Well, this market is nothing if not special. ?The S&P 500 has gone 84 trading days without a loss of 1% or more. ?As you can see in the table below, that ranks it #17 of all streaks since 1950. ?If it can last through February 27th, it will be the longest streak since 1995. ?If it can last through March 23rd, it will be the longest streak since 1966. ?The all-time record (since 1950) would take us all the way to June.

Here’s another way to think about this — look at the VIX. ?It closed today at 10.85. ?Sleepy, sleepy… no risk to be found. ?When you don’t have any significant falls in the market, the VIX tends to sag. ?Aside from the election, which is an exception to the rule, the last two peaks of the VIX over the last six months were after 1%+ drops in the S&P 500.

The same would apply to credit spreads, which are also tight. ?No one expects a change in liquidity, a credit event, a national security incident, etc. ?But as I commented on Friday:

I think the thing that would hurt the most money managers is a melt-up that they would feel forced 2 chase, followed by a hard correction $$

This is an awkward time when you have a lot of people arguing that the market CAN’T GO HIGHER! ?Let me tell you, it can go higher.

Will it go higher? ?Who knows?

Should it go higher? ?That’s the better question, and may help with the prior question. ?If you’re thinking strictly about absolute valuation, it shouldn’t go higher — we’re in the mid-80s on a percentile basis. ?On a relative valuation basis, where are you going to go? ?On a momentum basis, it should go higher. ?It’s not a rip-roarer in terms of angle of ascent, which bodes well for it. ?The rallies that fail tend to be more violent, and this one is kinda timid.

We sometimes ask in investing “who has the most to lose?” ?As in my tweet above, that very well could be asset allocators with low stock allocations that conclude that they need to chase the rally. ?Or, retail waking up to how great this bull market has been, concluding that they have been missing out on “free money.”

Truth, I’m not hearing many people at all banging the drum for this rally. ?There is a lot of skepticism.

As for me, I don’t care much. ?It’s not a core skill of mine, nor is it a part of my business. ?I am finding cheap stocks still, and I will keep investing through thick and thin, unless the 10-year forecast model that I use says future returns are below 3%/year. ?Then I will hedge, and encourage my clients to do so as well.

Until then, the game is on. ?Let’s see how far this streak goes.

Comments are always appreciated from readers, if they are polite. ?Here’s a recent one from the piece?Distrust Forecasts.

You made one statement that I don?t really understand. ?Most forecasters only think about income statements. Most of the limits stem from balance sheets proving insufficient, or cash flows inverting, and staying that way for a while.?

What is the danger of balance sheets proving insufficient? Does that mean that the company doesn?t have enough cash to cover their ?burn rate??

Not having enough cash to cover the burn rate can be an example of this. ?Let me back up a bit, and speak generally before focusing.

Whether economists, quantitative analysts, chartists or guys who pull numbers out of the air, most people do not consider balance sheets when making predictions. ?(Counterexample: analysts at the ratings agencies.) ?It is much easier to assume a world where there are no limits to borrowing. ?Practical example #1 would be home owners and buyers during the last financial crisis, together with the banks, shadow banks, and government sponsored enterprises that financed them.

In economies that have significant private debts, growth is limited, because of higher default probabilities/severity, and less capability of borrowing more should defaults tarry. ?Most firms don?t like issuing equity, except as a last resort, so restricted ability to borrow limits growth. High debt among consumers limits growth in another way ? they have less borrowing capacity and many feel less comfortable borrowing anyway.

Figuring out when there is “too much debt” is a squishy concept at any level — household, company, government, economy, etc. ?It’s not as if you get to a magic number and things go haywire. ?People have a hard time dealing with the idea that as leverage rises, so does the probability of default and the severity of default should it happen. ?You can get to really high amounts of leverage and things still hold together for a while — there may be extenuating circumstances allowing it to work longer — just as in other cases, a failure in one area triggers a lot more failures as lenders stop lending, and those with inadequate liquidity can refinance and then fail.

Three?More Reasons to Distrust Predictions

1) Media Effects — the media does not get the best people on the tube — they get those that are the most entertaining. ?This encourages extreme predictions. ?The same applies to people who make predictions in books — those that make extreme predictions sell more books. ?As an example, consider this post from Ben Carlson on Harry Dent. ?Harry Dent hasn’t been right in a long time, but it doesn’t stop him from making more extreme predictions.

2) Momentum Effects — this one is two-sided. ?There are?momentum effects in the market, so it’s not bogus to shade near term estimates based off of what has happened recently. ?There are two problems though — the longer and more severe the rise or fall, the more you should start downplaying momentum, and increasingly think mean-reversion. ?Don’t argue for a high returning year when valuations are stretched, and vice-versa for large market falls when valuations are compressed.

The second thing is kind of a media effect when you begin seeing articles like “Everyone Ought to be Rich,” etc. ?”Dow 36,000″-type predictions come near the end of bull markets, just as “The Death of Equities’ comes at the end of Bear Markets. ?The media always shows up late; retail shows up late; the nuttiest books show up late. ?Occasionally it will fell like books and pundits are playing “Can you top this?” near the end of a cycle.

3) Spurious Math — Whether it is the geometry of charts or the statistical optimization of regression, it is easy to argue for trends persisting longer than they should. ?We should always try to think beyond the math to the human processes that the math is describing. ?What levels of valuation or indebtedness are implied? ?Setting new records in either is always possible, but it is not the most likely occurrence.

If you knew me when I was young, you might not have liked me much. ?I was the know-it-all who talked a lot in the classroom, but was quieter outside of it. ?I loved learning. ?I mostly liked my teachers. ?I liked and I didn’t like my fellow students. ?If the option of being home schooled had been offered to me, I would have jumped at it in an instant, because then I could learn with no one slowing me down, and no kids picking on me.

I read a lot. A LOT. ?Even when young I spent my time on the adult side of the library. ?The librarians typically liked me, and helped me find stuff.

I became curious about investing for two reasons. 1) my mother did it, and it was difficult not to bump into it. ?She would watch Wall Street Week, and often, I would watch it with her. ?2) Relatives gave me gifts of stock, and my Mom taught me where to look up the price in the newspaper.

Now, if you knew the stocks that they gave me, you would wonder at how I still retained interest. ?The two were the conglomerate Litton Industries, and the home electronics company?Magnavox. ?Magnavox was bought out by Philips in 1974 for a price that was 25% of the original cost basis of my shares. ?We did worse on Litton. ?Bought in the mid-to-late ’60s and sold in the mid-’70s for a 80%+ loss. ?Don’t blame my mother for any of this, though. ?She rarely bought highfliers, and told me that she would have picked different stocks. ?Gifts are gifts, and I didn’t need the money as a kid, so it didn’t bother me much.

