One of the challenges of fundamental investing is trying to find decent ideas that are off the radar. There are a number of ways to try to do that by looking at:

smaller foreign companies

companies that have made some significant losses.

companies where the relative performance is so awful that no?manager benchmarked to an index would dare touch the company.

small companies with modest?insider buying.

companies in boring industries that you know can’t have any significant growth. ?(This excludes “buggy whip” industries.)

companies where insiders own so much of the company, that it can’t easily be taken over.

complex companies that are difficult to understand.

Okay, tall order. ?That said, I’ll do a few articles over the next two months that try to unearth companies that might be suitable candidates for analysis. ?Tonight’s article follows up on what I wrote in my last article, where I said:

Sometimes I like to run a screen for?stocks have done badly over the last four years, but have begun to outperform over the last year. ?This can point out areas that are still ignored by most of the market, but where trend may have shifted. ?I?ll post that screen after my software has its weekly update on Saturday.

I’m going to show you the list, with some additional data to give some context, but remember this: the only reason these stocks are here is that they underperformed the market massively for the last four years, and have had a turn in performance in the last year. ?Anyway, here is the list:

I’ve been analyzing stocks for over 20 years… out of the 49 companies listed here, I recognize 24 of them. ?I own none of them at present, though I have owned four?of them in the past [AKS, DYN, TNP & YRCW]. ?That said, four years of lousy relative performance likely means that few are actively looking at these companies.

As with any analysis on the internet, purchasing or selling shares of companies like this is?at your own risk. ?I’m planning on looking through this list for ideas, and if I find one good enough to buy for my clients and me, I will do a write-up after we have established our position.

In order to get there, I would have to be satisfied about a number of things regarding any one of these companies:

What went wrong over the last four years?

Has management fixed what was wrong? ?(Or, is there a new management with better ideas?)

Is the business adequately capitalized?

Is the accounting likely honest/conservative?

Do they have a?large?area where they can earn money sustainably, or are they up against stronger competition almost everywhere?

If they are in a tough industry, are they one of the few that could survive if conditions got markedly worse?

Does management seem intelligent in using excess cash?

The question is to look for a margin of safety, and then see whether the company will earn a return on its business that is attractive at your entry price. ?This is a challenge, but maybe one or two companies out of 49 could make it.

I’m going to show you two portfolios — I’m not initially going to tell you much about either one, but then you can consider which one you might like better. ?Here’s portfolio A:

And here is portfolio B:

There is one obvious difference in the two portfolios: portfolio B has gone up more than portfolio A in the past year. ?But the hidden story is that portfolio A’s stocks have had price returns of -85% or worse over the past four years, whereas portfolio B’s stocks have has price returns of 1000% or better. ?They are the only stocks with current market caps of over $100 million that meet those criteria.

Now, which one would you choose, if you had to hold one portfolio for the next year? The next four years?

Oddly, the right answer might be portfolio A. ?Currently, I am reading through a book called Deep Value, which I will review in a week or two, and they cite in Chapter 5 some research by Thaler and De Bondt which indicates that portfolios that have gone through extreme failure tend to outperform portfolios?that have gone through extreme?success.

Though the momentum anomaly (weak as it has been recently) usually favors portfolios with stronger price momentum, the relationship breaks down over longer periods of time, and more severe moves, where mean-reversion tends to take over. ?One thing that I can tell looking at the two portfolios — the expectations are a lot, lot higher for portfolio B than portfolio A. ?Things only have to stop getting worse for there to some positive price action there.

Sometimes I like to run a screen for?stocks have done badly over the last four years, but have begun to outperform over the last year. ?This can point out areas that are still ignored by most of the market, but where trend may have shifted. ?I’ll post that screen after my software has its weekly update on Saturday. ?Until then.

PS — as an aside, it will be fun to review the relative performance of these portfolios.

The dirty truth is that some investments in this life are sold, and not bought. ?The prime reason for this is that many people are not willing to learn enough to save and invest on their own. ?Instead, they rely on others to corral them and say, “You ought to be saving and investing. ?Hey, I’ve got just the thing for you!”

That thing could be:

Life Insurance

Annuities

Front-end loaded mutual funds

Illiquid securities like Private REITs, LPs, some Structured Notes

Etc.

Perhaps the minimal effort necessary to avoid this is to seek out a fee-only financial planner, and ask him to set up a plan for you. ?Problem solved, unless…

Unless the amount you have is so small that when look at the size of the financial planner’s fee, you say, “That doesn’t work for me.”

But if you won’t do it yourself, and you can’t find something affordable, then the only one that will help you (in his own way) is a commissioned salesman.

Now, to generate any significant commission off of a financial product, there have to be two factors in place: 1) the product must be long duration, and 2) it must be illiquid. ?By illiquid, I mean that either you can’t easily trade it, or there is some surrender charge that gets taken out if the contract is cashed out early.

The long duration of the contract allows the issuer of the contract the ability to take a portion of its gross margins over life of the contract, and pay a large one-time commission to the salesman. ?The issuer takes no loss as it pays the commission, because they spread the acquisition cost over the life of the contract. ?The issuer can do it because it has set up ways of recovering the acquisition cost in almost all circumstances.

Now in some cases, the statements that the investor will get will?explicitly reveal the commission, but that is rare. ?Nonetheless, to the extent that it is required, the first statement will?reveal how much the contractholder would lose if he tries to cash out early. ?(I think this happens most of the time now, but it would not surprise me to find some contract where that does not apply.)

