I’ve said this before, but I like it when research destroys a preconceived notion of mine. ?Today’s post stems from an exchange that I had with Jackdamn (what a name) on Stocktwits, talking about a chart created by?dshort.

S&P 500 Percent Off High Since March 9, 2009. Chart by Doug Short. $SPX$SPY$DIA

To which he responded: That’s a great question. ?And it is a great question, but I’m not going to answer it directly here… because I think I am answering a better question.

Let me take you through my thought process, because I went through four different ways of trying to answer the question before settling on the better question, and getting the answer.

How do you summarize an area of a price graph in order to make comparisons of different periods? ?How do you determine when the market has been near highs for a long time, or far away for a long time? ?How does the intensity/distance below the high matter? ?If you are looking at troughs, where does one begin and another end?

I started by trying to identify the troughs individually, and the difficulty was trying to establish that in a mechanical way that did not require interpretation. ?I stumbled around playing with minimum periods between troughs, recovery levels before a new trough could start, moving averages to establish when a new trough was genuinely significant. ?Sigh.

I tried a lot of different things, and I could create rules that mostly made the troughs look decent, but I could never get it to be fully mechanical or lack arbitrariness. ?Why this trough?and not that? ?The same criticisms can be applied to dshort’s graph as well.

I finally pulled out of my mental gymnastics when I concluded: couldn’t I just take the area under the maximum line in percentage terms and use that as a measure, say over a 200-day period? ?200 days is arbitrary, and so is the measure, but that is less than most of the measures that I considered, and at least this one corresponds to a relatively simple calculation.

So if you look at the red line in my graph above, you will note that it has dipped below 2.0?five times in the last 66 years, in 1954, 1959, 1964, 1995 and 2014. ?These observations followed periods where the markets moved to new highs rather smartly and without a lot of downside volatility. ?Then there were 3 times that the measure peaked?higher than 64, in 1975, 2003 and 2009. ?These times followed incredible market falls, and were great times to be putting money into the market.

Below you can see ?a table of values for how often the measure is below a given threshold. ?It’s only above 64 about 5% of the time, and below 2 about 3.5% of the time. ?My main thought is this measure is this: high values of the measure probably are a “buy signal.” ?Low values of the measure aren’t necessarily a “sell signal.”

That signals are asymmetric should not be surprising. ?The largest factor in most long-term market moves, the credit cycle, is also asymmetric. ?It’s like my continuing series, Goes Down Double Speed. ?Bull markets have shallower moves and longer duration, the same way that the bull phase of the credit cycle goes. ?Extend credit, extend credit, extend credit… loosen standards, loosen standards, loosen standards… tighten spreads, tighten spreads, tighten spreads, etc. ?Then in the bear phase it is DENY CREDIT!! TIGHTEN STANDARDS!! SHEPHERD LIQUIDITY!! SURVIVE!! ?Short and sharp. ?Painful. ?Prices are lower, and yields higher at the end.

To close this off, where is this indicator now? ?It’s around 8, which is near the 40th percentile… kind of a blah figure, not saying much of anything… which is good in its own way. ?The market meanders and hits a few new highs, sags a little, comes back, hits a few new highs, etc. ?Not many people believe in it, but we are inches off the highs. ?Odds are we go higher from here, but not aggressively higher.

One final note: we are in the fourth and final phase of the credit cycle now, so don’t get too aggressive. ?Debt is getting higher inside nonfinancial corporations. ?Be wary, and do your fundamental due diligence on balance sheets.

When I was 29, nearly half a life ago, Donald Trump was a struggling real estate developer. ?In 1990, I was still trying to develop my own views of the economy and finance. ?But one day heading home from work at AIG, I was listening to the business report on the radio, and I heard the announcer say that Donald Trump had said that he would be “the king of cash.” ?My tart comment was, “Yeah, right.”

At that point in time, I knew that a lot of different entities were in need of financing. ?Though the stock market had come back from the panic of 1987, many entities had overborrowed to buy commercial real estate. ?The major insurance companies of that period were deeply at fault in this as well, largely driven by the need to issue 5-year Guaranteed Investment Contracts [GICs] to rapidly growing stable value funds of defined contribution plans. ?Outside of some curmudgeons in commercial mortgage lending departments, few recognized that writing 5-year mortgages with low principal amortization rates against long-lived commercial properties was a recipe for disaster. ?This was especially true as lending yield spreads grew tighter and tighter.

(Aside: the real estate area of Provident Mutual avoided most of the troubles, as they sold their building that they built seven years earlier for twice what they paid to a larger competitor. ?They also focused their mortgage lending on small, ugly, economically necessary properties, and not large trophy properties. ?They were unsung heroes of the company, and their reward was elimination eight years later as a “cost saving move.” ?At a later point in time, I talked with the lending group at Stancorp, which had a similar philosophy, and expressed admiration for the commercial mortgage group at Provident Mutual… Stancorp saw the strength in the idea, and still follows it today as the subsidiary of a Japanese firm. ?But I digress…)

Many of the insurance companies making the marginal commercial mortgage loans had come to AIG seeking emergency financing. ?My boss at AIG got wind of the fact that I was looking elsewhere for work, and subtly regaled me of the tales of woe at many of the insurance companies with these lending issues, including one at which I had recently interviewed. ? ?(That was too coincidental for me not to note, particularly as a colleague in another division asked me how the search was going. ?All this from one stray comment to an actuary I met coming back from the interview…)

Back to the main topic: good investing and business rely on the concept of a margin of safety. ?There will be problems in any business plan. ?Who has enough wherewithal to overcome those challenges? ?Plans where everything has to go right in order to succeed will most likely fail.

