightening cycles usually end with something blowing up. ?Maybe this time it is the emerging markets. ?I don’t see a large concentration of US-based bad debt that the Fed might inadvertently blow up, at least not yet. ?(Maybe the day will come when the US Treasury might complain about rising financing rates. ?After all, debt is high, but affordable while rates are low.)

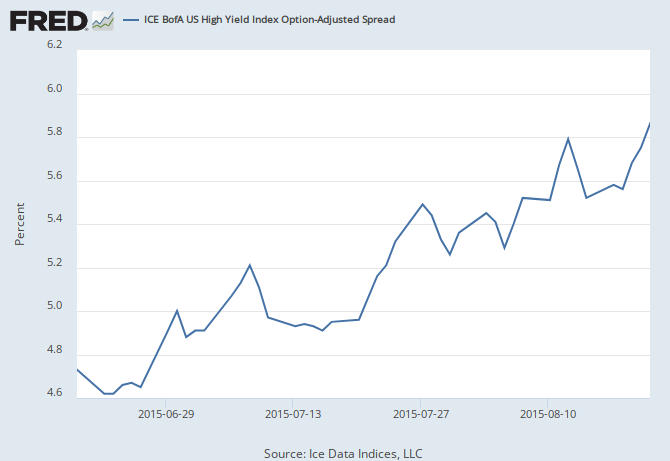

Valuation is the main issue as I see it at present, as I commented in my recent piece “Stocks or Bonds?” ?When stocks are priced at a level that discounts 4.5%/year returns over the next 10 years, you don’t have a lot of margin for error, especially when you can create a safer bond portfolio that yields the same.

Now, since I wrote that piece, the S&P 500 is down around 10.5%. ?The bond portfolio is down around 4.5% (it was a risky portfolio, and some of the emerging markets bonds hurt), while the Barclays’ Aggregate is up 1%. ?High-yield bond spreads have widened over that time by ~1.2%.

The anticipated return on the S&P 500 has maybe risen by 1%/year over the next 10 years, to 5.5%. ?That said, so has the yield on the risky bond portfolio. ?I see the selloff as being in-line with the yields of risky debt, which at some higher level of spread, will attract buyers, given that there have been no significant defaults recently.

The US stock market could go down another 20% from here, but I think it will be less. ?My main point is that we shouldn’t get a big washout, but just a correction of valuation levels that got too high relative to other risky assets, like junk bonds.

So don’t panic. ?You could still move some assets from stocks to bonds if you want to sleep better, but don’t do anything severe.

This is a story of triumph and tragedy. ?Jesse Livermore is notable as one of the few people who ever made it into the richest tiers of society by speculating — by trading stocks and commodities — betting on price movements.

This is three stories in one. ?Story one is the clever trader with an intuitive knack who learned to adapt when conditions changed, until the day came when it got too hard. ?Story two is the man who lacked financial risk control, and took big chances, a few of which worked out spectacularly, and a few of ruined him financially. ?Story three is how too much success, if not properly handled, can ruin a man, with lust, greed and pride leading to his death.

The author spends most of his time on story one, next most on story two, then the least on story?three. ?The three stories flow naturally from the narrative that is largely chronological. ?By the end of the book, you see Jesse Livermore — a guy who did amazing things, but?ultimately failed in money and life.

Let me briefly summarize those three aspects of his life so that you can get a feel for what you will run into in the book:

The Clever Trader

Jesse Livermore came to the stock market in Boston at age 14, and was a very quick study. ?He showed intuition on market affairs that impressed the most of the older men who came to trade at the brokerage where he worked. ?It wasn’t too long before he wanted to invest for himself, but he didn’t have enough money to open a brokerage account, so he went to a bucket shop. ?Bucket shops were gambling parlors where small players gambled on stock prices. ?He showed a knack for the game and made a lot of money. ?Like someone who beats the casinos in Vegas, the proprietors forced him to leave.

He then had more than enough money to meet his current needs, and set up a brokerage account. ?But the stock market did not behave like a bucket shop, and so he lost money while he learned to adapt. ?Eventually, he succeeded at speculating on both stocks and commodities, leading to his greatest successes in being short the stock market prior to the panic of 1907, and the crash in 1929. ?During the 1920s, he started his own firm to try to institutionalize his gifts, and it worked for much of the era.

