This is a small thing, and so this will be a small post.

Learn to set your expectations right.

When you buying something and see a price like $19, $19.95, or $19.99, think $20.

When you are buying a car, and see prices like $19,000, $19,900, $19,990, or $19,999, think $20,000. ?The same thing applies to homes, and be sure you have a strong estimate of all of the extra taxes and fees that will get thrown into the price.

People tend to look at the front number(s) and get mesmerized. ?Learn to round it up as a buyer. ?We tend to get too quick in our judgments, and be too optimistic when we buy, so round prices up — especially true if you are on a budget, and you are keeping a running total of costs.

Now, if you think this doesn’t happen in institutional pricing, it happens there as well. ?I remember cases where I was trying to sell bonds, and I could not get a deal done, I would ask my sales coverage, “Why? How is the other side pricing the bond?” ?If it was a dollar price like $100, I would make a note of it, and if the market fell for general reasons under that price, I would make an offer a little under the price, say $99.95. ?Frequently, I would sell?the bonds for my client, even if the yield spread had worsened in relative terms, and the bonds were less attractive to a more rational buyer. ?The same applied to other means of pricing bonds, and applied the opposite way if I was trying to buy bonds. ?You would be surprised how many were looking for a shiny price like $105, and after a general rally deals would get done at $105.01.

Buffett has sometimes had a phrase, “Your price, my terms.” ?If there are other facets to the deal than merely price, try giving the other guy his price in a prominent way, with other terms that favor what you want to achieve.

You would think that people would be more rational, but they are often not, and you and I aren’t much better. ?That is why I encourage you to think conservatively in your economic decisions to avoid undue optimism.

PS — remember that this happens with institutional investors in setting target prices as well — they like the glossy round numbers.

I will admit, when I first read about the Permanent Portfolio in the late-80s, I was somewhat skeptical, but not totally dismissive.? Here is the classic Permanent Portfolio, equal proportions of:

S&P 500 stocks

The longest Treasury Bonds

Spot Gold

Money market funds

Think about Inflation, how do these assets do?

S&P 500 stocks ? mediocre to pretty good

The longest Treasury Bonds ? craters

Spot Gold ? soars

Money market funds ? keeps value, earns income

Think about Deflation, how do these assets do?

S&P 500 stocks ? pretty poor to pretty good

The longest Treasury Bonds ? soars

Spot Gold ? craters

Money market funds ? makes a modest amount, loses nothing

Long bonds and gold are volatile, but they are definitely negatively correlated in the long run.? The Permanent Portfolio concept attempts to balance the effects of inflation and deflation, and capture returns from the overshooting that these four asset classes do.

What did I do?

I got the returns data from 12/31/69 to 9/30/2011 on gold, T-bonds, T-bills, and stocks.? I created a hypothetical portfolio that started with 25% in each, rebalancing to 25% in each whenever an asset got to be more than 27.5% or less than 22.5% of the portfolio.? This was the only rebalancing strategy that I tested.? I did not do multiple tests and pick the best one, because that would induce more hindsight bias, where I torture the data to make it confess what I want.

I used a 10% band around 25% ( 22.5%-27.5%) figuring that it would rebalance the portfolio with moderate frequency.? Over the 566 months of the study, it rebalanced 102?times. ?At the top of this article is a graphical summary of the results.

The smooth-ish gold line in the middle is the Permanent Portfolio.? Frankly, I was surprised at how well it did.? It did so well, that I decided to ask, what if we drop out the T-bills in order to leverage the idea.? It improves the returns by 1%, but kicks up the 12-month drawdown by 7%.? Probably not a good tradeoff, but pretty amazing that it beats stocks with lower than bond drawdowns. ?That’s the light brown line.

Results

S&P TR

Bond TR

T-bill TR

Gold TR

PP TR

PP TR levered

Annualized Return

10.40%

8.38%

4.77%

7.82%

8.80%

9.93%

Max 12-mo drawdown

-43.32%

-22.66%

0.02%

-35.07%

-7.65%

-14.75%

Now the above calculations assume no fees.? If you decide to implement it using SPY, TLT, SHY and GLD, (or something similar) there will be some modest level of fees, and commission costs.

?What Could Go Wrong

Now, what could go wrong with an analysis like this?? The first point is that the history could be unusual, and not be indicative of the future.? What was unusual about the period 1970-2017?

Went off the gold standard; individual holding of gold legalized.

High level of gold appreciation was historically abnormal.

Deregulation of money markets allowed greater volatility in short-term rates.

ZIRP crushed money market rates.

Federal Reserve micro-management of short-term rates led to undue certainty in the markets over the efficacy of monetary policy ? ?The Great Moderation.?

Volcker era interest rates were abnormal, but necessary to squeeze out inflation.

Low long Treasury rates today are abnormal, partially due to fear, and abnormal Fed policy.

Thus it would be unusual to see a lot more performance out of long Treasuries. The stellar returns of the past can?t be repeated.

Three hard falls in the stock market 1973-4, 2000-2, 2007-9, each with a comeback.

By the end of the period, profit margins for stocks were abnormally high, and overvaluations are significant.

But maybe the way to view the abnormalities of the period as being ?tests? of the strategy.? If it can survive this many tests, perhaps it can survive the unknown tests of the future.

Other risks, however unlikely, include:

Holding gold could be made illegal again.

The T-bills and T-bonds have only one creditor, the US Government. Are there scenarios where they might default for political reasons?? I think in most scenarios bondholders get paid, but who can tell?