With Trump back in 1990, the goal was admirable — become liquid in order to purchase properties that were now at bargain prices. ?As was said in the Wall Street Journal back in April of 1990, the article started:

In a two-hour interview, Mr. Trump explained that he is raising cash today so he can scoop up bargains in a year or two, after the real estate market shakes out. Such an approach worked for him a decade ago when he bet big that New York City’s economy would rebound, and developed the Trump Tower, Grand Hyatt and other projects.

“What I want to do is go and bargain hunt,” he said. “I want to be king of cash.”

That’s where?Trump said it first. ?After that he received many questions from reporters and creditors, because his businesses were heavily indebted, and?property values were deflated, including the properties that he owned. ?Who wouldn’t want to be the “king of cash” then? ?But to be in that position would mean having sold something when times were good, then sitting on the cash. ?Not only is that not in Trump’s nature, it is not in the nature of most to do that. ?During good times, the extra cash that Buffett keeps on hand looks stupid.

Trump did not get out of the mess by raising cash, but by working out a deal with his creditors in bankruptcy. ?Give Trump credit, he had convinced most of his creditors that they were better off continuing to finance him rather than foreclose, because the Trump name made the properties more valuable. ?Had the creditors called his bluff, Trump?would have lost a lot, possibly to the point where we wouldn’t be hearing much about him today.

Trump escaped, but most other debtors don’t get the same treatment Trump did. ?The only way to survive in a credit crunch is plan ahead by getting adequate long-term financing (equity and long-term debt), and keep a “war kitty” of cash on the side.

During 2002, I had the chance to test this as a bond manager. ?With the accounting disasters at mid-year, on July 27th, two of my best brokers called me and said, ?The market is offered without bid.? We?ve never seen it this bad.? What do you want to do??? I kept a supply of liquidity on hand for situations like this, so with the S&P falling, and the VIX over 50, I put out a series of lowball bids for BBB assets that our analysts liked.? By noon, I had used up all of my liquidity, but the market was turning.? On October 9th, the same thing happened, but this time I had a larger war chest, and made more bids, with largely the same result.

That’s tough to do, and my client pushed me on the “extra cash sitting around.” ?After all, times are good, there is business to be done, and we could use the additional interest to make the estimates next quarter.

To give another example, we have the visionary businessman Elon Musk facing a?cash crunch?at Tesla?and?SolarCity. ?Leave aside for a moment his efforts to merge the two firms when stockholders tend to prefer “pure play” firms to conglomerates — it’s interesting to look at how two “growth companies” are facing a challenge raising funds at a time when the stock market is near all time highs.

Both Tesla and Solar City are needy companies when it comes to financing. ?They need a lot of capital to grow their operations before the day comes when they are both profitable and cash flow from operations is positive. ?But, so did a lot of dot-com companies in 1998-2000, of which a small number exist to this day. ?Elon Musk is in a better position in that presently he can dilute?issue shares of Tesla to finance matters, as well as buy 80% of the Solar City bond issue. ?But it feels weird to have to finance something in less than a public way.

There are other calls on cash in the markets today — many companies are increasing dividends and buying back stock. ?Some are using debt to facilitate this. ?I look at the major oil companies and they all seem to be levering up, which is unusual given the recent trajectory of crude oil prices.

We are in the fourth phase of the credit cycle now — borrowing is growing, and profits aren’t. ?There’s no rule that says we have to go through a bear market in credit before that happens, but that is the ordinary?way that excesses get purged.

That is why I am telling you to pull back on risk, and review your portfolio for companies that need financing in the next three years or they will croak. ?If they don’t self finance, be wary. ?When things are bad only cash flow can validate an asset, not hopes of future growth.

With that, I close this article with a poem that I saw as a graduate student outside the door of the professor for whom I was a teaching assistant when I first came to UC-Davis. ?I did not know that is was out on the web until today. ?It deserves to be a classic:

Once upon a midnight dreary as I pondered weak and weary

Over many a quaint and curious volume of accounting lore,

Seeking gimmicks (without scruple) to squeeze through

Some new tax loophole,

Suddenly I heard a knock upon my door,

Only this, and nothing more.

Then I felt a queasy tingling and I heard the cash a-jingling

As a fearsome banker entered whom I?d often seen before.

His face was money-green and in his eyes there could be seen

Dollar-signs that seemed to glitter as he reckoned up the score.

?Cash flow,? the banker said, and nothing more.

I had always thought it fine to show a jet black bottom line.

But the banker sounded a resounding, ?No.

Your receivables are high, mounting upward toward the sky;

Write-offs loom.? What matters is cash flow.?

He repeated, ?Watch cash flow.?

Then I tried to tell the story of our lovely inventory

Which, though large, is full of most delightful stuff.

But the banker saw its growth, and with a might oath

He waved his arms and shouted, ?Stop!? Enough!

Pay the interest, and don?t give me any guff!?

Next I looked for noncash items which could add ad infinitum

To replace the ever-outward flow of cash,

But to keep my statement black I?d held depreciation back,

And my banker said that I?d done something rash.

He quivered, and his teeth began to gnash.

When I asked him for a loan, he responded, with a groan,

That the interest rate would be just prime plus eight,

And to guarantee my purity he?d insist on some security?

All my assets plus the scalp upon my pate.

