Yesterday I was a judge (one of five) for the Washington/Baltimore Investment Research Challenge.? Five teams from local colleges participated to analyze a prominent local company, Under Armour.? (My kids love the stuff, I hate to pay the price.)

I have to say that I admire all of the young men and women who presented to us.? It takes a lot of guts to present to people 30 years older then you.? The experience differential is considerable.

One practical difference is that the students apply many methods from Modern Portfolio Theory that are roundly ignored by most investment managers.? Few investment managers apply Discounted Cash Flows [DCF], because it is too flexible, with too many parameters that are hard to calculate.? Some apply reverse DCF, attempting to estimate the rate of return of companies at their current price… same problems exist, though the comparability of results is simpler.

My advice to future contestants would be to spend more time on qualitative issues, and less on quantitative.? Regarding quantitative issues, I would encourage abandoning DCF in favor of simpler valuation methodologies.

Also, I would discourage using regression unless you really understand what it means.? It’s easy to teach people to use advanced statistical methods, but tough to teach them the limitations of where the methods get abused, or don’t work.? As I have often said, I rarely see advanced statistics used properly by Wall Street, and yesterday was no exception.

But all that said, there are a lot of bright people entering the talent pool for investing; for investment firms in a given region, going to an event like this could be a good recruiting tool.

PS — make sure you understand the liability structure in full, also…

I read an article or a comment from a blog that inked to your sight.? the statement was akin to this. ” The market is dead.? The lack of growth over ten years shows the deadness of the market.? If the market had kept pace with inflation over the last ten years it would be at 32,000 not the 11,000 we see today.”

I am not all that concerned that this is a true statement, nor am I convinced that their is any better long term investment then a good market strategy.? but I do not have the wisdom to know how to answer this sort of claim in my mind.

“Whitney Tilson?s latest monthly letter provides us with some insightful lessons for the current market environment. ?Regular readers will know that I believe there is no such thing as a one size fits all investment strategy or a holy grail approach. ?Instead, investors must understand the macro environment and apply the correct strategy to fit that particular environment. ?That micro approach could involve buy and hold, trading, value investing, etc. ?But the likelihood of success using one strategy in all environments is unlikely. The current turmoil and unusual asset class correlation is making for a very difficult environment for value investors. ?Tilson explains (thanks to Zero Hedge):”

Later on he states the following: “Value investing might not be dead (it?s certainly not dead for those who have the ability to implement it in the actual way that Warren Buffett implements it ? no, not the ?buy and hold? myth that Wall Street has sold to everyone), but we can be almost certain that it?s more important than ever to understand the macro. ?If there?s one great lesson to learn from the recent turmoil that should be it?.”

Is the above author stating the difficulty of being a value investor, or is this a man trying to validate his own lack of plan or strategy in a difficult market?? Besides a difficult month for some value investors what is their augment against it.? Would your “bloodless” strategy of quarterly trading be the answer their the accusation of the “buy and hold myth.”

With respect to the tripling of the index level due to inflation, that seems really high to me, akin to a 10% inflation rate.? I think that government inflation statistics are biased low, but by 1-2%/year not 6-8%/year.

On value investing, I rely on Ben Graham’s dictum that the stock market is a voting machine in the short run, and a weighing machine in the long run.? Periods of high correlation where the voting machine dominates eventually go away, and when they go away the weighing machine comes back and patient holders of cheap quality stocks get rewarded.

Value investing has gone through far deeper periods of underperformance such as the one in the late ’90s where many famous value investors got fired, just before the paradigm was about to shift, and value outpace growth by more than the underperformance.

“Buy and hold” is always lionized in a bull market, and castigated in a bear market.? That’s normal.? I grew up in the ’70s watching Wall Street Week with Louis Rukeyser, and at that time, traders were dominant in a static market.? That was not true in the ’80s and ’90s.

My quarterly trading strategy strikes a balance between too-frequent trading that most mutual fund managers do, and the never trade strategies that those who misunderstand value investing do.? Most investors trade at the wrong times, giving up on a stock merely due to bad performance, or buying because it is fashionable.? But if the business is fundamentally sound, it can be held through periods of weakness, and even add to the position.

That’s what I do, and it has worked well for me.? May it work so well for my clients.

I lead a finance class for church.? I think we have talked of it before.? I do not deal much with investing. Mostly I work with cleaning up the personal finances of the families.? Paying down debt, increasing savings, Setting and living below your income, budget, basic investing, using your tax shelters, and avoiding risky investments.