At the library, sometimes I would look through some of the research volumes that were there for stocks. ?There are a few things that stuck with me from that era.

1) All bonds traded at discounts. ?It’s not that I understood it well, but I remember looking at bond guides, and noted that none of the bonds traded over $100 — and not surprisingly, they all had low coupons.

In those days, some people owned individual bonds for income. ?I remember my Grandma on my mother’s side talking about how little one of her bonds paid in interest, given that inflation was perking up in the 1970s. ?Though I didn’t hear it in that era, bonds were sometimes called “certificates of confiscation” by professionals ?in the mid-to-late ’70s. ?My Grandpa on my father’s side thought he was clever investing in short-term CDs, but he never changed on that, and forever missed the rally in stocks and long bonds that kicked off in 1982.

When I became a professional bond investor at the ripe old age of 38 in 1998, it was the opposite — almost all bonds traded at premiums, and had relatively high coupons. ?Now, at that time I knew a few firms that were choking because they had a rule that said you can never buy premium bonds, because in a bankruptcy, the premium will be automatically lost. ?Any recoveries will be off the par value of the bond, which is usually $100.

2) Many stocks paid dividends that were higher than their earnings. ?I first noticed that while reading through Value Line, and wondered how that could be maintained. ?The phrase “borrowing the dividend” was bandied about.

Today as a professional I know that we should look at free cash flow as a limit for dividends (and today, buybacks, which were unusual to unheard of when I was a boy), but earnings still aren’t a bad initial proxy for dividend viability. ?Even if you don’t have a cash flow statement nearby, if debt is expanding and earnings don’t cover the dividend, I would be concerned enough to analyze the situation.

3) A lot of people were down on stocks and bonds — there was a kind of malaise, and it did not just emanate from Jimmy Carter’s mind. [Cue the sad Country Music] Some concluded that inflation hedges like homes, short CDs, and gold/silver were the only way to go. ?I remember meeting some goldbugs in 1982 just as the market was starting to take off, and they disdained the idea of stocks, saying that history was their proof.

The “Death of Equities” came and went, but that reminds me of one more thing:

4) There was a decent amount of pessimism about defined benefit plan pension funding levels and life insurer solvency. ?Inflation and high interest rates made life insurers look shaky if you marked the assets alone to market (the idea of marking liabilities to market was at least 10 years off in concept, and still hasn’t really arrived, though cash flow testing accomplishes most of the same things). ?Low stock and bond prices made pension plans look shaky. ?A few insurance companies experimented with buying gold and other commodities, just in time for the grand shift that started in 1982.

Takeaways

The biggest takeaway is to remember that as a fish you don’t notice the water that you swim in. ?We are so absorbed in the zeitgeist (Spirit of the Times)?that we usually miss that other eras are different. ?We miss the possibility of turning points. ?We miss the possibility of things that we would have not thought possible, like negative interest rates.

In the mid-2000s, few thought about the possibility of debt deflation having a serious impact on the US economy. ?Many still feared the return of inflation, though the peacetime inflation of the late ’60s through mid-’80s was historically unusual.

The Soviet Union will bury us.

Japan will bury us. ?(I’m listening to some Japanese rock as I write this.) 😉

China will bury us.

Few people can see past the zeitgeist. ?Many can’t remember the past.

Should we?be concerned about companies not being able pay their dividends and fulfill their buybacks? ?Yes, it’s worth analyzing.

Should we be concerned about defined benefit plan funding levels? Yes, even if interest rates rise, and percentage deficits narrow. ?Stocks will likely fall with bonds if real interest rates rise. ?And, interest rates may not rise much soon. ?Are you ready for both possibilities?

Average people don’t seem that excited about any asset class today. ?The stock market is at new highs, and there isn’t really a mania feel now. ?That said, the ’60s had their highfliers, and the P/Es eventually collapsed amid inflation and higher real interest rates. ?Those that held onto the Nifty Fifty may not have lost money, but few had the courage. ?Will there be a correction for the highfliers of this era, or, is it different this time?

It’s never different.

It’s always different.

Separating the transitory from the permanent is tough. ?I would be lying to you if I said I could do it consistently or easily, but I spend time thinking about it. ?As Buffett has said, (something like)?”We’re paid to think about things that can’t happen.”

Ending Thoughts

Now, lest the above seem airy-fairy, here are my biases at present as I try to separate the transitory from the permanent:

The US is in better shape than most of the rest of the world, but its securities are relatively priced for that reality.

Before the US has problems, Japan, China, OPEC, and the EU will have problems, in about that order. ?Sovereign default used to be a large problem. ?It is a problem that is returning. ?As I have said before — this era reminds me of the 1840s — huge debts and deficits, with continued currency debasement. ?Hopefully we don’t get a lot of wars as they did in that decade.

I am treating long duration bonds as a place to speculate — I’m dubious as to how much Trump can truly change things. ?I’m flat there now. ?I think you almost have to be a trend follower there.

The yield curve will probably flatten quickly if the Fed tightens more than once more.

The internet and global demographics are both forces for deflationary pressure. ?That said, virtually the whole world has overpromised to their older populations. ?How that gets solved without inflation or defaults is a tough problem.

Stocks are somewhat overvalued, but the attitude isn’t frothy.

DIvidend stocks are kind of a cult right now, and will suffer some significant setback, particularly if interest rates rise.

Eventually emerging markets and their stocks will dominate over developed markets.

Value investing will do relatively better than growth investing for a while.

That’s all for now. ?You may conclude very differently than I have, but I would encourage you to try to think about the hard problems of our world today in a systematic way. ?The past teaches us some things, but not enough, which should tell all of us to do risk control first, because you don’t know the future, and neither do I. 🙂

I’ve thought about this problem before, but always thought it was more of a curiosity until I read this on page 66 of Jeff Gramm’s very good book, Dear Chairman: Boardroom Battles and the Rise of Shareholder Activism. ?(Note: anyone entering through this link and buying something at Amazon, I get a small commission.)

I saw Eddie Lampert, a hedge fund manager who is chairman of Sears Holdings, make some interesting points at a New York Public Library event in 2006. When he was discussing the challenges of managing a public company, he raised a question few people in the room had considered. How do you run a company well when the stock is overvalued? What happens when management can’t meet investors’ unrealistic expectations without taking more risk? And what happens to employee morale if everyone does a good job but the stock declines? Lampert, of course, knew what he was talking about. Sears closed that day at $175 per share versus today’s price of around $35. In an efficient market, it’s easy to develop tidy theories about optimal corporate governance. Once you realize stock prices can be totally crazy, the dogma needs to go out the window.