After the crash in 1929, the creation of the SEC and all the associated laws and regulations made speculating a lot more difficult, to the point where he could not make significant money speculating anymore.

The Poor Financial Risk Manager

Amid the successes, he tended to aim for greater wins after his largest successes, which led to him losing much of what he had previously made. ?One time he was cheated out of much of what he had while trading cotton.

Amid all of that, he was well-liked by most he interacted with in a business context. ?Even after great losses, many wanted him to succeed again, and so they bankrolled him after failure. ?Before?the Great Depression, he did not disappoint them — he succeeded in speculation and came roaring back, repaying all of his past debts with interest.

In one sense, it was live by the big speculation, and?die by the big speculation. ?When you play with so much borrowed money, it’s hard for results to not be volatile.

A?Rock Star of His Era

When he won big, he lived big. ?Compared to many wealthy people of his era, he let spending expand far more than many who had ?more reliable sources of income. ?Where did the money go? ?Yachts, homes, staff, wives, women, women, women… ?Aside from the last of his three wives, his marriages were troubled.

His last wife was a nice woman who was independently wealthy, and after Livermore lost?it all in the mid-’30s, he increasingly relied on her to stay afloat. ?When he could no longer be the hero who could win a good living out of the market via speculation, his deflated pride led him to commit suicide in 1940.

A Sad Book Amid Amazing Successes

Sadly, his son and grandson who shared his name committed suicide in 1975 and 2006, respectively. ?On the whole, the story of Jesse Livermore’s?life and legacy is a sad one. ?It should disabuse people of the notion that wealth?brings happiness. ?If anything, it teaches that money that comes too easily tends to get lost easily also.

The author does a good job?weaving the strands of his life into a consistent whole. ?The book is well-written, and probably the best book out there on the life of the famous speculator that so many present speculators admire. ?A side benefit is that in passing, you will learn a lot about the development of the markets during a time when they were less regulated. ?(The volatility of markets was obvious then. ?It not obvious now, which is why people get surprised by it when it explodes.)

Quibbles

None.

Summary / Who Would Benefit from this Book

This is a comprehensive book that explains?the life and times of Jesse Livermore, one of the greatest speculators in history. ?It will teach you history, but it won’t teach you how to speculate. ?If you want to buy it, you can buy it here: Jesse Livermore – Boy Plunger: The Man Who Sold America Short in 1929.

Full disclosure:?I?received a?copy from a kind PR flack.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

The following may be controversial. It also may be dull to the point that you might not care. Here’s why you should care: quarterly reporting is a useful and productive use of corporate resources, and it would be a shame to lose it because some people with a patina of intelligence think it is harmful. Who knows? Losing it might even make you poorer.

Influential law firm Wachtell, Lipton, Rosen & Katz has an idea that may be music to the ears of its big corporate clients and a nightmare for some investors and analysts: end quarterly earnings reports.

Wachtell on Tuesday called on the Securities and Exchange Commission to consider allowing U.S. companies to do away with the obligatory updates, one of the most important rituals on Wall Street and in corporate America, suggesting that they distract executives from long-term goals.

The basic case is that quarterly earnings lead companies to behave in a short-term manner, and underinvest for longer-term growth, thus hurting the US economy. ?I disagree. There are at least four?things that are false in the arguments made in the article, and in books like?Saving Capitalism from Short-Termism:

Quarterly earnings don’t produce value in and of themselves

Quarterly earnings cause most corporations to ignore the long-term.

Ending quarterly earnings will end activism, buybacks, and dividends.

Buybacks and dividends are bad uses of capital, and more capital investment, especially for long-dated projects, is necessarily a good thing.

Most of the value of a Corporation on a going concern basis stems from the future earnings of the company.? Investors want to have an estimate of forward earnings so that they can gauge whether the company is growing at an appropriate rate.

