Caption from the WSJ: Regulators don?t think it is the place of Congress to second guess how they size up securities. Fed Chairwoman Janet Yellen said recently that legislation would ?interfere with our supervisory judgments.? PHOTO: BAO DANDAN/ZUMA PRESS

Catch the caption from the WSJ for the above picture:

Regulators don?t think it is the place of Congress to second guess how they size up securities. Fed Chairwoman Janet Yellen said recently that legislation would ?interfere with our supervisory judgments.?

Regulators are not required by the Constitution, but Congress, perverse as it is, is the body closest to the people, getting put up for election regularly. ? Of course Congress should oversee financial regulation and monetary policy from?an unelected Federal Reserve. ?That’s their job.

I’m not saying that the Congressmen themselves understand these things well enough to do anything — but that’s true of most laws, etc. ?If the Federal Reserve says they are experts on these matters, past bad results notwithstanding, Congress can get people who are experts as well to aid them in their decisions on laws and regulations.

The above is not my main point, though. ?I have a specific example to draw on: municipal bonds. ?As the Wall Street Journal headline says, are they “Safe or Hard to Sell?” ?For financial regulation, that’s the wrong question, because this should be an asset-liability management problem. ?Banks should be buying assets and making loans that fit the structure of their liabilities. ?How long are the CDs? ?How sticky are the deposits and the savings accounts?

If the maturities of the munis match the liabilities of the bank, they will pay out at the time that the bank needs liquidity to pay those who place money with them. ?This is the same as it would be for any bond or loan.

If a bank, insurance company, or any financial institution relies on secondary market liquidity in order to protect its solvency, it has a flawed strategy. ?That means any market panic can ruin them. ?They need table stability, not bicycle stability. ?A table will stand, while a bicycle has to keep moving to stay upright.

What’s that you say? ?We need banks to do maturity transformation so that long dated projects can be cheaply funded by short-term savers. ?Sorry, that’s what leads to financial crises, and creates the run on liquidity when the value of long dated assets falls, and savers want their money back. ?Let long dated assets that want debt financing be financed by REITs, pension plans, endowments, long-tail casualty insurers, and life insurers. ?Banks should invest short, and use the swap market t aid their asset liability needs.

Thus, there is no need for the Fed to be worrying about muni market liquidity. ?The problem is one of asset-liability matching. ?Once that is settled, banks can make intelligent decisions about what credit risk to take versus their liabilities.

In many ways, our regulators learned the wrong lessons in the recent crisis, and as such, they meddle where they don’t need to, while neglecting the real problems.

But given the strength of the banking lobby, is that any surprise?

Before I start this evening, I want to add one follow-up to last night’s piece on Berkshire Hathaway. ?My summary was that it wasn’t a great year, and the profit margins are likely to shrink in insurance, because BRK is being conservative there. ?So why do I still own it for my clients and me?

BRK is trading maybe 8% over the level at which it would begin buying back stock. ?Even in a pessimistic year, I expect BRK’s book value to rise to the level that triggers the buyback. ?Thus, I think the floor for the stock is pretty close below me, and there is a decent possibility that Buffett could do some things with the cash that are even better than buybacks, especially if the market falls into bear territory.

It is positioned well for most market environments, even one where insurance gets hit hard. ?BRK is “the last man standing” in any insurance crisis — they have the ability to prosper when other companies will have their capital impaired, and can’t write as much business as they want.