The price of Sears Holding is around $13 now, though there have been a lot of spinoffs. ?Could Eddie have done better for shareholders? ?Before answering that, let’s take a simpler example: what should a the managers/board of a closed end fund do if it persistently trades at a large premium to its net asset value [NAV]? ?I can think of three ideas:

1) Conclude that the best course of action is to?minimize the eventual price crash that will happen. ?Therefore issue stock as near the current price level as possible, and use it to buy non-inflated assets, bringing down the discount. ?What’s that, you say? ?The act of announcing a stock offering will crater the price? ?Okay, good point, which brings us to:

2) Merge with another closed end fund, trading at a discount, but offering them a premium to their NAV, hopefully a closed end fund?related to the type of closed end fund that you are. ?What’s that, you say? ?Those that manage other closed end funds are financial experts, and would never agree to that? ?Uhh, maybe. ?Let me say that not all financial experts are equal, and who knows what you might be able to do. ?Also, they do have a duty to their investors to maximize value, and for those that?sell above net asset value this is a big win. ?In the meantime, you have reduced your effective economic discount for those that continue to hold your fund.

3) Issue bonds or preferred stock convertible into common stock at a level that virtually guarantees conversion. ?Use the proceeds to invest in your ordinary investment strategy, bringing down the effective discount as dilution slowly takes place.

Of all the ideas, I think 3 might work best, because it would have the best chance of allowing you to issue equity near the overvalued level. ?If the overvaluation was 50%, maybe you could get it down to 25% by doubling the asset base, in which case you did your holders a big favor. ?If it works, maybe repeat it in two years if the premium persists.

A closed end fund is simple compared to a company — but that added complexity may allow strategies one or two to work better. ?Before we go there, let’s take one more detour — PENNY STOCKS!

Okay, I haven’t written about those in a while, but what do penny stock managements with no revenues do to keep their firm alive? ?They trade stock at discount levels in order to source goods and services. ?This creates dilution, but they don’t care, they are waiting for the day when they can exit, possibly after a promotion. ?Also, they could issue their stock to buy up a small firm,?adding some value behind the worthless shares. ?One guy wrote me after my penny stock articles, telling me of how he foolishly did that, with the stock being restricted, and he watched in horror as the ?price sank 60% before he was allowed to sell any shares. ?He lost most of what he worked for in life, took the company to court, and I suspect that he lost… it was his responsibility to do “due diligence.”

So with that, strategy one can be to issue as much stock as possible as quietly as possible. ?Offer your employees stock in order to reduce wages. ?Give them options. ?Where possible, pay for real assets and services with stock. ?Issue stock, saying that you have big plans for organic growth, then, try to grow the company. ?In this case, strategy three can make more sense, as the set of buyers taking the convertible stock and bonds don’t see the dilution. ?That said, the hard critical element is the organic growth strategy — what great thing can you do? ?Maybe this strategy would apply to a cash hungry firm like Tesla.

In strategy two, merge with other companies either to achieve diversification or vertical integration. ?Issue stock at a premium to the value received, but not not as great as the premium underlying your current stock price. ?Ordinarily, I would argue against dilutive acquisitions, but this is a special case where you are trying to reduce the premium valuation without reducing the share price.

This brings us to another set of examples: conglomerates and roll-ups. ?Think of the go-go years in the ’60s where conglomerates bought up low P/E stocks using?their high P/E stocks as currency. ?Initially, the process produces earnings growth. ?It works until the eventual bloat of the businesses is difficult to manage, and?the P/Es fall. ?Final acquisitions are sometimes ugly, leading to failure. ?The law of decreasing returns to scale eventually catches up.

With roll-ups an aggressive management team buys up peers. ?The acquirer is a faster growing company, and so its stock trades at a premium. ?If the acquirer is clever, it can shed costs in the target, and continue to show earnings growth for some time until it finally slows down and has to rationalize the mess of peer companies that have been bought.

This brings up one more area for overvalued companies: frauds. ?This past evening, my wife and I watched The Billion Dollar Bubble, which was the largest financial fraud up until Madoff. ?One thing Equity Funding?did was use the funds that they had generated to buy other insurers. (That’s not in the movie, which kept things simple, and compressed the time it took for the fraud to take place.)

Enron is another example of a fraudulent company that used its inflated share price to buy up other companies. ?Not everything Enron did was fraudulent, but having a highly valued stock allowed it to buy up companies with assets which reduced some of its valuation premium, though not enough for the stock to go out at a positive figure.

Summary

It is an unusual situation, but the best strategy for a company with an overvalued stock is to try to grow their way out of it, usually through mergers and acquisitions. ? The twist I offer you at the end of my piece is this: thus, watch highly acquisitive firms. Not all of them are overvalued or fraudulent, but some will be. Avoid the shares of those firms.

[bctt tweet=”watch highly acquisitive firms. Not all of them are overvalued or fraudulent, but some will be. Avoid the shares of those firms.” username=”alephblog”]

I have sometimes said that it is common for many people to imitate the behavior of others, rather than think for themselves. ?There are several reasons for that:

It”s simple.

It’s fast.

And so long as you don’t run into a resource constraint it works well.

People generally have a decent idea who their smartest friends are, and who seems to give good advice on simple issues. ?If your neighbor says that the new Chinese food place is excellent, and you know he knows his food, there is a very good chance that when you go there that you will get excellent Chinese food as well.

You might even tell your friends about it; after all, you want to look bright as well, and its neighborly to share good information. ?That works quite well until the day that Yogi Berra’s dictum kicks in:

Nobody goes there anymore. It?s too crowded.

The information indeed was free, but space inside the restaurant was not, even if patrons weren’t paying to get in. ?And even if they have carryout, the line could go around the block… a hardship for many even if?you are getting the famous Ocean Broccoli Beef. ?(Warning: Hot in every way.)

Readers of my blog know that the same thing happens in markets. ?Imitation was a large part of the dot-com bubble and the housing bubble. ?When a less knowledgeable friend is making what is seemingly free money, it is very difficult for many people to resist the temptation to imitate, because if it works for him, it ought to work better for the more knowledgeable.

As such, prices can get overbid, and the overshoot above the intrinsic value of the assets can be considerable. ?It all ends when the cost of capital to finance?the asset is considerably higher than the cash flow that the asset throws off. ?And as with all bubbles, the end is pretty ugly and rapid.