I have a family who some years ago purchased $8000 worth of Microsoft stock.? This has over the course of their holdings dropped between $8-10 a share.? Their financial situation requires cash, cash they do not have.? They need to pay off debts, and their current income gives them very little wiggle room to pay extra on debts.? They asked me what to do with the Microsoft stock, that is now down about $1500 from when they purchased it.? Microsoft stock has remained at a price of $23-29 a share for over a year now.? with the average being somewhere around $24-27 My thoughts have been: That the stock has corrected for the time being and

$25 is probably the true value.? IF $6500? would make a big diffrence in you budget, let you pay down alot of debt and free up some extra cash in your budget to pay off other debts, then sell the stock now.? $1500 is a cheap price to pay for a not so wise investment decision, if it can be use to improve your overall financial standing.? I told him he might ask his broker to sell as soon as it hits $26.

I have however read that Microsoft is a company that has put up good sales and profits in the past few years and that their stock price might be well undervalued.? should I encourage him to hold or sell.? Not asking you to predict the future, simply wanting to get counsel on the advise I have given.

If you think this is good advice let me know.? He is able to get by without the funds immediately, but it will be best if he sell them and use them eventually.

Microsoft is a test for value investors.? What do you do with a company that is cheap on a price-to-earnings basis, but tends to waste free cash flow on foolish acquisitions, investments, and stock buybacks?? My view is that you reject Microsoft; there are better things to buy.

But what of the decision of Microsoft versus cash?? Look, one of the first principles of investing is never invest what you can’t afford to lose.? If you might need the money to spend in the near term, don’t invest it in stocks.

Reconsider my article, Build the Buffer.? Until someone can meet all cash needs easily, including small disasters, he should not be investing in stocks.

With that, I would say that he should sell the stock to the degree that he needs liquidity.? Ability to pay cash in advance is worth far more than equity market returns.

I have had two prior posts on this topic, and I can tell you that Bonanza Goldfields and GTX Corp both cratered though they still live, sort of.? Bioneutral has done poorly, but has not cratered.

So today, while I was reading an article at Time.com, the liberal magazine, I clicked on a link but the page was not fully loaded, and I was transferred to this page.? As scams through postal mail die, so they must appear on the web.

As for today’s folly, let read a part of the disclaimer:

Compensation

AmericanEnergyReport.com has been retained by an unrelated third party to perform promotional and advertising services intended to increase investor awareness of UnionTown Energy Inc. (UTOG). To date, AmericanEnergyReport.com has received five hundred thousand USD from an unrelated third party for performing these services. The services performed have included profiling the company on the AmericanEnergyReport.com website and issuing opinions concerning UTOG in newsletters and press releases. In addition, AmericanEnergyReport.com expects to receive an additional two million USD cash in future compensation for the continuation of the marketing program for an additional 3 months and to cover marketing vendors to pay for the costs of creating and distributing this report online in an effort to build market awareness. AmericanEnergyReport.com will disclose any future compensation. Anyone viewing the AmericanEnergyReport.com website or its newsletters and press releases should assume the hiring party or affiliates of the hiring party own shares of UTOG, which they plan to liquidate. Further, it must be understood that the liquidation of those shares may or may not negatively impact the share price. AmericanEnergyReport.com has received this amount as a production budget for advertising efforts and will retain amounts over and above the cost of production, copywriting services, mailing and other distribution expenses as a fee for our services. As such, our opinion is neither unbiased nor independent, and you should consider that when evaluating our statements regarding UTOG.

Since AmericanEnergyReport.com receives compensation from, and its owners, operators and affiliates may hold stock in, the profiled companies, there is an inherent conflict of interest in AmericanEnergyReport.com statements and opinions and such statements and opinions cannot be considered independent. AmericanEnergyReport.com and its owners, operators and affiliates may benefit from any increase in the share prices of the profiled companies. AmericanEnergyReport.com services are often paid for using free-trading shares. AmericanEnergyReport.com and/or its owners, operators and affiliates may be selling shares of stock at the same time the profile (or other information) is being disseminated to potential investors; AmericanEnergyReport.com will not advise when it or its affiliates decide to sell. Investors must make all investment decisions based on their own judgment of the market and the particular securities.

So, the writers get paid a lot, and may be paid? in the stock of those they write about?? No way they have independent opinions, and no wonder the type is so tiny and at the far bottom of the page.

Much as I like the prospects for oil, I do not believe that “Oil prices can only go up!”? That’s the language of fools.? In almost every economic environment, there can be significant setbacks to? a long-term trend, or even reversals.