Now the product may or may not be what the person buying it needed, but that’s what he?gets for not taking control of his?own finances. ?I don’t begrudge the salesman his commission, but I do want to encourage readers to put their own best interests first and either:

Learn enough so that you can take care of your own finances, or

Hire a fee-only planner to build a financial plan for you.

That will immunize you from financial salesmen, unless you eventually become rich enough to use life insurance, trusts, and other instruments to limit your taxation in life and death.

Now, I left out one thing — there are still brokers out there that make their money through lots of smallish commissions by trading a brokerage account of yours aggressively, or try to sell you some of the above products. ?Avoid them, and?let your fee-only planner set up a portfolio of low cost ETFs for you. ?It’s not sexy, but it will do better than aggressive trading. ?After all, you don’t make money while you trade; you make it while you wait.

If you don’t have a fee only planner and still want to index — use half SPY and half AGG, and add funds periodically to keep the positions equal sized. ?It will never be the best portfolio, but over time it will do better than the average account.

One final note before I go: with insurance, if you want to keep your costs down, keep your products simple — use term insurance for protection, and simple deferred annuities for saving (though I would buy a bond ETF rather than insurance in most cases). ?Commissions go up with product complexity, and so do expenses. ?Simple products are easy to compare, so that you know that you are getting the best deal. ?Unless you are wealthy, and are trying to achieve tax savings via the complexity, opt for simple insurance products that will cover basic needs. ?(Also avoid product riders — they are really expensive, even though the additional premiums are low, the likely benefits paid are lower still.)

Somewhat less than three years ago, I wrote two articles on Behemoth stocks [one, two], which I define as stocks with over $100 Billion of market cap. ?Today I want to revisit those stocks, and those that have joined them. ?The last time I wrote, there were 39 of them actively trading on US Exchanges. ?Now there are 61, for a difference of 22. ?24 stocks are new, and two?have dropped out. ?Let start with those two:

Vodapone plc [VOD] sold off its interest in Verizon Wireless to Verizon, creating a lot of value, and returned a lot of capital to shareholders. ?For those of us who were shareholders, I can only say, great job. ?You made Verizon pay up, and you didn’t blow all of the new free capital on suboptimal projects.

The stock price of Vale, SA [VALE] has gone down considerably (~40%). ?China is no longer a giant vacuum cleaner for minerals The pace of China’s expansion has slowed, and that has had an impact on base metals producers like Vale.

This highlights three things:

In a bull market, once you are big, you tend to stay there.

If you want to create value for shareholders as a behemoth, you need to take radical actions that sell off parts of the company, and return capital to shareholders. ?Managements should think, “How can we reorganize the company such that each component part will be better managed, and lines that we aren’t so good at are sold off.”

In general, these companies are too large to be taken over; change must come from within. ?Activists will only succeed if the managements let them.

Now let’s look at the new companies, which fall into six main groups: Consumer Oriented, Banks,?Pharmaceuticals,?Information Technology,??Industrials, and??Internet.

Consumer Oriented

Anheuser Busch Inbev SA (ADR) [BUD]

British American Tobacco PLC [BTI]

Comcast Corporation [CMCSA]

Home Depot, Inc. [HD]

Visa Inc [V]

Walt Disney Company [DIS]

Banks

Banco Santander, S.A. (ADR) [SAN]

Bank of America Corp [BAC]

Citigroup Inc [C]

Royal Bank of Canada [RY]

Westpac Banking Corp (ADR) [WBK]

Pharmaceuticals

Amgen, Inc. [AMGN]

Bayer AG (ADR) [BAYRY]

Gilead Sciences, Inc. [GILD]

Sanofi SA (ADR) [SNY]

Information Technology

Cisco Systems, Inc. [CSCO]

QUALCOMM, Inc. [QCOM]

Taiwan Semiconductor Mfg. Co. [TSM]

Industrials

Siemens AG (ADR) [SIEGY]

United Technologies Corp [UTX]

Volkswagen AG (ADR) [VLKAY]

?Internet

Amazon.com, Inc. [AMZN]

Facebook Inc [FB]

?Energy

China Petroleum & Chemical Corp [SNP]

Most of these stocks have become Behemoths as a result of rising earnings and expanding P/E multiples amid the bull market. ?A few, like Facebook and Amazon don’t require much in the way of earnings to support their stock price versus something like an Apple or a Google. ?But let me show you my summary graph regarding now and three years ago for Behemoth stocks:

Three years ago, 2011-13 earnings were estimated, versus 2014-16 earnings today. ?If you look at 2008-10, you can see the impact of the new stocks on the median P/E of the group as a whole. ?In general, the P/Es of the new Behemoth stocks were higher than those that were already Behemoths three years ago, pulling the median at least one multiple turn higher.

And looking at 2011-13 estimated versus the actual, you can see how much valuations have increased over that period. ?It didn’t happen all at once, but the S&P 500 is ~60% higher now than when I wrote the first two pieces (not counting dividends).

In December 2011 you could consider getting 9-10% earnings yields out of the Behemoths. ?Today, you’re looking at 7%. ?Quite a difference. ?Some of it could be attributed to tighter yield spreads, but not to changes in Treasury yields, which are actually higher now than they were in December 2011.

You aren’t as well-compensated today relative?to BBB corporate yields to play in the Behemoth stocks today. ?Now, the Behemoths may be safer than many other stocks in the market, and are priced at a discount to the market averages, but your absolute margin of safety is lower.