But what if you had a really big and liquid strategy, one that threw off decent cash flow. ?Could that ever be a bubble? ?The odds are low but the answer is yes. ?It is possible for any strategy to distort?relative prices such that the assets inside a strategy get significantly above intrinsic value — to the point where they discount negative future returns over a 5-10 year horizon. ?(As an aside, negative interest rates are by definition a bubble, and the instruments traded there are in big liquid markets. ?The severity of that bubble collapsing is likely to be limited, though, unless there is some sort of payments crisis. ?The relative amount of overvaluation is small, and has to be small.)

Then there is the second way of imitation: indexing because it is now the received wisdom — all your friends are doing it. ?This is a momentum effect, and at some point even indexing through a large index like the S&P 500 or Wilshire 5000 could become overdone. ?The effects could vary, though.

You could see more larger private corporations go public because the advantage of cheap capital overwhelms the informational and other advantages of remaining private.

You could see corporations reverse financial engineering, and issue more cheap stock to retire expensive debt. ?On the other hand, it would be more likely that credit spreads would tighten significantly, leaving debt and equity balanced.

You would see pressure on corporations with odd capital structures like?multiple share classes to simplify, so that all of the equity would trade at high multiples.

Corporations could dilute their stock to pay for resources — labor, land, intellectual capital and physical capital. ?Or, buy up competitors. ?If you think that is farfetched, I remember the late ’90s where it was cool for executives to say, “Let the stock market pay your employees.”

People could borrow against their homes to buy more stock, or just margin up.

If you see what I am doing — I’m trying to show what a distorted price for publicly traded stocks in an big index could do — and I haven’t even suggested the obvious — that an unsustainable price will correct eventually, and maybe, in a dramatic way.

I’m not saying that indexing is a bubble presently. ?I’m only saying it could be one day. ?Like the imitation illustrations given above, when a lot of people want to do the same thing without bringing additional information to the process, shortages develop, and in some cases prices rise as a result.

One final note: active management would get more punch at some point, because informationless index investing would lead to some degree of mispricing that active managers would take advantage of. ?At the rate money is currently exiting active management and going into indexing, that could be five years from now (just a guess).

As with all things in investing, the proof will be seen only in hindsight, so take this with a saltshaker of salt. ?As for me, I will continue to pick stocks. ?It has worked well for me.

Six years ago, I reviewed a book?The Club No One Wanted To Join. ?It was a poorly done book written by a bunch of people who were swindled by Bernie Madoff. ?Now, I?didn’t want to be unsympathetic — after all, they were cheated. ?But they missed many signals that tipped off others, and could have tipped off them to the fraud. ?Worse, they tried to argue that since many top-performing mutual funds had total returns similar to that of Madoff, there was no way anyone could have figured out that it was a scam. ?They neglected to note that Madoff’s returns were ultra-smooth, while the returns of the mutual funds were not. ?Big difference.

There’s one more thing: many of them gave in to the idea that they had found a hole in the system. ?Far from it being “The Club No One Wanted To Join,” rather, it was their own secret private club that they were smart enough to join when fate smiled on them, and they got their opportunity.

Tonight, I am talking about a different sort of scam that sucked in a different class of people. ?This scam was a corporation where the management took a?firm into bankruptcy that could easily pay its debts, at least in the short-run. ?The management likely conspired with the bondholders against its shareholders, seemingly in an effort to gain a greater reward from the bondholders who would own the firm post-bankruptcy than they could from operating the firm outside of bankruptcy. ?The name of this firm is Horsehead Holdings [ZINCQ].

I’m not writing about?this to give a blow-by-blow description of how the bondholders and management cheated shareholders out of their ownership interests, though I will touch on that at points. ?I am writing about this to respond to those who wrote to me in the midst of the bankruptcy trial to try to gain some coverage of what was going on.

Over 20 people wrote to me and almost 100?journalists/media in an attempt to create “viral” coverage of the trial, and if nothing else, bring public attention to the travesty that was the bankruptcy process. ?As it is, I wrote one paragraph on the matter, but I didn’t see anything from any major publication until after the trial completed. ?I did mention to a number of the writers that efforts to get coverage would not affect the outcome of the bankruptcy court; it is relatively insulated from public opinion, as it should be.

(As an aside: if you write such a letter to journalists, or me, try to stay on topic. ?It is not relevant to call the bondholders “greedy,” that they are a hedge fund, or talk about their prior dealings with Collateralized Debt Obligations that failed during the recent financial crisis.)

Aleph Blog is mostly about risk control. ?As I read the letters from the shareholders who were watching their ownership rights be destroyed, I noted a few things that might have enabled some of them to avoid much of the unfavorable outcome:

Buying a levered highly cyclical company.

Relying on the insights of bright investors who buy concentrated stakes ?in a few companies.

Not diversifying enough.

Let me take these in order:

Buying a levered highly cyclical company

If you look at the risk of owning a single company, there are two ways where a company can affect the degree to which a change in sales can raise the profits of the company. ?The first way is to choose a production method that has high fixed costs and low variable costs, which is typically true of cyclical companies. ?The second way is to borrow money. ?Both methods magnify returns, right or wrong.

Typically, you only do one at a time. ?Supermarkets are stable, so they often borrow more to lever up returns. ?Mining companies, among other industries that require heavy capital investment, are anything but stable booms and busts are common and follow product prices.

Horsehead Holdings had a high degree of leverage from both debt and being in a cyclical industry. ?It ran into a scenario where the price of its main product, zinc, fell hard. ?At the time before they filed for bankruptcy, management could legitimately say to themselves, “If the price of zinc remains this low we will shortly be insolvent, particularly if our new processing plant doesn’t work out.”

Now, the bankruptcy code is a rather flexible beastie. ?It allows for a management team to file before things are at their worst so that they can try to preserve a better outcome for the company. ?My suspicion is that management’s motives were mixed when they filed — they wanted the best deal they could get for themselves, but may have assumed that there wasn’t much life left to the equity anyway. ?Who could have predicted that the price of zinc would rally back so much, such that the company could have survived in its pre-bankruptcy state?

Now, has this ever happened to me? ?Not exactly, but there are other ways that managements can dispose of a company to the detriment of the stockholders. ?I lost money on C. Brewer Homes when management did a leveraged buyout when the stock price was unduly depressed. ?Enough stock was in the hands of arbs that the deal went through. ?Oh, and if you want another one, there was the loss on National Atlantic Holdings which I described in ugly detail in this article.