The advertising appeals to the naive view that because other companies have reach share prices in the 30s, so might this stock. One of those comparable companies in that group is Northern Oil & Gas (NOG), of which my friend John Hempton is skeptical.

Now, I am not going to do a complete teardown of UnionTown Energy Inc.? At present, I am busy, and I know that companies that seek? paid analysts are usually crooked.? Why?? Simple.? Small companies with something good going keep it quiet, so that management can buy more of the company.? Unless they need more capital to build up plant and equipment, they don’t need to seek coverage.? Those that seek paid analysts to sing their praises are seeking for strength to sell into.

That’s how simple it is, and I record the price of UnionTown here: $1.55.? Also please note that the advertising campaign has run out and the price is now falling.? Caveat emptor.

Compensation

AmericanEnergyReport.com has been retained by an unrelated third party to perform promotional and advertising services intended to increase investor awareness of UnionTown Energy Inc. (UTOG). To date, AmericanEnergyReport.com has received five hundred thousand USD from an unrelated third party for performing these services. The services performed have included profiling the company on the AmericanEnergyReport.com website and issuing opinions concerning UTOG in newsletters and press releases. In addition, AmericanEnergyReport.com expects to receive an additional two million USD cash in future compensation for the continuation of the marketing program for an additional 3 months and to cover marketing vendors to pay for the costs of creating and distributing this report online in an effort to build market awareness. AmericanEnergyReport.com will disclose any future compensation. Anyone viewing the AmericanEnergyReport.com website or its newsletters and press releases should assume the hiring party or affiliates of the hiring party own shares of UTOG, which they plan to liquidate. Further, it must be understood that the liquidation of those shares may or may not negatively impact the share price. AmericanEnergyReport.com has received this amount as a production budget for advertising efforts and will retain amounts over and above the cost of production, copywriting services, mailing and other distribution expenses as a fee for our services. As such, our opinion is neither unbiased nor independent, and you should consider that when evaluating our statements regarding UTOG.

Since AmericanEnergyReport.com receives compensation from, and its owners, operators and affiliates may hold stock in, the profiled companies, there is an inherent conflict of interest in AmericanEnergyReport.com statements and opinions and such statements and opinions cannot be considered independent. AmericanEnergyReport.com and its owners, operators and affiliates may benefit from any increase in the share prices of the profiled companies. AmericanEnergyReport.com services are often paid for using free-trading shares. AmericanEnergyReport.com and/or its owners, operators and affiliates may be selling shares of stock at the same time the profile (or other information) is being disseminated to potential investors; AmericanEnergyReport.com will not advise when it or its affiliates decide to sell. Investors must make all investment decisions based on their own judgment of the market and the particular securities.

I was sorry to read about the demise of your firm a month ago.? I hope God prospers you in whatever path you pursue now.? I?m writing to you with a few investing questions because I know you actually can evaluate what I?ve done- and from a perspective that I think matches mine (buy dividend-paying value for the long-term), and I really would like to deliberately practice improving my evaluation of companies with testing & feedback.? If, however, my request falls under your own business plan- I understand completely.

4 years ago, I picked several energy stocks using only one metric: P/E ratio.? Since then, I found Graham?s writing on investing and your blog and started thinking that one-stick-measuring for something as complicated as a business is a dangerous game.? Using what?s available to me on Vanguard?s website (plus what I?ve learned from you and Graham), I have a slightly less incomplete model to measure a business.

I know you?re very busy, but if you ever have a chance, would you look at my scoring system and give me some small feedback?? I?m curious about a few specific things:

a) Have I left out any key aspects or ratios?? If so, what?? (and what should they be?)

b) Graham suggests going back years and years when looking at a business.? What is the point where you get such diminished returns that?s it not worth the effort to dig up the numbers?? 3 years? 5 years? 10 years?

c) Follow up to b: does your answer to that question change based on the aspect examined?? (ie: EPS should be?reviewed for the last 5 years but Cash only for the previous year)

d) In my scoring system, have I over- or under-weighted any of the categories?? Have I not been stringent enough in?awarding points?

Naturally, I have many more questions.??But I?ll greatly appreciate any feedback you give me on these.

-==–==–=-=-=-==–=-==-=-=-=-=-=-=-=-=–=

I get a lot of e-mail.? I wish I could freeze time, and respond to all of it.? I have been spending time recently clearing out the e-mail box.? I am down to seven flagged messages.

