I’m thinking of starting a limited series called “dirty secrets” of finance and investing. ?If anyone wants to toss me some ideas you can contact me here. ?I know that since starting this blog, I have used the phrase “dirty secret” at least ten times.

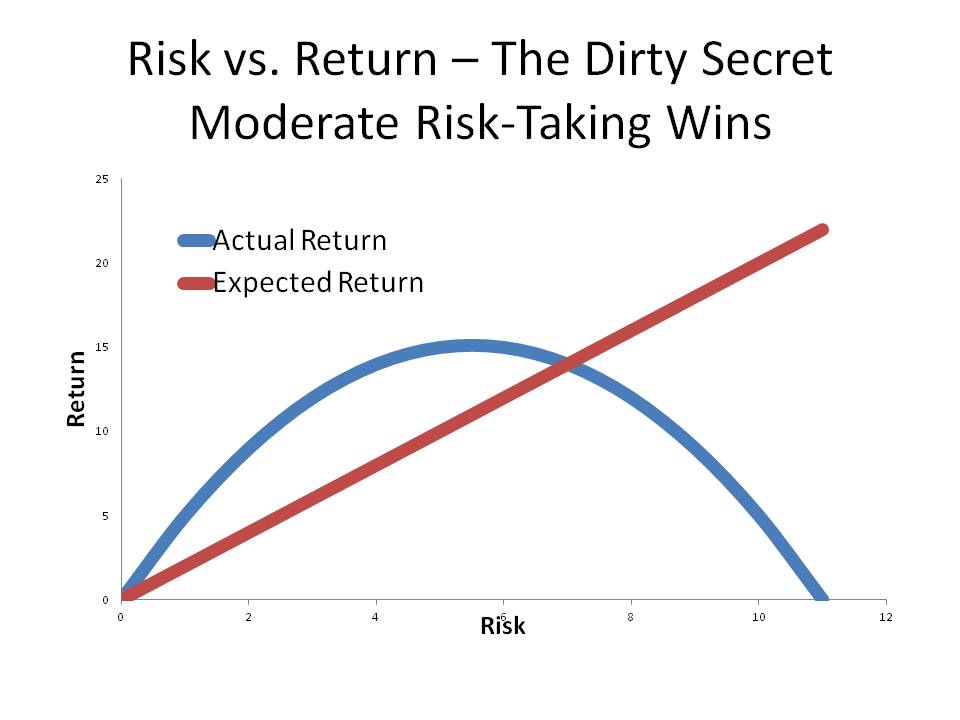

Tonight’s dirty secret is a simple one, and it derives mostly from investor behavior. ?You don’t always get more return on average if you take more risk. ?The amount of added return declines with each unit of additional risk, and eventually turns negative at high levels of risk. ?The graph above is a vague approximate representation of how this process works.

Why is this so? ?Two related reasons:

People are not very good at estimating the probability of success for ventures, and it gets worse as the probability of success gets lower. ?People overpay for chancy lottery ticket-like investments, because they would like to strike it rich. ?This malady affect men more than women, on average.

People get to investment ideas late. ?They buy closer to tops than bottoms, and they sell closer to bottoms than tops. ?As a result, the more volatile the investment, the more money they lose in their buying and selling. ?This malady also affects men more than women, on average.

Put another way, this is choosing your investments based on your circle of competence, such that your probability of choosing a good investment goes up, and second, having the fortitude to hold a good investment through good and bad times. ?From my series on dollar-weighted returns you know that the more volatile the investment is, the more average people lose in their buying and selling of the investment, versus being a buy-and-hold investor.

Since stocks are a long duration investment, don’t buy them unless you are going to hold them long enough for your thesis to work out. ?Things don’t always go right in the short run, even with good ideas. ?(And occasionally, things go right in the short run with bad ideas.)

For more on this topic, you can look at my creative piece,?Volatility Analogy. ?It explains the intuition behind how volatility affects the results that investors receive as they get greedy, panic, and hold on for dear life.

In closing, the dirty secret is this: size your risk level to what you can live with without getting greedy or panicking. ?You will do better than other investors who get tempted to make rash moves, and act on that temptation. ?On average, the world belongs to moderate risk-takers.

A: I dealt mainly with investment grade credit. ?What’s more, I had a real balance sheet behind me at the life insurance company. ?An ordinary open-end mutual fund has investors that can leave whenever they want — often at the worst possible time for them, or in this case, those that could not get out.

The main difference was that I could never be forced to sell, under most conditions. ?I could buy and hold, and if the eventual credit of the borrower was good, my client would receive all that he expected. ?TFCIX faced significant redemptions, and increasingly had mostly bonds that could not be quickly sold, and thus, were difficult to value. ?That’s why they cut off redemptions — they couldn’t?liquidate assets to give cash to customers on a favorable basis. ?Personally, I think setting up the liquidation trust was the best that could be done. ?That will allow Third Avenue to negotiate with interested buyers of the bonds without being rushed by redemptions. ?The remaining fundholders should be grateful for them doing this now, though it would have been better to act sooner.

Q: But I own shares in?TFCIX and need the money now. ?What can I do?

A: Oh, my. ?My sympathies. ?You can’t do?much. ?There might be some off the beaten track lenders out there that might take it off your hands, but they wear “panky rangs,” as a mortgage borrower once said to me.

Q: Panky Rangs?

A: Pinky rings. ?He was from the deep South. ?I.e., no one is going to give you a decent bid for your shares, even if you could find someone willing to do so. ?First, the value of the bonds is questionable, and the timing of the sales are?uncertain.

A: JP Morgan became too great of a part of the indexed credit derivatives market, and as a result, they lost the ability to value their positions, because they were too big relative to the market in which they traded. ?Their very buying and selling had a huge impact on the pricing. ?Though a value was placed on the positions, the entire situation was impossible to value accurately; ?you couldn’t assemble a group to buy it all.

Some clever hedge funds took note of it, and began taking the opposite positions, thinking that they were overvalued, and fed JP Morgan more of what it was already bloated with. ?Now maybe, if there hadn’t been so much press furor over it, together with the accounting questions that affected the financials of JP Morgan, they could have found a way out. ?JP Morgan’s balance sheet was big enough, and if you left them alone, they would have all self -liquidated. ?They might not have made the money they wanted that way, but it could have been done. ?As it was, they were forced to liquidate more rapidly, and if I recall, they even called upon one of the opposing hedge funds to help them.