What Can Behemoth Stocks do for You?

They can pay you dividends. ?They have relatively protected market niches, and they pay above average dividends — 2.9% on average, and that is with seven that have dividends of less than 1%.

They can go down less than other stocks whenever the next bear market?hits.

What Can’t Behemoth Stocks do for You?

They can’t grow as rapidly as smaller companies.

They can’t be taken over, so improvements from entrenched management teams must come from sweet reason convincing them, rather than barbarians at the gates.

What Could Behemoth Stocks do for You, if Management Teams were Willing to Take Some Chances?

These ideas aren’t likely, because those that manage Behemoth companies like managing these monstrosities, but if they did consider shareholders first:

Energy companies would split into upstream, midstream, refining?and retail companies.

Conglomerates would divide into more focused companies.

Large financial companies would split into companies focused on serving specific markets, realizing that there are few advantages from diversification, and much loss from lack of focus.

Companies would segment into slow-growing legacy businesses which can be reliable income vehicles, and the rapidly-growing portions that could be amazing with some focus.

Frito-Lay would spin off Pepsi.

Procter and Gamble and GE would be even more aggressive about spinning off entities.

The main problem with Behemoths is that they are undermanaged. ?There is only so much a single senior management team can do; the incentives of management teams get rather dull with respect to each division. ?Even the radical decentralization of Berkshire Hathaway can only do so much; a day will come when they will centralize, reorganize and prune, but not while Warren Buffett still leads.

As for me and my clients, we own six of the cheaper Behemoth stocks, comprising ?14% of our holdings, biding our time until I?see better opportunities.

Full Disclosure: Long BRK/B, BP, CVX, SNP, TOT, and WFC

Starting again with another letter from a reader, but I will just post his questions in response to this article:

1)?How much emphasis do you put on the credit cycle? I guess given your background rather a great deal, although as a fundamentals guy, I imagine you don?t try and make macro calls.

2) ?What sources do you look at to make estimates of the credit cycle? Do you look at individual issues, personal models, or are there people like Grant?s you follow?

3) Do you expect the next credit meltdown to come from within the US (as your article suggests is possible) or externally?

4)?How do you position yourself to avoid loss / gain from a credit cycle turn? Do you put more?emphasis?on?avoiding loss or looking for profitable speculation (shorts or quality)

1) I put a lot of emphasis on the credit cycle. ?I think it is the governing cycle in the overall economic cycle. ?When some sector of the economy finds itself under credit stress, it has a large impact on stocks in that sector and related areas.

The problem is magnified when that sector is banks, S&Ls and other lending enterprises. ?When that happens, all of the lending-dependent areas of the economy tend to slump, especially those that have had the greatest percentage increase in debt.

There’s a saying among bond managers to avoid the area with the greatest increase in debt. ?That would have kept you out of autos in the early 2000s, Telecoms after that, and Banks/Finance heading into the Financial Crisis. ?Some suggest that it is telling us to avoid the junior energy names now — those taking on a lot of debt to do fracking… but that’s too small to be a significant crisis. ?Question to readers: where do you see debt rising? ?I would add the US Government, other governments, and student loans, but where else?

2) I just read. ?I look for elements of bad underwriting: loosening credit standards, poor collateral, financial entities focused on growth at all costs. ?I try to look at credit spread relationships relative to risks undertaken. ?I try to find risks that are under- and over-priced. ?If I can’t find any underpriced risks, that tells me that we are in trouble… but it doesn’t tell me when the trouble will hit.

I also try to think through what the Fed is doing, and think what might be harmed in the next tightening cycle. ?This is only a guess, but I suspect that emerging markets will get hit again, just not immediately once the FOMC starts tightening. ?It may take six months before the pain is felt. ?Think of nations that have to float short-term debt to keep things going, particularly if it is dollar-denominated.

I would read Grant’s… I love his writing, but it costs too much for me. ?I would rather sit down with my software and try to ferret out what industries are financing with too much debt (putting it on my project list…).

3) At present, I think that an emerging markets crisis is closer than a US-centered crisis. ?Maybe the EU,?Japan, or China will have a crisis first… the debt levels have certainly been increasing in each of those places. ?I think the US is the “least dirty shirt,” but I don’t hold that view strongly, and am willing to be challenged on that.

That last piece on the US was written about the point of the start of the last “bitty panic,” as I called it. ?For a full-fledged crisis in US corporates, we need the current high issuance of??corporates to mature for 2-3 years, such that the cash is gone, but the debts remain, which will be hard amid high profit margins. ?Unless profit margins fall, a crisis in US corporates will be remote.

4) My goal is not to make money off of the bear phase of the credit cycle, but to lose less. ?I do this because this is very hard to time, and I am not good with Tactical Asset Allocation or shorting. ?There are a lot of people that wait a long time for the cycle to turn, and lose quite a bit in the process.

Thus, I tend to shift to higher quality companies that can easily survive the credit cycle. ?I also avoid industries that have recently taken on a lot of debt. ?I also raise cash to a small degree — on stock portfolios, no more than 20%. ?On bond portfolios, stay short- to intermediate-term, and high to medium high quality.