Now, it wouldn?t matter if the system were set up by third-party sell side analysts, by buyside analysts, by companies themselves, or by a combination thereof.? The thing is investors are forward-looking, and they want a forward-looking estimate to allow them to estimate whether the companies are doing well with their current earnings or not.

Don’t think of the quarterly earnings in isolation. ?A good or bad quarterly earnings number conveys information not about the current period only, but about all future periods. ?A bad earnings number?lowers the estimates of all future earnings, telling market players that the long-term efforts of the company are not going to be so great. ?Vice-versa for a good number.

Now, in some cases, that might not be true, and the management team will say, “But we still expect our future earnings to reach the levels that we expected before this quarter.” ?That still leaves the problem of getting to the high future earnings, which if missed will lead the market to reprice the stock down.

They might also use a non-GAAP measure of earnings to explain that earnings are not as bad as they might seem. ?In the short-run the market may accept that, but if you do that often enough, eventually the markets factor in the many “one-time” adjustments, and lower the earnings multiple on the stock to reflect the reduced quality of earnings.

In addition, having shorter-term targets causes corporations to not get lazy in managing expenses and capital. ?When the measurement periods get too long, discipline can be lost.

Quarterly Earnings Don’t Cause Most Firms to Neglect the Long-Term

Firms aren’t interested in only the current period’s earnings, but about the entire future path of earnings. ?Even if?the current period’s earnings meet the estimates, the job is not done. ?If there aren’t plans to grow earnings for the next 3-5 years, eventually earnings won’t meet the expectations of investors, and the price of the stock will fall. ?The short-term is just the beginning of the long-term. ?It is not either/or but both/and. ?A company has to try to explain to investors how it is?growing the value of the firm — if present targets aren’t being met, why should there be any confidence that the future will be good?

Think of corporate earnings like a long-term project which has a variety of things that have to be done en route to a significant goal. ?The quarterly earnings measure?whether the progress toward completing the goal is adequate or not. ?Now, the measure is not perfect, but who can think of a better one?

Ending Quarterly Earnings Would Not?End Activism, Buybacks, and Dividends

I can think of an area in business where earnings estimates don’t play a role — private equity. ?Are the owners long-term oriented? Yes. ?Are they short-term oriented? ?Yes. ?Is?capital managed tightly? ?Very tightly. ?All excess capital is dividended back — it as if activists run the firms permanently.

If there were no quarterly earnings in the public equity markets, firms would still be under pressure to return excess capital to shareholders. ?Activists would still analyze companies to see if they are badly managed, and in need of change. ?If anything, when companies would release their earnings less frequently, the adjustments to the market price of the stock would be more severe. ?Companies that disappoint would find the activists arriving regardless of the periodicity of the release of earnings.

On the Use of Excess Capital

Investing, particularly for the long-term, is not risk-free. ?In an environment where there is rapid technological change, like there is today, it is difficult to tell what investments will not be made obsolete. ?In such an environment, it can make a lot of sense to focus on shorter-term?investments that are more certain as to the success of the project. ?It is also a reason why dividends and buybacks are done, as capital returned to shareholders is associated with higher stock prices, because the capital is used more efficiently. ?Companies that shrink their balance sheets tend to outperform those that grow them.

As an example, large acquisitions tend not to benefit shareholders, while small acquisitions that lead to greater organic growth do tend to benefit investors. ?The same is true of large versus small investments for organic growth away from M&A. ?Most management teams can adequately estimate and plan for the growth that stems from incremental action. Large revolutionary investments are another thing. ?There is usually no way to estimate how those will work out, and whether the prospects are reasonable or not.

In one sense, it’s best to leave those kinds of investment projects to highly focused firms that do only that. ?That’s how biotech firms work, and it is why so many of them fail. ?The few winners are astounding.

Or, think about how progressive Japanese firms were viewed to be in the 1980s, as they pursued long-term projects that had very low returns on equity. ?All of that failed, to a first approximation, while the derided American model of shareholder capitalism prospered, as capital was used efficiently on projects with high risk-adjusted?returns, and not wasted on speculative projects with uncertain returns. ?The same will prove true of China over the next 20 years as they choke on all of their bad investments that yield low returns, if indeed the returns are positive.