In any case, the forced liquidation led to losses. ?Most forced liquidations do.

Q: So, what do think my shares are worth?

A: They are worth the liquidating distributions that you will receive.

Q: That’s no help.

A: Is the Federal Reserve willing to step up and buy the assets as they did with?the Maiden Lane Trusts? ?No one has a bigger balance sheet than they do, oh, oops. ?Maybe they can’t do that anymore… who know where those emergency lending rules go…

Look, I’m sorry that you are stuck. ?The Madoff “investors” were stuck also. ?They had to wait quite a while. ?In the end, they got paid more than most imagined they ever would. ?Subject to credit conditions,?I would suspect that the more time Third Avenue takes to liquidate, the more you will get.

Q: But that’s dribs and drabs over time, and I need it now.

A: Patience is a virtue. ?Make other adjustments; sell something else; scale back plans… it’s no different than most people have to do when they have a loss. ?It happens.

Q: I guess… but it would help to know what it was worth, so that I could estimate tradeoffs.

A: yes, it would, but the timing and amount of liquidations are uncertain, and the “market prices” don’t really exist for the underlying — they are too influenced by Third Avenue’s holdings.

Maybe they could have converted it into a closed-end fund, ?but that would have cost money, and there still would have been the valuation issue. ?People could have gotten paid now if that had happened, but I bet they would have blanched at the size of the unrealized losses. ?I would just accept the payments as they come, that will probably give the best return, subject to future credit conditions.

A: An asset is worth whatever the highest bidder will pay for it at the time you offer it for sale.

After all, if it is worth the liquidating distributions if I wait, maybe you should add, “or the cash flows you receive over time.”

A: I will do that, and that is part of what I have been arguing for here, but the price here and now is not that. ?Just because you can’t sell it now doesn’t mean it doesn’t have value… we just don’t know what that value is.

Anyway, lunch is on me today, because there is another thing that you can’t sell that has value.

This post was triggered by a guy from the UK who sent me an infographic on reducing risk that I thought was mediocre at best. ?First, I don’t like infographics or video. ?I want to learn things quickly. ?Give me well-written text to read. ?A picture is worth maybe fifty words, not a thousand, when it comes to business writing, perhaps excluding some well-designed graphs.

Here’s the problem. ?Do you want to reduce?the volatility of your asset portfolio? ?I have the solution for you. ?Buy bonds and hold some cash.

And some say to me, “Wait, I want my money to work hard. ?Can’t you find investments that offer a higher return that diversify my portfolio of stocks and other risky assets?” ?In a word the answer is “no,” though some will tell you otherwise.

Now once upon a time, in ancient times, prior to the Nixon Era, no one hedged, and no one looked for alternative investments. ?Those buying stocks stuck to well-financed “blue chip” companies.

Some clever people realized that they could take risk in other areas, and so they broadened their stock exposure to include:

Growth stocks

Midcap stocks (value & growth)

Small cap stocks (value & growth)

REITs and other income passthrough vehicles (BDCs, Royalty Trusts, MLPs, etc.)

Developed International stocks (of all kinds)

Emerging Market stocks

Frontier Market stocks

And more…

And initially, it worked. ?There was significant diversification until… the new asset subclasses were crowded with institutional money seeking the same things as the original diversifiers.

Now, was there no diversification left? ?Not much. ?The diversification from investor behavior is largely gone (the liability side of correlation). ?Different sectors of the global economy don’t move in perfect lockstep,?so natively the return drivers of the assets are 60-90% correlated (the asset side of correlation, think of how the cost of capital moves in a correlated way across companies). ?Yes, there are a few nooks and crannies that are neglected, like Russia and Brazil, industries that are deeply out of favor like gold, oil E&P, coal, mining, etc., but you have to hold your nose and take reputational risk to buy them. ?How many institutional investors want to take a 25% chance of losing a lot of clients by failing unconventionally?

Why do I hear crickets? ?Hmm…

Well, the game wasn’t up yet, and those that pursued diversification pursued alternatives, and they bought:

Timberland

Real Estate

Private Equity

Collateralized debt obligations of many flavors

Junk bonds

Distressed Debt

Merger Arbitrage

Convertible Arbitrage

Other types of arbitrage

Commodities

Off-the-beaten track bonds and derivatives, both long and short

And more… one that stunned me during the last bubble was leverage nonprime commercial paper.

Well guess what? ?Much the same thing happened here as happened with non-“blue chip” stocks. ?Initially, it worked. ?There was significant diversification until… the new asset subclasses were crowded with institutional money seeking the same things as the original diversifiers.

Now, was there no diversification left? ?Some, but less. ?Not everyone was willing to do all of these. ?The diversification from investor behavior was reduced?(the liability side of correlation). ?These don’t move in perfect lockstep,?so natively the return drivers of the risky components of the assets are 60-90% correlated over the long run (the asset side of correlation, think of how the cost of capital moves in a correlated way across companies). ?Yes, there are some?that are neglected, but you have to hold your nose and take reputational risk to buy them, or sell them short. ?Many of those blew up last time. ?How many institutional investors want to take a 25% chance of losing a lot of clients by failing unconventionally?

Why do I hear crickets again? ?Hmm…

That’s why I don’t think there is a lot to do anymore in diversifying risky assets beyond a certain point. ?Spread your exposures, and do it intelligently, such that the eggs are in baskets are different as they can be, without neglecting the effort to buy attractive assets.

But beyond that, hold dry powder. ?Think of cash, which doesn’t earn much or lose much. ?Think of some longer high quality bonds that do well when things are bad, like long treasuries.

Remember, the reward for taking business risk in general varies over time. ?Rewards are relatively thin now, valuations are somewhere in the 9th decile (80-90%). ?This isn’t a call to go nuts and sell all of your risky asset positions. ?That requires more knowledge than I will ever have. ?But it does mean having some dry powder. ?The amount is up to you as you evaluate your time horizon and your opportunities. ?Choose wisely. ?As for me, about 20-30% of my total assets are safe, but I?have been a risk-taker most of my life. ?Again, choose wisely.