In short, that’s how I view the situation, and what I would do. ?I am always open to suggestions, particularly in a confusing environment like this. ?If you’re not puzzled about the current environment, you’re not thinking hard enough. 😉

One of the best things for me regarding blogging are the readers who ask me questions. ?When I get a set of them that are general enough, I answer them for all my readers, after stripping out identifying data. ?Here is the most recent:

Thank you for your work on your blog which I read with great interest!

I would have a question for you regarding private equity vs. public traded stocks:

– Does a private investor who is investing/saving for?retirement?need?private equity investments?

– Does such an investor make a big mistake if only investing in publicly traded stocks?

– Do you also invest in private equity?

– Is there any evidence that private equity is outperforming simple passive index investing?

?Many thanks for your time and all the best.

Before I answer the questions, let me take a step backward, and be a little more general, asking a few questions of my own:

1) If you wanted to invest in private equity, how would you do it?

2) What are some of the disadvantages and advantages of investing in private equity?

3) Why don’t?amateur investors invest in just a few public stocks?

Okay, here goes:

If you wanted to invest in private equity, how would you do it?

There are two ways to do it, and I have done each one in my life:

a) invest in a private equity fund

b) invest in a friend’s business

I’m going to ignore the new phenomenon of crowdsourcing, because it is too new to evaluate. ?Wait for it to mature before committing funds.

Now, investing in a private equity fund usually requires being an accredited investor, because the legal form is that of a limited partnership, and those who invest in that are supposed to be sophisticated investors who can afford to lose it all.

Now, in my days of working inside insurance companies, late in?the ’90s, it was all the rage for life insurers to invest in private equity funds. ?I remember being brought in to vet deals after my boss had informally set his heart on doing them. ?As you might guess, I was not too crazy about a tech-heavy fund that was investing in dot-coms, still, we ended up doing it. ?I liked better a?private equity fund that was investing in small and medium-sized ordinary businesses in the Mid-Atlantic region.

We invested in both of them; neither one ended up returning the capital to the insurance company. ?Just because?the institution?is big enough to be a Qualified Institutional Buyer does not mean that it has?the smarts to actually evaluate the risks taken?on. ?Similarly, just because you are an “Accredited Investor” doesn’t mean you are capable of evaluating the risks you will be taking. ?All it means is that the government won’t stand in the way of you losing money that they keep the little guys from losing.

As for investing in a friend’s business, I have done it twice, and so far, seemingly successfully with each: Wright Manufacturing and Scutify. ?You don’t have to be accredited to be an angel investor, but it can be a take it as it comes sort of thing if you don’t live in an area where lots of new ventures get created.

In these situations, it is?good if you bring more than capital to the table. ?Particularly with Wright Manufacturing, I have tried to make my help available when needed when the firm has faced challenges.

What are some of the disadvantages and advantages of investing in private equity?

Disadvantages

Illiquid — in a fund, you are locked up for years. ?Investing in a friend’s business means you are at the mercy of the firm and other shareholders if you want to buy more or sell some. ?If you think bid/ask spreads for illiquid public stocks are wide, they are narrow compared to owning shares in a private business.

The management has information advantages, whether it is the fund or the friend’s business.

The variability of results is very high, with many investments being total losses. ?As true of public equities, don’t invest what you can’t afford to lose.

Your friend may try to raise capital at times where you can’t or don’t want to participate.

You may not get the same amount of data to analyze as with a public company; then again, you may get the inside scoop.

Advantages

The fund could have genuine professionals sourcing business prospects otherwise unavailable to most for investment.

Your friend could really be onto something big.

There is the remote possibility of hitting a home run and making a return many times greater than your capital.

Sometimes there are tax advantages (say, for creating manufacturing jobs in Maryland).

Stock prices are not posted for you, and so you don’t panic so easily, and after all, you would have a hard time selling.

Why don’t?amateur investors invest in just a few public stocks?

Most amateur investors are not good enough at business to find a few superior?businesses and hang onto only those. ?Don’t feel bad, though, that’s true of almost all professionals. ?Diversification is the only free lunch in the business,?because it reduces the variability of returns. ?If you think investors do badly panicking with diversified funds as in 2008-9, if they were only holding a few companies, the volatility would be so great that many more would lose confidence.

The upshot here is that the results of own shares in just a few private companies will vary tremendously; most people will not be able to live with that level of variability,?lack of liquidity, and lack of control.

So, onto my reader’s?questions:

Do you also invest in private equity?

I have done so, as I have said, but most of my investments are in public equities following my own strategies. ?My?asset allocation would look something like this:

Public equities 55%

Private equities 15%

House 15%

Bonds & cash 15%

No debt

Does a private investor who is investing/saving for?retirement?need?private equity investments?

Need it? No. ?Could you use it if accredited, or investing in the businesses of friends? Yes.

Does such an investor make a big mistake if only investing in publicly traded stocks?

No. ?Think of it this way — private equity tends to do about as well as leveraged index funds, on average. ?A portfolio of private equity and bonds will do about as well as some equity index funds, on average, with a much wider degree of variation than the index funds.

As an aside, to two private firms in which I hold shares carry little debt. ?That lowers my risk.

Is there any evidence that private equity is outperforming simple passive index investing?

It does better in good times on average, and worst in bad times, and is far more variable. ?One note, be careful about some of the Internal Rate of Return [IRR] figures that some private equity funds trot out. ?The returns are overstated because the capital is drawn on slowly, which inflates the IRR. ?That said, investors have to plan for that capital to be drawn, and must have some slack assets earning less to fund the later draws on capital. ?If that cost were factored in, the IRR would go down considerably.