The above message is from a friend of mine, whose father is a close friend of mine.? The father taught me a lot.? He might be my top intellectual influence — he is certainly in the top 5.

I sympathize with my young friend here.? I was once an individual investor myself, and I tried a wide variety of ideas before I settled on my current strategy, which grew out of my value strategy in the mid-90s, when I was much younger.

Before I answer his questions, I will say that for two decades I spent one hour per day at minimum (excluding Sundays) improving my skills.? Investing well takes training.? Simple solutions are rare.? The alternative name for this blog was “The Investment Omnivore,” because I have studied so many things in investing, from so many different angles.

Now for advice to my friend:

You have six criteria, it seems. I will handle them in the order of your spreadsheet.

1) You analyze versus 1 and 3-year price action.? With 3-year price action mean reversion is likely, but with one year price action, momentum tends to persist.? Change the direction of your scoring system on 1 year price performance, because investors tend to lag fundamental improvement in the short-run.? Momentum tends to persist over a year or two.

2) With dividends and earnings per share, your scoring is logical, though there is this difficulty — stocks react to changes in expectations, not data on the announcement date, though surprises change expectations.

3) I use the current ratio as a disqualifier.? I don’t use it for scoring, but for whether it is worthwhile to consider a given company.

4) The same is true for Cash-to-Total-Debt.? Low ratios would disqualify a company, but high ratios would not get points in my opinion.

5) And also for total debt to equity.? I should tell you that one has to consider these matters on an industry by industry basis.? Stable industries can bear more debt.

6) Then you have cheapness — price to book, earnings and cashflow.? With financials and utilities, I use P/E times P/B as a criterion, as Graham did.? With Industrials I use Price-to-Sales.? With Industrials I also look at price to cashflow and free cashflow.

So, my advice for you is this: the key idea of value investing is margin of safety.? The first task of a value investor is to assure safety.? This means using balance sheet statistics that you cut the universe in two — worthy of consideration, and out of the question.

After that, we look at valuation and analyze those companies that are acceptable to find those that offer the best values.? I give more credit to companies that have better growth prospects, but that is a soft criterion.

And after that, price momentum and mean-reversion.? Momentum works in the short run, and mean reversion in the intermediate-term.

Though you might think I am critical of your efforts here, please understand that in the mid-90s I was much like you, struggling with the concepts of value, and trying to come up with a coherent thesis.? I am impressed with your work and not dismissive.

This is a trail that I rode when I was young.? With additional study, you can do better as well.

And I say this to all readers, because there are many who follow simple ideas that fail.? I urge those who read me to read broadly in investing, and pursue the broad ideas that seem to work.

There is one fundamental rule on the idea generation process to get across to new retail investors:

Buy what you have researched.? Don’t buy what your friends are buying, or even worse, what someone is trying to sell you.

(For those with access to RealMoney.com, you could review my Using Investment Advice series.)

The point here is to become capable of doing the basic research necessary to make reasonable decisions.? You don’t have to make great decisions in order to succeed.? You do have to avoid making major errors, which requires a degree of skepticism toward the opinions of your non-expert friends, and modest hostility toward those selling investment products.

What led to this article was a eight-page glossy advertisement from a publication that I do not deign to name (I worry about lawsuits), about a company called GTX Corp [GTXO].? Now, maybe I need to refresh my free subscription to the direct mail preference service, which really cuts down on the amount of junk mail that I receive.

GTX Corp is an example of a company with a high valuation, and uncertain prospects.? There is no provision for adverse deviation.? It trades on the Bulletin Board, and here is its business:

GTX Corporation integrates global positioning system (GPS) technology into consumer electronics devices.? The technology allows for real-time oversight of loved ones.

Now, why don’t I like this company, aside from the advertisement that did not mention valuation, balance sheet strength, or any other risk factors?

It trades at a high ratio of book, and trailing earnings don’t exist.

It was created out of a merger with a failed mining company.

Its recent financing this month offered equity interests far cheaper than the current market price.

Their auditor is not a major auditing firm.

Give the auditor credit though, they did not give them a “going concern” opinion, but instead expressed doubts.

The stock is on the Nasdaq’s Threshold Securities list, so finding shares to short is problematic.

Major shareholders are doing a secondary offering.

The advertiser was paid $186,000 to do the ad by a third party.

I have no idea how good their GPS technology might be, but there are too many risk factors here to make me even consider a long position.

I am not here to beat on GTX Corp.? I am using them, and the guy who advertised them as an example.