PS — if the low volatility anomaly weren’t overfished, along with other aspects of factor investing (Smart Beta!) those might also offer some diversification. ?You will have to wait for those ideas to be forgotten. ?Wait to see a few fund closures, and a severe reduction in AUM for the leaders…

This book is not what I expected; it’s still very good. Let me explain, and it will give you a better flavor of the book.

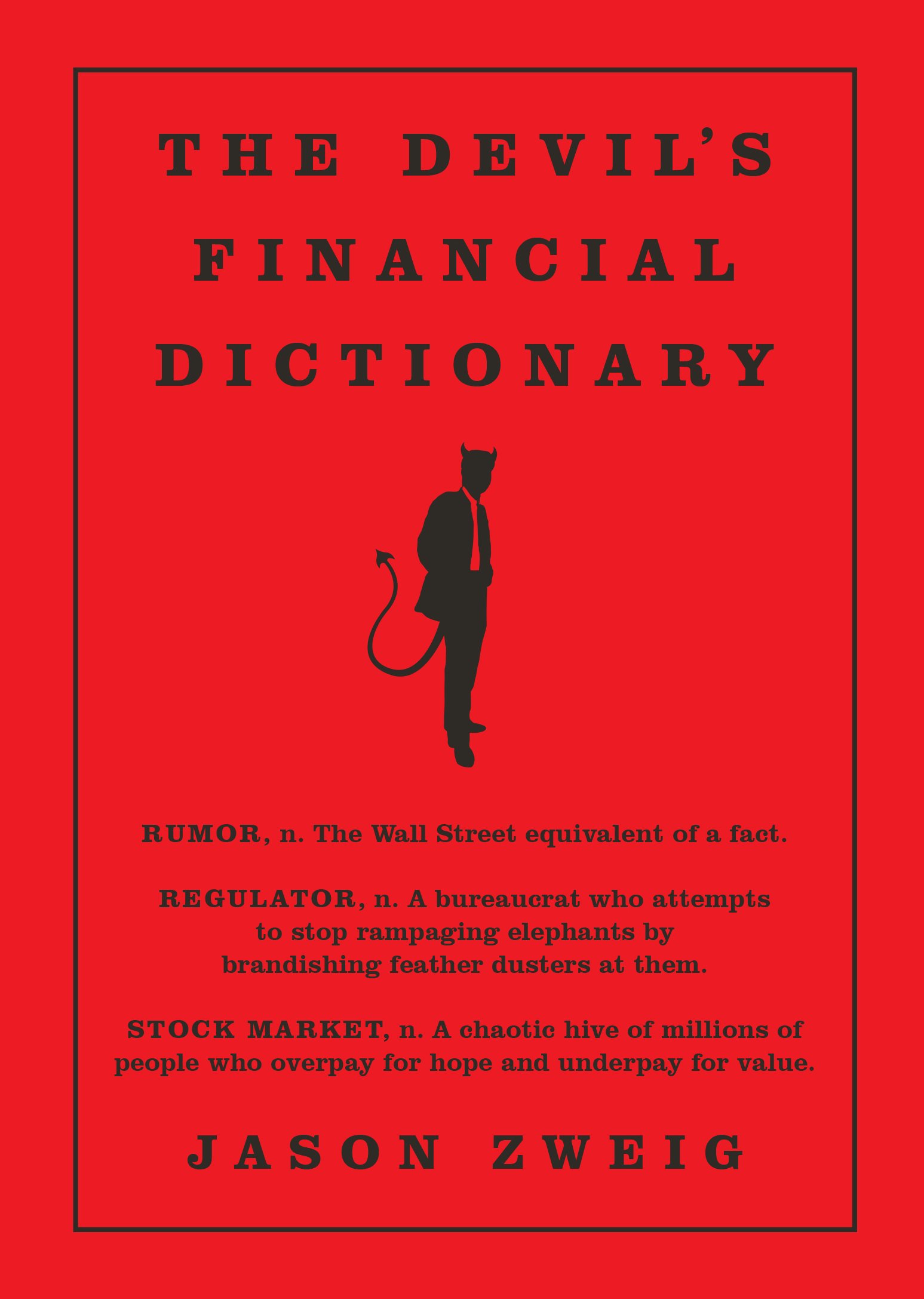

The author, Jason Zweig, is one of the top columnists writing about the markets for The Wall Street Journal. ?He is very knowledgeable, properly cautious, and wise. ?The title of the book Ambrose Bierce’s book that is commonly called The Devil’s Dictionary.

There are three differences in style between Zweig and Bierce:

Bierce is more cynical and satiric.

Bierce is usually shorter in his definitions, but occasionally threw in whole poems.

Zweig spends more time explaining the history of concepts and practices, and how words evolved to mean what they do today in financial matters.

If you read this book, will you learn a lot about the markets? ?Yes. ?Will it be fun? ?Also yes. ?Is it enough to read this and be well-educated? ?No, and truly, you need some knowledge of the markets to appreciate the book. ?It’s not a book for novices, but someone of intermediate or higher levels of knowledge will get some chuckles out of it, and will nod as he agrees along with the author that the markets are a treacherous place disguised as an easy place to make money.

As one person once said, “Whoever called them securities had a wicked sense of humor.” ?Enjoy the book; it doesn’t take long to read, and it can be put down and picked up with no loss of continuity.

Quibbles

None

Summary / Who Would Benefit from this Book

If you have some knowledge of the markets, and you want to have a good time seeing the?wholesome image of the markets?skewered, you will enjoy this book. ?if you want to buy it, you can buy it here: The Devil’s Financial Dictionary.

Full disclosure:?The author sent a free copy?to me via his publisher.

If you enter Amazon through my site, and you buy anything, including books, I get a small commission. This is my main source of blog revenue. I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip. Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book. Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website. Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites. Whether you buy at Amazon directly or enter via my site, your prices don?t change.

WESLEY GRAY: Imagine the following theoretical investment opportunity: Investors can invest in a fund that will beat the market by 5% a year over the next 10 years. Of course, there is the catch: The path to outperformance will involve a five-year stretch of poor relative performance.? ?No problem,? you might think?buy and hold and ignore the short-term noise.

Easier said than done.

Consider Ken Heebner, who ran the CGM Focus Fund, a diversified mutual fund that gained 18% annually, and was Morningstar Inc.?s highest performer of the decade ending in 2009. The CGM Focus fund, in many respects, resembled the theoretical opportunity outlined above. But the story didn?t end there: The average investor in the fund lost 11% annually over the period.

