Volatility Can Be Risk, At Rare Times

There is a saying in the markets that volatility is not risk. In general this is true, and helps to explain why measures like beta and standard deviation of returns do not measure risk, and are not priced by the market. After all, risk is the probability of losing money, and the severity thereof.

It’s not all that different from the way that insurance underwriters think of risk, or any rational businessman for that matter. But just to keep things interesting, I’d like to give you one place where volatility is risk.

When overall economic conditions are serene, many people draw the conclusion that it will stay that way for a long time. That’s a mistake, but that’s human nature. As a result, those concluding that economic conditions will remain serene for a long time decide to take advantage of the situation and borrow money.

When volatility is low, typically credit spreads are low. Why not take advantage of cheap capital? Well, I would simply argue that interest rates are for a time, and if you don’t overdo it, paying interest can be managed. But what happens if you have to refinance the principal of the loan at an inopportune time?

When volatility and interest spreads are low for you, they are low for a lot of other people also. Debt builds up not just for you, but for society as a whole. This can have the impact of pushing up prices of the assets purchased using debt. In some cases, the rising asset prices can attract momentum buyers who also borrow money in order to own the rising assets.

This game can continue until the economic yield of the assets is less than the yield on the debt used to finance the assets. Asset bubbles reach their breaking point when people have to feed cash to the asset beyond the ordinary financing cost in order to hold onto it.

In a situation like this, volatility becomes risk. Too many people have entered into too many fixed commitments and paid too much for a group of assets. This is one reason why debt crises seem to appear out of the blue. The group of assets with too much debt looks like they are in good shape if one views it through the rearview mirror. The loan-to-value ratios on recent loans based on current asset values look healthy.

But with little volatility in some subsegment of the overly levered assets, all of a sudden a small group of the assets gets their solvency called into question. Because of the increasing level of cash flows necessary to service the debt relative to the economic yield on the assets, it doesn’t take much fluctuation to make the most marginal borrowers question whether they can hold onto the assets.

Using an example from the recent financial crisis, you might recall how many economists, Fed governors, etc. commented on how subprime lending was a trivial part of the market, was well-contained, and did not need to be worried about. Indeed, if subprime mortgages were the only weak financing in the market, it would’ve been self-contained. But many people borrowed too much chasing inflated values of residential housing. ?As asset values fell, more and more people?lost willingness to pay for the depreciating assets.

We’ve had other situations like this in our markets. Here are some examples:

- Commercial mortgage loans went through a similar set of issues in the late 80s.

- Lending to lesser developed countries went through similar set of issues in the early 80s.

- The collateralized debt obligation markets seem to have their little panics every now and then. (late 90s, early 2000s, mid 2000s, late 2000s)

- During the dot-com bubble, too much trade finance was extended to marginal companies that were burning cash rapidly.

- The roaring 20s were that way in part due to increased debt finance for corporations and individuals.

At the peak some say, “Nobody rings a bell.” This is true. But think of the market peak as being like the place where the avalanche happened 10 minutes before it happened. What set off the avalanche? Was it the little kid at the bottom of the valley who decided to yodel? Maybe, but the result was disproportionate to the final cause. The far more amazing thing was the development of the snow into the configuration that could allow for the avalanche.

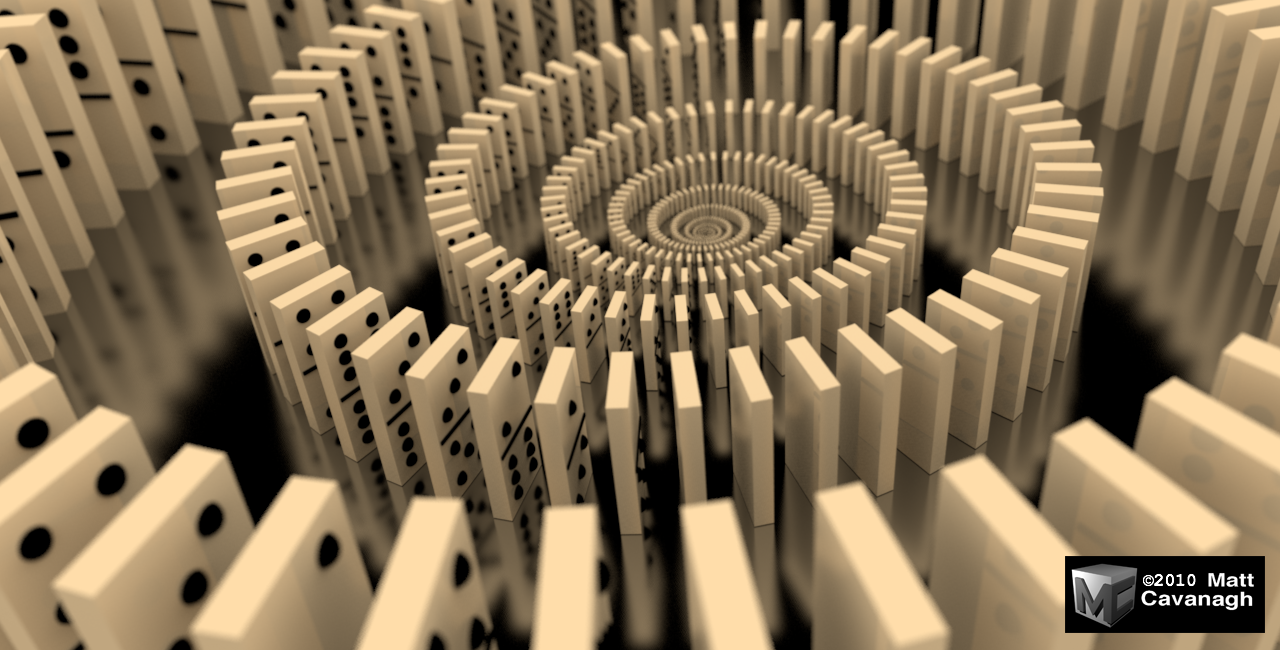

This is the way things are in a heavily indebted financial system. At its end, it is unstable, and at its initial unwinding the proximate cause of trouble seems incapable of doing much harm. But to give you another analogy ask yourself this: what is more amazing, the kid who knocks over the first domino, or the team of people spending all day lining up the huge field of dominoes? It is the latter, and so it is amazing to watch large groups of people engaging in synchronized speculation not realizing that they are heading for a significant disaster.

As for today, I don’t see the same debt buildup has we had growing from 2003 to 2007. The exceptions maybe student loans, parts of the energy sector, parts of the financial sector, and governments. That doesn’t mean that there is a debt crisis forming, but it does mean we should keep our eyes open.