Stock markets can close for protracted periods of time; in principle, public corporations could be made illegal, as they are statutory creations.

The US as a society could become less creative & productive, leading to malaise in its markets. Think of how promising Argentina was 100 years ago.

But if risks this severe happen, almost no investment strategy will be any good.? If the US isn?t a desirable place to live, what other area of the world would be?? And how difficult would it be to transfer assets there?

Summary

The Permanent Portfolio strategy is about as promising as any that I have seen for preserving the value of assets through a wide number of macroeconomic scenarios.? The volatility is low enough that almost anyone could maintain it.? Finally, it?s pretty simple.? Makes me want to consider what sort of product could be made out of this.

I delayed on posting this for a while — the original work was done five years ago. ?In that time, there has been a decent amount of digital ink spilled on the Permanent Portfolio idea of Harry Browne’s. ?I have two pieces written:?Permanent Asset Allocation, and?Can the ?Permanent Portfolio? Work Today?

Part of the recent doubt on the concept has come from three sources:

Zero Interest rate policy [ZIRP] since late 2008, (6.8%/yr PP return)

The fall in Gold since late 2012 (2.7%/yr PP return), and

The fall in T-bonds in since mid-2016 (-4.7%?annualized PP return).

Out of 46 calendar years, the strategy makes money in 41 of them, and loses money in 5 with the losses being small: 1.0% (2008), 1.9% (1994), 2.2% (2013), 3.6% (2015), and 4.5% (1981). ?I don’t know about what other people think, but there might be a market for a strategy that loses ~2.6% 11% of the time, and makes 9%+?89% of the time.

Here’s the thing, though — just because it succeeded in the past does not mean it will in the future. ?There is a decent theory behind the Permanent Portfolio, but can it survive highly priced bonds and stocks? ?My guess is yes.

Scenarios: 1) inflation runs, and the Fed falls behind the curve — cash and gold do well, bonds tank, and stocks muddle. ?2) Growth stalls, and so does the Fed: bonds rally, cash and stocks muddle, and gold follows the course of inflation. 3) Growth runs, and the Fed swarms with hawks. Cash does well, and the rest muddle.

It’s hard, almost impossible to make them all do badly at the same time. ?They react differently to?changes in the macro-economy.

Upshot

There are a lot of modified permanent portfolio ideas out there, most of which have done worse than the pure strategy. ?This permanent portfolio strategy?would be relatively pure. ?I’m toying with the idea of a lower minimum ($25,000) separate account that would hold four funds and rebalance as stated above, with fees of 0.2% over the ETF fees. ?To minimize taxes, high cost tax lots would be sold first. ?My question is would there be interest for something like this? ?I would be using a better set of ETFs than the ones that I listed above.

I write this, knowing that I was disappointed when I started out with my equity management. ?Many indicated interest; few carried through. ?Small accounts and a low fee structure do not add up to a scalable model unless two things happen: 1) enough accounts want it, and 2) all reporting services are provided by Interactive Brokers.

Closing

Besides, anyone could do the rebalancing strategy. ?It’s not rocket science. ?There are enough decent ETFs to use. ?Would anyone truly want to pay 0.2%/yr on assets to have someone select the funds and do the rebalancing for him? ?I wouldn’t.

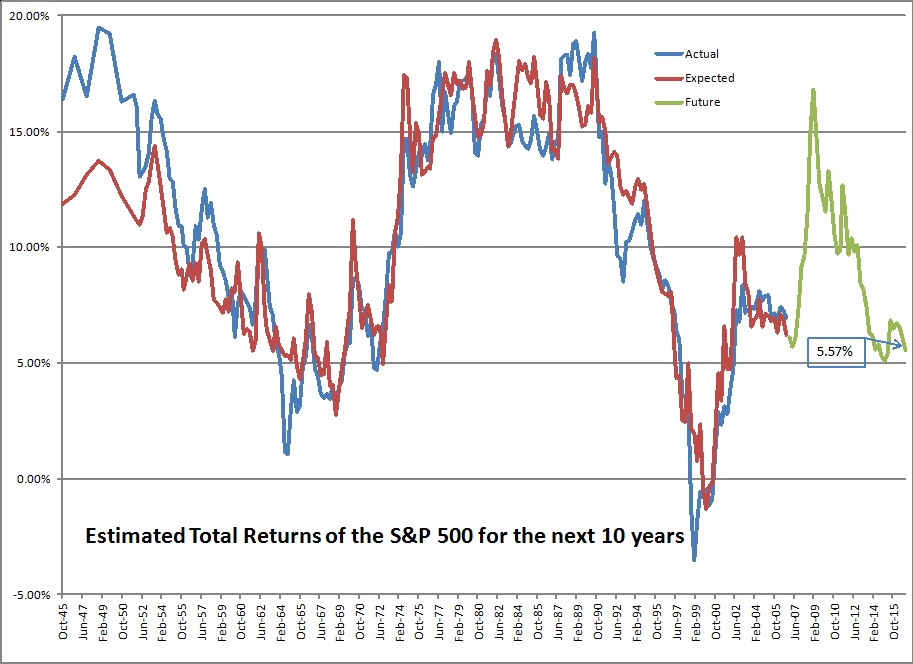

Are you ready to earn 6%/year until 9/30/2026? ?The data from the Federal Reserve comes out with some delay. ?If I had it instantly at the close of the third quarter, I would have said 6.37% ? but with the run-up in prices since then, the returns decline to 6.01%/year.