What happened? The massive divergence in the fund?s performance and what the typical fund investor actually earned can be explained by the ?behavioral return gap.?

The behavioral return gap works as follows: During periods of strong fund performance, investors pile in, but when fund performance is at its worst, short-sighted investors redeem in droves. Thus, despite a fund?s sound long-term process, the ?dollar-weighted? returns, or returns actually achieved by investors in the fund, lag substantially.

In other words, fund managers can deliver a great long-term strategy, but investors can still lose.

That’s why I wanted to write this post. ?Ken Heebner is a really bright guy, and has the strength of his convictions, but his investors don’t in general have similar strength of convictions. ?As such, his investors buy high and sell low with his funds. ?The graph at the left is from the CGM Focus Fund, as far back as I could get the data at the SEC’s EDGAR database. ?The fund goes all the way back to late 1997, and had a tremendous start for which I can’t find the cash flow data.

The column marked flows corresponds to a figure called “Change in net assets derived from capital share transactions” from the Statement of Changes in Net Assets in the annual and semi-annual reports. ?This is all public data, but somewhat difficult to aggregate. ?I do it by hand.

I use annual cashflows for most of the calculation. ?For the buy and hold return, i got the data from Yahoo Finance, which got it from Morningstar.

Note the pattern of cashflows is positive until?the financial crisis, and negative thereafter. ?Also note that more has gone into the fund than has come out, and thus the average investor has lost money. ?The buy-and-hold investor has made money, what precious few were able to do that, much less rebalance.

This would be an ideal fund to rebalance. ?Talented manager, will do well over time. ?Add money when he does badly, take money out when he does well. ?Would make a ton of sense. ?Why doesn’t it happen? ?Why doesn’t at least buy-and-hold happen?

It doesn’t happen because there is a Asset-Liability mismatch. ?It doesn’t matter what the retail investors say their time horizon is, the truth is it is very short. ?If you underperform for less?than a few years, they yank funds. ?The poetic justice is that they yank the funds just as the performance is about to turn.

Practically, the time horizon of an average investor in mutual funds is inversely proportional to the volatility of the funds they invest in. ?It takes a certain amount of outperformance (whether relative or absolute) to get them in, and a certain amount of underperformance to get them out. ?The more volatile the fund, the more rapidly that happens. ?And Ken Heebner is so volatile that the only thing faster than his clients coming and going, is how rapidly he turns the portfolio over, which is once every 4-5 months.

Pretty astounding I think. ?This highlights two main facts about retail investing that can’t be denied.

Asset prices move a lot more than fundamentals, and

Most investors chase performance

These two factors lie behind most of the losses that retail investors suffer over the long run, not active management fees. ?remember as well that passive investing does not protect retail investors from themselves. ?I have done the same analyses with passive portfolios — the results are the same, proportionate to volatility.

I know buy-and-hold gets a bad rap, and it is not deserved. ?Take a few of my pieces from the past:

If you are a retail investor, the best thing you can do is set an asset allocation between risky and safe assets. ?If you want a spit-in-the-wind estimate use 120 minus your age for the percentage in risky assets, and the rest in safe assets. ?Rebalance to those percentages yearly. ?If you do that, you will not get caught in the cycle of greed and panic, and you will benefit from the madness of strangers who get greedy and panic with abandon. ?(Why 120? ?End of the mortality table. 😉 Take it from an investment actuary. 😉 We’re the best-kept secret in the financial markets. 😀 )

Okay, gotta close this off. ?This is not the last of this series. ?I will do more dollar-weighted returns. ?As far as retail investing goes, it is the most important issue. ?Period.

How can a book be largely true, but not be a good book? ?By offering people a way to make a lot of money that is hard to do, but portraying it as easy. ?It can be done, and a tiny number succeed at it, but most of the rest lose money or don’t make much in the process. ?This is such a book.

Let me illustrate my point with an example. ?Toward the end of every real estate bull market, books come out on how easy it is to make money flipping homes. ?The books must sell to some degree or the publishers wouldn’t publish them. ?Few actually succeed at it because:

It’s a lot of work

It’s competitive

It only works well when you have a bunch of people who are uneducated about the value of their homes and are willing to sell them to you cheap, and/or offer you cheap financing while you reposition it.

Transaction costs are significant, and improvements don’t always pay back what you put in.