In Closing

If I were talking to an amateur investor who wanted to run a concentrated portfolio of value stocks in the public markets, I would say, learn a lot, and put in enough time to make it a second job. ?The same would be more true for the fellow attempting to do the same thing in private equity — it is harder.

If I were talking with an amateur investor trying to find a very good?mutual fund manager or registered investment adviser [RIA] for his funds, I would tell him to look carefully for active share, is?the process sensible and repeatable, etc. ?If he were accredited, and wanted to do the same for private equity, I would be inclined to tell him to hire a specialist consultant to find it for him, because the data is not as available, and the games are more opaque. ?Add in that the big, respected names stick with institutions as clients — smaller amounts of money will have to find a good manager that is also off the beaten track.

So no, there is no advantage to private equity after taking into account the disadvantages. ?Both of my investments have had more than their share of ups and downs; I don’t think the average person is made for that.

Ordinarily, I read all of the books that I review, but when I don’t, I tell my readers. This book I started to read, but I found it so dry that I started skimming it. It’s not that I don’t know the material; it is that I do know it.

The book covers most areas of behavioral finance, however, it does it in an academic way. ?The book would be ideal for academics and those that appreciate an academic approach to finance, that want to have a taste of many different areas of behavioral finance.

?When I review books, I try to say who it would be good for — in this case, it is academics. ?Let average market participants seek elsewhere for more engaging content. ?If you still want to buy it, you can buy it here:?Investor Behavior: The Psychology of Financial Planning and Investing.

Full disclosure: The PR flack?asked me if I would like a copy and I said ?yes.?

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

?It ain?t what you don?t know that hurts you, it?s what you know that ain?t so.?

(Attributed to Mark Twain, Will Rogers,?Satchel Paige, Charles Farrar Browne,?Josh Billings,?and a number of others)

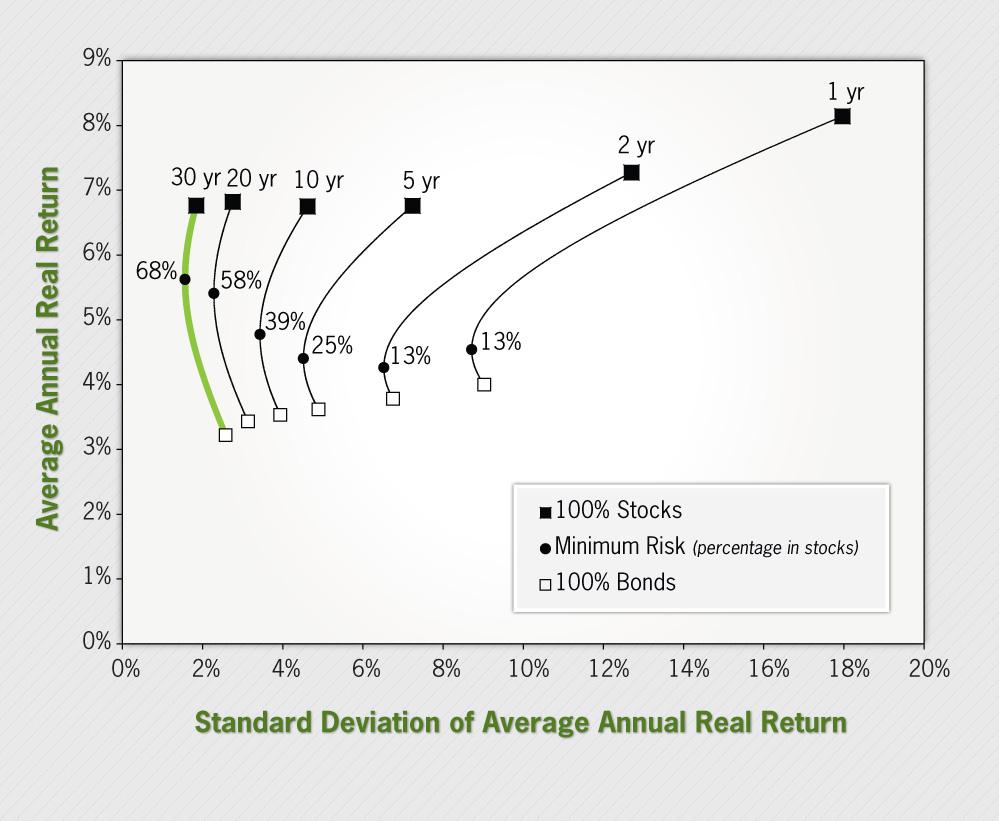

A lot of what passes for investment knowledge is history-dependent, and may not serve us well in the future. ?Further, a certain amount of it is misinterpreted, or, those writing about it, even really bright people, don’t understand the hidden assumptions that they are making. ?I’m going to clarify this by commenting on three graphs that I have seen recently — two that I think deceive, and one that I think is accurate. ?Let’s start with one of the two, which come from this article at AAII, interviewing Jeremy Siegel:

Leaving aside the difficulties with the data from 1802-1871, there is an implicit assumption of buying and holding that undergirds these statistics. ?Though the lines look really smooth now in hindsight, for those investing at the time they were often scared to death in bear markets, selling out at the worst possible time, and in bull markets, getting greedy at the worst possible time.