The advertisement had all manner of positive things to say about the technology and what it could do.? That’s fine, but what has it done?? Why doesn’t this corporation have significant revenues?

Why does the ad use the scam language “as featured on” and “as seen in,” naming prominent publications and channels, when all he likely did was buy some slack advertisements at a late hour, or in regional editions?

The ad compares the company to Garmin and other successful companies.

The ad uses a bunch of emotive problems that the technology could solve.

The ad puts forth a target price of $12 without any justification.

Buyer beware, and don’t listen to strangers giving you advice.? Cultivate networks of knowledgeable friends who are trustworthy, and avoid getting taken for a ride by slick-talking (writing) hucksters who pitch clever ideas to you.? Do your work, and buy cheap, boring ideas like I do.

Everybody has a series of longer-term goals that they want to achieve financially, whether it is putting the kids through college, buying a home, retirement, etc.? Those priorities compete with short run needs, which helps to determine how much gets spent versus saved.

To the extent that one can estimate what one can reasonably save (hard, but worth doing), and what the needs of the future will cost, and when they will come due (harder, but worth doing), one can estimate personal contribution and required investment earnings rates.? Set up a spreadsheet with current assets and the likely savings as positive figures, and the future needs as negative figures, with the likely dates next to them.? Then use the XIRR function in Excel to estimate the personal required investment earnings rate [PRIER].

I’m treating financial planning in the same way that a Defined Benefit pension plan analyzes its risks.? There’s a reason for this, and I’ll get to that later.? Just as we know that a high assumed investment earnings rate at a defined benefit pension plan is a red flag, it is the same to an individual with a high PRIER.

Now, suppose at the end of the exercise one finds that the PRIER is greater than the yield on 10-year BBB bonds by more than 3%.? (Today that would be higher than 9%.)? That means you are not likely to make your goals.?? You can either:

Save more, or,

Reduce future expectations,whether that comes from doing the same things cheaper, or deferring when you do them.

Those are hard choices, but most people don’t make those choices because they never sit down and run the numbers.? Now, I left out a common choice that is more commonly chosen: invest more aggressively.? This is more commonly done because it is “free.”? In order to get more return, one must take more risk, so take more risk and you will get more return, right?? Right?!

Sadly, no.? Go back to Defined Benefit programs for a moment.? Think of the last eight years, where the average DB plan has been chasing a 8-9%/yr required yield.? What have they earned?? On a 60/40 equity/debt mandate, using the S&P 500 and the Lehman Aggregate as proxies, the return would be 3.5%/year, with the lion’s share coming from the less risky investment grade bonds.? The overshoot of the ’90s has been replaced by the undershoot of the 2000s.? Now, missing your funding target for eight years at 5%/yr or so is serious stuff, and this is a problem being faced by DB pension plans and individuals today.

While the ’80s and ’90s were roaring, DB plan sponsors made minimal contributions, and did not build up a buffer for the soggy 2000s.? Part of that was due to stupid tax law that the government put in because they didn’t want pension plans to shelter income from taxes for plan sponsors.? (As an aside, public plans did less than corporations, even though they did not face any tax consequences.)

But the same thing was true of individuals.? When the markets were good, they did not save.? Now when the markets are not good, the habit of not saving is entrenched, and now being older, saving might be more difficult because of kids in college, interest on a mortgage for a house larger than was needed, etc.

Now, absent additional saving, when investment earnings lag behind the PRIER, that makes the future PRIER rise, to try to make up for lost time.? Perhaps I need to apply the five stages of grieving here as well… trying to earn more to make up for lost time is a form of bargaining.? It rarely works, and sometimes blows up, leaving a person worse off than before.? Most aggressive asset allocation strategies only work over a long period of time, and only if a player is willing to buy-rebalance-hold, which only a few people are constitutionally capable of doing.? Most people get scared at the bottoms, and get euphoric near tops.? Few follow Buffett’s dictum, “Be greedy when others are fearful, and fearful when others are greedy.”? Personally, I expect the willingness to take investment risk over the next five years to rise, but over the next ten years, I don’t think it will be rewarded.

Now, as time progresses, and the Baby Boomers gray, unless the equity markets are returning the low teens in terms of returns, there will be a tendency for the average PRIER to rise, absent people realizing that they have to save more than planned, or reduce their goals.? This problem will be faced in the ’10s, bigtime.? The pensions crisis will be front page news, and I’m not talking about Social Security and Medicare, though those will be there also.? The demographics will be playing out.? After all, what drives the funding of retirement at a DB plan, but aging, where the promised expected payments get closer each day.