Remember, bad investments are just expenses in fancy garb — it just takes the accounting longer to recognize the losses. ?Think of Enron if you need an example, which brings up one more point: good investing focuses on accounting quality. ?Accrual items on the asset side of the balance sheets of corporations get higher valuations the shorter the accrual is, and the more likely it is to produce cash. ?Most long term projects tend to be speculative, and as such, drag down the valuation of the stock, because in most cases, it lowers the long-term earnings of the company.

Conclusion

If quarterly earnings are abolished, intelligent corporations won’t change much. ?Investment won’t go up much, and the time horizon of most management teams will not rise much. ?If you need any proof of that, look at how private equity and large mutual insurers manage their firms — they still analyze quarterly results, and are conservative in how they deploy capital.

The only great change of eliminating quarterly earnings will be a loss of quality information for equity investors. ?Bond investors and banks will still require more frequent financial updates, and equity investors may try to find ways to get that data, perhaps through the rating agencies.

I’m currently reading a book about the life of Jesse Livermore. ?Part of the book describes how Livermore made a fortune shorting stocks just before the panic of 1907 hit. ?He had one key insight: the loans of lesser brokers were being funded by the large brokers, and the large brokers were losing confidence in the creditworthiness of the lesser brokers, and banks were now funding the borrowings by the lesser brokers.

What Livermore didn’t know was that the same set of affairs existed with the banks toward trust companies and smaller banks. ?Most financial players were playing with tight balance sheets that did not have a lot of incremental borrowing power, even considering the lax lending standards of the day, and the high level of the stock market. ?Remember, in those days, margin loans required only 10% initial equity, not the 50% required today. ?A modest move down in the stock market could create a self-reinforcing panic.

All the same, he was in the right place at the right time, and repeated the performance in 1929 (I’m not that far in the book yet). ?In both cases you had a mix of:

High leverage

Short lending terms with long-term assets (stocks) as collateral.

Chains of lending where party A lends to party B who lends to party C who lends to party D, etc., with each one trying to make some profit off the deal.

Inflated asset values on the stock collateral.

Inadequate loan underwriting standards at many trusts and banks

Inadequate solvency standards for regulated financials.

A culture of greed ruled the day.

Now, this is not much different than what happened to Japan in the late 1980s, the US in the mid-2000s, and China today. ?The assets vary, and so does the degree and nature of the lending chains, but the overleverage, inflated assets, etc. were similar.

In all of these cases, you had some institutions that were leaders in the nuttiness that went belly-up, or had significant problems in advance of the crisis, but they were dismissed as one-time events, or mere liquidity and not solvency problems — not something that was indicative of the system as a whole.

Those were the warnings — from the recent financial crisis we had Bear Stearns, the failures in short-term lending (SIVs, auction rate preferreds, ABCP, etc.), Bank of America, Citigroup, credit problems at subprime lenders, etc.

I’m not suggesting a credit crisis now, but it is useful to keep a list of areas where caution is being thrown to the wind — I can think of a few areas: student loans, agricultural loans, energy loans, lending to certain weak governments with large liabilities and no independent monetary policy… there may be more — can you think of any? ?Leave a comment.

Subprime lending is returning also, though not in housing yet…

Parting Thoughts

I’ve been toying with the idea that maybe there would be a way to create a crisis model off of the financial sector and its clients, working off of a “how much slack capital exists across the system” basis. ?Since risky?borrowers vary over time, and some lenders are more prudent than others, the model would have to reflect the different links, and dodgy borrowers in each era. ?There would be some art to this. ?A raw leverage ratio, or fixed charges ratio?in?the financial sector wouldn’t be a bad idea, but it probably wouldn’t be enough. ?The constraint that bind varies over time as well — regulators, rating agencies, general prudence, etc…)

In a highly leveraged situation with chains of lending, confidence becomes crucial. ?Indeed, at the time, you will hear the improvident squeal that they “don’t have a solvency crisis, but just a liquidity crisis! We just need to restore confidence!” ?The truth is that they put themselves in an unstable situation where a small change in cash flows and collateral values will be the difference between life and death. ?Confidence only deserves to exist among balance sheets that are conservative.