The main point is this: don’t assume that management will act in the interests of stockholders, particularly in a stressed situation. ?The leverage and cyclicality of Horsehead Holdings set up the possibility of that occurrence, and the fall in the price of zinc triggered it.

Relying on the insights of bright investors who buy concentrated stakes ?in a few companies

I respect both Mohnish Pabrai and Guy Spier. ?They are bright guys, and from what I can tell at a distance, ethical too. ?They were big holders of Horsehead Holdings, and I’m sure they had good reasoning behind their decisions. ?But, even excellent investment managers aren’t infallible. If you are just picking one of their ideas, that could be a rocket to the sky — or the ground, while their portfolio as a whole might do well.

Also, they will make their decisions with some lead time over you if the data shifts. ?Any investment advisor you mimic is not required to tell you when they change their mind, aside from required filings with the SEC… which are delayed, and sometimes don’t cover everything.

Has this happened to me? ?Yes it has. ?I have sometimes invested partly ?on who is invested in a company, though never to the point of not?doing my “due diligence.” ?But aside from some early failures 20+ years ago, it never hurt me much because I was never guilty of:

Not Diversifying Enough

A number of the people emailing me said they put more than half their savings into Horsehead Holdings. ?If you are going to engage in such risky behavior, you need to know more than everyone else investing in the stock. ?No exceptions. ?I agree with investing in a concentrated way, but?my view of that for average people is no positions larger than 5% of your capital. ?That is plenty concentrated enough.

I have one holding that is 13% of my assets — a private company that I know exceptionally well. ?My house is another 13%. ?After that, my next largest holding is 3% of my assets. ?I believe in the assets that I buy, but I concentrate enough by only owning individual stocks, and very little in the way of pooled investment vehicles.

Again, my sympathies to those who lost on Horsehead. ?I can’t do anything about those losses. ?At least you have the opportunity to sue the?management of the company. ?It certainly seems like the management team cheated the stockholders, though I can’t say for sure.

What I can help are future investors, and my counsel is this: Diversify! ?You are your own best defender, so don’t merely mimic bright investors; do your own due diligence. ?Be wary of investing in cyclical companies with high debt levels. ?Don’t implicitly trust that management teams will act in your interest. ?And finally, diversify, as it protects against failures in other areas.

PS — I looked through my notes of the past. ?I did look at Horsehead Holdings, and I passed on it. ?That said, I don’t know why… hopefully it was for a good reason, though I expect that I didn’t have room for another cyclical company, and not another one in base metals.

When I was 29, nearly half a life ago, Donald Trump was a struggling real estate developer. ?In 1990, I was still trying to develop my own views of the economy and finance. ?But one day heading home from work at AIG, I was listening to the business report on the radio, and I heard the announcer say that Donald Trump had said that he would be “the king of cash.” ?My tart comment was, “Yeah, right.”

At that point in time, I knew that a lot of different entities were in need of financing. ?Though the stock market had come back from the panic of 1987, many entities had overborrowed to buy commercial real estate. ?The major insurance companies of that period were deeply at fault in this as well, largely driven by the need to issue 5-year Guaranteed Investment Contracts [GICs] to rapidly growing stable value funds of defined contribution plans. ?Outside of some curmudgeons in commercial mortgage lending departments, few recognized that writing 5-year mortgages with low principal amortization rates against long-lived commercial properties was a recipe for disaster. ?This was especially true as lending yield spreads grew tighter and tighter.

(Aside: the real estate area of Provident Mutual avoided most of the troubles, as they sold their building that they built seven years earlier for twice what they paid to a larger competitor. ?They also focused their mortgage lending on small, ugly, economically necessary properties, and not large trophy properties. ?They were unsung heroes of the company, and their reward was elimination eight years later as a “cost saving move.” ?At a later point in time, I talked with the lending group at Stancorp, which had a similar philosophy, and expressed admiration for the commercial mortgage group at Provident Mutual… Stancorp saw the strength in the idea, and still follows it today as the subsidiary of a Japanese firm. ?But I digress…)

Many of the insurance companies making the marginal commercial mortgage loans had come to AIG seeking emergency financing. ?My boss at AIG got wind of the fact that I was looking elsewhere for work, and subtly regaled me of the tales of woe at many of the insurance companies with these lending issues, including one at which I had recently interviewed. ? ?(That was too coincidental for me not to note, particularly as a colleague in another division asked me how the search was going. ?All this from one stray comment to an actuary I met coming back from the interview…)

Back to the main topic: good investing and business rely on the concept of a margin of safety. ?There will be problems in any business plan. ?Who has enough wherewithal to overcome those challenges? ?Plans where everything has to go right in order to succeed will most likely fail.

With Trump back in 1990, the goal was admirable — become liquid in order to purchase properties that were now at bargain prices. ?As was said in the Wall Street Journal back in April of 1990, the article started:

In a two-hour interview, Mr. Trump explained that he is raising cash today so he can scoop up bargains in a year or two, after the real estate market shakes out. Such an approach worked for him a decade ago when he bet big that New York City’s economy would rebound, and developed the Trump Tower, Grand Hyatt and other projects.

“What I want to do is go and bargain hunt,” he said. “I want to be king of cash.”

That’s where?Trump said it first. ?After that he received many questions from reporters and creditors, because his businesses were heavily indebted, and?property values were deflated, including the properties that he owned. ?Who wouldn’t want to be the “king of cash” then? ?But to be in that position would mean having sold something when times were good, then sitting on the cash. ?Not only is that not in Trump’s nature, it is not in the nature of most to do that. ?During good times, the extra cash that Buffett keeps on hand looks stupid.

Trump did not get out of the mess by raising cash, but by working out a deal with his creditors in bankruptcy. ?Give Trump credit, he had convinced most of his creditors that they were better off continuing to finance him rather than foreclose, because the Trump name made the properties more valuable. ?Had the creditors called his bluff, Trump?would have lost a lot, possibly to the point where we wouldn’t be hearing much about him today.

Trump escaped, but most other debtors don’t get the same treatment Trump did. ?The only way to survive in a credit crunch is plan ahead by getting adequate long-term financing (equity and long-term debt), and keep a “war kitty” of cash on the side.

During 2002, I had the chance to test this as a bond manager. ?With the accounting disasters at mid-year, on July 27th, two of my best brokers called me and said, ?The market is offered without bid.? We?ve never seen it this bad.? What do you want to do??? I kept a supply of liquidity on hand for situations like this, so with the S&P falling, and the VIX over 50, I put out a series of lowball bids for BBB assets that our analysts liked.? By noon, I had used up all of my liquidity, but the market was turning.? On October 9th, the same thing happened, but this time I had a larger war chest, and made more bids, with largely the same result.