So now I say:

Are you ready to earn 5%/year until 12/31/2026? ?The data from the Federal Reserve comes out with some delay. ?If I had it instantly at the close of the fourth?quarter, I would have said 5.57% ? but with the run-up in prices since then, the returns decline to 5.02%/year.

A one percent drop is pretty significant. ?It stems from one main factor, though — investors are allocating a larger percentage of their total net worth to stocks. ?The amount in stocks moved from 38.00% to 38.75%, and is probably higher now. ?Remember that these figures come out with a 10-week delay.

Remember that the measure in question covers both public and private equities, and is market value to the extent that it can be, and “fair value” where it can’t. ?Bonds and most other assets tend to be a little easier to estimate.

So what does it mean for the ratio to move up from 38.00% to 38.75%? ?Well, it can mean that equities have appreciated, which they have. ?But corporations buy back stock, pay dividends, get acquired for cash which reduces the amount of stock outstanding, and places more cash in the hands of investors. ?More cash in the hands of investors means more buying power, and that gets used by many long-term institutional investors who have fixed mandates to follow. ?Gotta buy more if you hit the low end of your equity allocation.

And the opposite is true if new money gets put into businesses, whether through private equity, Public IPOs, etc. ?One of the reasons this ratio went so high in 1998-2001 was the high rate of business formation. ?People placed more money at risk as they thought they could strike it rich in the Dot-Com bubble. ?The same was true of the Go-Go era in the late 1960s.

Remember here, that average returns are around 9.5%/year historically. ?To be at 5.02% places us in the 88th percentile of valuations. ?Also note that I will hedge what I can if expected 10-year returns get down to 3%/year, which corresponds to a ratio of 42.4% in stocks, and the 95th percentile of valuations. ?(Note, all figures in this piece are nominal, not inflation-adjusted.) ?At that level, past 10-year returns in the equity markets have been less than 1%, and in the short-to-intermediate run, quite poor.)

You can also note that short-term and 10-year Treasury yields have risen, lowering the valuation advantage versus cash and bonds.

The investors? positioning suggests burgeoning optimism, with TD Ameritrade clients increasing their net exposure to stocks in February, buying bank shares and popular stocks such as Amazon.com Inc. and sending the retail brokerage?s Investor Movement Index to a fresh high in data going back to 2010. The index tracks investors? exposure to stocks and bonds to gauge their sentiment.

?People went toe in the water, knee in the water and now many are probably above the waist for the first time,? said JJ Kinahan, chief market strategist at TD Ameritrade.

This is sad to say, but it is rare for a rally to end before the “dumb money” shows up in size. ?Running a small asset management shop like I do, at times like this I suggest to clients that they might want more bonds (with me that’s short and high quality now), but few do that. ?Asset allocation is the choice of my clients, not me. ?That said, most of my clients are long-term investors like me, for which I give them kudos.

Then there is this piece over at Bloomberg.com called:?Wall Street’s Buzz Over ‘Great Leader’ Trump Gives Shiller Dot-Com Deja Vu. ?I want to see the next data point in this analysis, which won’t be available by mid-June, but I do think a lot of the rally can be chalked up to willingness to take more risk.

I do think that most people and corporations think that they will have a more profitable time under Trump rather than Obama. ?That said, a lot of the advantage gets erased by a higher cost of debt capital, which is partly driven by the Fed, and partly by a potentially humongous deficit. ?As I have said before though, politicians are typically limited in what they can do. ?(And the few unlimited ones are typically destructive.)

Shiller’s position is driven at least partly by the weak CAPE model, and the rest by his interpretation of current events. ?I don’t make much out of policy uncertainty indices, which are too new. ?The VIX is low, but hey, it usually is when the market is near new highs. ?Bull markets run on complacency. ?Bear markets plunge on revealed credit risk threatening economic weakness.

One place I will agree with Shiller:

What Shiller will say now is that he?s refrained from adding to his own U.S. stock positions, emphasizing overseas markets instead.

That is what I am doing. ?Where I part ways with Shiller for now is that I am not pressing the panic button. ?Valuations are high, but not so high that I want to hedge or sell.

That’s all for now. ?This series of posts generates more questions than most, so feel free to ask away in the comments section, or send me an email. ?I will try to answer the best questions.

=========================

Late edit: changed bolded statement above from third to fourth quarter.

I am a fiduciary in my work that I do for my clients. I am also the largest investor in my own strategies, promising to keep a minimum of 80% of my liquid net worth in my strategies, and 50% of my total net worth in them (including my house, etc.).

I believe in eating my own cooking. ?I also believe in treating my clients well. ?I’ve treated part of this in an earlier post called?It?s Their Money, where I describe how I try to give exiting clients a pleasant time on the way out. ?For existing clients, I will also help them with situations where others are managing the money at no charge, no payment from another party, and no request that I manage any of those assets. ?I do that because I want them to be treated well by me, and I know that getting good advice is hard. ?As I wrote in a prior article?The Problem of Small Accounts:

We all want financial advice.? Good advice.? And we want it for free.? That?s why we come to the Aleph Blog, where advice is regularly dispensed, and at no cost.

But? I can?t be personal, and give you advice that is tailored to your situation.? And in my writing here, much as I try to be highly honest, I am not acting as a fiduciary, even though I still make my writings hold to such a standard.

Ugh.? Here?s the problem.? Good advice costs money.? Really good advice costs a lot of money, and is worth it, if you have enough money to spread the cost over.