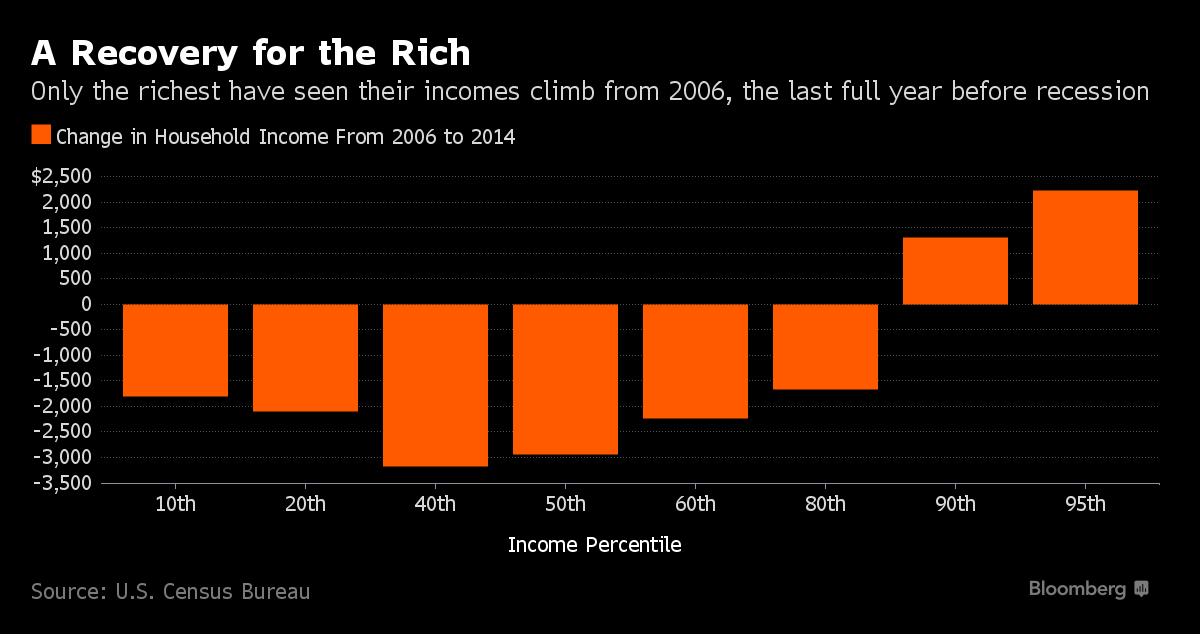

Incomes have not improved for the bottom 80% of Americans over the last decade. ?Before I go on, recognize that the income distribution is not static. ?The same people are not in each decile today, as were in 2006. ?Examples:

Highly skilled students in a field that is in demand graduate and get jobs that pay well.

Highly skilled immigrants?in a field that is in demand come to the US?and get jobs that pay well.

Less skilled people who relied on the private debt culture to keep getting larger no longer have jobs that pay well in finance, construction, real estate, etc.

Workers and businessman who expected the commodities and crude oil boom to go on forever have seen their prospects diminish.

Some people have retired and their income has fallen as a result.

Layoffs have come in some industries because many people did not realize that they were lower skilled workers, and as such the work that they did could be automated or transferred to other countries.

Manufacturing continues to get more efficient, and we need fewer jobs in manufacturing to produce the same output (or more). ?This is true globally; manufacturing jobs are being reduced globally.

Technology firms that apply the advantages of the internet gain value, while legacy firms lose value. ?Whole classes of goods go away because they are replaced, and in other cases, some firms find that they can’t price their products to make a decent profit, while other firms can.

Some effects are demographic, like mothers ceasing work to raise children, or industries with a lot of older workers becoming uncompetitive because their pension plans are too expensive to fund.

Divorce usually ruins the prospects of the wife, if not the husband.

Throw in death, disability, substance abuse, and serious diseases.

And more…

Thus there is a lot of reason to look at the graph and not say, “The rich are getting richer,” but, “Those who are getting rich today are doing so faster than those who were getting rich back in 2006.”

My life is even an example of that… I make less than 30% of what I was making in 2006. ?On an income basis, I’ve gone from the top of the graph to the middle. ?I’m not upset, because I’m debt free, and manage my finances well. ?I’m grateful to have my own little firm, and every client that I have.

Resentment

That said, many feel that the comfortable life that was theirs has been denied to them by forces beyond their control. They think that shadowy elites want to turn previously well-off people into modern serfs.

It’s a tempting thought, because most of us don’t like to blame ourselves. ?Myself included, we all make mistakes. ?Here is a sampling:

Did we make a bad decision in the industry in which we chose to work? ?The particular firm?

Did we choose a bad field of study in college? ?Rack up too much student loan debt?

Did we borrow too much money at the wrong time? ?(Remember, debt is always a risk. ?If you don’t know that, you shouldn’t borrow money.)

Did you make bad decisions regarding your assets, and get too greedy or fearful at the wrong times?

Did you spend too much during your good years, and not save enough for the future?

Did you not buy the insurance that would have protected you from the disaster that hit you?

Throw in relationship errors, etc.

The truth is, changes in technology, and to a lesser extent demography, affect the entities that we work in, and affect our personal economics as a result. ?There are some politicians blaming immigrants for our problems, and that’s not a major source of our difficulties. ?Most people don’t want to do the work that unskilled immigrants do, and skilled immigrants get hired when there aren’t enough people seeking those positions.

There is a need for retraining, but even that has its difficulties, as technology is changing rapidly enough that more areas may face job reductions. ?Again, this is a global thing. ?Those that think that?making trade less free will help matters are wrong. ?It’s not trade; it’s technology.

Some think that matters can be fixed by changing government taxes and spending. ?That would only help limitedly, if at all. ?Businesses and people can move to other countries. ?In an era of the internet, many more things can move than ever did previously.

Now, if the developed ?countries collaborated to unify tax policies, some of that would end. ?But cheating under such a regime is too tempting, just as Indiana and Wisconsin try to attract businesses to move out of Illinois. ?The relatively healthy governmental entities have advantages that allow them to prosper at the expense of the sick ones.

You’re Going to be Disappointed

Politicians live to promise. ?I can tell you right now that not one of the surviving candidates for President has a realistic proposal that could be voted up by the next Congress or the buyers in the US Treasury market. ?It’s all airy-fairy… just as most politicians have been since we stopped running balanced budgets.

I would encourage you therefore to look at your own situation and resources soberly, and assume that the next government will do nothing better for you than the current one. ?All of the main drivers of what could improve matters for the middle class are outside the power of any individual government, so plan your own situation accordingly and adjust your economic expectations down. ?After all, there is no place in the world that can promise its people prosperity. ?Why should the USA be any different in this matter?