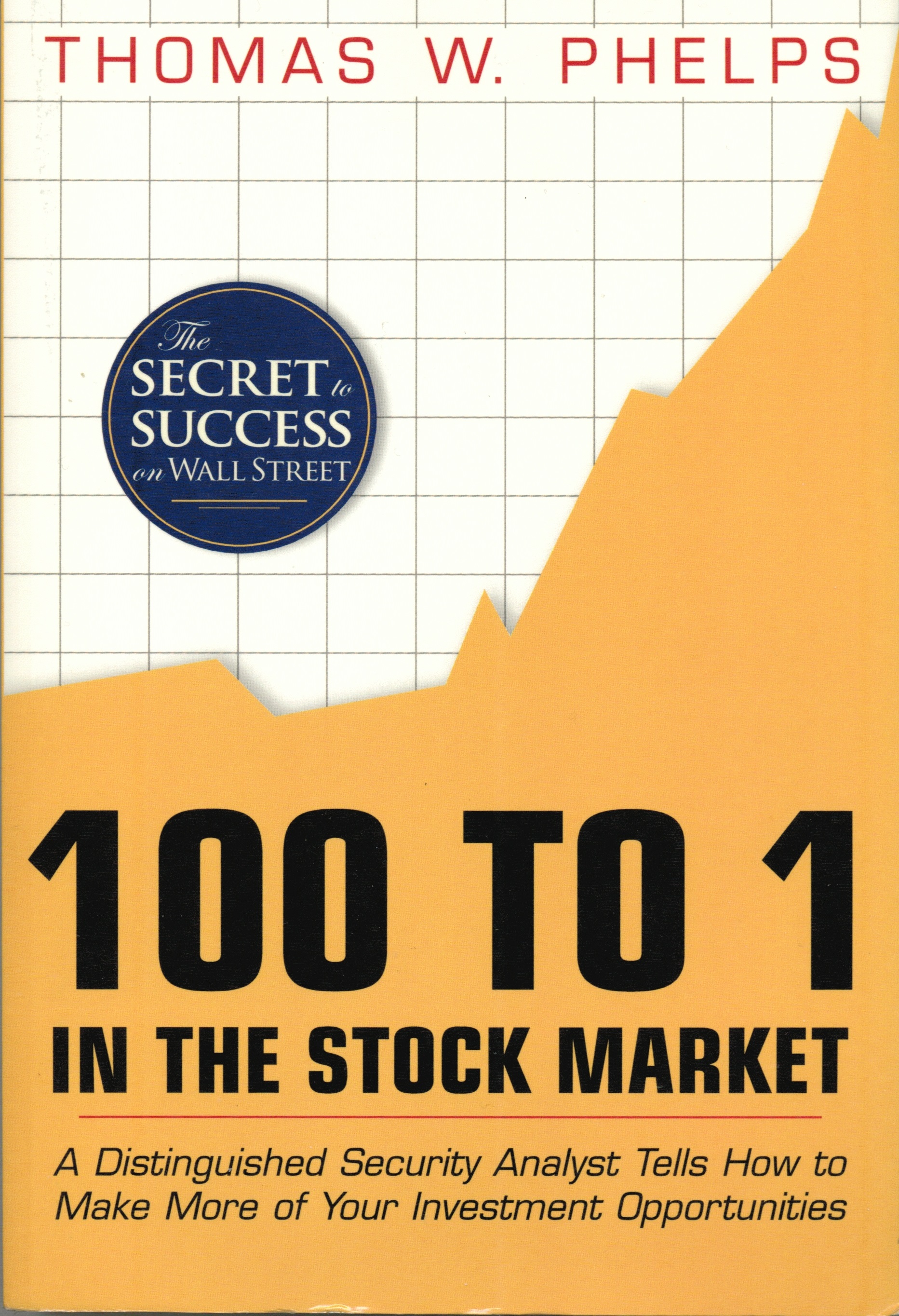

You could make a lot of money at it, but it is unlikely. ?Now with this book, “100 to 1 in the Stock Market,” the value proposition is a little different:

Find one company that will experience stunning compound growth over 20-30+ years.

Invest heavily in it, and don’t diversify into a lot of other stocks, because that will dilute your returns.

Hold onto it, and don’t sell any ever, ever, ever! ?(Forget Lord Rothschild, who said the secret to his wealth was that he always sold too soon.)

Learn to mention the company name idly in passing, and happily live off of the dividends, should there be any. 😉

Here are the problems. ?First, identifying the stock will be tough. ?Less than 1% of all stocks do that. ?Are you feeling lucky? ?How lucky? ?That lucky? ?Wow.

Second, most people will pick a dog of a stock, and lose a lot of money. ?If you aren’t aware, more than half of all stocks lose money if held for a long time. ?Most of the rest perform meh. ?Even if you pick a stock you think has a lot of growth potential, there is often a lot of competition. ?Will this be the one to survive? ?Will some new technology obsolete this? ?Will financing be adequate to let the plan get to fruition without a lot of dilution of value to stockholders.

Third, most people can’t buy and hold a single stock, even if it is doing really well. ?Most succumb to the temptation to take profits, especially when the company hits a rough patch, and all companies hit rough patches, non excepted.

Fourth, when you do tell friends about how smart you are, they will try to dissuade you from your position. ?So will the financial media, even me sometimes. ?As Cramer says, “the bear case always sounds more intelligent.” ?Beyond that, never underestimate envy. 🙁

But suppose even after reading this, you still want to be a home run hitter, and will settle for nothing less. ?Is this the book for you? ?Yes. ?it will tell you what sorts of stocks appreciate by 100 times or more, even if finding them will still be rough.

This book was written in 1972, so it did not have the benefit of Charlie Munger’s insights into the “Lollapalooza” effect. ?What does it take for a stock to compound so much?

It needs a sustainable competitive advantage. ?The company has to have something critical that would be almost impossible for another firm to replicate or obsolete.

It needs a very competent management team that is honest, and shareholder oriented, not self-oriented.

They have to have a balance sheet capable of funding growth, and avoiding crashing in downturns, while rarely issuing additional shares.

It has to earn a high return on capital deployed.

It has to be able to reinvest earnings such that they earn a high return in the business over a long period of time.

That means the opportunity has to be big, and can spread like wildfire.

Finally, it implies that not a lot of cash flow needs to be used to maintain the investments that the company makes, leaving more money to invest in new assets.

You would need most if not all of these in order to compound capital 100 times. ?That’s hard. ?Very hard.

Now if you want a lighter version of this, a reasonable alternative, look at some of the books that Peter Lynch wrote, where he looked to compound investments 10 times or more. ?Ten-baggers, he called them. ?Same principles apply, but he did it in the context of a diversified portfolio. ?That is still very tough to do, but something that mere mortals could try, and even if you don’t succeed, you won’t lose a ton in the process.

Quibbles

Already given.

Summary / Who Would Benefit from this Book

You can buy this book to enjoy the good writing, and learn about past investments that did incredibly well. ?You can buy it to try to hit a home run against a major league pitcher, and you only get one trip to the plate. ?(Good luck, you will need it.)

But otherwise don’t buy the book, it is not realistic for the average person to apply in investing. ?if you still want to buy it, you can buy it here: 100 to 1 in the Stock Market.

Full disclosure:?I bought it with my own money. ?May all my losses be so small.

If you enter Amazon through my site, and you buy anything, including books,?I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

This is a story of triumph and tragedy. ?Jesse Livermore is notable as one of the few people who ever made it into the richest tiers of society by speculating — by trading stocks and commodities — betting on price movements.

This is three stories in one. ?Story one is the clever trader with an intuitive knack who learned to adapt when conditions changed, until the day came when it got too hard. ?Story two is the man who lacked financial risk control, and took big chances, a few of which worked out spectacularly, and a few of ruined him financially. ?Story three is how too much success, if not properly handled, can ruin a man, with lust, greed and pride leading to his death.

The author spends most of his time on story one, next most on story two, then the least on story?three. ?The three stories flow naturally from the narrative that is largely chronological. ?By the end of the book, you see Jesse Livermore — a guy who did amazing things, but?ultimately failed in money and life.