Only this, a standard rate.

Though my bottom line is black, I am flat upon my back,

My cash flows out and customers pay slow.

The growth of my receivables is almost unbelievable:

The result is certain?unremitting woe!

And I hear the banker utter an ominous low mutter,

?Watch cash flow.?

Herbert S. Bailey, Jr.

Source: ?The January 13, 1975, issue of Publishers Weekly, Published by R. R. Bowker, a Xerox company.? Copyright 1975 by the Xerox Corporation. ?Credit also to?aridni.com.

Before I write this evening, I would like to point out?what is going on with Horsehead Holdings [ZINCQ]. ?There was an article in the New York Times on it recently. ?It’s an interesting situation where an equity committee exists in a bankruptcy, largely because the management team looks like it is not trying to maximize the value of the bankruptcy estate, but is perhaps instead trying to sell the company off to creditors cheaply in an effort to receive a benefit later from the new owners. ?Worth a look, because if the equity committee wins, it will be unusual, and if the debtors win, it very well may take value that legitimately belonged to the equity.

That said, I don’t have a strong opinion because I don’t have enough data. ?But I will be watching.

=-=-=-=-=-=-==-=-=-=-=-=-=-=-=-=-=-=-=-=-=-=-

I received a letter from a reader yesterday on a related topic from my most recent article. ?Here it is:

Hi David,

First of all, it’s nice to find you (and Ed Yardeni and Mohamed El-Erian) working when most analysts seem to be at the beach. That said, a question:

In early ’09, as you will recall, the big banks were begging for relief from mark-to-market accounting for their holdings of mortgage-backed securities, on the grounds that these securities weren’t trading at all.

“Ridiculous!” said Jeremy Grantham. “Put 2 percent of your holding out to auction and you will learn its market value quick enough.”

At the time, I thought Grantham had a fair point. Now I’m not so sure.

What was your view on that issue? John Hussman has said repeatedly that it was the FASB’s relaxation of the mark-to-market rules that set off the dramatic resurgence in stock prices that we have seen (and which he deplores).

Was the FASB’s change of policy warranted, under the circumstances?

And should the mark-to-market rule now be restored?

Here was my reply:

Hi,

I wrote a lot about this at the time.? I remain in favor of mark-to-market accounting.? The companies that got into trouble from the effects of mark-to-market accounting had engaged in sloppy risk management practices, and got caught with their pants down.

The difficulty that most of the complaining companies had was a mix of liquid liabilities requiring prompt payment, and relatively illiquid assets that would be difficult to sell.? It was the classic asset-liability mismatch — long illiquid assets financed by short liquid liabilities.? Looks like genius during the bull phase.? Toxic during the bear phase.

On Grantham’s comments: my comments Saturday night are pertinent here for two reasons — anyone selling illiquid CDO tranches, subordinated mortgage bonds, etc., immediately prior to the crisis would find two things: 1) the bids were non-existent or really poor, and 2) if the trade did take place, it would be at levels that reset the pricing grid for that area of the market a LOT lower, leaving the remaining securities looking worse, and a diminution of GAAP equity.

(As an aside, the diminution of GAAP equity might affect the ability to do secondary IPOs of stock at attractive prices, but in itself it did not affect solvency of most financial firms, because statutory accounting allowed for investments to held at amortized cost.? As such the firms could be economically insolvent, but not regulatorily insolvent unless they ran out of cash, or their short-term lending lines of credit got pulled.)

The regulators were pretty lenient with most of the companies involved — the creditors weren’t.? They enforced margin agreements, and pulled discretionary credit lines.

I’m not of Hussman’s opinion that relaxation of the mark-to-market rules had ANY effect on stock prices.? In general, GAAP accounting rules don’t affect stock prices, because they don’t affect free cash flow, unless the GAAP rules are embedded in credit covenants.? Statutory accounting does affect free cash flow, and can affect the prices of stocks.

This post may be a little more complex than most. It will also be more theoretical. For those disinclined to wade through the whole thing, skip to the bottom where the conclusions are (assuming that I have any). 😉

Asset Prices are (Mostly) Validated by a Thin Stream of Transactions

One thing that I have been musing about recently is how few transactions exist to validate the pricing of various markets. ?I’ll start with two obvious ones, and then I will broaden out to some more markets that are less obvious. ?(Hint: markets that have a high level of transactions relative to the underlying asset value have a lot of speculative “noise traders.”)

Let me start with the market that I know best as far as this topic goes: bonds. ?Aside from some government and quasi-governmental bonds, very few bonds trade each day — less than a few percent. ?It’s very difficult to use the small volume of trades to price the whole market, but it can be done.

When I was a bond manager for a semi-major insurance company, I was the only one of the top managers that was a mathematician, and?familiar with all of the structures underlying the bonds. ?I could create my own models of bonds if needed, and I often did for interest rate risk analyses (which was still a responsibility amid bond management). ?Combined with my knowledge of insurance accounting, it made me ideal to do a certain monthly task: making sure all of the bonds got priced.

The first part of that isn’t hard. ?The pricing service typically covers 90-98% the bonds ?in the portfolio. ?What I would receive on the first day of the month was a list of all the bonds the pricing service could not calculate a price for. ?I would take that list and compare it to last month’s?list of the same bonds and add to it any new bonds we had bought that month, and who the lead dealer was. ?I would then ask the dealers for their prices on the bonds (which were typically illiquid). ?I would compare those prices to the prices of the prior month, and maybe ask a question or two about the prices that were out of line. ?That would usually elicit a comment from my coverage akin to, “The analyst thinks spreads have widened out for that credit because spreads in that industry have widened out, and a less liquid bond would widen out more. ?The why the price fell more (or rose less).