Now one might say to me, “But David, forget what happened to individuals. ?As a group, people must made returns like this, because every buyer has a seller — even if some panicked or got greedy, someone had to take the other side of the trade and benefit.” ?True enough, though I am suggesting that average people can’t live with that much volatility. ?Even if you cut 1929-32 in half by being 50/50 Stocks/Treasury Notes, how many people could live with a 40% downdraft without selling out?

But there is another problem: when does cash enter and exit the stock market? ?Hint: it doesn’t happen via secondary trading.

Cash Enters the Stock Market

An Initial Public Offering [IPO], secondary IPO, or rights offering leads people to give money to a corporation in exchange for new shares.

Employees forgo pay to receive company stock.

Shares get issued to suppliers in lieu of cash (common with scammy promoted stocks)

Warrants get exercised, and new shares are issued for the price of cash plus warrants.

Cash Exits the Stock Market

Cash dividends get paid, and not reinvested in new shares

Stock gets bought back for cash

Companies get bought out either entirely or partially for cash.

I’m sure there are other ways that cash enters and exits the stock market, but you get the idea. ?It means that cash is exchanged with the company for shares, and vice versa, not the trading that goes on every day. ?Now, here’s the critical question: when do these things happen? ?Is it random?

Well, no. ?Like any other thing in investing, n one is out to do you a favor. ?New stock tends to be offered at a time when valuations are high, and companies tend to be taken private when valuations are low. ?Thus back in the tech bubble, 1998-2000, a lot of cash got soaked up into companies with dubious valuations and business models. ?With a few exceptions, most lost over 90%+. ?Now consider October 2002. ?How many companies IPO’ed then? ?Very few, but?I remember one, Safety Insurance, that came public at the worst possible moment because it had?no other choice. ?Why else would the IPO price be below liquidation value? ?Great opportunity for those who had liquidity at a bad time.

The upshot is that because stock is issued at times that do not favor new investors, and stock is retired at times that do not favor existing investors, the dollar-weighted?returns for stocks in the above graph are overestimated by 1-2%/year. ?Stocks still beat bonds, but not by as much as one would think.

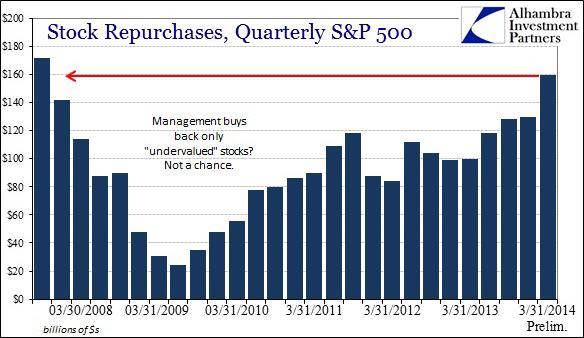

Note that buybacks don’t follow that pattern. ?Corporate managements often exist to justify themselves, and so a great number of them do not behave like value investors when they buy back stock. ?Part of this is that capital seems cheap during the boom phase of the market, and so they lever the company up, issuing debt to buy back stock at high prices. ?It increases earnings in the short-run, but when the bear market comes, the debt hangs ?around, and intensifies the fall in the stock price.

This is why I favor companies that shut off their buybacks at a certain valuation level. ?If they have to dispose of excess cash to avoid takeovers, pay out special dividends… leave the reinvestment issues to shareholders. ?If they buy back stock at levels that are too high, it does not increase the intrinsic value of the firm, though it might keep the price higher for a little while.

What this graph is trying to say is that if you just buy and hold on long enough, results get really, really certain, and investing a lot in stocks reduces your risks, it does not raise your risks.

I’m here to tell you that is an amplification of the past, and maybe not even the best amplification of the past. ?This is where the victors write the history books. ?Your nation is blessed if:

You haven’t had war on your home soil.

There are no plagues or famines

Socialism is kept in check; expropriation is not a risk (note the many countries grabbing pension assets today)

Hyperinflation is avoided (we can handle the ordinary inflation)

Any of those, if bad enough, can really dent a portfolio. ?We can have fancy statistics, and draw smooth curves, but that only says that the future?will be like the past, only more so. 😉 ?I try to avoid the idea that?mankind will avoid the worst outcomes out of self-interest. ?There have been enough cases in history where that has not proven true, and envy and revenge dominate over shared prosperity.

I’ve already made the comment on how many can’t bear with short-run volatility. ?There is another factor: when you look at the above graph, it represents the average valuation level, yield curve shape, etc. ?If you are applying this model to today, where credit spreads are low, cash earns nothing, the yield curve is wide, equity valuations are medium-high, you would have to adjust the expected returns to reflect what the likely outcomes are, and the graph would not look as favorable. ?Volatility looks low today, but realized volatility is likely to be higher, and will not likely follow a normal distribution.

Closing

My main point here is to beware of history sneaking in and telling you that stocks are magic. ?Don’t get me wrong, they are very good, but:

they?rely on a healthy nation standing behind them

their past results are overstated on a dollar-weighted basis, and

their past results come from a prosperous time which may not repeat to the same degree in the future

you may not have the internal fortitude to buy and hold during hard times.

About 1 1/2 years ago, I wrote a seven-part series on investing in insurance stocks. ?It is still a good series, and worthy of your time, because there aren’t *that* many writers freely available on the topic.

This particular article deals expands on part 4 of that series, which deals with insurance reserving. ?I wanted to do this at the time, but I was short on time, and wrote out the general theory there, while not actually doing the time-consuming job of ranking the conservativeness of P&C insurers reserving practices.