Let me briefly summarize those three aspects of his life so that you can get a feel for what you will run into in the book:

The Clever Trader

Jesse Livermore came to the stock market in Boston at age 14, and was a very quick study. ?He showed intuition on market affairs that impressed the most of the older men who came to trade at the brokerage where he worked. ?It wasn’t too long before he wanted to invest for himself, but he didn’t have enough money to open a brokerage account, so he went to a bucket shop. ?Bucket shops were gambling parlors where small players gambled on stock prices. ?He showed a knack for the game and made a lot of money. ?Like someone who beats the casinos in Vegas, the proprietors forced him to leave.

He then had more than enough money to meet his current needs, and set up a brokerage account. ?But the stock market did not behave like a bucket shop, and so he lost money while he learned to adapt. ?Eventually, he succeeded at speculating on both stocks and commodities, leading to his greatest successes in being short the stock market prior to the panic of 1907, and the crash in 1929. ?During the 1920s, he started his own firm to try to institutionalize his gifts, and it worked for much of the era.

After the crash in 1929, the creation of the SEC and all the associated laws and regulations made speculating a lot more difficult, to the point where he could not make significant money speculating anymore.

The Poor Financial Risk Manager

Amid the successes, he tended to aim for greater wins after his largest successes, which led to him losing much of what he had previously made. ?One time he was cheated out of much of what he had while trading cotton.

Amid all of that, he was well-liked by most he interacted with in a business context. ?Even after great losses, many wanted him to succeed again, and so they bankrolled him after failure. ?Before?the Great Depression, he did not disappoint them — he succeeded in speculation and came roaring back, repaying all of his past debts with interest.

In one sense, it was live by the big speculation, and?die by the big speculation. ?When you play with so much borrowed money, it’s hard for results to not be volatile.

A?Rock Star of His Era

When he won big, he lived big. ?Compared to many wealthy people of his era, he let spending expand far more than many who had ?more reliable sources of income. ?Where did the money go? ?Yachts, homes, staff, wives, women, women, women… ?Aside from the last of his three wives, his marriages were troubled.

His last wife was a nice woman who was independently wealthy, and after Livermore lost?it all in the mid-’30s, he increasingly relied on her to stay afloat. ?When he could no longer be the hero who could win a good living out of the market via speculation, his deflated pride led him to commit suicide in 1940.

A Sad Book Amid Amazing Successes

Sadly, his son and grandson who shared his name committed suicide in 1975 and 2006, respectively. ?On the whole, the story of Jesse Livermore’s?life and legacy is a sad one. ?It should disabuse people of the notion that wealth?brings happiness. ?If anything, it teaches that money that comes too easily tends to get lost easily also.

The author does a good job?weaving the strands of his life into a consistent whole. ?The book is well-written, and probably the best book out there on the life of the famous speculator that so many present speculators admire. ?A side benefit is that in passing, you will learn a lot about the development of the markets during a time when they were less regulated. ?(The volatility of markets was obvious then. ?It not obvious now, which is why people get surprised by it when it explodes.)

Quibbles

None.

Summary / Who Would Benefit from this Book

This is a comprehensive book that explains?the life and times of Jesse Livermore, one of the greatest speculators in history. ?It will teach you history, but it won’t teach you how to speculate. ?If you want to buy it, you can buy it here: Jesse Livermore – Boy Plunger: The Man Who Sold America Short in 1929.

Full disclosure:?I?received a?copy from a kind PR flack.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

The following may be controversial. It also may be dull to the point that you might not care. Here’s why you should care: quarterly reporting is a useful and productive use of corporate resources, and it would be a shame to lose it because some people with a patina of intelligence think it is harmful. Who knows? Losing it might even make you poorer.

Influential law firm Wachtell, Lipton, Rosen & Katz has an idea that may be music to the ears of its big corporate clients and a nightmare for some investors and analysts: end quarterly earnings reports.

Wachtell on Tuesday called on the Securities and Exchange Commission to consider allowing U.S. companies to do away with the obligatory updates, one of the most important rituals on Wall Street and in corporate America, suggesting that they distract executives from long-term goals.

The basic case is that quarterly earnings lead companies to behave in a short-term manner, and underinvest for longer-term growth, thus hurting the US economy. ?I disagree. There are at least four?things that are false in the arguments made in the article, and in books like?Saving Capitalism from Short-Termism:

Quarterly earnings don’t produce value in and of themselves

Quarterly earnings cause most corporations to ignore the long-term.

Ending quarterly earnings will end activism, buybacks, and dividends.

Buybacks and dividends are bad uses of capital, and more capital investment, especially for long-dated projects, is necessarily a good thing.

Most of the value of a Corporation on a going concern basis stems from the future earnings of the company.? Investors want to have an estimate of forward earnings so that they can gauge whether the company is growing at an appropriate rate.

Now, it wouldn?t matter if the system were set up by third-party sell side analysts, by buyside analysts, by companies themselves, or by a combination thereof.? The thing is investors are forward-looking, and they want a forward-looking estimate to allow them to estimate whether the companies are doing well with their current earnings or not.

Don’t think of the quarterly earnings in isolation. ?A good or bad quarterly earnings number conveys information not about the current period only, but about all future periods. ?A bad earnings number?lowers the estimates of all future earnings, telling market players that the long-term efforts of the company are not going to be so great. ?Vice-versa for a good number.

Now, in some cases, that might not be true, and the management team will say, “But we still expect our future earnings to reach the levels that we expected before this quarter.” ?That still leaves the problem of getting to the high future earnings, which if missed will lead the market to reprice the stock down.

They might also use a non-GAAP measure of earnings to explain that earnings are not as bad as they might seem. ?In the short-run the market may accept that, but if you do that often enough, eventually the markets factor in the many “one-time” adjustments, and lower the earnings multiple on the stock to reflect the reduced quality of earnings.

In addition, having shorter-term targets causes corporations to not get lazy in managing expenses and capital. ?When the measurement periods get too long, discipline can be lost.

Quarterly Earnings Don’t Cause Most Firms to Neglect the Long-Term

Firms aren’t interested in only the current period’s earnings, but about the entire future path of earnings. ?Even if?the current period’s earnings meet the estimates, the job is not done. ?If there aren’t plans to grow earnings for the next 3-5 years, eventually earnings won’t meet the expectations of investors, and the price of the stock will fall. ?The short-term is just the beginning of the long-term. ?It is not either/or but both/and. ?A company has to try to explain to investors how it is?growing the value of the firm — if present targets aren’t being met, why should there be any confidence that the future will be good?