But when you have a small account, you have a problem in getting advice.? There is no way for someone who is fiduciary (like me) to make money addressing your concerns.? That is why I have a high minimum for investing: $100,000.? With that, I can spend time on clients, even helping them with assets from which I make no money.

What extra things have I done for clients over time? ?I have:

Analyzed asset allocations.

Analyzed the performance of other managers.

Advised on changing jobs, negotiating salary, etc.

Explained the good and bad points of certain insurance companies and their policies, and suggested alternatives.

Analyzed chunky assets that they own elsewhere, aiding them in whether they keep, sell, or sell part of the asset.

Analyzed a variety of funky and normal investment strategies.

Advised on buying a building, and future business plans.

Told a client he was better off reinvesting the slack funds in his business that needed?financing, rather than borrow and invest the funds with me.

Told a client to stop sending me money, and pay down his mortgage. ?(He has since resumed sending money, but he is now debt-free.)

I take the fiduciary side of this seriously, and will?tell clients that want to put a?lot of their money in my stock?strategy that they need less risk, and should put funds in my bond strategy, where I earn less.

I’ve got a lot already. ?I don’t need to feather my nest at the expense of the best interests of my clients.

Over the last six years, around half of my clients have availed themselves of this help. ?If you’ve read Aleph Blog for awhile, you know that I have analyzed a wide number of things. ?Helping my clients also sharpens me for understanding the market as a whole, because issues come into focus when the situation of a family makes them concrete.

So informally, I am more than an “investments only” RIA [Registered Investment Advisor], but I only earn money off of my investment fees, and no other way. ?Personally, I think that other “investments only” RIAs would mutually benefit their clients if they did this as well — it would help them understand the struggles that they go through, and inform their view of the economy.

Thus I say to my competitors: do you want to justify your fees? ?This is a way to do it; perhaps you should consider it.

Postscript

Having some people in an “investment only” shop that understand the basic questions that most clients face also has some crossover advantages when it comes to understanding financial companies, and different places that institutional money gets managed. ?It gives you a better idea of the investment ecosystem that you live and work in.

Comments are always appreciated from readers, if they are polite. ?Here’s a recent one from the piece?Distrust Forecasts.

You made one statement that I don?t really understand. ?Most forecasters only think about income statements. Most of the limits stem from balance sheets proving insufficient, or cash flows inverting, and staying that way for a while.?

What is the danger of balance sheets proving insufficient? Does that mean that the company doesn?t have enough cash to cover their ?burn rate??

Not having enough cash to cover the burn rate can be an example of this. ?Let me back up a bit, and speak generally before focusing.

Whether economists, quantitative analysts, chartists or guys who pull numbers out of the air, most people do not consider balance sheets when making predictions. ?(Counterexample: analysts at the ratings agencies.) ?It is much easier to assume a world where there are no limits to borrowing. ?Practical example #1 would be home owners and buyers during the last financial crisis, together with the banks, shadow banks, and government sponsored enterprises that financed them.

In economies that have significant private debts, growth is limited, because of higher default probabilities/severity, and less capability of borrowing more should defaults tarry. ?Most firms don?t like issuing equity, except as a last resort, so restricted ability to borrow limits growth. High debt among consumers limits growth in another way ? they have less borrowing capacity and many feel less comfortable borrowing anyway.

Figuring out when there is “too much debt” is a squishy concept at any level — household, company, government, economy, etc. ?It’s not as if you get to a magic number and things go haywire. ?People have a hard time dealing with the idea that as leverage rises, so does the probability of default and the severity of default should it happen. ?You can get to really high amounts of leverage and things still hold together for a while — there may be extenuating circumstances allowing it to work longer — just as in other cases, a failure in one area triggers a lot more failures as lenders stop lending, and those with inadequate liquidity can refinance and then fail.

Three?More Reasons to Distrust Predictions

1) Media Effects — the media does not get the best people on the tube — they get those that are the most entertaining. ?This encourages extreme predictions. ?The same applies to people who make predictions in books — those that make extreme predictions sell more books. ?As an example, consider this post from Ben Carlson on Harry Dent. ?Harry Dent hasn’t been right in a long time, but it doesn’t stop him from making more extreme predictions.

2) Momentum Effects — this one is two-sided. ?There are?momentum effects in the market, so it’s not bogus to shade near term estimates based off of what has happened recently. ?There are two problems though — the longer and more severe the rise or fall, the more you should start downplaying momentum, and increasingly think mean-reversion. ?Don’t argue for a high returning year when valuations are stretched, and vice-versa for large market falls when valuations are compressed.

The second thing is kind of a media effect when you begin seeing articles like “Everyone Ought to be Rich,” etc. ?”Dow 36,000″-type predictions come near the end of bull markets, just as “The Death of Equities’ comes at the end of Bear Markets. ?The media always shows up late; retail shows up late; the nuttiest books show up late. ?Occasionally it will fell like books and pundits are playing “Can you top this?” near the end of a cycle.

3) Spurious Math — Whether it is the geometry of charts or the statistical optimization of regression, it is easy to argue for trends persisting longer than they should. ?We should always try to think beyond the math to the human processes that the math is describing. ?What levels of valuation or indebtedness are implied? ?Setting new records in either is always possible, but it is not the most likely occurrence.

Here’s the quick summary of what I will say: People and companies need liquidity. ?Anything where payments need to be made needs liquidity. ?Secondary markets will develop their own liquidity if it is needed.

