=-=-=-=-=-=-=-=-=-

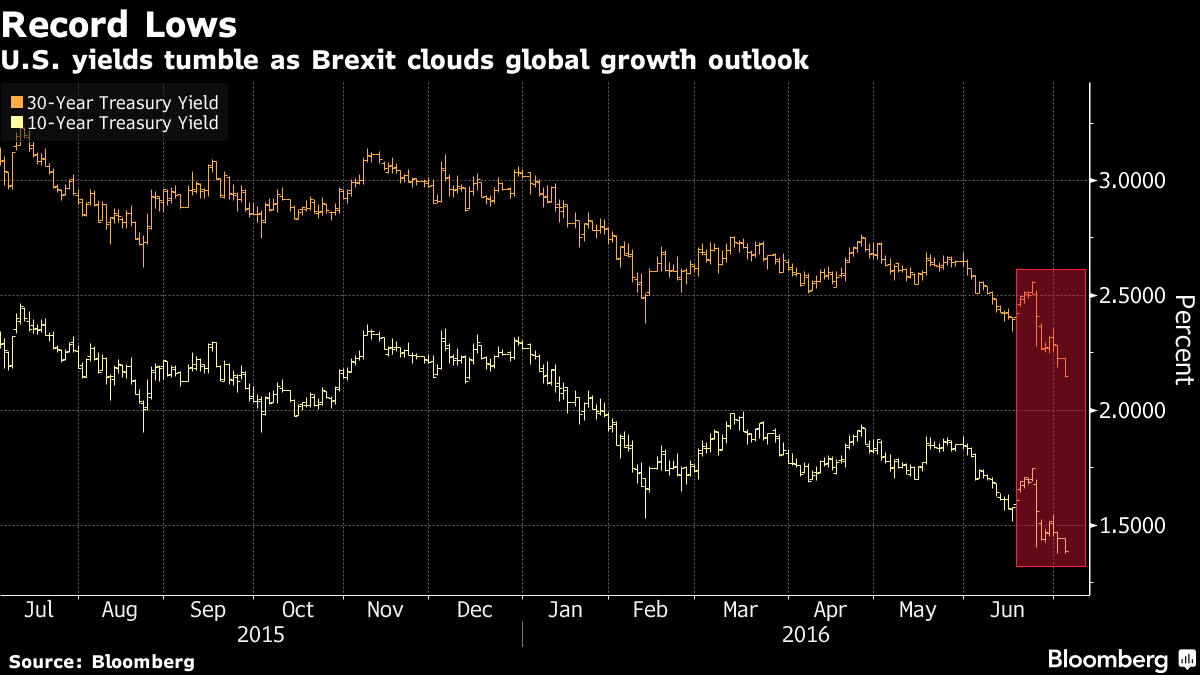

Rates can go lower from here. ?For as long as I can remember, I have been told by many experts that rates can’t go lower, or, that they must go up — there is no way they can go lower. ?I have argued with that idea, as has Hoisington (Lacy Hunt), Gary Shilling and a few others.

Note also that the Fed and most central banks have been on the wrong side of this as well. ?They keep saying that inflation will come, economic activity will pick up,?and that interest rates will rise.

The Fed keeps saying that they will tighten policy. ?I’ll tell you this — with only 0.82% between the yields on 10- and 2-year Treasuries, the Fed is not tightening.

WIth debt levels as high as they are (both government and private), trying to influence economic activity though interest rates is a dumb idea. ?Incenting borrowers to borrow more is difficult, aside from the government — and they rarely do anything with the money that helps produce opportunities for greater economic activity.

We would be better off without “policymakers” trying to “stimulate” the economy, “manage” it, “stabilize” it, etc. ?(But where is the political will to change things — the populace wants easy prosperity, and who is there to tell them to accept a rough world where work and competition is tough, and there is no “Big Daddy” to make life easy? ?The people are the problem. ?The politicians are only a symptom.)