Last year, when BRK [Berkshire Hathaway] reported their annual earnings with the letter, report, and 10K, I concluded:

From an earnings growth standpoint, there was nothing that amazing about the earnings in 2014. ?A few new subsidiaries like NV Energy added earnings, but existing subsidiaries? earnings were flattish. ?Comprehensive income was considerably lower because of the lesser degree of unrealized appreciation on portfolio holdings.

On net, it was a subpar year for Berkshire Hathaway. ?The annual letter provided a lot of flash and dazzle, but 2014 was not a lot to write home about, and limits to the BRK business model with respect to float are becoming more visible.

What I said one year ago would be a good summary for this year, though Buffett was more upbeat about outcomes this year, with BRK’s book value advancing while the S&P 500 fell on a total return basis.

Overall, BRK had a mediocre year. ?Insurance wasn’t that great. ?Here are my summary points:

BRK is reducing reinsurance — i suspect they aren’t getting the rates that they want. ?There are too many reinsurance wannabes attempting to write business to generate float that they can invest against. ?Typically, writing insurance in order to invest usually doesn’t work out. ?People forget how much money was lost writing marginal insurance business in soft markets thinking they would more than make up the losses with investment income. ?BRK is showing some discipline here — good.

Aside from new lines of business (specialty insurance), growth is slowing; BRK is trying to remain a conservative underwriter.

Reserving conservatism has not changed.

Asbestos position has not materially changed.

GEICO had a bad year for claims — maybe they grew too much, and maybe picked up a lower class of auto driver.

Profit margins falling

Float growth slowing

Continued problems with workers’ comp and long-term care at Gen Re. ?Also problems with payment annuities (blames FX, should blame longevity) and Life Reinsurance.

A few?quotes from the 10K on insurance issues:

“We define pre-tax catastrophe losses in excess of $100 million from a single event or series of related events as significant. In 2015, we recorded estimated losses of $136 million in connection with a property loss event in China.”

and on GEICO:

“Losses and loss adjustment expenses incurred in 2015 increased $2.7 billion (17.1%)?over 2014. Claims frequencies (claim counts per exposure unit) in 2015 increased in all major coverages over 2014, including property damage and collision coverages (three to five percent range), bodily injury coverage (four to six percent range) and personal injury protection (PIP) coverage (one to two percent range). Average claims severities were also higher in 2015 for property damage and collision coverages (four to five percent range), bodily injury coverage (six to seven percent range) and PIP coverage (two to four percent range). We believe that increases in miles driven, repair costs (parts and labor) and medical costs, as well as weather conditions contributed to the increases in frequencies and severities.”

Regarding Gen Re:

“The property/casualty business generated pre-tax underwriting gains in 2015 of $944 million compared to $1.4 billion in 2014. In 2015, we incurred losses of $86 million from an explosion in Tianjin, China. There were no significant catastrophe losses in 2014. Underwriting results in 2015 included comparatively lower gains from property catastrophe reinsurance and the run off of prior years? business.”

I found the mention of two large loss events in China interesting — maybe it was just one event of $136 million, but they could have been more clear.

Float Note

Before I leave the topic of insurance, I do want to set the record straight on how valuable float is. ?This is my best article on the topic. ?Buffett is a bit of a salesman in his annual letter, but generally an honest one.

Float is only as good as the insurance business generating it. ?If it is generating underwriting losses, the investments will have to earn at least as much per year as the losses divided by the average duration of how long the float will exist in years, in order to break even.

We’re coming off of years where there have been no underwriting losses, so float is?magical — but the P&C insurance industry is getting more competitive, and float will no longer be costless.

Widespread use of float for financing is like trying to finance off of other seemingly costless liabilities — in the hands of some?investors, that can lead to disaster — after all, consider all of the disasters that I have written about where people finance short to invest long.

Conservative insurers invest their premium reserves in cashlike instruments, and their loss reserves they invest in bonds of a similar duration. ?They typically don’t invest float in equities, and certainly not whole businesses.

Buffett has done just that and done well. ?That said, he runs his insurers at lower levels of leverage than most insurers, to allow room for taking more investment risk.

Note that BRK doesn’t guarantee the debts of BNSF, BHE, etc., but does guarantee the debts of the finance arms.

There is room for another article on float and cost of capital — not sure when I will get to it, but it will be a WACC-y article. 😉

Final Notes:

1) Note that Buffett keeps profits overseas also. Quoting the 10K: “We have not established deferred income taxes on accumulated undistributed earnings of certain foreign subsidiaries. Such?earnings were approximately $10.4 billion as of December 31, 2015 and are expected to remain reinvested indefinitely.” ?My guess is that he will use them to buy a foreign subsidiary.

2) BRK Pays taxes at about a 30% rate.

3) Regarding his comments on goodwill amortization — he thinks some of it is economically valid, and some not. ?Buffett has the option of putting more data on the income statement if he wants. ?Or put it in note 11 (goodwill). ?He already does that by breaking apart revenues and expenses by corporate divisions on the income statement. ?Do us all a favor, BRK, and split the goodwill into what you think is economically valid, and what is not.