Recently, I was at an annual meeting of a private company that I own shares in. ?Toward the end of the meeting, one fellow who was kind of new to the firm asked?what liquidity the shares had and how people valued them. ?The board and management of the company wisely said little. ?I gave a brief extemporaneous talk that said that most people who owned these shares know they are illiquid, and as such, they hold onto them, and enjoy the distributions. ?I digressed a little and explained how one *might* put a value on the shares, but trading values really depended on who was more motivated — the buyer or the seller.

Now, there’s no need for that company to have a liquid market in its stock. ?In general, if someone wants to sell, someone will buy — trades are very infrequent, say a handful per year. ?But the holders know that, and most plan not to sell the shares, looking to other sources if they need money to spend — liquidity.

And in one sense, the shares generate their own flow of liquidity. ?The distributions come quite regularly. ?Which would you rather have? ?A bucket of golden eggs, or the goose that lays them one at a time?

Now the company itself doesn’t need liquidity. ?It generates its liquidity internally through profitable operations that don’t require much in the way of reinvestment in order to maintain its productive capacity.

Now, Buffett used to?purchase only companies that were like this, because he wanted to reallocate the excess liquidity that the companies threw off to new investments. ?But as time has gone along, he has purchased capital-intensive businesses like BNSF that require continued capital investment. ?Quoting from a good post at Alpha Architect?referencing Buffett’s recent annual meeting:

Question: ?In your 1987 Letter to Shareholders, you commented on the kind of companies Berkshire would like to buy: those that required only small amounts of capital. You said, quote, ?Because so little capital is required to run these businesses, they can grow while concurrently making all their earnings available for deployment in new opportunities.? Today the company has changed its strategy. It now invests in companies that need tons of capital expenditures, are over-regulated, and earn lower returns on equity capital. Why did this happen?

Warren Buffett?It?s one of the problems of prosperity. The ideal business is one that takes no capital, but yet grows, and there are a few businesses like that. And we own some?We?d love to find one that we can buy for $10 or $20 or $30 billion that was not capital intensive, and we may, but it?s harder. And that does hurt us, in terms of compounding earnings growth. Because obviously if you have a business that grows, and gives you a lot of money every year?[that] isn?t required in its growth, you get a double-barreled effect from the earnings growth that occurs internally without the use of capital and then you get the capital it produces to go and buy other businesses?[our] increasing capital [base] acts as an anchor on returns in many ways. And one of the ways is that it drives us into, just in terms of availability?into businesses that are much more capital intensive.

Emphasis that of Alpha Architect

Liquidity is meant to support the spending of corporations and people who need services and products to further their existence. ?As such, intelligent entities plan for liquidity needs in advance. ?A pension plan in decline allocates more to bonds so that the cash flow from the bonds will fund expected net payouts. ?Well-run insurance companies and banks match expected cash flows at least for a few years.

Buffer funds are typically low-yielding assets of high quality and short duration — short maturity bonds, CDs, savings and bank deposits, etc. ?Ordinary people and corporations need them to manage the economic bumps of life. ?Expenses are up, and current income doesn’t exceed them. ?Got cash? ?It certainly helps to be able to draw on excess assets in a pinch. ?Those who run a balance on their credit cards pay handsomely for the convenience.

In a crisis, who needs liquidity most? ?Usually, it’s whoever is at the center of the crisis, but usually, those entities are too far gone to be helped. ?More often, the helpable needy are the lenders to those at the center of the crisis, and woe betide us if no one will privately lend to them. ?In that case, the financial system itself is in crisis, and then people end up lending to whoever is the lender of last resort. ?In the last crisis, Treasury bonds rallied as a safe haven.

In that sense, liquidity is a ‘fraidy cat. ?Marginal borrowers can’t get it when they need it most. ?Liquidity typically flows to quality in a crisis. ?Buffett bailed out only the highest quality companies in the last crisis. Not knowing how bad it would be, he was happy to hit singles, rather than risk it on home runs.

Who needs liquidity most now? ?Hard to say. ?At present in the US, liquidity is plentiful, and almost any?person or firm can get a loan or equity finance if they want it. ?Companies happily extend their balance sheets, buying back stock, paying dividends, and occasionally investing. ?Often when liquidity is flush, the marginal bidder is a speculative entity. ?As an example, perhaps some emerging market countries, companies and people would like additional offers of liquidity.

That’s a major difference between bull and bear markets — the quality of those that can easily get unsecured loans. ?To me that is the leading reason why we are in the seventh or eighth inning of a bull market now, because almost any entity can get the loans they want at attractive levels. ?Why isn’t it the ninth inning? ?We’re not at “nuts” levels yet. ?We may never get there though, which is why baseball analogies are sometimes lame. ?Some event can disrupt the market when it is so high, and suddenly people and firms are no longer so willing to extend credit.

Ending the article here — be aware. ?The time to take inventory of your assets and their financing needs is before the markets have an event. ?I’ve just completed my review of my portfolio. ?I sold two of the 35 companies that I hold and replaced them with more solid entities that still have good prospects. ?I will sell two more in the new year for tax reasons. ?My bond portfolio is high quality. ?My clients and I are ready if liquidity gets worse.

How would you like a really good model to make money as a money manager? You would? Great!

What I am going to describe is a competitive business, so you probably won’t grow like mad, but what money you do bring in the door, you will likely keep for some time, and earn significant fees.