Think of corporate earnings like a long-term project which has a variety of things that have to be done en route to a significant goal. ?The quarterly earnings measure?whether the progress toward completing the goal is adequate or not. ?Now, the measure is not perfect, but who can think of a better one?

Ending Quarterly Earnings Would Not?End Activism, Buybacks, and Dividends

I can think of an area in business where earnings estimates don’t play a role — private equity. ?Are the owners long-term oriented? Yes. ?Are they short-term oriented? ?Yes. ?Is?capital managed tightly? ?Very tightly. ?All excess capital is dividended back — it as if activists run the firms permanently.

If there were no quarterly earnings in the public equity markets, firms would still be under pressure to return excess capital to shareholders. ?Activists would still analyze companies to see if they are badly managed, and in need of change. ?If anything, when companies would release their earnings less frequently, the adjustments to the market price of the stock would be more severe. ?Companies that disappoint would find the activists arriving regardless of the periodicity of the release of earnings.

On the Use of Excess Capital

Investing, particularly for the long-term, is not risk-free. ?In an environment where there is rapid technological change, like there is today, it is difficult to tell what investments will not be made obsolete. ?In such an environment, it can make a lot of sense to focus on shorter-term?investments that are more certain as to the success of the project. ?It is also a reason why dividends and buybacks are done, as capital returned to shareholders is associated with higher stock prices, because the capital is used more efficiently. ?Companies that shrink their balance sheets tend to outperform those that grow them.

As an example, large acquisitions tend not to benefit shareholders, while small acquisitions that lead to greater organic growth do tend to benefit investors. ?The same is true of large versus small investments for organic growth away from M&A. ?Most management teams can adequately estimate and plan for the growth that stems from incremental action. Large revolutionary investments are another thing. ?There is usually no way to estimate how those will work out, and whether the prospects are reasonable or not.

In one sense, it’s best to leave those kinds of investment projects to highly focused firms that do only that. ?That’s how biotech firms work, and it is why so many of them fail. ?The few winners are astounding.

Or, think about how progressive Japanese firms were viewed to be in the 1980s, as they pursued long-term projects that had very low returns on equity. ?All of that failed, to a first approximation, while the derided American model of shareholder capitalism prospered, as capital was used efficiently on projects with high risk-adjusted?returns, and not wasted on speculative projects with uncertain returns. ?The same will prove true of China over the next 20 years as they choke on all of their bad investments that yield low returns, if indeed the returns are positive.

Remember, bad investments are just expenses in fancy garb — it just takes the accounting longer to recognize the losses. ?Think of Enron if you need an example, which brings up one more point: good investing focuses on accounting quality. ?Accrual items on the asset side of the balance sheets of corporations get higher valuations the shorter the accrual is, and the more likely it is to produce cash. ?Most long term projects tend to be speculative, and as such, drag down the valuation of the stock, because in most cases, it lowers the long-term earnings of the company.

Conclusion

If quarterly earnings are abolished, intelligent corporations won’t change much. ?Investment won’t go up much, and the time horizon of most management teams will not rise much. ?If you need any proof of that, look at how private equity and large mutual insurers manage their firms — they still analyze quarterly results, and are conservative in how they deploy capital.

The only great change of eliminating quarterly earnings will be a loss of quality information for equity investors. ?Bond investors and banks will still require more frequent financial updates, and equity investors may try to find ways to get that data, perhaps through the rating agencies.

I’m currently reading a book about the life of Jesse Livermore. ?Part of the book describes how Livermore made a fortune shorting stocks just before the panic of 1907 hit. ?He had one key insight: the loans of lesser brokers were being funded by the large brokers, and the large brokers were losing confidence in the creditworthiness of the lesser brokers, and banks were now funding the borrowings by the lesser brokers.

What Livermore didn’t know was that the same set of affairs existed with the banks toward trust companies and smaller banks. ?Most financial players were playing with tight balance sheets that did not have a lot of incremental borrowing power, even considering the lax lending standards of the day, and the high level of the stock market. ?Remember, in those days, margin loans required only 10% initial equity, not the 50% required today. ?A modest move down in the stock market could create a self-reinforcing panic.

All the same, he was in the right place at the right time, and repeated the performance in 1929 (I’m not that far in the book yet). ?In both cases you had a mix of:

High leverage

Short lending terms with long-term assets (stocks) as collateral.

Chains of lending where party A lends to party B who lends to party C who lends to party D, etc., with each one trying to make some profit off the deal.

Inflated asset values on the stock collateral.

Inadequate loan underwriting standards at many trusts and banks

Inadequate solvency standards for regulated financials.

A culture of greed ruled the day.

Now, this is not much different than what happened to Japan in the late 1980s, the US in the mid-2000s, and China today. ?The assets vary, and so does the degree and nature of the lending chains, but the overleverage, inflated assets, etc. were similar.

In all of these cases, you had some institutions that were leaders in the nuttiness that went belly-up, or had significant problems in advance of the crisis, but they were dismissed as one-time events, or mere liquidity and not solvency problems — not something that was indicative of the system as a whole.

Those were the warnings — from the recent financial crisis we had Bear Stearns, the failures in short-term lending (SIVs, auction rate preferreds, ABCP, etc.), Bank of America, Citigroup, credit problems at subprime lenders, etc.

I’m not suggesting a credit crisis now, but it is useful to keep a list of areas where caution is being thrown to the wind — I can think of a few areas: student loans, agricultural loans, energy loans, lending to certain weak governments with large liabilities and no independent monetary policy… there may be more — can you think of any? ?Leave a comment.

Subprime lending is returning also, though not in housing yet…

Parting Thoughts

I’ve been toying with the idea that maybe there would be a way to create a crisis model off of the financial sector and its clients, working off of a “how much slack capital exists across the system” basis. ?Since risky?borrowers vary over time, and some lenders are more prudent than others, the model would have to reflect the different links, and dodgy borrowers in each era. ?There would be some art to this. ?A raw leverage ratio, or fixed charges ratio?in?the financial sector wouldn’t be a bad idea, but it probably wouldn’t be enough. ?The constraint that bind varies over time as well — regulators, rating agencies, general prudence, etc…)

In a highly leveraged situation with chains of lending, confidence becomes crucial. ?Indeed, at the time, you will hear the improvident squeal that they “don’t have a solvency crisis, but just a liquidity crisis! We just need to restore confidence!” ?The truth is that they put themselves in an unstable situation where a small change in cash flows and collateral values will be the difference between life and death. ?Confidence only deserves to exist among balance sheets that are conservative.