That’s all for now. ?Again, if you can think of other areas where debt has grown too quickly, or lending standards are poor, please e-mail me, or leave a message in the comments. Thanks.

Suppose you wanted a comprehensive book on all of the ways that there are to get excess returns from the stock market as a type of value investor (as of year-end 2013), and you wanted it in one slim volume. ?This is that book. ?As with most desires there is the “be careful what you wish for, you just might get it” effect. ?This book is not immune.

At Aleph Blog, I try to write book reviews that always include what sort of reader might benefit from a given book. ?Because this book packs so much into such a small space, it is not a?book for beginners unless they are?prodigies. ?If you are a beginner, better to warm up with something like The Intelligent Investor, by Ben Graham. ?Beginners need time to see concepts described in greater detail, and more slowly.

Though it is a book on value investing, it is expansive in what it considers value investing. ?It includes topics as varied as:

Behavioral Economics

Market-timing from a valuation standpoint

Growth at a reasonable price [GARP] investing

Private investing

Shorting

Event-driven investing

Barriers to considering investments that keep others from buying them at attractive prices

In a book of around 300 pages, this is ambitious. ?It gives you one or two passes over important topics, so you are only getting a taste of the ideas involved. ?This is also predominantly a book on qualitative investing. ?Pure quantitative value investing doesn’t get much play. ?Non-value anomalies don’t get much coverage.

The other?thing the book lacks is a way to pull it all together in a practical way. ?Yes, the last chapter tries to pull it all together, but given the breadth of the material, it gets pulled together in terms of the attitudes you need to do this right, but less of a “how do you structure an overall investment process to put these principles into practical action.” ?Providing more examples could have been useful, and really, the whole book could have benefited from that.

Additional Resources

Now, if you want a greater taste of the book without buying it, I’ve got a deal for you: this is a medium-sized slide presentation that summarizes the book. ?Pretty sweet, huh? ?It represents the book well, so if you are on the fence, I would look at it — after that you would know if you want to buy it.

Full disclosure:?I?received a?copy from the author.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

Pension plan reform has to face three realities.? The first is people don?t know how much to put away for retirement.? I?ll give you a hint: for almost all people, it should be over 10% of your gross pay.? The second is that people don?t know how to invest, so hand it off to advisors who will do it for them, and cheaply.? The third is silent, and leaves a lot of money on the table ? most people would be better off taking an annuity from their pension plan than a third party, or trying to manage a lump sum on their own.? This is usually an option only for defined benefit [DB] plans.

It would be nice if we could give everyone a DB plan, but as I pointed out last time, the costs would be too high. ?DC [Defined Contribution] plans are inexpensive enough, but they have the above three flaws.

Q: How could we get people and firms to save more for retirement?

A: I’m not sure you can. ?Present needs are large for many people, and they can’t imagine saving anything over 3%, much less 10%+ of pay. ?Firms could do more, but it would raise costs, unless it is taken out of other benefits or wages.

A: Think about high school for a moment. ?It’s a very peer conscious part of life for many people. ?How well would an appeal go over asking the bulk of students to behave well, like the best-behaved students in the class?

Q: It might affect a few, but for the most part people are set in their ways. ?They’ve already done their own implicit comparisons, and concluded that they are doing well enough relative to the peers they care about, given the circumstances. ?They also might not like the comparison and say something like, “Fine for them, but I have different realities in my life.”

A:?I think that treats adults like kids. ?If they don’t want to save, let them be. ?They might regret it later, or, they might say, “This is my lot in life. ?I have to take care of what I think is important now, and when I am old, I’ll work if I have to.” ?Also, people have an incredible ability to ignore reality if they need to.

Q: But isn’t there a public policy reason to encourage retirement plans and savings?

A: Most politicians think so, but retirement is a modern concept that with longer lifespans may not make sense in every situation. ?The generation that fought WWII had a unique situation that allowed many of them to retire very comfortably that we don’t have now. ?Productivity increases were larger, the demographics were right, global labor competition was a lot lower, and investment returns were a lot better.