That’s tough to do, and my client pushed me on the “extra cash sitting around.” ?After all, times are good, there is business to be done, and we could use the additional interest to make the estimates next quarter.

To give another example, we have the visionary businessman Elon Musk facing a?cash crunch?at Tesla?and?SolarCity. ?Leave aside for a moment his efforts to merge the two firms when stockholders tend to prefer “pure play” firms to conglomerates — it’s interesting to look at how two “growth companies” are facing a challenge raising funds at a time when the stock market is near all time highs.

Both Tesla and Solar City are needy companies when it comes to financing. ?They need a lot of capital to grow their operations before the day comes when they are both profitable and cash flow from operations is positive. ?But, so did a lot of dot-com companies in 1998-2000, of which a small number exist to this day. ?Elon Musk is in a better position in that presently he can dilute?issue shares of Tesla to finance matters, as well as buy 80% of the Solar City bond issue. ?But it feels weird to have to finance something in less than a public way.

There are other calls on cash in the markets today — many companies are increasing dividends and buying back stock. ?Some are using debt to facilitate this. ?I look at the major oil companies and they all seem to be levering up, which is unusual given the recent trajectory of crude oil prices.

We are in the fourth phase of the credit cycle now — borrowing is growing, and profits aren’t. ?There’s no rule that says we have to go through a bear market in credit before that happens, but that is the ordinary?way that excesses get purged.

That is why I am telling you to pull back on risk, and review your portfolio for companies that need financing in the next three years or they will croak. ?If they don’t self finance, be wary. ?When things are bad only cash flow can validate an asset, not hopes of future growth.

With that, I close this article with a poem that I saw as a graduate student outside the door of the professor for whom I was a teaching assistant when I first came to UC-Davis. ?I did not know that is was out on the web until today. ?It deserves to be a classic:

Once upon a midnight dreary as I pondered weak and weary

Over many a quaint and curious volume of accounting lore,

Seeking gimmicks (without scruple) to squeeze through

Some new tax loophole,

Suddenly I heard a knock upon my door,

Only this, and nothing more.

Then I felt a queasy tingling and I heard the cash a-jingling

As a fearsome banker entered whom I?d often seen before.

His face was money-green and in his eyes there could be seen

Dollar-signs that seemed to glitter as he reckoned up the score.

?Cash flow,? the banker said, and nothing more.

I had always thought it fine to show a jet black bottom line.

But the banker sounded a resounding, ?No.

Your receivables are high, mounting upward toward the sky;

Write-offs loom.? What matters is cash flow.?

He repeated, ?Watch cash flow.?

Then I tried to tell the story of our lovely inventory

Which, though large, is full of most delightful stuff.

But the banker saw its growth, and with a might oath

He waved his arms and shouted, ?Stop!? Enough!

Pay the interest, and don?t give me any guff!?

Next I looked for noncash items which could add ad infinitum

To replace the ever-outward flow of cash,

But to keep my statement black I?d held depreciation back,

And my banker said that I?d done something rash.

He quivered, and his teeth began to gnash.

When I asked him for a loan, he responded, with a groan,

That the interest rate would be just prime plus eight,

And to guarantee my purity he?d insist on some security?

All my assets plus the scalp upon my pate.

Only this, a standard rate.

Though my bottom line is black, I am flat upon my back,

My cash flows out and customers pay slow.

The growth of my receivables is almost unbelievable:

The result is certain?unremitting woe!

And I hear the banker utter an ominous low mutter,

?Watch cash flow.?

Herbert S. Bailey, Jr.

Source: ?The January 13, 1975, issue of Publishers Weekly, Published by R. R. Bowker, a Xerox company.? Copyright 1975 by the Xerox Corporation. ?Credit also to?aridni.com.

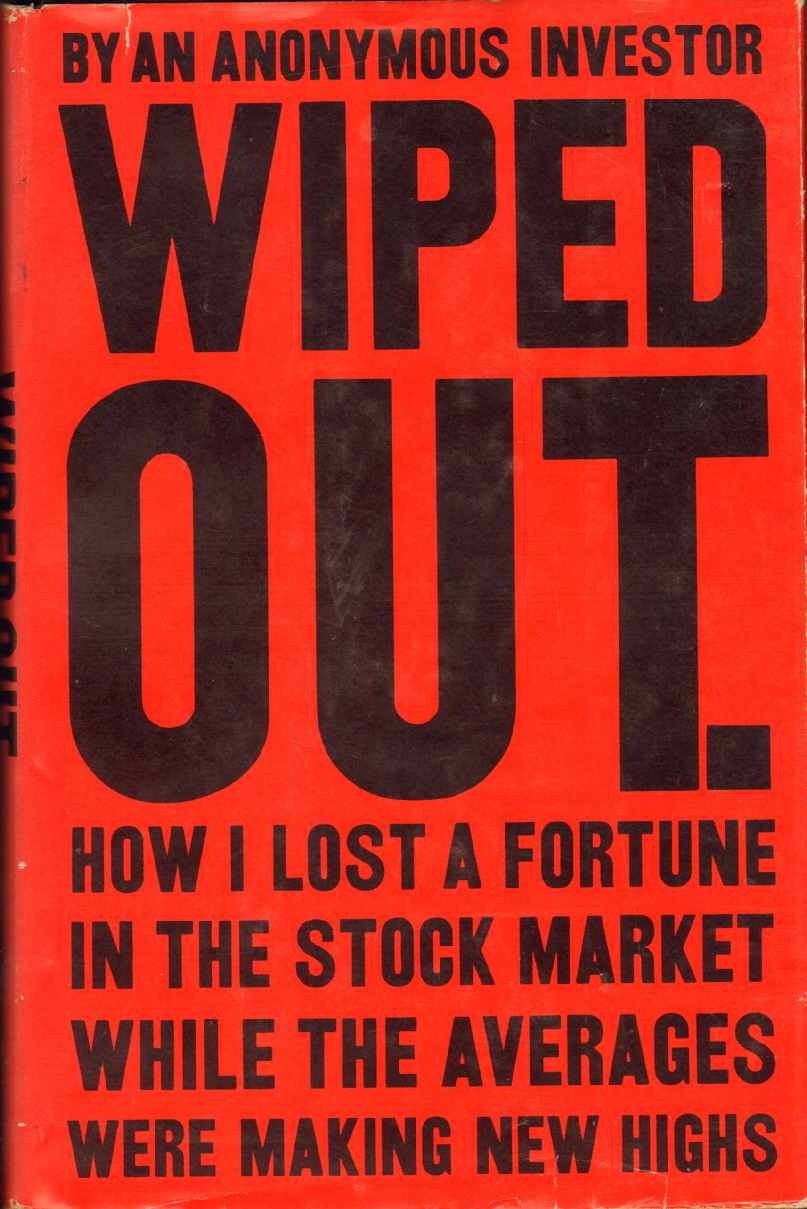

This is an obscure little book published in 1966. ?The title is direct, simple, and descriptive. ?A more flowery title could have been, “Losing Money in the Stock Market as an Art Form.” ?Why? ?Because he made every mistake possible in an era that favored stock investment, and managed to lose a nice-sized lump sum that could have been a real support to his family. ?Instead, he tried to recoup it by anonymously publishing ?this short book which goes from tragedy to tragedy with just enough successes to keep him hooked.