4) Buffett gives an extended defense of Clayton Homes lending. ?In general, I thought his points were good — even before Buffett, Clayton was the “class act” in manufactured housing, and financing it.

5)?Even BRK has underfunded pension plans, and it has a relatively conservative 6.5% expected return on assets.

6) I note a modest change in 10K risk factors — BNSF and the automatic braking issue. ?BNSF will have to spend a lot of money to deal with the need to stop runaway trains remotely. ?True of all?US and Canadian railroads.

7)?BRK has less free cash flow to invest in new projects because more of their businesses are capital-intensive. ?BRK invested $16B in property, plant and equipment.

8 ) BNSF had a good year. ?BH Energy had a good year, mostly from a new Canadian Transmission utility, and their home brokerage arm.

9) BRK bought Precision Castparts, Van Tuyl (auto dealerships), and AltaLink (the Canadian Transmission utility). ?Also bolt-ons to existing subsidiaries.

10) Kraft merged with Heinz.?Heinz preferred will be redeemed.

11) The big four publicly traded firms owned by BRK didn’t have a good year. AXP, KO, IBM, WFC — he bought more of IBM and WFC. ?Buffett argues that the retained earnings of the firms benefit BRK. ?I’m dubious. ?IBM has particularly been a dog — look at free cash flow. ?Much of the earnings at IBM?aren’t real. ?You can’t use what they don’t dividend.

12) Quoting Buffett from his section?on optimism about the US, he tempered it by saying: “Though the pie to be shared by the next generation will be far larger than today?s, how it will be divided?will remain fiercely contentious.”

Well, you can say that again, but fairness is a squishy concept. ?Is fairness:

Even division (from each according to his ability, to each according to his needs)

Proportionate to productivity

Equal to what you negotiate

Derived from the formula of a bureaucrat

What you can negotiate through the political process

Impossible

Or something else?

Buffett worked with the easy stuff, and waved his hands at the hard stuff. ?I’ll phrase it this way: in general, the US has done well because we have not wrangled as much as the rest of the world over distribution issues, and have left a lot of room for people to?gain a lot from their own productivity. ?That has led to a lot of wealth, and in general, a growing pie for everyone to benefit from.

Productivity goes in waves, and labor plays catchup with capital after technological progress. ?We have seen people redeployed from agriculture and servanthood/slavery in the past 150 years. ?We will see them redeployed from manufacturing in the next 100 years. ?They will provide services to their fellow men, should there continue to be peace and tranquility, allowing labor income to catch up with that of capital.

Photo Credit: Friends of the Earth International || Note: the above is just a photo to illustrate a point. I do not endorse debt cancellation under most circumstances. ?I do support debt-for-equity swaps to delever the system.

Debt, debt, debt…?debt is kind of like a snowflakes. ?A single snowflake is a pretty star, but one quintillion of them is a horrendous mess. ?In the same way, most individual debts are reasonable and justifiable, but when debt becomes a pervasive part of the economic system, the second order effects kick in:

As fixed claims grow relative to equity claims, the economy becomes less flexible, because many are counting on the debts for which they are creditors to be paid back at par.

Economies that are heavily indebted grow slower.

Central banks following untested and dubious theories like QE and negative interests rates try help matters, but end up making things worse. ?(Gold would be an improvement. ?Just regulate the solvency of banks tightly, which was not?done in cases where?the gold standard failed.)

Political unrest leads to dubious populism, and demands for debt cancellation, and a variety of other quack economic cures.

The most solvent governments find high demand for their long debt. ?Long-dated claims raise in value as inflation falls along with monetary velocity.

Thus the mess. ?Bloomberg had an article on the topic recently, where it tried to ask whether and where there might be a crisis. ?I’ve argued in the last year that we shouldn’t have a major crisis in the US over domestic debts. ?There are a few areas that look bad:

Student loans

Agriculture loans

Corporate debts to speculative grade companies that are negatively affected by falling crude oil and commodity prices.

Maybe some auto loans?

But those don’t add up to a debt market in trouble as when residential mortgages were on the rocks.

But what of other nations and their debts, public and private?

Tough question.

That said, the answer is akin to that for a corporation with a tweak or two. ?It’s not the total amount of indebtedness versus assets or income that is the main issue, it is whether the debts can continue to be rolled over or not. ?A smaller amount of debt can be a much larger problem than a bigger amount that is longer. (point 2 below)

Take a step back. ?With countries there are a variety of factors that would make skeptical about their financial health:

Large increases in indebtedness

Large amounts of short-term debt

Large amounts of foreign currency-denominated liabilities (also true of the entire Eurozone — you don’t control the value of what you will pay back)

A fixed, or pseudo-fixed exchange rate (versus floating)

A weak economy, and

Debt and/or debt service to GDP ratios are high

The first point is important because whatever class of debt increases the most rapidly is usually the best candidate for credit troubles. ?Debt that is issued rapidly rarely gets put to good uses, and those that buy it usually aren’t doing their homework.