Well, same thing for individuals.? Every day that passes brings a slow weakening of our bodies and minds.? Dollars not saved today, or bad investment returns mean the PRIER rises, making the probability of attaining goals less achievable.

Now, is there nothing that can be done aside from increasing savings and reducing future plans?? In aggregate, no.? You will have to be someone special to beat the pack, because few do that.? Better you should take the simple solution, which is a humble one: save more, expect less.? For those that do have the talent, you will have to take the risks that few do, and be unconventional.? Note: for every four persons that think they can do this, at best one will succeed.? My own methods are always leaning against what is popular in the markets, and I think that I am one of those few, but it takes work and emotional discipline to do it.

Then again, I have done it, as far as my PRIER is concerned — it is below the rate on 10-year Treasuries.? Most of that is that my goals are modest, aside from putting my eight kids through college, and I am not planning on retiring.

With that, I leave to consider a post I wrote at RealMoney two years ago.? It’s kind of a classic, and Barry Ritholtz e-mailed me to say that he loved it.? Given what we are experiencing lately, it seems prescient.? Here it is:

Make the Money Sweat, Man! We Got Retirements to Fund, and Little Time to do it!

3/28/2006 10:23 AM EST

What prompts this post was a bit of research from the estimable Richard Bernstein of Merrill Lynch, where he showed how correlations of returns in risky asset classes have risen over the past six years. (Get your hands on this one if you can.) Commodities, International Stocks, Hedge Funds, and Small Cap Stocks have become more correlated with US Large Cap Stocks over the past five years. With the exception of commodities, the 5-year correlations are over 90%. I would add in other asset classes as well: credit default, emerging markets, junk bonds, low-quality stocks, the toxic waste of Asset- and Mortgage-backed securities, and private equity. Also, all sectors inside the S&P 500 have become more correlated to the S&P 500, with the exception of consumer staples. In my opinion, this is due to the flood of liquidity seeking high stable returns, which is in turn driven partially by the need to fund the retirements of the baby boomers, and by modern portfolio theory with its mistaken view of risk as variability, rather than probability of loss, and the likely severity thereof. Also, the asset allocators use “brain dead” models that for the most part view the past as prologue, and for the most part project future returns as “the present, but not so much.” Works fine in the middle of a liquidity wave, but lousy at the turning points.

Taking risk to get stable returns is a crowded trade. Asset-specific risk may be lower today in a Modern Portfolio Theory sense. Return variability is low; implied volatilities are for the most part low. But in my opinion, the lack of volatility is hiding an increase in systemic risk. When risky assets have a bad time, they may behave badly as a group.

The only uncorrelated classes at present are cash and bonds (the higher quality the better). If you want diversification in this market, remember fixed income and cash. Oh, and as an aside, think of Municipal bonds, because they are the only fixed income asset class that the flood of foreign liquidity hasn’t touched.

Don’t make aggressive moves rapidly, but my advice is to position your portfolios more conservatively within your risk tolerance.

I’m sure a lot of people have already told you but I want to tell you anyway: Your blog is awesome! I came across The Aleph Blog a couple of months ago and I?m very impressed with your content. I particularly like that 4-part article on Using Investment Advice. I am in the financial industry myself and it makes me wish I came up with the kind of ideas that you have on your blog. Awesome stuff!

Keep up the good work,

Many thanks to the reader, and if you want to read that series, it is located here. ?But when I considered what he wrote to me, it made me think, “Why do we have to tell people how to think about investment advice?”

Then it hit me: because people are looking for easy tips to execute. ?After all, when I wrote the 4-piece series, I had?listening to Jim Cramer in mind. ?The ?tip culture? of inexperienced investors don?t want to learn the ideas behind investing, but just want someone to say, ?Buy this.?? There is little if any guarantee that the same pundit?will ever update his opinion.

We see this on the web, in magazines, newsletters, newspapers, etc. ?On rare occasion, I will print one out, and add it to my “delayed research stack” which means I will look at it in 1-3 months. ?I just did my quarterly clean-out a few days ago — anything I add to the stack now will wait until November.