This post is inspired by a piece written by Jason Zweig at the Wall Street Journal:?The Trendiest Investment on Wall Street?That Nobody Knows About. ?The article talks about interval funds. ?Interval funds hold illiquid investments that would be difficult to sell at a fair price ?quickly. ?As such, liquidity is limited to quarterly or annual limits, and investors line up for distributions. ?If you are the only one to ask for a distribution, you might get a lot paid out, perhaps even paid out in full. ?If everyone asked for a part of the distribution, everyone would get paid their pro-rata share.

But there are other ways to capture assets, and as a result, fees.

Various types of business partnerships, including Private REITs, Real Estate Partnerships, etc.

Illiquid?debts, such as structured notes

Variable, Indexed and Fixed Annuities with looong surrender charge periods.

Life insurance as an investment

Weird kinds of IRAs that you can only set up with a venturesome custodian

Odd mutual funds that limit withdrawals because they offer “guarantees” of a sort.

And more, but I am talking about those that get sold to or done by retail investors… institutional investors have even more chances to tie up their money for moderate, modest or negative incremental returns.

(One more aside, Closed end funds are a great way for managers to get a captive pool of assets, but individual investors at least get the ability to gain liquidity subject to the changing premium/discount versus NAV.)

My main point is short and simple. ?Be wary of surrendering liquidity. ?If you can’t clearly identify what you are gaining from giving up liquidity, don’t make the investment. ?You are likely being hoodwinked.

It’s that simple.

[bctt tweet=”If you can’t clearly identify what you are gaining from giving up liquidity, don’t make the investment.” username=”alephblog”]

A question?from a reader on my recent post Me Too!:

I recently ran across Ed Thorp?s ?Beat the Market.? I find reasonable his idea that you can take on risks that (almost / essentially) cancel each other out. Find assets that are negatively correlated to buy one long and the other short (he did it with stock warrants in the 60?s but when I started looking into that, well, I?m late to that party, so nevermind).

I?m uncomfortable with shorting anyway, so what about going long in everything and rebalancing when the assets get out of whack? Aren?t a lot of the price movements of various assets (cash, bonds, stocks, real estate, precious metals) the result of money flowing towards or away from that asset? If people are, on net, selling their stocks, to what type of asset are they sending the proceeds? I can?t predict where people will stash their money next, but if I own a little of everything, I?m both hedged against prolonged depression of one asset class and aware of what?s gotten ?expensive? and what?s ?cheap? now.

Along these same ?indexing? lines, what do you think of using ALL the sector ETFs (Vanguard has 11) to index each sector and then rebalance among them as they change in value? How would that application of your portfolio rule 7 differ than when applied to individual stocks? Also, do you think it would be subject to the same / similar danger as everyone else ?indexing? as you wrote about above?

My, but there is a lot here. ?Let me try to unpack this.

Paragraph 1: All of the easy arbitrages are gone or occupied to the level where the risks are fairly priced. ?Specialists ply those trades now, and for the most part, they earn returns roughly equal to short-term risky debt. ?They tend to get hurt during financial crises, because at those points in time, fundamental relationships get disturbed because of illiquidity and defaults amid demands for liquidity and safety.

Paragraph 2:?First, rebalancing is almost always a good idea, but it presumes the asset classes/subclasses in question is high quality enough that it will mean-revert, and that your time horizon is long enough to benefit from the mean reversion when it happens. ?Also, it presumes that you aren’t headed for an utter disaster like pre-WWII Germany with hyperinflation. ?Or confiscation of assets in a variety of ways, etc.

Then again, in really horrible times, no strategy works well, so that is not a criticism of rebalancing — just that it is useful most but not all of the time.

Aren?t a lot of the price movements of various assets [snip] the result of money flowing towards or away from that asset?

Back to the basics. ?Money does not flow into or out of assets. ?When a stock trade happens, shares flow?from one account to another, and money flows the opposite direction, with the brokers raking off a tiny amount of cash in the process. ?Prices of assets change based on the relative desire of buyers and sellers to buy or sell shares near the existing prior price level. ?In a nutshell, that is how secondary markets work.

Then, there is the primary market for assets, which is when they were originally sold to the public. ?In this case, corporations offer stocks, bonds, etc. to individuals and institutions in what are called initial public offerings [IPOs]. ?The securities flow from the companies to the accounts of the buyers, and the money flows from the accounts of the buyers to the companies. ?The selling prices of the assets are typically set by syndicates of investment bankers, who rake off a decent-sized chunk of the money going to the companies. ?In this case, yes, the amount of money that people are willing to pay for the assets will dictate the initial price, unless the deal is received so poorly that it does not take place. ?After that, secondary trading starts. ?(Note: this covers 95%+ of all of the ways that assets get to public markets; there are other ways, but I don’t have time for that now. ?The same is true for how securities get extinguished, as in the next paragraph.)

The same thing happens in reverse when companies are bought in entire, either fully and partially for cash, and in the process, cease to be publicly traded. ?The primary and secondary markets complement each other. ?Corporations and syndicates take pricing cues from the levels securities trade at in the secondary markets in order to price new securities, and buy out existing securities. ?Value investors often look at primary markets to estimate what the assets of whole companies are worth, and apply those judgments to where they buy and sell in the secondary markets.

Trying to guess where market players?will raise their bids for assets in secondary trading is difficult. ?There are a few hints:

Valuation: are asset cheap or rich relative to where normalized valuation levels would be for this class of assets?

Changes in net supply of assets: i.e., the primary markets. ?Streaks in M&A tend to persist.

Price momentum: in the short-run (3-12 months), things that rise continue to rise, and vice versa for assets with?falling prices.