That’s all for now. ?Again, if you can think of other areas where debt has grown too quickly, or lending standards are poor, please e-mail me, or leave a message in the comments. Thanks.

One of the constants in investing is that average investors show up late to the party or to the crisis. ?Unlike many gatherings where it may be cool to be fashionably late, in investing it tends to mean you earn less and lose more, which is definitely not cool.

One reason why this happens is that information gets distributed in lumps. ?We don’t notice things in real time, partly because we’re not paying attention to the small changes that are happening. ?But after enough time passes, a few people notice a trend. ?After a while longer, still more people notice the trend, and it might get mentioned in some special purpose publications, blogs, etc. ?More time elapses and it becomes a topic of conversation, and articles make it into the broad financial press. ?The final phase is when?general interest magazines put it onto the cover, and get rich quick articles and books point at how great fortunes have been made, and you can do it too!

That slow dissemination and?gathering of information is paralleled by a similar flow of money, and just as the audience gets wider, the flow of money gets bigger. ?As the flow of money in or out gets bigger, prices tend to overshoot fair value, leaving those who arrived last with subpar returns.

There is another aspect to this, and that stems from the way that people commonly evaluate managers. ?We use past returns as a prologue to what is assumed to be still?greater returns in the future. ?This not only applies to retail investors but also many institutional investors. ?Somme institutional investors will balk at this conclusion, but my experience in talking with institutional investors has been that though they look at many of the right forward looking indicators of manager quality, almost none of them will hire a manager that has the right people, process, etc., and has below average returns relative to peers or indexes. ?(This also happens with hedge funds… there is nothing special in fund analysis there.)

For the retail crowd it is worse, because?most investors look at past returns when evaluating managers. ?Much as Morningstar is trying to do the right thing, and have forward looking analyst ratings (gold, silver, bronze, neutral and negative), yet much of the investing public will not touch a fund unless it has four or five stars from Morningstar, which is a backward looking rating. ?This not only applies to individuals, but also committees that choose funds for defined contribution plans. ?If they don’t choose the funds with four or five stars, they get complaints, or participants don’t use the funds.

Another Exercise in Dollar-Weighted Returns

One of the ways this investing shortfall gets expressed is looking at the difference between time-weighted (buy-and-hold) and dollar-weighted (weighted geometric average/IRR) returns. ?The first reveals what an investor who bought and held from the beginning earned, versus what the average dollar invested earned. ?Since money tends to come after good returns have been achieved, and money tends to leave after bad returns have been realized, the time-weighted returns are typically higher then the dollar-weighted returns. ?Generally, the more volatile the performance of the investment vehicle the larger the difference between time- and dollar-weighted returns gets. ?The greed and fear cycle is bigger when there is more volatility, and people buy and sell at the wrong times to a greater degree.

(An aside: much as some pooh-pooh buy-and-hold investing, it generally beats those who trade. ?There may be intelligent ways to trade, but they are always a minority among market actors.)

HSGFX Dollar and Time Weighted Returns

That brings me to tonight’s fund for analysis: Hussman Strategic Growth [HSGFX]. John Hussman, a very bright guy, has been trying to do something very difficult — time the markets. ?The results started out promising, attracting assets in the process, and then didn’t do so well, and assets have slowly left. ?For my calculation this evening, I run the calculation on his fund with the longest track record from inception to 30 June 2014. ?The fund’s fiscal years end on June 30th, and so I assume cash flows occur at mid-year as a simplifying assumption. ?At the end of the scenario, 30 June 2014, I assume that all of the funds remaining get paid out.

To run this calculation, I do what I have always done, gone to the SEC EDGAR website and look at the annual reports, particularly the section called “Statements of Changes in Net Assets.” ?The cash flow for each fiscal year is equal to the?net increase in net assets from capital share transactions plus the net decrease in net assets from distributions to shareholders. ?Once I have?the amount of money moving in or out of the fund in each fiscal year, I can then run an internal rate of return calculation to get the dollar-weighted rate of return.

In my table, the cash flows into/(out of) the fund are in millions of dollars, and the column titled Accumulated PV is the?accumulated present value calculated at an annualized rate of -2.56% per year, which is the dollar-weighted rate of return. ?The zero figure at the top shows that a discount rate -2.56% makes the cash inflows and outflows net to zero.

From the beginning of the Annual Report for the fiscal year ended in June 2014, they helpfully provide the buy-and-hold return since inception, which was +3.68%. ?That gives a difference of 6.24% of how much average investors earned less than the buy-and-hold investors. ?This is not meant to be a criticism of Hussman’s performance or methods, but simply a demonstration that a lot of people invested money after the fund’s good years, and then removed money after years of underperformance. ?They timed their investment in a market-timing fund poorly.

Now, Hussman’s fund may do better when the boom/bust cycle turns if his system makes the right move?somewhere near the bottom of the cycle. ?That didn’t happen in 2009, and thus the present state of affairs. ?I am reluctant to criticize, though, because I tried running a strategy like this for some of my own clients and did not do well at it. ?But when I realized that I did not have the personal ability/willingness to?buy when valuations were high even though the model said to do so because of momentum, rather than compound an error, I shut down the product, and refunded some fees.

One thing I can say with reasonable confidence, though: the low returns of the past by themselves are not a reason to not invest in Mr. Hussman’s funds. ?Past returns by themselves tell you almost nothing about future returns. ?The hard questions with a fund like this are: when will the cycle turn from bullish to bearish? ?(So that you can decide how long you are willing to sit on the sidelines), and when the cycle turns from bearish to bullish, will Mr. Hussman make the right decision then?

Those questions are impossible to answer with any precision, but at least those are the right questions to ask. ?What, you’d rather have the answer to a simple question like how did it return?in the past, that has no bearing on how the fund will do in the future? ?Sadly, that is the answer that propels more investment decisions than any other, and it is what leads to bad overall investment returns on average.

PS — In future articles in this irregular series, I will apply this to the Financial Sector Spider [XLF], and perhaps some fund of Kenneth Heebner’s. ?Till then.