There is one thing that could change this, but it would lay bare the intellectual and moral bankruptcy of what policymakers have been trying to do, which is try to maintain the real value of debt claims while still trying to “stimulate” the economy. ?They could burn away the value of debt claims through an inflation greater than that of the 1970s.

So far, they aren’t willing to do that. ?But their existing policies will prolong the stagnation.

And as such, rates can fall further — with a lot of noise/variation around it.

Central banks and governments are trying to preserve the real value of all or most debt claims – some debt claims should have been written down. One could make the point that central banks are warping the functioning of the market – had they not printed so much money, more debts would have gone bad. Looking at Japan the alternative may be a very long period of stagnation followed by the mother of all sovereign debt crises. When Japan finally does blow up the game will be up for the rest of the developed economies which are already functionally insolvent on a long run basis.

How much farther would they get if they:

– stopped sterilizing reserves by eliminating interest on them, encouraging banks to withdraw reserves and put the money to work in the real economy?

– sold off (or at least stopped re-upping) the balance sheet on the long end, which would presumably cause the market clearing rate of interest to rise, steepening the curve?

Neo-classical economics – which looks at everything as an equilibrium, would argue that these policies (certainly the second one) would be harmful. Media parrot this line, because they are “slaves to a defunct economist”. But I think higher rates might be helpful, ironically. I will explain in a minute.

Seems to me that most of what policymakers are doing is actually a form of bailout for the banks. Banks get guaranteed profits on their reserves, in return for keeping mountains of reserves, thus reducing the interconnectedness of the banks to each other by increasing the interconnectedness to the Fed, which since it has special powers to issue non-interest bearing bearer notes (USD) is theoretically immune from systematic failures…

Nevertheless, I think policy is over-credited as a cause. There is a reason that rates are low – and have been in Japan for decades. Older populations don’t like credit. They also fear outliving their savings, so their intertemporal consumption preferences do not conform to basic logic about the time value of money. In their case, it is essential to *have* income and future assets, not to pull them forward. This has been true at least since “retirement” was invented, tho I guess it was true before as well. What has changed is that there are so many more elderly people trying to have 30 years of permanent 3 day weekends than before. This has been growing since about the same time as interest rates peaked, but has perhaps now reached critical mass, as those born in 1950 and earlier have already made it to “full” retirement age and many near retirees found themselves taking early retirement due to the financial crisis. (Note that all of these problems are similar and in most cases, more acute in other developed countries than in the US, thanks in large part to those Mexicans social conservatives are always complaining about).

Here is why I think higher rates might be good… Higher rates would lower asset prices AND improve reinvestment yields on many securities. This would help older people (they wouldn’t like watching their accounts decline, but their interest payments could be reinvested at higher cash yields which would enable them to have more confidence in their future income and to be more willing to spend. Because of psychology and the intertemporal issues noted above, when cap rates fall, they don’t sell some of their securities to fund consumption. They often save more). Second, it would help younger people, because it would reduce the real cost of housing. This would piss off the upper middle class elite to which policymakers belong, which is why no one campaigns on “lower house prices”. Politicians talk of “affordability” by which they mean – higher prices and more leverage. Note that this strategy, which benefitted older people alot – can only be done once. Lower real housing costs would have a profound benefit on younger people, who now are forced to save (and thereby force down rates) to try and get on the property ladder (and the school credential ladder) and are facing a social democratic welfare state that offered yesterdays aged something for nothing and exploited intertemporal financing options to hide the costs, now saying to them, sorry you get very little for rather alot …

My wife,made the observation last night, interest rates won’t go up until wages do, which is the flip side of inflating away the debt. Inflation only works if there is some way to transmit into wages so people can make good debts with inflated (devalued) cash, inflation without wage increases just increases the misery and political risk. On the other hand, wage increases from increased productivity (backdated to 1980, or when the disconnect happened would also fix the problem. (Personally I’d settle for wages increases for future productivity gains at this point).

Well it’s nice to dream !