Whom God Would Destroy

There is a saying, “”Whom the gods would destroy, they first make mad.” ?My modification of it is, “Whom God would destroy, he first makes proud.” ?In this book, the author knows little about investing, but wishing to make more money in the midst of a boom, he entrusts a sizable nest egg for a young middle-class family to a broker, and lo and behold, the broker makes money in a rising market with a series of short-term investments, with very few losses.

Rather than be grateful, the author got greedy. ?Spurred by success, he became somewhat compulsive, and began reading everything he could on investing. ?To brokers, he became “the impossible client,” (my words, not those of the book) because now he could never be satisfied. ?Instead of being happy with a long-run impossible goal of 15%/year (double your money every five years), he wanted to double his money every 2-3 years. (26-41%/year)

As such, he moved his money from the broker that later he admitted he should have been satisfied with, and sought out brokers that would try to hit home runs. ?The baseball analogy is useful here, because home run hitters tend to strike out a lot. ?The analogy breaks down?here: a home run hitter can be useful to a team even if he has a .250 average and strikes out three times for every home run. ?Baseball is mostly a game of team compounding, where usually a number of batters have to do well in order to score. ?Investment is a game of individual compounding, where strikeouts matter a great deal, because losses of capital are very difficult to make up. ?Three 25% losses followed by a 100% gain is a 15% loss.

In the process of trying to win big, he ended up losing more and more. ?He concentrated his holdings. ?He bought speculative stocks, and not “blue chips.” ?He borrowed money to buy more stock (used margin). ?He bought “story stocks” that did not possess a margin of safety, which would maybe deliver high gains ?if the story unfolded as illustrated. ?He did not do homework, but listened to “hot tips” and invested off them. ?He let his judgment be clouded by his slight relationships with corporate insiders at the end. ?HE TRIED TO MAKE BIG MONEY QUICKLY, AND CUT EVERY CORNER TO DO SO. ?His expectations were desperately unrealistic, and as a result, he lost it all.

As he lost more and more, he fell into the psychological trap of wanting to get back what he lost, and being willing to lose it all in order to do so. ?I.e., if he lost so much already, it was worth losing what was left if there was a chance to prove he wasn’t a fool from his “investing.” ?As such, he lost it all… but there are three good things to say about the author:

He had the humility to write the book, baring it all, and he writes well.

He didn’t leave himself in debt at the end, but that was good providence for him, because if he had waited one more day, the margin clerk would have sold him out at a decided loss, and he would have owed the brokerage money.

In the end, he knew why he had gone wrong, and he tells his readers that they need to: a) invest in quality companies, b) diversify, and c) limit speculation to no more than 20% of the portfolio.

His advice could have been better, but at least he got the aforementioned ideas?right. ?Margin of safety is the key. ?Doing significant due diligence if you are going to buy individual stocks is required.

Quibbles

This book will not teach you what to do; it teaches what not to do. ?It is best as a type of macabre financial entertainment.

Also, though you can still buy used copies of the book, if enough of you try to buy the used books out there, the price will rise pretty quickly. ?If you can, borrow it from interlibrary loan. ?It is an interesting historical curiosity of a book, and a cautionary tale for those who are tempted to greed. ?As the author closes the book:

“Cupidity is seldom circumspect.”

And thus, much as the greedy need to hear this advice, it is unlikely they will listen. ?Greed is compulsive.

Summary / Who Would Benefit from this Book

A good book, subject to the above limitations. ?It is best for entertainment, because it will teach you what not to do, rather than what to do.

Full disclosure:?I bought it with my own money for three bucks.

If you enter Amazon through my site, and you buy anything, including books, I get a small commission. This is my main source of blog revenue. I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip. Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book. Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website. Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites. Whether you buy at Amazon directly or enter via my site, your prices don?t change.