After that was done, that left me with a small number of utterly illiquid bonds that we had sourced totally privately, or where the dealers who had originated the bonds had ceased to exist. ?All of those deals lacked options to accelerate or decelerate payment, so it was a question of modeling the cash flows and applying an appropriate yield spread over the Treasury or Swap yield curve. ?[Note: the swap curve gives the yield rates at which AA-rated banks are willing to trade fixed rate exposures in their own credit for floating rate exposures in their own credit, and vice-versa.]

But what is appropriate and how did the three methods of getting prices differ? ?The second question is easier. ?They didn’t differ much at all. ?The dealers and I were likely doing the same things — just with different sets of bonds. ?The pricing service, on the other hand, was much more complex, and the other two methods relied on its results.

It was was called “grid” or “matrix” pricing, though it was much more complex than a grid or a matrix. ?The pricing service models would look at all of the most recent trades that had happened in the bond market, and use all of the prices to estimate yields that were adjusted for the options inherent in the bonds that could accelerate or decelerate payments. ?From that, they would piece together yield curves that varied by industry and collateral type, credit rating (agency or implied by a model that involved stock prices and equity option prices), individual creditors, etc. ?Trades on different days were adjusted for market conditions to make the?pricing?as similar as possible to the end of the month. ?After that the yield and yield spread curves generated would be applied to the structures of individual bonds with a adjustments for whether the bonds were:

premium or discount

large deals that were widely traded or small illiquid deals

callable or putable

senior or subordinate or structurally subordinate (a bond of a subsidiary not guaranteed by the parent company)

secured or unsecured

bullet or laddered maturities (sinking funds, etc.)

different currencies

and more

And there you would have a set of self-consistent prices that would price most of the bond universe. ?That’s not where transactions would necessarily take place… particularly with illiquid securities, what would matter most is who was more incented to make the trade happen — the buyer or the seller.

Implicitly, I learned a lot of this not just from modeling for risk purposes, but from trading a lot of bonds day by day. ?How do you make the right adjustments when you compare two bonds to make a swap, and, how much of a margin do you put in as a provision to make sure you are getting a good deal without the other side of the trade walking away? ?It’s tough, but if you?know how all of the tradeoffs work, you can come to a reasonable answer.

One more note before the summary. ?The less common it is for a bond or group of related bonds to trade, the more effect a trade has on the overall process. ?It becomes a critical datapoint that can redefine where bonds like it trade. ?Illiquidity begets volatile prices changes in the grid/matrix as a result. ?On the bright side, illiquidity is usually associated with small sizes, so it doesn’t affect most of the market. ?There is an exception to this rule: trades done during a panic or the recovery from a panic tend to be sparse as well. ?The trades that happen then can temporarily change a wider area of pricing. ?I remember that vividly from the whipsaw markets 2001-3, especially when the bond market was restarting after 9/11. ?If that crisis had happened later in the month, the quarterly closing prices might not have been as accurate.

Summary for Part 1 (Bonds)

The bond market is complex, far more complex than the stock market. ?Pricing the market as a whole is a complex affair, but one for which prices are reasonably calculable. ?For the average retail investor investing in ETFs, the bonds are liquidi enough that pricing of NAVs is fairly clean. ?But even for a large ugly insurance company bond portfolio, pricing can be significantly accurate. ?Next time, I’ll talk about a related market that has its own pricing grid(s) — mortgages and real estate. ?Till then.

In the time I have been managing money for myself and others in my stock strategy, I set a limit on the amount of cash in the strategy. ?I don’t let it go below 0%, and I don’t let it go over 20%.

I have bumped against the lower limit six or so?times in the last sixteen years. ?I bumped against it around five times in 2002, and once in 2008-9. ?All occurred near the bottom of the stock market. ?In 2002, I raised cash by selling off the stocks that had gotten hurt the least, and concentrating in sound stocks that had taken more punishment. ?In September 2002, when things were at their worst, I scraped together what spare cash I had, and invested it. ?I don’t often do that.

In 2008-9 I behaved similarly, though my household cash situation was tighter. ?Along with other stocks I thought were bulletproof, but had gotten killed, I bought a double position of RGA near the bottom, and then held it until last week, when it finally broke $100.

But, I had never run into a situation yet where I bumped into the 20% cash limit until yesterday. ?Enough of my stocks ran up such that I have been selling small bits of a number of companies for risk control purposes. ?The cash started to build up, and I didn’t have anything that I deeply wanted to own, so it kept building. ?As the limit got closer, I had one stock that I liked that would serve as at least a temporary place to invest — Tesoro [TSO]. ?Seems cheap, reasonably financed, and refining spreads are relatively low right now. ?I bought a position in Tesoro yesterday.

As it is, my actions are that of following the rules that discipline my investing, but acting in such a way that reflects my moderate bearishness over the intermediate term. ?In the short run, things can go higher; the current odds even favor that, though at the end the market plays for small possible gains versus a larger possible loss.

The credit cycle is getting long in the tooth; though many criticize the rating agencies, their research (not their ratings) can serve as a relatively neutral guidepost to investors. ?Corporate debt is high and increasing, and profits are flat to shrinking… not the best setup for longs. ?(Read John Lonski at Moody’s.)