Let me quote the two most important sections from part 4:

When an insurance policy is written, the insurer does not know the true cost of the liability that it has incurred; that will only be known over time.

Now the actuaries inside the firm most of the time have a better idea than outsiders as to where reserve should be set to pay future claims from existing business, but even they don?t know for sure.? Some lines of insurance do not have a strong method of calculating reserves.? This was/is true of most financial insurance, title insurance, etc., and as such, many such insurers got wiped out in the collapse of the housing bubble, because they did not realize that they were taking one big nondiversifiable risk.? The law of large numbers did not apply, because the results were highly correlated with housing prices, financial asset prices, etc.

Even with a long-tailed P&C insurance coverage, setting the reserves can be more of an art than science.? That is why I try to underwrite insurance management teams to understand whether they are conservative or not.? I would rather get a string of positive surprises than negative surprises, and you tend to one or the other.

and

What is the company?s attitude on reserving?? How often do they report significant additional claims incurred from business written more than a year ago?? Good companies establish strong reserves on current year business, which depress current year profits, but gain reserve releases from prior year strongly set reserves.

So get out the 10K, and look for ?Increase (decrease) in net losses and loss expenses incurred in respect of losses occurring in: prior years.?? That value should be consistently negative.? That is a sign that he management team does not care about maximizing current period profits but is conservative in its reserving practices.

One final note: point 2 does not work with life insurers.? They don?t have to give that disclosure.? My concern with life insurers is different at present because I don?t trust the reserving of secondary guarantees, which are promises made where the liability cannot easily be calculated, and where the regulators are behind the curve.

As such, I am leery of life insurers that write a lot of variable business, among other hard-to-value practices.? Simplicity of product design is a plus to investors.

Today’s post analyzes Property & Casualty Insurers, and looks at their history of whether they consistently reserve conservatively each year. ? Repeating from above, management teams that reserve conservatively?establish strong reserves on current year business, which depress current year profits, but gain reserve releases from prior year strongly set reserves. ?This should give greater confidence that the accounting is fair, if not conservative.

So, I went and got the figures for “Increase (decrease) in net losses and loss expenses incurred in respect of losses occurring in: prior years,” for?67 companies over the past 12 years from the EDGAR database. ?Today I share that with you.

When you look at the column “Reserving by Year,” that tells you how the reserving for business in prior years went over time. ?A company that was consistently conservative of the past twelve?years would have “12N’ written there for twelve negative adjustments to reserves. ?Using Allstate as an example, the text is “5N, 1P. 3N, 3P” which means for the last 5 years [2013-2009], Allstate had negative adjustments to prior year reserves. ?In 2008, it had to strengthen prior year reserves. ?2007-2005, negative adjustments. ?2004-3,?it had to strengthen prior year reserves.

Now, in reserving, current results are more important than results in the past. ?Thus, in order to come up with a score, I discounted each successive year by 25%. ?That is, 2013 was worth 100 points, 2012 was worth 75, 2011 was worth 56, 2010 was worth 42 points, etc. ?Since not all of the companies were around for the full 12 years, I normalized their scores by dividing by the score of a hypothetical company that was around as long as they were that had a perfect score.

Now, is this the only measure for evaluating an insurance company? ?Of course not. ?All this measures?in a rough way is the willingness of a management team to reduce income in the short-run in order to be more certain about the accounting. ?Consult my 7-part series for more ways to analyze insurance companies.

As an example, imagine an insurance company that consistently writes insurance business at an 80% combined ratio. ?[I.e. 20% of the premium emerges as profit.] ?I wouldn’t care much about minor reserve understatement. ?Trouble is, few companies are regularly that profitable, and companies that understate reserves tend to get into trouble more frequently.

Comments and Surprises

1) Now, it is possible for a company to game this measure in the short run, where the management aims to always release some reserves from prior year business whether it is warranted or not. ?That may have happened with Tower Group. ?Very aggressive in growth, after their initial periods, they consistently released reserves for eight years, before delivering huge reserve increases for two years.

Now, someone watching carefully might have noticed a reserve strengthening for their non-reciprocal business in 2011, and then strengthenings in mid-2012, before the whole world realized the trouble they were in.

2) Notice in the red zone (scores of 40% and lower) the number of companies that did subprime auto insurance — Infinity, Kingsway, and Affirmative. ?That business is very hard to underwrite. ?In the short run, it is hard to not want to be aggressive with reserves.

3) Also notice the red zone is loaded with companies with much recent strengthening of reserves. ?Many of these companies are smaller, with a few exceptions — the law of large numbers doesn’t apply so well with smaller companies, so they mis-estimate more frequently. ?I won’t put companies with less than $1 billion of market cap into the Hall of Shame. ?It’s hard to get reserving right as a smaller company.

4) As for larger companies, they can be admitted to the Hall of Shame, and here they are:

Hall of Shame

AIG

The Hartford

AmTrust Financial Services

Mercury General, and?

National General Holdings

AIG is no surprise. ?I am a little surprised at the Hartford and Mercury General. ?National General Holdings and Amtrust are controlled by the Karfunkels, who are aggressive in managing their companies. ?Maiden Holdings, another of their companies is in the yellow zone.

Final Notes

I would encourage insurance investors to stick to the green zone for their investing, and maybe the yellow zone if the company has compensating strengths. ?Stay out of the red zone.