Mean-reversion: in the intermediate term (3-5 years), things that currently rise will fall, and vice-versa. ?This effect is weaker than the momentum effect.

Changes in operating performance: if you have insight into companies or industries such that you see earnings trends ahead of others, you will have insights into the likely future performance of prices.

All of these effects vary in intensity and reliability, both against each other, and over time. ?If you own a little of everything, many of these effects become like that of the market, but noisier.

Paragraph 3:?If you want to apply rule 7 to a portfolio of sectors, you can do it, but I would probably decrease the trading band from 20% to 10%. ?Ditto for a portfolio of country index ETFs, but size your trading band relative to volatility, and limit your assets to developed and the largest emerging?market countries. ?With a portfolio of 35 stocks, the 20% band has me trade about 4-5 times a month. ?With 11 sectors your band should be sized to trade 1-2 times a month. ?20 countries, around 3x/month. ?If it is a taxable account set the taxation method to be sell highest tax cost lots first.

Remember that portfolio rule 7 is meant to be used over longer periods of time — 3 years minimum. ?There are other rules out there that adjust for volatility and momentum effect that have done better in the past, but those two effects are being more heavily traded on now relative to the past, which may invalidate the analogy from history to the future.

Using portfolio rule 7 overweights smaller companies, industries, sectors, or countries vs larger ones. ?It will not be as index-like, but it is still a diversified strategy, so it will still be somewhat like an indexed portfolio.

Finally, even if we get to the point where active management outperforms indexing regularly, remember that indexing is still likely to be a decent strategy — the low cost advantage is significant.

That’s all for now, and as always, comments and questions are welcome.

I have sometimes said that it is common for many people to imitate the behavior of others, rather than think for themselves. ?There are several reasons for that:

It”s simple.

It’s fast.

And so long as you don’t run into a resource constraint it works well.

People generally have a decent idea who their smartest friends are, and who seems to give good advice on simple issues. ?If your neighbor says that the new Chinese food place is excellent, and you know he knows his food, there is a very good chance that when you go there that you will get excellent Chinese food as well.

You might even tell your friends about it; after all, you want to look bright as well, and its neighborly to share good information. ?That works quite well until the day that Yogi Berra’s dictum kicks in:

Nobody goes there anymore. It?s too crowded.

The information indeed was free, but space inside the restaurant was not, even if patrons weren’t paying to get in. ?And even if they have carryout, the line could go around the block… a hardship for many even if?you are getting the famous Ocean Broccoli Beef. ?(Warning: Hot in every way.)

Readers of my blog know that the same thing happens in markets. ?Imitation was a large part of the dot-com bubble and the housing bubble. ?When a less knowledgeable friend is making what is seemingly free money, it is very difficult for many people to resist the temptation to imitate, because if it works for him, it ought to work better for the more knowledgeable.

As such, prices can get overbid, and the overshoot above the intrinsic value of the assets can be considerable. ?It all ends when the cost of capital to finance?the asset is considerably higher than the cash flow that the asset throws off. ?And as with all bubbles, the end is pretty ugly and rapid.

But what if you had a really big and liquid strategy, one that threw off decent cash flow. ?Could that ever be a bubble? ?The odds are low but the answer is yes. ?It is possible for any strategy to distort?relative prices such that the assets inside a strategy get significantly above intrinsic value — to the point where they discount negative future returns over a 5-10 year horizon. ?(As an aside, negative interest rates are by definition a bubble, and the instruments traded there are in big liquid markets. ?The severity of that bubble collapsing is likely to be limited, though, unless there is some sort of payments crisis. ?The relative amount of overvaluation is small, and has to be small.)

Then there is the second way of imitation: indexing because it is now the received wisdom — all your friends are doing it. ?This is a momentum effect, and at some point even indexing through a large index like the S&P 500 or Wilshire 5000 could become overdone. ?The effects could vary, though.

You could see more larger private corporations go public because the advantage of cheap capital overwhelms the informational and other advantages of remaining private.

You could see corporations reverse financial engineering, and issue more cheap stock to retire expensive debt. ?On the other hand, it would be more likely that credit spreads would tighten significantly, leaving debt and equity balanced.

You would see pressure on corporations with odd capital structures like?multiple share classes to simplify, so that all of the equity would trade at high multiples.

Corporations could dilute their stock to pay for resources — labor, land, intellectual capital and physical capital. ?Or, buy up competitors. ?If you think that is farfetched, I remember the late ’90s where it was cool for executives to say, “Let the stock market pay your employees.”

People could borrow against their homes to buy more stock, or just margin up.

If you see what I am doing — I’m trying to show what a distorted price for publicly traded stocks in an big index could do — and I haven’t even suggested the obvious — that an unsustainable price will correct eventually, and maybe, in a dramatic way.

I’m not saying that indexing is a bubble presently. ?I’m only saying it could be one day. ?Like the imitation illustrations given above, when a lot of people want to do the same thing without bringing additional information to the process, shortages develop, and in some cases prices rise as a result.

One final note: active management would get more punch at some point, because informationless index investing would lead to some degree of mispricing that active managers would take advantage of. ?At the rate money is currently exiting active management and going into indexing, that could be five years from now (just a guess).

As with all things in investing, the proof will be seen only in hindsight, so take this with a saltshaker of salt. ?As for me, I will continue to pick stocks. ?It has worked well for me.