I will close this piece by saying that I am looking over my existing holdings and analyzing them for need for financing over the next three years, and selling those that seem weak… though what I will replace them with is a mystery to me.

Bumping up against my upper cash limit is bearish… and that is what I am working through now.

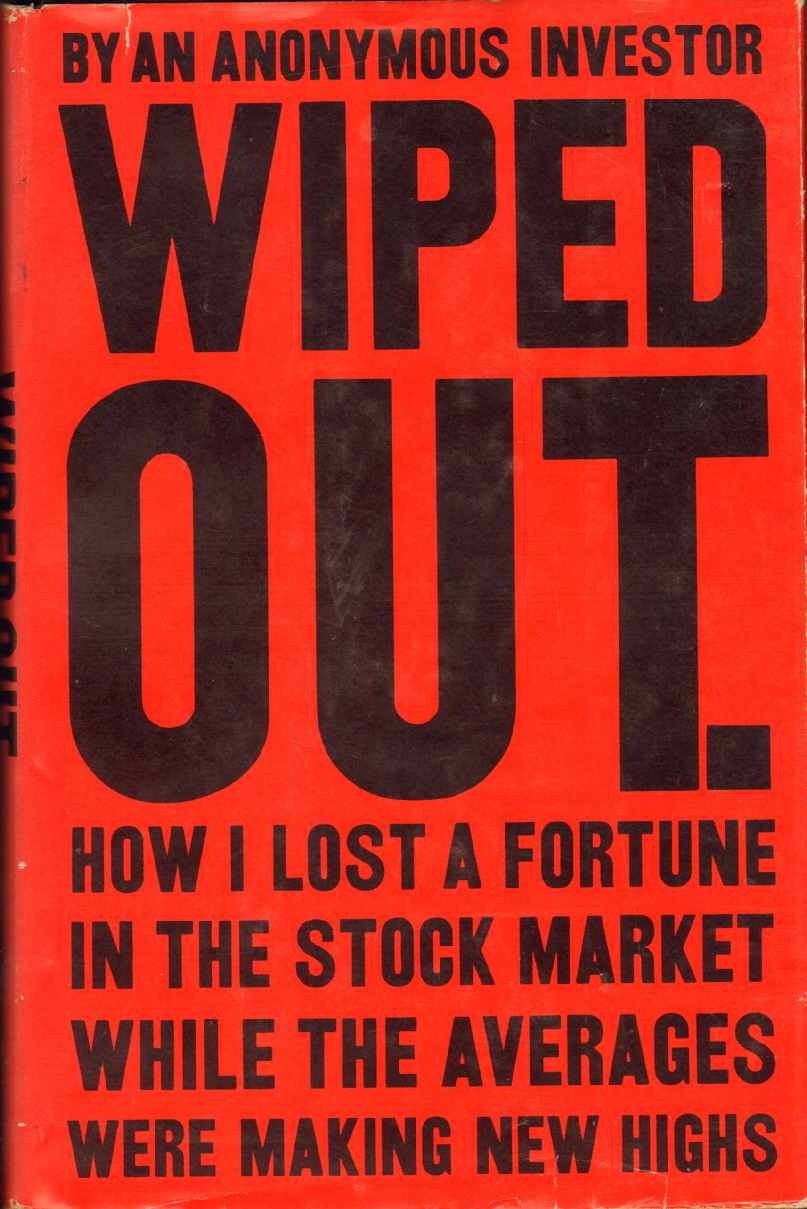

This is an obscure little book published in 1966. ?The title is direct, simple, and descriptive. ?A more flowery title could have been, “Losing Money in the Stock Market as an Art Form.” ?Why? ?Because he made every mistake possible in an era that favored stock investment, and managed to lose a nice-sized lump sum that could have been a real support to his family. ?Instead, he tried to recoup it by anonymously publishing ?this short book which goes from tragedy to tragedy with just enough successes to keep him hooked.

Whom God Would Destroy

There is a saying, “”Whom the gods would destroy, they first make mad.” ?My modification of it is, “Whom God would destroy, he first makes proud.” ?In this book, the author knows little about investing, but wishing to make more money in the midst of a boom, he entrusts a sizable nest egg for a young middle-class family to a broker, and lo and behold, the broker makes money in a rising market with a series of short-term investments, with very few losses.

Rather than be grateful, the author got greedy. ?Spurred by success, he became somewhat compulsive, and began reading everything he could on investing. ?To brokers, he became “the impossible client,” (my words, not those of the book) because now he could never be satisfied. ?Instead of being happy with a long-run impossible goal of 15%/year (double your money every five years), he wanted to double his money every 2-3 years. (26-41%/year)

As such, he moved his money from the broker that later he admitted he should have been satisfied with, and sought out brokers that would try to hit home runs. ?The baseball analogy is useful here, because home run hitters tend to strike out a lot. ?The analogy breaks down?here: a home run hitter can be useful to a team even if he has a .250 average and strikes out three times for every home run. ?Baseball is mostly a game of team compounding, where usually a number of batters have to do well in order to score. ?Investment is a game of individual compounding, where strikeouts matter a great deal, because losses of capital are very difficult to make up. ?Three 25% losses followed by a 100% gain is a 15% loss.