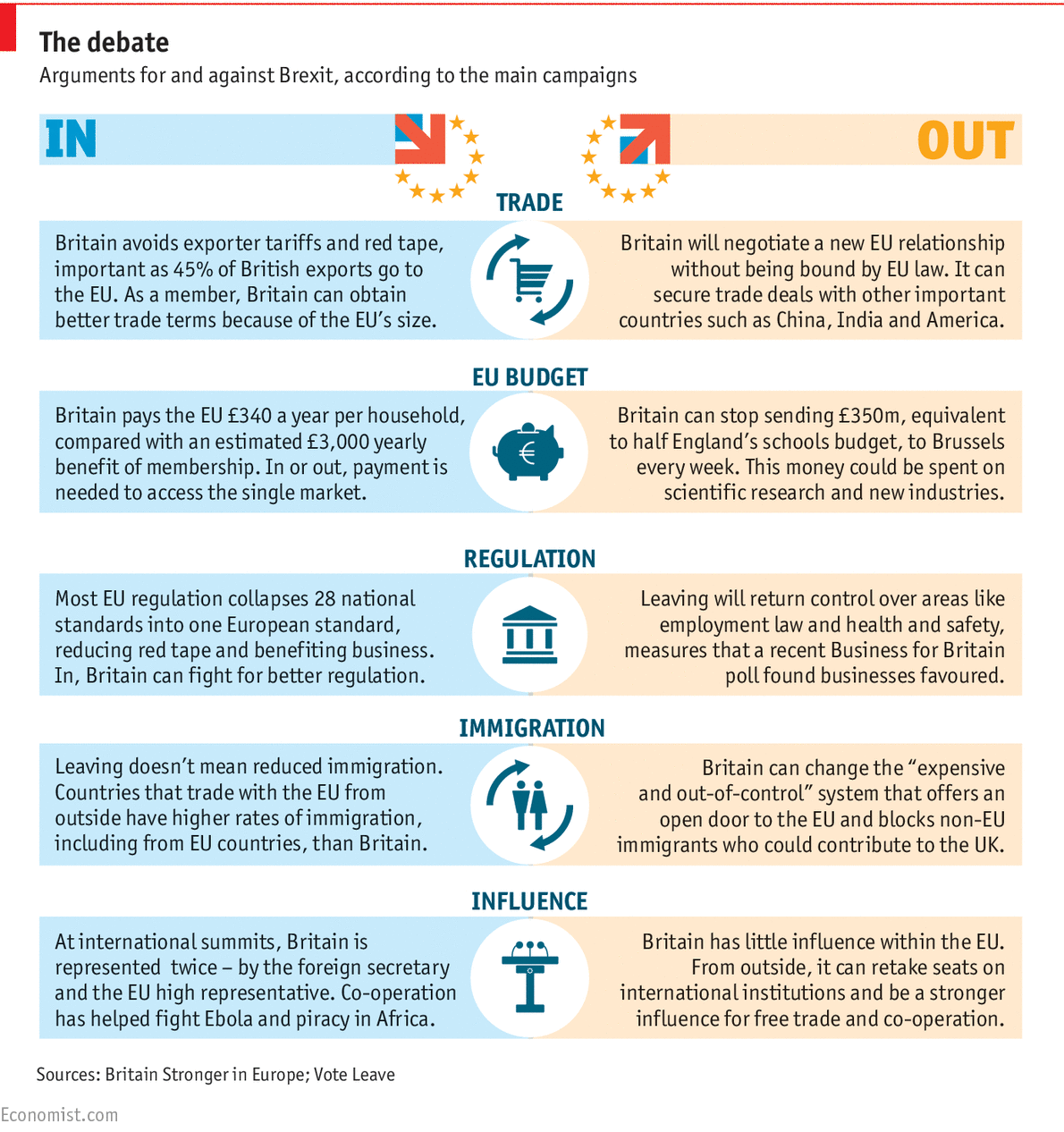

Investors need things to scare them, or they don’t have a normal life. ?This is kind of like the bachelor uncle who tells little?nieces and nephews about scary things that lurk under their beds, and only come out at night for mischief and mayhem. ?(Then the parents pick up the pieces later, when they wonder why William or Elizabeth no longer sleep well at night.)

That’s the way I feel about US & international market reactions to the possibility of UK/Britain exiting the EU, otherwise called “Brexit.” ?It’s overblown. ?Quoting from an older article of mine:

Governments are smaller than markets; markets are smaller than cultures.

What I am saying is that almost everything affecting the needs of people will get done when there is sufficient freedom. ?If Brexit occurs, the UK will negotiate some agreement that is mutually beneficial to the UK and the EU, and most things will go on as they do today. ?Even with a subpar agreement, perfidious Albion is very effective at getting what they need completed. ?This is especially true of their very effective and creative financial sector in the City of London without which most effective international secrecy, taxation avoidance and regulatory avoidance business could not be done.

There are other reasons not to worry as well if you live outside the UK. ?The biggest reason is that the UK is only a small part of the global economy, and the economic effects on non-EU trade and finance are smaller still. ?And unlike the idea was small but “contained,” in this case, large second order effects aren’t there. ?Yes, someday other nations may wise up and decide to leave the EU, but?no major countries are likely to do that over the next decade, absent some crisis. ?(Crises in the EU? Those aren’t allowed to happen; ask any Eurocrat, they’ll tell ya.)

A second reason not to worry is that leaving the EU ends a second level of regulation of UK economic activity. ?This will enable better growth in the longer term. ?Are there things that the UK will lose? ?Sure, they won’t have as good of a trade deal with the EU, but they will have the ability to try to craft better deals elsewhere, like a Transatlantic Free Trade Area.

Looking over this, the UK already depends less on the EU than most member states, making the exit less of a big deal for the UK and the EU.

My view is this: leaving the EU won’t be a big thing in the long run for the UK. ?In the short-run, there will be some uncertainty and volatility as things get worked out. ?For the rest of the world, it will be a big fat zero, so ignore this, and focus on something with more meaning, like bizarre monetary policy, and the twisting effects it is having on our world, or the global entitlements crisis — too many people retiring, too few to support them, especially medically.

So, be willing to take some additional risk if people mindlessly panic if the UK/Britain exits the EU.

There were four?main ideas that came out of those articles:

Saudi Arabia would allow the price of crude oil to fall to hurt competitors/rivals, particularly Iran.

The price of crude oil would stay near $50/barrel.

Lots of overlevered companies dependent on a high price for crude oil would go bankrupt.

But?bankruptcy would happen to fewer, and more slowly, because of all the private equity wanting to buy distressed assets.

All that said, my view has changed a little recently. ?I could be wrong, but I think that the ceiling price for crude oil may be $70/barrel for a few years, with the average remaining at $50. ?I believe this because I think the Saudis are more desperate for cash than most believe.

Here’s my reasoning:

First, you have them selling off a?5%?interest in Saudi Aramco. ?When you need?money, there is a tendency to sell high quality easily saleable assets, because they will sell for a high price, and with little fuss. ?Admittedly, they aren’t rushing to do it, which weakens my point. ?My view is that you would sell off lesser things that aren’t core, rather than complicate life by selling off a portion of a top quality asset.

Fifth, and most speculatively, I wonder if many of the US Treasury holdings have been pledged to cover other debts. ?No proof here, but it’s not uncommon to use highly liquid assets as collateral for privately contracted debts. ?That may explain the musing by some that there had to be more US Treasuries ?there… but where are they?

What this implies to me is that Saudi Arabia is now little different than most of their associates in OPEC. ?Their financial situation is tight enough that they must pump crude oil without respect?to the strategy of holding crude oil off the markets to get better prices. ?It’s not just punishing US shale oil production and Iranian crude production — the Saudis need the money.

If the Saudis need the money, and must pump, then OPEC lacks any significant coalition to raise prices. ?Prices will rise with growth in demand, and cheap resource depletion… but as for right now, there are enough barrels to come out of the ground below $70.

The Saudi need for money is a much simpler explanation than trying to knock out US shale oil, or gouge the Iranians, because it has the Saudis acting directly in their own interests, and it fits the price series for crude oil better.

PS — One more note: this is mildly bearish for the US Dollar as the US does not have the same dedicated buyer of US Dollar assets as it once did. ?I say mildly bearish, because most of the damage is already past.