Under ordinary circumstances, this would implicate China, but the Chinese government probably has enough resources to cover their next credit crisis. ?That won’t be true forever, though, and China needs to take steps to make their banking system sound, such that it never generates losses that an individual bank can’t handle. ?Personally, I doubt that it will get there, because members of the Party use the banking system for their own benefit.

Points 3, 4, and 6 deal with borrowers compromising on terms in order to borrow. ?They are stretching, and accepting?terms not adjustable in favor of the debtor, or can be adjusted against the debtor. ? If you control your own currency, these problems are modified, because of the option to print currency to pay off debt, and inflate problems away. (Which creates other problems…)

By pseudo-fixed interest rates, I take into account countries that as neo-mercantilists make policy to benefit their exporters at the cost of their importers and consumers. ?These countries fight changes in the exchange rate, even though the exchange rate may technically float.

Point 5 simply says that there is insufficient growth to absorb the increases in debt. ?Economies growing strongly rarely default.

Conclusion?

My view is this: the next major credit crisis will be an international one, and will involve governments that can’t pay on their debts. ?It won’t include the US, the UK, and certainly not Canada. ?It probably won’t involve China. ?Weak parts of the Eurozone and Japan are possibilities, along with a number of emerging markets.

And, as an aside, if?this happens, people will lose faith in central banks as being able to control everything. ?I think the central banks and national treasuries will find themselves hard pressed to find agreement at that time. ?QE and negative interest rates might be controllable in a domestic setting, but in an international framework, other nations might finally say, “Why would I want to get paid back in that weak currency?” ?(And what holds that back now is that virtually all of the world’s currencies except gold are involved in competitive devaluation to some extent.)

My advice is this: be careful with your international holdings. ?The world may be peaceful right now, and everyone may be getting along, but that might not last. ?Diversification is a good idea, but don’t forget that there is no place like home, unless the crisis is in your home.

There are many ways to try to cheat people in the investment world. ?You can promise them:

No risk (an appeal to fear)

High returns (greed)

Secret knowledge (can appeal to either or both fear and greed)

An easy life, free from the worries common to man.

And more…

For virtually every human weakness or sin, there is a road to cheating men. ?This is why it is difficult to cheat a truly honest man, because an honest man is:

Industrious — he knows most ways to improve his lot in life involve considerable work, whether physical or mental.

Skeptical — he knows not everyone is honest, and there are many that pursue ways that harm themselves or others.

Self-controlled — he doesn’t need to become wealthy, but if it comes bit-by-bit, he can handle it.

Unafraid — he doesn’t scare easily, and there are many purported scares out there. ?There are always people trying to make money off of apocalyptic scenarios. ?(Believe me, in a truly apocalyptic scenario, where the government breaks down, or you lose a war on your home soil — no one wins. ?And, there is no way to prepare.)

Studious, and has wise?friends — he doesn’t quickly buy novel reasoning, or unfamiliar concepts without testing them, and running them past his personal “brain trust.”

Patient — he can’t be rushed into something, and he can walk away.

Virtuous — when he does commit, he holds to it, and makes good on what he promised. ?He expects the same of others, and does not deal with those of bad reputation.

There’s more, and I don’t hold myself out to be perfect here, but that is a part of what I aim for. ?If you are like this, you will be very difficult to cheat.

The Dishonest Pitch

With that wind-up, here is the pitch: I ran across a video while doing my usual work, when I saw a picture of Buffett. ?Now, everyone wants to invoke Buffett because he is a genuinely bright guy on all affairs affecting money and wealth. ?Many who do so twist what Buffett has done for their own ends. ?You can see the graphic used to the left.

So this guy posits that Buffett got rich off of “Guaranteed Income Certificates.” ?You can listen to the whole 39-minute video, and never learn what a?Guaranteed Income Certificate is. ?This is a tactic to make you think that the video-maker has hidden knowledge. ?He does not lie, per se, but dances around what it is and how Buffett has used them. ?I figured out what he was talking about in a about two?minutes, but only because the language was so discursive, with many rabbit-trails.

So what is the vaunted?Guaranteed Income Certificate?

Preferred stock.

Preferred stock?

Yes, preferred stock, that hoary creation that gets wiped out when most firms go into bankruptcy. ?There are few cases where the preferred stock is worth anything in a crisis. ?It is far from guaranteed. ?It has all of the disadvantages of a bond, with none of the countervailing advantages of common stock, which can provide strong returns.

Geek note: why is preferred stock called preferred? ?Three, maybe four reasons:

Its dividend payment can only be unpaid if the common dividend is unpaid first. ?It has a dividend payment priority.

If the dividend is eliminated, preferred stockholders as a group typically gain representation on the Board of Directors.

In bankruptcy, they receive preference over the common shareholders when the company is recapitalized or liquidated. ?That said, in bad scenarios, their claim is the second lowest of all claims — behind the secured creditors, the government, lawyers, general creditors, bank debt, and unsecured bonds. ?Believe me, that preference on common shareholders is not a big protection.

The preferred dividend is usually, but not always higher than the common dividend.