In the process of trying to win big, he ended up losing more and more. ?He concentrated his holdings. ?He bought speculative stocks, and not “blue chips.” ?He borrowed money to buy more stock (used margin). ?He bought “story stocks” that did not possess a margin of safety, which would maybe deliver high gains ?if the story unfolded as illustrated. ?He did not do homework, but listened to “hot tips” and invested off them. ?He let his judgment be clouded by his slight relationships with corporate insiders at the end. ?HE TRIED TO MAKE BIG MONEY QUICKLY, AND CUT EVERY CORNER TO DO SO. ?His expectations were desperately unrealistic, and as a result, he lost it all.

As he lost more and more, he fell into the psychological trap of wanting to get back what he lost, and being willing to lose it all in order to do so. ?I.e., if he lost so much already, it was worth losing what was left if there was a chance to prove he wasn’t a fool from his “investing.” ?As such, he lost it all… but there are three good things to say about the author:

He had the humility to write the book, baring it all, and he writes well.

He didn’t leave himself in debt at the end, but that was good providence for him, because if he had waited one more day, the margin clerk would have sold him out at a decided loss, and he would have owed the brokerage money.

In the end, he knew why he had gone wrong, and he tells his readers that they need to: a) invest in quality companies, b) diversify, and c) limit speculation to no more than 20% of the portfolio.

His advice could have been better, but at least he got the aforementioned ideas?right. ?Margin of safety is the key. ?Doing significant due diligence if you are going to buy individual stocks is required.

Quibbles

This book will not teach you what to do; it teaches what not to do. ?It is best as a type of macabre financial entertainment.

Also, though you can still buy used copies of the book, if enough of you try to buy the used books out there, the price will rise pretty quickly. ?If you can, borrow it from interlibrary loan. ?It is an interesting historical curiosity of a book, and a cautionary tale for those who are tempted to greed. ?As the author closes the book:

“Cupidity is seldom circumspect.”

And thus, much as the greedy need to hear this advice, it is unlikely they will listen. ?Greed is compulsive.

Summary / Who Would Benefit from this Book

A good book, subject to the above limitations. ?It is best for entertainment, because it will teach you what not to do, rather than what to do.

Full disclosure:?I bought it with my own money for three bucks.

If you enter Amazon through my site, and you buy anything, including books, I get a small commission. This is my main source of blog revenue. I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip. Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book. Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website. Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites. Whether you buy at Amazon directly or enter via my site, your prices don?t change.

Photo Credit: elycefeliz || Enron and some other US corporations have been ethics-hostile places also

=-=-=-=-=-=-=-=-=-=-=-

Yesterday I gave a talk on ethics to the incoming class at?The Johns Hopkins Carey Business School. ?As some of you might know, I received my BA and MA from Johns Hopkins in 1982 long before they had a business school. ?It was fun to talk to all of the entering MBA students who came to the school from all over the world. ?It largely serves international students.

At the end of my talk I took questions, both formally, and informally after the talk was over. ?The biggest question was, “Mr. Merkel, what you say about ethics might be the best policy for business in the US, but when I return to my home country, it will not be well-received. ?What should I do?”

This is a tough one. ?I think people have an easier time missing out on gains by being ethical than losing one’s job. ?But let me give a few ideas anyway.

Many countries where business ethics aren’t practiced set themselves up for financial crises and scandals. ?One strategy could be to bide your time and wait for the next large scandal or crisis. ?Then suggest to your management (assuming your firm survived) that managing in an ethical way could prevent these problems, and potentially attract more business to your firm.

Take a chance and try to create your country’s equivalent of Vanguard. ?Low cost, mostly passive investing, owned by clients, limited management salaries, etc.

Same as #2, but if you get the chance to start or run any firm, adopt ethical practices and make it a selling point. ?You could be the start of cultural change. ?(Now elements of that could prove difficult if there are government officials expecting bribes… how you work that out is difficult. ?Friends of mine working as missionaries in corrupt countries tell me that you can still get things done without bribes, but it takes longer, with more effort.)

Suggest to government ministers that a lack of ethics holds back growth. ?Countries with no bribery, low corruption, and moderate regulations tend to grow faster.

Propose small experiments in your firm testing whether an ethical approach will produce better results.

Consider working for a foreign firm in your country if they have ethical standards.

Consider gaining experience in a country other than your home country, and propose to that firm that they try setting up a subsidiary in your home country.

On the side, develop a voluntary organization that promotes ethical business conduct. ?Consider publishing some books that point out how unscrupulous business practices are harming most people. ?Recruit well-known foreign businessmen known for clean business practices to come talk in your country.

I can’t think of anything more right now. ?Readers, if you can think of other ideas, please mention them in the comments. ?Thanks.

PS — One more note, having worked for a few firms that were ethics-challenged as far as accounting and sales practices went, I can say that trying to promote change from inside is tough. ?Taking a job at another firm was my way out of those situations. ?No surprise that almost all of those firms failed.

WARNING ? On-Line Article Regarding Warren Buffett, BREXIT and Anderson Cooper is a Fraud

OMAHA, Neb.–(BUSINESS WIRE)–Berkshire Hathaway Inc. (NYSE: BRK.A; BRK.B) ?

It has come to Berkshire?s attention that there is an article on-line concerning Warren Buffett and BREXIT with respect to a conversation that Mr. Buffett allegedly had with Anderson Cooper. The article is headlined as follows ? ?Warren Buffett Warns ?BREXIT? Chaos is going to cost Millions of Americans Jobs.? For the record, Mr. Buffett has not spoken with Anderson Cooper for about five years and never about BREXIT.