You could look at my piece,?Ancient and Modern: The Retirement Tripod?for more on this. ?As it is, it will be difficult to take care of the Baby Boomers to the same degree that their parents were taken care of — it doesn’t matter how you fund it — it is a humongous claim on GDP, and what will be left for those who are younger?

Q: So, you argue for freedom to choose in contributions, but you don’t argue for it in investing or distributions?

A: Uh, yes. ?The main difference is that I think most people are capable of estimating their tradeoff of money now versus money in the future, and they are implicitly saying they don’t want to retire, regardless of what they say explicitly.

On investing, most people do not know what to do, and I would strip down most DC plans down to a small bunch of blended funds managed by professionals getting paid at low institutional rates. ?There would be at most five funds, ranging from conservative to aggressive, with a default option that adjusts which fund a participant is in based on age.

On distributions, no one, not even professionals, are good at managing a lump sum of money to provide a stream of income. ?Dig the ten reasons for that in this article. ?People are capable of budgeting, so give them a fixed or slowly rising income to live off of, while investing their slack assets to cover future increases in costs.

Q: It seems inconsistent to me.

A:?I’m just trying to be realistic about what people are capable of doing, and what their needs are.

I don’t think it is wise to entrust so much of the investing in the economy to a single entity. ?Backdoor socialism is a real risk here. ?Nor is it wise to fund the government via pensions. ?Note how well the government did with Social Security. ?It would be one thing if the government had used the money to improve infrastructure, but the money was generally spent on current consumption.

Q: The CFA Institute has put out their own plans for an Ideal Retirement System. ?Wouldn’t that be a good idea?

A: When I was a kid, one of my friends would say to me, “If wishes were fishes, we’d all have a big fry.” ?Like giving everyone?a strong DB plan — it fails the cost test. ?You could start doing this for a new group of retirees that would retire in the 2060s and beyond, but it is unrealistic for the present cohorts looking to retire sooner that have not saved enough individually or corporately.

Q: This is pretty dour. ?Don’t you have anything encouraging to say here?

A: I would note that elderly people tend to be happier than younger people. ?Some of it is coming to terms with life, grasping that many of the things that we aimed for when we were younger weren’t worth it, and taking some satisfaction in what good you have in the present. ?It’s not all money based, but certainly money helps. ?Some will look back at the past and say they did what was best for all their responsibilities. ?Others may regret missed opportunities.

There may be some good that comes out of the American tendency toward voluntarism. ?Who knows what elderly Baby Boomers might do when they put their mind to it? ?Hopefully it won’t be voting more money for themselves from the public purse.

Q: Any final advice?

A: You are you own best guardian of your own retirement. ?I encourage you to:

Save what you can. ?This is one factor you can control.

On the home front, I have been doing more basic financial counseling than usual, and I’ve had some say to me that it would be hard to build a buffer of 3-6 months of expenses. ?If that is true of you, I would encourage you to build a smaller buffer of one month’s wages. ?Why?

A change to good habits rarely happens immediately. ?You gotta walk before you can run.

Psychological changes happen slowly, and there is a mental reward to achieving a smaller, interim goal.

The idea of living off of last month’s paycheck is a simple one.

Contra Aristotle, money is not sterile. ?It tends to beget more money, once you pass a certain threshold. ?Why?

There are discounts for upfront payment on large purchases, but the biggest reason is that once you get used to living on less than your full income, and living off of the buffer fund, there is a tendency for the buffer to grow. ?You have begun to master a key concept:

Money has importance?tomorrow that is more valuable?than spending on purchases of trivial importance today.

I’m surprised at how money burns a hole in the pocket of so many people. ?Spend down to the last dollar in the pocket and then some. ?No wonder the credit card companies are so big and profitable.

I have another article coming up on this, but it is critical to basic financial management that you place importance on the ability to meet future needs with greater certainty. ?Thus the need for the buffer, which implies saying “no” to low value and low priority spending.

It’s not a question of the intellect usually, but of the will. ?When will you start making money your servant, rather than serving it? ?Go build the buffer, even if it is small. ?In time, with increased will power on your part, it will grow.