Dan Primack of Fortune wrote in his daily email:

Saving unicorns from themselves? There was an interesting piece last week from Martin Peers in The Information?(sub req), arguing that the private markets need some sort of shorting mechanism so that there is a check on unreasonable valuation inflation. It would make the market more efficient, Peers argues, even though implementation would require several structural changes (particularly to stock transfer rules). He writes:

“Private companies will probably resist the development of a short-selling market, given it would hurt valuations, which in turn can undermine the value of employee option programs, and give them less control over their shareholder group. But those risks are likely to be outweighed by the long term benefits of bringing more buyers into the market and ensuring the company’s valuation can be sustained outside of the constraints of the private market.”

Leaving out the technical difficulties — including?the lack of ongoing price discovery — one big counter could be that shorts didn’t so much to stop the earlier dotcom bubble (which largely took place in the public markets).

Adam D’Augelli of True Ventures pointed me to a 2002 academic paper (Princeton/London Biz School) that found “hedge funds during the time of the technology bubble on the Nasdaq… were heavily tilted towards overpriced technology stocks.” They add that “arbitrageurs are concerned about attacking the bubble too early without support from their peers,” and that they’re more likely to ride the bubble until just a few months before the end.

That would seem to be?too late to impose price discipline in private markets, but I’m curious in your thoughts. Does some sort of private shorting system make sense? And, if so, how would it be structured?

I’m going to take a stab at answering the final questions. ?There is often a reason why the financial world is set up the way it is, and why truly helpful financial innovations are rare. ?The answer is “no, we should not have any way of shorting private companies, and it is not a flaw in the system that we don’t have any easy way to do it.”

Two notes before I start: 1) I haven’t read the paper at The Information, because it is behind a paywall, but I don’t think I need to do so. ?I think the answer is obvious. ?2) I ran into this question answered at Quora. ?The answers are pretty good in aggregate, but what exists here are my own thoughts to present the answer in what I hope is a simple manner.

What is required to have an effective means of shorting assets

- An asset must be capable of being easily transferred from one entity to another.

- Entities willing to lend the asset in exchange for some compensation over a given lending term.

- Entities willing to borrow the asset, put up collateral adequate to secure the asset, and then sell the asset to another entity.

- An entity or entities to oversee the transaction, provide custody of the collateral, transmit payments, assure return of the asset at the end of the lending term, and gauge the adequacy of collateral relative to the value of the asset.

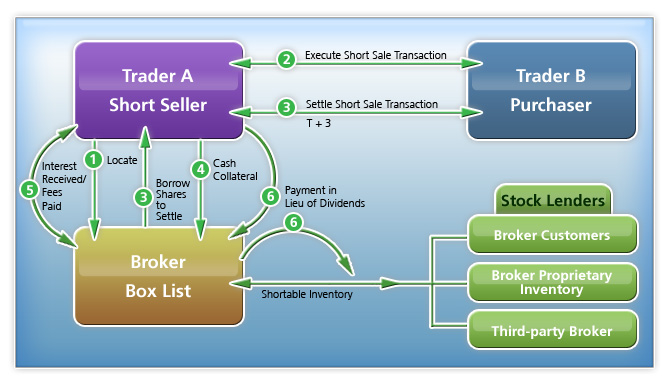

Here’s the best diagram I saw on the internet to help describe it (credit to this Latvian website):

I’m leaving aside the concept of naked shorting, because there are a lot of bad implications to allowing a third party to create ownership interests in a firm, a power which is reserved for?the firm itself.

The Troubles Associated with Shorting Private Assets

I can think of four?troubles. ?Here they are:

- The ability to sell, lend, or buy shares in a private company are limited by the private company.

- Lending over long terms with no continuous?price mechanism to aid in the gradual adjustment of collateral could lead to losses for the lender if the borrower can’t put up additional capital.

- The asset lender can decide only to lend over lending?terms that will likely be disadvantageous to the borrower. ?Getting the asset returned at the end of the lending term could be problematic.

- It is difficult enough shorting relatively illiquid publicly traded assets. ?Liquidity is required for any regular?shorting to happen.

The first one is the killer. ?There are no advantages to a private company to allow for the?mechanisms needed to allow for shorting. That is one of the advantages of being private. ?Information is not shared openly, and you can use the secrecy to aid your competitive edge. ?Skeptical short-sellers would not be welcome.

The second problem is tough, because sometimes?successive capital rounds are at considerably higher prices. ?The borrower will likely not have enough slack assets to increase his collateral, and he will be forced to buy shares in the round to cover his short because of that. ?The lender could find that the borrower cannot make good on the loan, and so the lender loses a portion of the value his ownership stake.

But imagining the first two problems away, problem three would still be significant. ?If the term for lending were not all the way to the IPO, next capital round or dissolution/sale, at the end of the term, the borrower would have to look for someone to sell shares to him. ?It is quite possible that no one would sell them at any reasonable price. ?They know they have a forced buyer on their hands, and there could be informal collusion on the price of a sale.

Perhaps another way to put it is don’t play in a game where the other team has significant control over the rules of the game. ?One of the reasons I say this is from my days of a bond manager. ?There were a lot of games played in securities lending, and bonds?are?not the most liquid place to short assets. ?I remember it being very difficult to get a bond back from an entity that borrowed it, and the custodian and trustee did not help much. ?I also remember how we used to gauge the liquidity of bonds we lent out, and if one was particularly illiquid, we would always recall the bond before selling it, which would often make the price of the bond rise. ?Games, games, games…

What Might Be Better

Perhaps using collateralized options or another type of derivative could allow bets to be taken, if the term extended all the way to the IPO, the next capital round, or dissolution/sale of the company. ?The options would have to be limited to the posted collateral being the most the seller of the option could lose. ?Some of the above four issues would still be in play at various points, but aside from issue one, this would minimize the troubles.

What Might Be Better Still

The value of the shorts is that they share information with the rest of the market that there is a bearish opinion on an asset. ?Short-sellers are nice to have around, but not necessary for the asset pricing function. ?It is not unreasonable to live with the problem that some assets will be overvalued in the intermediate-term, rather than set up a complex method to try to enable shorting. ?As Ben Graham said:

?In the short run, the market is a voting machine but in the long run, it is a weighing machine.?

The weighing machine will do its job soon enough, showing that the overvalued asset will never produce free cash adequate to justify its current high price. ?Is it a trouble?to wait for that to happen? ?If you don’t own it, you shouldn’t care much.

If you want to short it, I’m not sure that will hasten the price adjustment process that much, unless you can convince the existing owners of the asset that it isn’t worth even the current price. ?Given that buyers have convinced themselves to own the asset, because they think it will be worth more in the future, intellectually, convincing them that it is worth less?is a tough sell.

In the end, only asset and liability cash flows count, regardless of what secondary buyers and sellers do. ?Secondary trading does not affect the value of assets, though it may affect the perception of value in the short run. ?Thus, you don’t need short sellers to aid in setting secondary market prices, but they are an aid there. ?In the primary markets, where whole companies are bought and sold, the perceived cash return is all that matters.

Conclusion

Ergo, live with short run overvaluation in private markets. ?It is a high quality problem. ?Sell overvalued assets?if you own them. ?Watch if you don’t own them. ?Shorting, even if possible, is not worth the bother.

One thought on “We Don’t Need To Be Able To Short Private Companies”