The article among other fraudulent claims states that Mr. Buffett spoke with Mr. Cooper and indicated that Mr. Buffett was recommending something called ?The Global Cash Code.? Allegedly, per the on-line article, Mr. Buffett indicated that Sandra Barnes, the party who allegedly created ?The Global Cash Code,? has been teaching people how to successfully use ?The Global Cash Code.? Prior to learning of this fraudulent article, Mr. Buffett has never spoken with or even heard of Sandra Barnes.

Contacts

Berkshire Hathaway Inc. Marc D. Hamburg, 402-346-1400

There is no end of those that want to cash in on Warren Buffett. ?But those that know Buffett know that he doesn’t give investment advice aside from what he has written publicly himself. ?But to the uninformed, the pitch mentioned looks real enough.

I was curious, so I went looking for it, and I found a version of it here. ?It came up number one on my Google search. ?It looks like a fake CNN site, which fits the shtick of using Anderson Cooper interviewing Buffett. ?I decided to do a WHOIS search on the domain name “com-politics.us” to see if there was anything interesting. ?There was.

The domain was registered on June 28th, 2016. ?Here’s the data I found at the WHOIS site:

Name:?Devin Karapoulos

Organization:?Devin Karapoulos

Address:?1348 high bluff cir

City:?Park City

State / Province:?UT

Postal Code:?84060

Country:?United States

Phone:?1-435-214-1857

Email:?dkarapoulos@gmail.com

Now, that might not be the main site — the Global Cash Code site has hidden its owner, so you can’t tell, but who knows? ?That said, I can’t find another one. ?Maybe Mr. Karapoulos knows something about this misuse of Mr. Buffett’s name, likeness, and reputation.

Full disclosure: my clients and I own shares of BRK/B

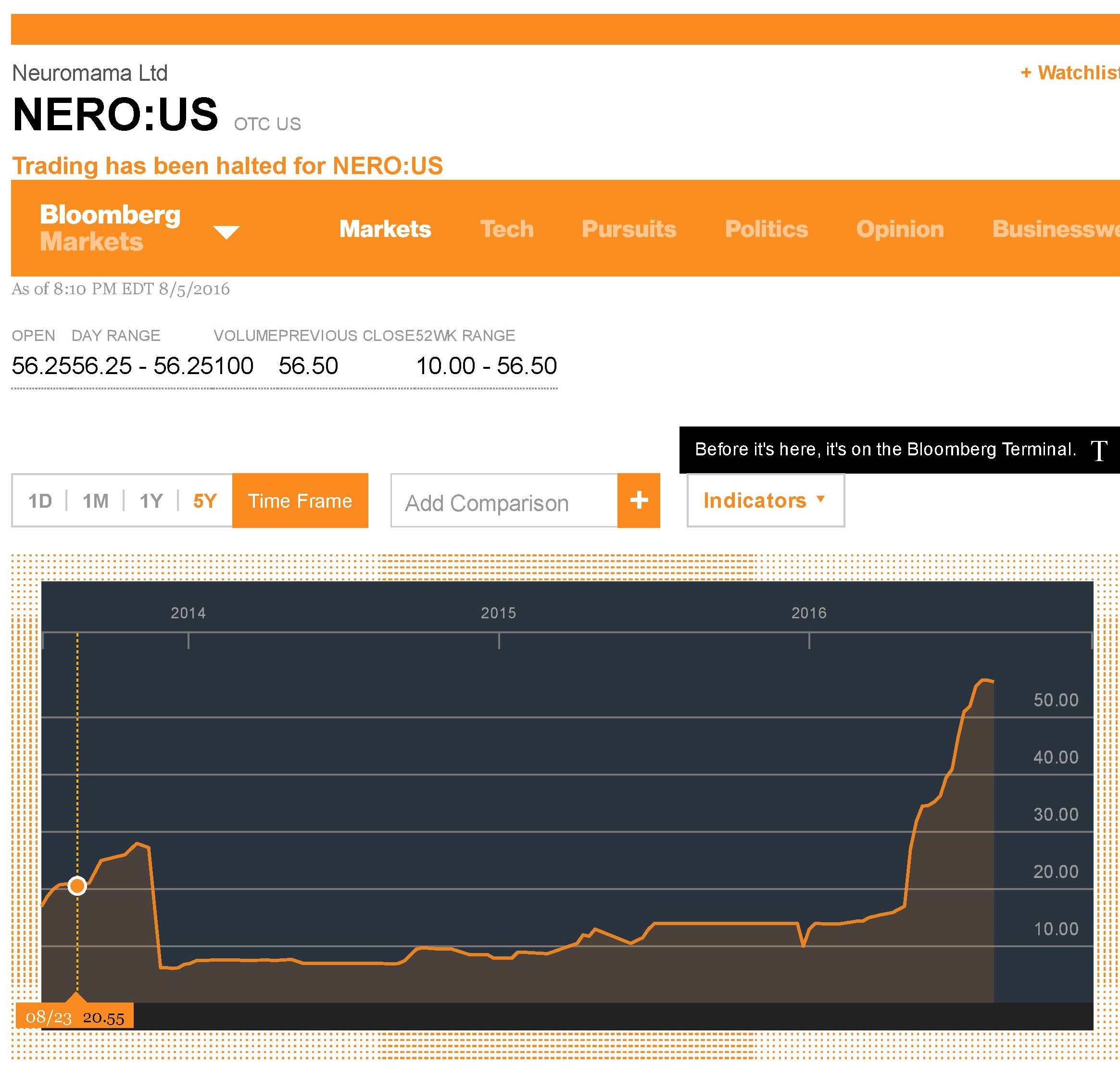

Would you like a 100?million-plus percent return on your money in a little more than four years? You would? Well, it can be done, but there are a couple of catches at the end that may prevent the enjoyment of the unearned riches.