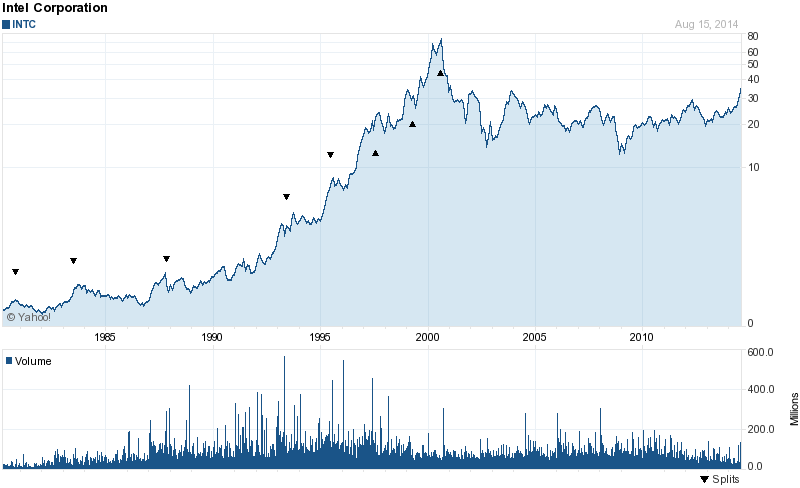

But why read articles like, “Ten Undervalued Large Cap Stocks with Growth Potential,” “Nine Stocks to Buy and Hold Forever,” “Eight Stocks that are Taking Off, Don’t Miss Out,” “Seven Hidden Gens Among Small Caps,” “Six Stocks for Income and Growth,” “Five Energy Stocks that are Poised to Surge,” Four Titanic Stocks that Every Investor Should Own,” “Three Turnaround Stocks with Potential for Large Capital Gains,” “Two Stocks with Breakthrough Technologies,” and “The One Stock that You Should Own for the Next Decade.”

Now, I made those titles up, though the last one was based off a Smart Money article on Intel in late 1999 which came very close to top-ticking ?the market. ?As you can see, Intel still hasn’t made it back to the tech bubble peak.

As I Googled phrases like, “Ten Best Stocks,” it was fascinating to see the range of pitches employed:

Appeals to Buffett (that never gets old)

Best stocks for this year

Favorite stocks of an author, manager or publication

With high dividends

With a low price

In emerging markets

That won’t lose money

That our patented investment screener spat out

For the rest of your life

Etc.

I know that I could get a lot more readers with list articles that tout stocks. ?I don’t do it because most of the articles that you read like that are bogus. ?[I also don’t want the inevitable scad of complaints that come with the territory.) ?So why do such articles?draw readers?

People would rather have false certainty than live in the reality that choosing good investments is difficult. ?Even very good investors hit rough patches where they do not outperform. ?Also, people aren’t comfortable with uncertain horizons for realizing value in investments — article tout holding forever, ten years, one year, but rarely 3-5 years or a market cycle.

The truth is, you can’t tell when a stock will perform, but when it does perform, the results will be lumpy. ?The performance of a stock is rarely smooth. ?During times when the success or failure of a stock idea is realized, the moves are often violent.

Now remember, those who write such articles are looking for media revenue — such articles are sensational, and pander to the desire for easy money. ?But where are the articles telling you to sell ten stocks now? ?(Yes, I know there are some, but they are not so common.) ?Or, where are follow up pieces indicating how well prior picks have done, and whether one should sell, hold, or buy more now?

My main point is this: good amateur investing is like having a part-time job. ?A part-time job, well, takes time. ?Weigh that against other priorities in your life — family, friends, church, public service, fun, etc. ?You may not want a part-time job, and so you can index your investments, or outsource them to a trusted advisor, who hopefully digs up his own ideas, and does not have a consensus, index-like portfolio (If he does, why not index?)

So, avoid tips if you can. ?If you can’t, develop a research discipline, or set them aside like I do, and revisit them when the original reason for buying it is forgotten, and you must evaluate for yourself now. ?The investment that you do not understand why you bought it, you will never know when it is the right time to sell it.

Either learn to evaluate investments on your own, or index your investments, or find a good investment advisor. ?But don’t think that you will do well off of tips.

I have a saying, ?Don?t buy what someone wants to sell you. Buy what you have researched.?

And so I would tell everyone: don?t give brokers discretion over you accounts, and don?t let them convince you to buy unusual bonds, or obscure securities of any sort.? By unusual bonds, I mean structured notes, and eminent men like Joshua Brown and Larry Swedroe encourage the same thing: Don?t buy them.

Understand yourself, understand the advisor, understand the counsel that is offered, and finally, we wary of what you here through the media, including me.

Before I start this evening, I would like to explain some of the reasons for these “Best of the Aleph Blog” articles. ?I write these no closer than one year after an article was written, so that I can have a more dispassionate assessment of how good they were. ?I write these for the following reasons:

Some people want a quick introduction to the way I think.