This analysis could be improved by using prior year reserve releases as a fraction of beginning of year reserves, and then discounting by 25% each year. ?Next time I run the analysis, that is how I will update it. ?Until then!

I’m sure a lot of people have already told you but I want to tell you anyway: Your blog is awesome! I came across The Aleph Blog a couple of months ago and I?m very impressed with your content. I particularly like that 4-part article on Using Investment Advice. I am in the financial industry myself and it makes me wish I came up with the kind of ideas that you have on your blog. Awesome stuff!

Keep up the good work,

Many thanks to the reader, and if you want to read that series, it is located here. ?But when I considered what he wrote to me, it made me think, “Why do we have to tell people how to think about investment advice?”

Then it hit me: because people are looking for easy tips to execute. ?After all, when I wrote the 4-piece series, I had?listening to Jim Cramer in mind. ?The ?tip culture? of inexperienced investors don?t want to learn the ideas behind investing, but just want someone to say, ?Buy this.?? There is little if any guarantee that the same pundit?will ever update his opinion.

We see this on the web, in magazines, newsletters, newspapers, etc. ?On rare occasion, I will print one out, and add it to my “delayed research stack” which means I will look at it in 1-3 months. ?I just did my quarterly clean-out a few days ago — anything I add to the stack now will wait until November.

But why read articles like, “Ten Undervalued Large Cap Stocks with Growth Potential,” “Nine Stocks to Buy and Hold Forever,” “Eight Stocks that are Taking Off, Don’t Miss Out,” “Seven Hidden Gens Among Small Caps,” “Six Stocks for Income and Growth,” “Five Energy Stocks that are Poised to Surge,” Four Titanic Stocks that Every Investor Should Own,” “Three Turnaround Stocks with Potential for Large Capital Gains,” “Two Stocks with Breakthrough Technologies,” and “The One Stock that You Should Own for the Next Decade.”

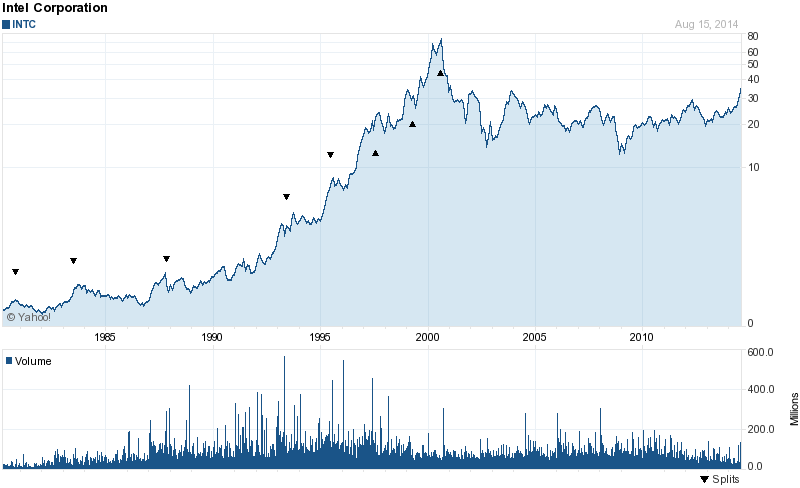

Now, I made those titles up, though the last one was based off a Smart Money article on Intel in late 1999 which came very close to top-ticking ?the market. ?As you can see, Intel still hasn’t made it back to the tech bubble peak.

As I Googled phrases like, “Ten Best Stocks,” it was fascinating to see the range of pitches employed:

Appeals to Buffett (that never gets old)

Best stocks for this year

Favorite stocks of an author, manager or publication

With high dividends

With a low price

In emerging markets

That won’t lose money

That our patented investment screener spat out

For the rest of your life

Etc.

I know that I could get a lot more readers with list articles that tout stocks. ?I don’t do it because most of the articles that you read like that are bogus. ?[I also don’t want the inevitable scad of complaints that come with the territory.) ?So why do such articles?draw readers?

People would rather have false certainty than live in the reality that choosing good investments is difficult. ?Even very good investors hit rough patches where they do not outperform. ?Also, people aren’t comfortable with uncertain horizons for realizing value in investments — article tout holding forever, ten years, one year, but rarely 3-5 years or a market cycle.

The truth is, you can’t tell when a stock will perform, but when it does perform, the results will be lumpy. ?The performance of a stock is rarely smooth. ?During times when the success or failure of a stock idea is realized, the moves are often violent.

Now remember, those who write such articles are looking for media revenue — such articles are sensational, and pander to the desire for easy money. ?But where are the articles telling you to sell ten stocks now? ?(Yes, I know there are some, but they are not so common.) ?Or, where are follow up pieces indicating how well prior picks have done, and whether one should sell, hold, or buy more now?

My main point is this: good amateur investing is like having a part-time job. ?A part-time job, well, takes time. ?Weigh that against other priorities in your life — family, friends, church, public service, fun, etc. ?You may not want a part-time job, and so you can index your investments, or outsource them to a trusted advisor, who hopefully digs up his own ideas, and does not have a consensus, index-like portfolio (If he does, why not index?)

So, avoid tips if you can. ?If you can’t, develop a research discipline, or set them aside like I do, and revisit them when the original reason for buying it is forgotten, and you must evaluate for yourself now. ?The investment that you do not understand why you bought it, you will never know when it is the right time to sell it.

Either learn to evaluate investments on your own, or index your investments, or find a good investment advisor. ?But don’t think that you will do well off of tips.