All preferred stock is is a promise to pay dividends if the company can do so without going broke, and ahead of the common shareholders. ?Like all risky investments, you can lose it all. ?Average recovery in bankruptcy for?preferred?stock is?around 5 cents on the dollar, versus 40 cents for most bonds,and 80 cents on bank debt.

Now, Buffett has done some clever things with preferred stock that is convertible into common stock, or alongside common stock or warrants. ?Occasionally he has bought some regular preferred stock as an income vehicle for his insurance companies. ?But Buffett almost never plays merely for income, he wants the gains that come from stocks.

Now, I didn’t listen to the whole video — after five minutes of the beautiful voice dancing around the issue, I stopped it, right clicked, downloaded it, and went?to the end. ?As is common with these sorts of videos, it makes it sound easy, as if infinite income could be yours if you just buy this service. ?They sell you on what your dream life will be like: you will have more than enough money for vacations, you’ll never have to work again, you can spend as much time visiting the faraway grandchildren…

The guy who put the video together, and sells his service, was big on hiding things behind new names that he concocted:

Preferred stock becomes Guaranteed Income Certificates

Venture Capital / Private Equity becomes Doriot Trusts

Master Limited Partnerships?become Secret Oil income Streams

Royalty Trusts are treated as a novel investment, rather than the backwater that it is.

The presentation is also expert in lying with true statistics, making the ordinary sound extraordinary. ?It also has the “but wait, there’s more!” pitch, where they throw in a bunch of old reports to make the deal seem sweeter. ?The cost of the newsletter if saved for the very end — beware of those that won’t tell you the cost up front. ?Good deals will always show you the price early. ?Charlatans hide the price.

There are no secrets. ?There is no easy road to an easy, wealthy life. ?I want to end this post ?the way I ended a similar post called “On the 770 Account,” which was a code name for permanent life insurance. [Sigh. ?Oddly, that post still gets a lot of hits, probably because no one has stepped forward to call that one out.]

Final Note

THERE ARE NO SECRETS IN MONEY MANAGEMENT! ?THERE ARE NO SECRETS IN MONEY MANAGEMENT! ?THERE ARE NO SECRETS IN MONEY MANAGEMENT!

There is no secret club. ?There are no secret formulas. There are a lot of clever lawyers, accountants, and actuaries that the wealthy employ, but for average people, the high fixed costs won?t make it work.

If you want to be wealthy, you have to run your own firm, run it well, providing value to many. ?Don?t listen to those who say they have an easy way to wealth. ?They are lying, and are looking to make money off of you. ?Those who give you free advice are using you in some way. ?(Wait, what does that make me to be? Sigh.)

Signing off, your servant David, who does this for his own reasons?

In some ways, this is a boring time in insurance investing. ?A lot of companies seem cheap on a book and/or earnings basis, but they have a lot of capital to deploy as a group, so there aren’t a lot of opportunities to underwrite or invest wisely, at least in the US.

As I have also pointed out before AIG’s reserving was liberal, and recently AIG took a $3.6 billion charge to strengthen reserves. ?Thus I am not surprised at the rating actions of Moody’s, S&P, ?and AM Best. ?Add in the aggressive plans to use $25 billion to buy back stock and pay more dividends?over the next two years, and you could see the ratings sink further, and possibly, the stock also. ?The $25 billion requires earning considerably more than what was earned over the last four years, and more than is forecast by sell-side analysts, unless AIG can find ways to release capital and excess reserves (if any) trapped in their complex holding company structure.

Improving?the Commercial P&C accident year loss ratio by 6 points

Targeted divestitures (United Guaranty, and what else gets you to $6 billion?)

Reinsurance (mostly life)

Borrowing $3-5B (maybe more after the $3.6B writedown)

Selling off some hedge fund assets to reduce capital use. (smart, hedge funds earn less than advertised, and the capital charges are high.)

Okay, this could work, but when you are done, you will have reduced the earnings capacity of the remaining company. ?Reinsurance that provides additional surplus strips future earnings out the the company, and leaves the subsidiaries inflexible. ?Trust me, I’ve worked at too many companies that did it. ?It’s a lousy way to manage a life company.

Expense reduction can always be done, but business quality can suffer. ?Improving the Commercial lines loss ratio will mean writing less business in an already overcompetitive market — can’t see how that will help much.

I don’t think the numbers add up to $25 billion, particularly not in a competitive market like we have right now. ?This is part of what I meant when I said:

…it would pay Carl Icahn and all of the others who would be interested in breaking up AIG to hire some insurance expertise. ?Insurance is a set of complex businesses, and few understand most of them, much less all of them. ?It would be easy to naively overestimate the ability to improve profitability at AIG if you don?t know the business,? the accounting, and how free cash flow emerges, if it ever does.

They might also want to have a frank talk with Standard and Poors as to how they would structure a breakup if the operating subsidiaries were to maintain all of their current ratings. ?Icahn and his friends might be surprised at how little value could initially be released, if any.

Thus I don’t see a lot of value at AIG right now. ?I see better opportunities in MetLife.

MetLife is spinning off their domestic individual life lines, which is the core business. ?I would estimate that it is worth around 15% of the whole company. ?In the process, they will be spinning off most of their ugliest liabilities as far as life insurance goes — the various living benefits and secondary guarantees that are impossible to value in a scientific way.