Some publishers on the web want additional copy, and I let them republish some of my best pieces.

One day I may bundle a bunch of them together, rewrite them to improve clarity, and integrate them to create a set of books on different topics.

One of my editors at RealMoney once shared with me that I was one of the few authors there whose articles got re-read, or read after a significant time had passed. ?This is meant to be mostly “timeless” stuff.

New readers might be interested in older stuff.

I enjoy re-reading my older pieces, and sometimes it stimulates updates, and new ideas.

Anyway, onto this issue of the “Best of the Aleph Blog.” ?These articles appeared between August 2012 and October 2012:

Goes through the details of how a school district outside San Diego mortgaged the future of the next generation who will live there, if any will live there.

A series of articles inspired by what I wrote at RealMoney, encouraging people to be careful about listening to advice in the media on stocks, including those recommended by Cramer.

Governments imagine that they can shape outcomes, and in the short-run, they can.? In the long-run, the real productivity of the economy matters, and only those that can make it without government help will make it.? Whatever government policy may try to achieve, eventually the economy reverts to what would happen naturally without incentives.? There is a natural carrying capacity for most activities, and efforts to change that usually fail.

Applying math to economics has been a loser.? Who has a consistently good macroeconomic model?? No one that I know.? Estimates of future GDP growth and inflation are regularly wrong, and no one calls turning points well.

Far from offering high price appreciation, it is far easier to cheat many people by offering a high yield, because average people look for ways to stretch their limited resources with a tight budget.

I had a long debate inside myself before writing my book review last night.? I could have written the review recommending purchase of Trend Following, because it teaches a truth that often gets ignored in the market — following price momentum pays around 80% of the time.? As a value investor, that was a hard lesson for me to learn, but I accepted it once the evidence was clear enough.

Why I did not recommend the purchase of the book was more over tone and style.? Here are two examples: on pages 294-296, he discusses this paper that shows that Commodity Trading Advisor [CTA] performance is little better than T-bills.? There is one substantive complaint, and I agree with it, that the Sharpe ratio is a lousy measure of performance.? Most of the other arguments focus on the author’s affiliations — AIG Financial Products and Vanguard.? It is not valid to dismiss evidence off of the background of the individual.? Deal with his arguments.? So what if he worked for AIGFP?? That doesn’t make him liable for everything done there.? Same for Vanguard.? Merely because you work for Vanguard does not mean that you shill for mutual fund industry in everything that you do.

Humble Student of the Markets Cam Hui raises these objections in his comments to my piece last night.? I object to the ad hominem arguments of Mr. Covel.? If we must argue, let us argue on the basis of principle, and may the best side win.

Now, when Mr. Covel responded to me, it was also an ad hominem argument, tying me to Jim Cramer.? Now note, the first piece has disappeared from the internet, and I know not why.? Perhaps he gets that I am not a Jim Cramer clone.? To my readers I ask, how many of you think that I am like Jim Cramer in the way I advise?? I wrote a long series of articles on using investment advice to inoculate people against using stock tips from the media, partially because as Jim Cramer became more of a media phenomenon, his recommendations became worse.? He is at his best when he writes/says less, and gives you his considered opinion.? Investing and doing something sensational for the media do not mix.? That’s the conundrum of the value proposition for TSCM.

That said, Cramer does use price momentum as one of the factors in his stock selections.? He is generally a “trend follower.”? Cramer also is not a value investor.? Much as I appreciate him giving me a chance to write, we aren’t very similar.? That’s consistent with TSCM philosophy — they want a large range of views.? I wrote there for four years, and was one of their leading writers.? I rarely interacted directly with Cramer, instead, putting forth my own views, which did better (in my opinion).

I’m not Cramer, and he’s not me.? He just gave me a chance to write, for which many are grateful.? (I would tell you that he taught me how to trade corporate bonds, even though he has never traded corporates, but that would be a long story.)

Pressing on

This is not my last article on this topic.? I intend on continuing this discussion, to flesh out where I agree with Mr. Covel, because at many points I do agree, but there are complexities that need further elucidation.

The main areas I will cover in the future include:

When does trend following fail?

What other factors should we consider?

What constitutes adequate proof that a strategy is superior?

I credit Michael Covel for commenting at my blog, and I will answer his question, but not today.? It is a valid question, but there are other questions that can be posed to him as well.? Let the debate commence on a fair basis.