Before I write my piece, I want to say a word about the virtue of voting for third party candidates for President. ?Personally, I would like to see an option where we can vote for None of the Above, on all races. ?That would allow us to break the duopolistic power of the Democrats and Republicans without having to have a viable third party. ?The ability to reject all of the candidates so that a new election would have to be held with new candidates would be powerful, and would make both parties more sensitive to all of the voters, not just minorities on the left and right.

Still, I’m voting for a third party candidate mostly as a protest. ?I consider the protest to be an investment, because it has no value for the current election, but may have value for future elections if it teaches the two main parties that they no longer have a stranglehold on the electorate. ?The cost of doing so in this election for President is minuscule, because both candidates are dishonest egotists.

Character matters; if a person is not honest you will not get what you thought you were voting for. ?In this election, more than most, people are projecting onto Hillary and Donald what they want to see. ?Trump is not a man of the people, and neither is Clinton. ?They are both elitist snobs; they are members of rival cliques that dominate their respective parts of the main country club that the privileged enjoy.

There is no loss in not voting for them. ?If you want to send a message, vote for someone other than Clinton or Trump.

==============================

Of Milk Cows and Moats

It’s become fashionable to talk about moats in investing as an analogy for sustainable competitive advantages. ?Buffett popularized it, and many use it in investment analysis today. ?Morningstar has made a lot out of it.

I’d like to talk about the concept from a broader societal angle. ?This may look like a divergence from talk on investing, but it does have a significant influence on some investing.

I live in the great state of Maryland. ?A while ago, I wrote an award-winning piece on publicly traded companies in Maryland. ?My main conclusion was that many corporations are?in Maryland because the founder lived here. ?Other corporations were in Maryland because of the talent available to manage healthcare firms, defense firms, hotels, and REITs. ?Only the last one, REITs, had any significant advantage imparted by the state itself — Maryland was the first state with a statute allowing for REITs.

Why do corporations leave Maryland? ?Well, when a merger takes place, the acquirer usually figures out that the company would likely be better off reducing its presence in Maryland, and increasing its presence elsewhere. ?Costs, taxes and regulation will be lower. ?The countervailing advantage of an educated workforce is usually not enough to keep jobs here, unless that is the main input to what the firm does, such as biotechnology — hard to beat the advantage of having Johns Hopkins, NIH, and the University of Maryland nearby.

All of this suggests a model of businesses and people entering and leaving an area that is akin to the moats we describe in business. ?Most businesses know that it will be expensive to move.

They will lose people, or, it will be costly to move them

There will be an interruption to operations in some ways.

The educational quality of people might not be as great in the new area.

Some taxes and regulations could be higher.

Thus to induce a move, another municipality might offer incentives of tax abatement, a low interest loan, etc. ?The attracting municipality is making a business decision — what do they give up in taxes (and have to spend on services) versus what they gain in other taxes, etc. ?The attracting municipality also assumes that there will be some stickiness when the incentives run out. ?If you need an analogy, it is not that much different than what it takes to attract and retain a major league sports franchise.

What municipalities lose businesses and people? ?Those that treat them like milk cows. ?Take a look at the states, counties and cities that have lost vitality, and will find that is one of the two factors in play, the other being a concentrated industry mix in where the dominant industry is in decline.

The more a municipality tries to milk its businesses and people, the more the businesses begin to hit their flinch point, and look for greener pastures. ?With the loss of businesses and people, they may try to raise taxes to compensate, leading to a self-reinforcing cycle that eventually leads to insolvency.

A municipality can fight back by offering its own incentives to retain companies and people. ?This can lead to a version of the prisoners’ dilemma, or a “race to the bottom” as corporations play off municipalities against each other in order to get the best deal possible. ?There is an analogy to war here, because the mobile enemy has significant advantages. ?There is an analogy to antitrust as well, because municipal governments are allowed to collude against corporations, and it would be to their advantage to do so, if they could agree.

In a game like this, the healthiest municipalities have the strongest bargaining position — they can offer the best deals. ?There is a tendency for the strong to get stronger and the weak weaker. ?Past prudence has its rewards. ?Present prudence is costly, both economically and politically, is difficult to achieve, and?future people will benefit who will not remember you politically.

One more note: Maryland has another problem, which affects some of my friends in the industry who have Maryland-centric.investment management practices. ?(My firm is national. ?More of my clients are outside of Maryland than inside.) ?When wealthy people in Maryland retire, their probability of leaving Maryland goes up, as the “moat” of their Maryland job disappears. ?Again states can adjust their tax policies to try to retain people in their states. ?On the other hand, some attempt to tax former residents who earned their pensions in their states, and things like that.

This is just another example of how municipalities have limits to the amount they can tax before the tax base erodes.

(Dare we mention how the internet is still costing states some of their sales taxes? ?Nah, too well known.)

Upshot

When considering businesses that rely on a given locality, ask how the health of the locality affects the business. ?It’s worth considering. ?For those who invest in municipal bonds, it is a critical factor. ?Particularly as the Baby Boomers age, weak municipalities will come under pressure. ?Stick with strong municipalities, and services that would be impossible to do without.

Finally, think about your own life. ?Is it possible:

that your firm could move and leave you behind?

that your taxes could rise significantly because businesses and people are leaving?

that your taxes could rise significantly because state employee benefit plans are deeply underfunded?

that your municipal job could be put in danger because of prior weak economic decisions on the part of the municipality?

that real estate prices could fall if the exodus of people from your area accelerates?

Etc.

Then consider what your own “plan B” might be, and remember, earlier actions to leave are better actions if you are correct. ?The options are always lousy once an economic bust arrives.