The main company remaining will retain some of the most stable life liabilities, the P&C operation, and the Group Insurance, Corporate Benefit Funding, and the International operations.

I look at it this way: the company they are spinning off will retain the most capital intensive businesses, with the greatest degree of reserving uncertainty. ?The main company will be relatively clean, with free cash flow being a high percentage of earnings.

I will be interested in the main company post-spin. ?At some point, I will buy some MetLife so that I can own some of that company. ?The only tough question in my mind is what the spinoff company will trade at.? Most people don’t get insurance accounting, so they will look at the earnings and think it looks cheap, but a lot of capital and cash flow will be trapped in the insurance subsidiaries.

There is no stated date for the spinoff, but if the plan is to spin of the company, a registration statement might be filed with the SEC in six months, so, you have plenty of time to think about this.

Get MET, it pays.

One Final Note

I sometimes get asked what insurance companies I own shares in. ?Here’s the current list:

Long RGA, AIZ, NWLI (note: illiquid), ENH, BRK/B, GTS, and KCLI (note: very illiquid)

In general, I tend not to go in for macro themes. ?Why? ?I tend to get them wrong, and I think most investors?also get them wrong, or at least, don’t get them right consistently.

I do have one macro theme, and it has served me well for a long time, though not over the past two years. ?I was using the theme as early as 2000, but finally articulated it in 2006.

At that time, I was running my equity strategy for my employer, as well as in my personal account. ?They used it for their profit sharing plan and endowment. ?They liked it because it was different from what the firm did to make money, which was mostly off of financial companies, both public and private. ?They didn’t want employees to worry that their accrued profit sharing bonuses would be in jeopardy if the firm’s ordinary businesses got into trouble. ?In general, a good idea.

At the end of the year, I needed to give a presentation to all of the employees on how I had been managing their money. ?Because my strategies had been working well, it would be an easy presentation to make… but as I looked at the prior year presentation, I felt that I needed to say more. ?It was at that moment that the macro theme that i had been working with became clear to me, and I called it: Our Growing World.

The idea is this: in a post-Cold War world where most economies have accepted the basic idea of Capitalism to varying degrees, there should be growth, and that growth should create a growing middle class globally. ?This middle class would be less well-off than what we presently see in America and Western Europe, at least not initially, but would manifest itself in a lot of demand for food, energy, and a variety of commodities and machinery as the middle class grew.

Now, I never committed everything to this theme, ever. ?Maybe one-third of the portfolio was influenced by it, on averaged. ?Most of what I do was and still is more influenced by my industry models, and by bottom-up stock-picking.

That said, the theme has a cyclical bias, and cyclicals have been kicked lately. ?I still think the theme is valid, but will have to?wait for overinvestment and overproduction in certain industries to get rationalized globally. ?Were this only a US problem, it might be easier to deal with because we’re far more willing to let things fail, and let the bankruptcy process sort these matters out. ?Governments in the rest of the world tend to interfere more, particularly if it is to protect a company that is a “national champion.”

But the rationalization will take place, and so until then in cyclical industries I try to own financially strong companies that are cheap. ?They will survive until the cycle turns, and make good money after that. ?That said, the billion dollar question remains — when will the cycle turn?

More next time, when I write about my industry model.

This is the first of a series of related posts. ?I took a one month break from blogging because of business challenges. ?As this series progresses, I will divulge a little more about that.

When I look at stocks at present, I don’t find a lot that is cheap outside of the stocks of companies that will do well if the global economy starts growing more quickly?in nominal terms. ?As it is, those companies have been taken through the shredder, and trade near their 52-week lows, if not their decade lows.

Unless an industry can be done away with in entire, some of the stocks an economically sensitive industry will survive and even soar on the other side of the economic cycle. ?At least, that was my experience in 2003, but you have to own the companies with balance sheets that are strong enough to survive the through of the cycle. ?(In some cases, you might need to own the debt, and not the common equity.)

The hard question is when the cycle will turn. ?My guess is that government policy will have little to do with the turn, because the various developed countries are doing nothing to clear away the abundance of debt, which lowers the marginal productivity of capital. ?Monetary policy seems to be pursuing a closed loop where little?incremental lending gets to lower quality borrowers, and a lot goes to governments.

But economies are greater than the governments that try to milk them. ?There is a growing middle class around the world, and along with that, a growing need for food, energy, and basic consumer goods. ?That is the long run, absent war, plague, resurgent socialism, etc.

To give an example of how markets can decouple from government policy, consider the corporate bond market, and lending options for consumers. ?The Fed can keep the Fed funds rate low, but aside from the strongest?borrowers, the yields that lesser borrowers?borrow at are high, and reflect the intrinsic risk of loss, not the temporary provision of cheap capital to banks and other strong borrowers.

It’s more difficult to sort through when accumulated organic demand will eventually well up and drive industries that are more economically sensitive. ?Over-indebted governments can not and will not be the driver here. ?(Maybe monetary policy like the 1970s could do it… what a thought.)