If you read through the documents on Neuromama, it’s not different from what gets done with a penny stock to boost its value, and that is largely because it was a new penny stock when it was formed and started trading over-the-counter four years ago.

So how do you turn a sow’s ear into several billion silk purses? ?Simple:

In March 2011, start the?company for $3500. ?35MM shares at $0.001 each.

In 2012, sell?720,000 shares @ $0.03 each ($21,600) and go public. ?30x as expensive as the first valuation. ?Initial name is Trance Global.

In 2013, change the name to Neuromama, split the stock 750:1, and announce really big plans. ?Total shares: 3.1B+

Borrow $370,000?to develop a website, and do a few other things.

In late 2013,?acquire a Library of Entertainment Assets including variety shows, feature films, television pilots, etc. Acquire the Assets in exchange for 4,866,180 of new?common shares at a price of $20.55 (the closing price on September 3, 2013) for a total value of $100,000,000. ?The main owner cancels 80% of the?common shares (which belonged to him)?as an aspect of the deal.? (Note: no cash changes hands.) ?Total shares: ?630MM+

Never file another financial statement with the SEC. ?Issue occasional 8Ks, and engage in a running dialogue with the SEC over how the development stage company doesn’t earn any money and has negative tangible net worth.

In my opinion, buying the intangible assets and attributing a price of $20.55/share for the stock given in exchange?was the critical element of getting the market valuation so high. ?If you look at the graph at Bloomberg.com, and click the 5Y button, you will see that in late 2013 after the exchange was made, the stock price hovered in the $20s. ?(or, click on the image below for a static image of poorer quality abstracted from the Bloomberg website)

Picture Credit: Bloomberg.com

Here is a?market cap of $35 billion for this stock with no business, no appreciable assets, no proprietary technology, no tangible net worth and no income — and can’t even do a few filings with the SEC. ?(It looks like they gave up talking in September 2014.)

So what is it worth? ?My best estimate is zero, to the nearest billion. 😉 ?This is still a cash-starved developmental stage business with no revenues after five or so years. ?It has?had the chance to bootstrap a business together, and there is nothing except the website. ?The price should drop to something near zero when trading resumes.

Even if trading had not been halted, the ability of the owners to realize the value would have been quite limited. ?All they would have had to do is sell a 100,000 shares, and the stock price would collapse, because there is no one out there with $5 million of real cash that wants to buy 0.015% of an empty company like Neuromama. ?The interesting question is “who has been trading the stock,” because it is strictly speculative. ?It is possible that related parties have slowly pushed the price up.

Anyway, this is a good reason to stay away from developmental stage companies — really, anything that doesn’t generate significant revenue. ?It is also a reason to watch the fundamentals of a company rather than the stock chart only, which in this case has run up hard since 2014, but on almost no volume. ?The market capitalization is an illusion if there is nothing that can produce the cash flow to justify it.

Information received since the Federal Open Market Committee met in April indicates that the pace of improvement in the labor market has slowed while growth in economic activity appears to have picked up.

Information received since the Federal Open Market Committee met in June indicates that the labor market strengthened and that economic activity has been expanding at a moderate rate.

FOMC shades GDP down and employment up, which is the opposite of last time.

Although the unemployment rate has declined, job gains have diminished.

Job gains were strong in June following weak growth in May. On balance, payrolls and other labor market indicators point to some increase in labor utilization in recent months.

Sentence moved up in the statement.? Expresses less confidence in the labor market.

Growth in household spending has strengthened. Since the beginning of the year, the housing sector has continued to improve and the drag from net exports appears to have lessened, but business fixed investment has been soft.

Household spending has been growing strongly but business fixed investment has been soft.

Drops comments on the housing sector and net exports.

Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports.

Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports.

No change.

Market-based measures of inflation compensation declined; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy.

The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will strengthen.

The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will strengthen.

No change.

Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further.

Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further.

The Committee continues to closely monitor inflation indicators and global economic and financial developments.

Near-term risks to the economic outlook have diminished. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

No change.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent.

No change.

The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

No change.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

No change.? Gives the FOMC flexibility in decision-making, because they really don?t know what matters, and whether they can truly do anything with monetary policy.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

No change.? Says that they will go slowly, and react to new data.? Big surprises, those.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

No change.? Says it will keep reinvesting maturing proceeds of agency debt and MBS, which blunts any tightening.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Esther L. George; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo.

Back to a small dissent.

Voting against the action was Esther L. George, who preferred at this meeting to raise the target range for the federal funds rate to 1/2 to 3/4 percent.

Our favorite dissenter returns.

Comments

This statement was a nothing-burger.

Policy continues to stall, as the economy muddles along.

But policy should be tighter. Savers deserve returns, and that would be good for the economy.

The changes for the FOMC?s view are that labor indicators are stronger, and GDP and household spending are weaker.

Equities and bonds rise a little. Commodity prices rise and the dollar falls.? Everything is a little looser.

The FOMC says that any future change to policy is contingent on almost everything.

The key variables on Fed Policy are capacity utilization, labor market indicators, inflation trends, and inflation expectations. As a result, the FOMC ain?t moving rates up much, absent much higher inflation, or a US Dollar crisis.

{kind=link}