So, what to do when the economic outlook for a wide number of industries that look seemingly cheap are poor? ?My answer is buy one of the strongest names in each industry, and then focus the rest of the portfolio on industries with better current prospects that are relatively cheap.

Anyway, this is the first of a few articles on this topic. ?My next one should be on industry valuation and price momentum. ?Fasten your seatbelts and don your peril-sensitive sunglasses. ?It will be an ugly trip.

I get letters from all over the world. ?Here is a recent one:

Respected Sir,

Greetings of the day!

I read your blog religiously and have gained quite a lot of practical insights in financial field. Your book reviews are very helpful and impartial.

I request you to write blog post on dollar pegs in Middle East and under what conditions those dollar pegs would fall.

If in case you cannot write about it, kindly point me to some material which can be helpful to me.

Thanks for your valuable time.

Now occasionally, some people write me and tell me that I am outside my circle of competence. ?In this case I will admit I am at the edge of that circle. ?But maybe I can say a few useful things.

Many countries like pegging their currency to the US dollar because it provides stability for business relationships as businesses in their country trade with the US, or, with other countries that peg their US dollar, or, run a dirty peg of a controlled devaluation. ?Let me call that informal group of countries the US dollar bloc. [USDB]

The problem comes when the country trading in?the USDB begins to import a lot more than they export, and in the process, they either liquidate US dollar-denominated assets or create?US dollar-denominated liabilities in order to fund the difference.

Now, that’s not a problem for the US — we get a pseudo-free pass in exporting claims on the US dollar. ?The only potential cost is possible future inflation. But, it is a problem for other countries that try to do so, because they can’t manufacture those claims out of thin air as the US Treasury does.

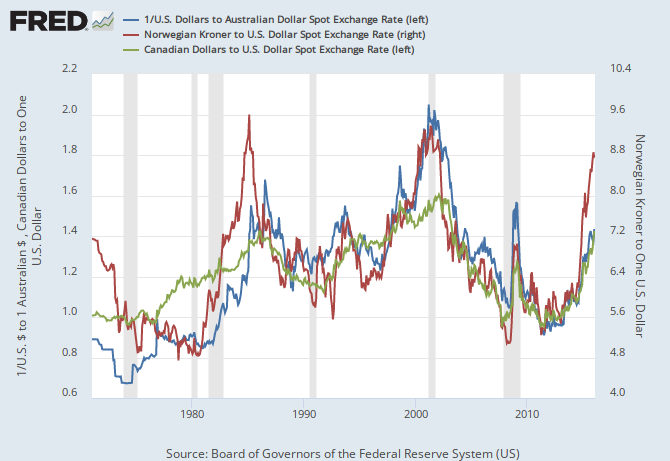

Now in the Middle East it used to be easy for many countries there because of all the crude oil they produced. ?Crude oil goes out, goods and US dollar claims come in. ?Now it is reversed, as the price of crude is so low. ?Might this have an effect on the currencies of the Middle East. ?Well, first let’s look at some currencies that float that are heavily influenced by crude oil and other commodities: Australia, Canada, and Norway:

Commodity Currencies

As oil and commodities have?traded off so have these currencies. ?That means for pegged currencies the same stress exists. ?But with a pegged currency, if adjustments happen, they are rather large violent surprises. ?Remember the old saying, “He lied like a finance minister on the eve of the devaluation,” or Monty Python, “No one expects the Spanish Inquisition!”

That’s not saying that any currency peg will break imminently. ?It will happen later for those countries with large reserves of hard currency assets, especially the dollar. ?It will happen later for those countries that don’t have to draw on those reserves so rapidly.

Thus my advice is threefold:

Watch hard currency reserve levels and project future levels.

Listen to the rating agencies as they downgrade the foreign currency sovereign credit ratings of countries. ?When the ratings get lowered and there is no sign that there will be any change in government policy, watch out.

Watch the behavior of wealthy and connected individuals. ?Are they moving their assets out of the country and into hard currency assets? ?They always do some of this, but are they doing more of it — is it accelerating?

Point 3 is an important one, and is one seemingly driving currency weakness in China at present. ?US Dollar assets may come in due to an excess of exports over imports, but they are going out as wealthy people look to preserve their wealth.

On point 2, the rating agencies are competent, but read their writeups more than the ratings. ?They do their truth-telling in the verbiage even when they delay downgrades longer than they ought to.

Point 1 is the most objective, but governments will put off adjustments as long as they can — which makes the eventual adjustment larger and more painful for those who are not connected. ?Sadly, it is the middle class and poor that get hit the worst on these things as the price of imported staple goods rise while the assets of the wealthy are protected.

And thus my basic advice is this: gradually diversify your assets into ones that will not be harmed by a devaluation. ?This is one where your government will not look out for your well-being, so you have to do it yourself.

Information received since the Federal Open Market Committee met in October suggests that economic activity has been expanding at a moderate pace.

Information received since the Federal Open Market Committee met in December suggests that labor market conditions improved further even as economic growth slowed late last year.

Shades up labor conditions.? Shades down economic growth.

Household spending and business fixed investment have been increasing at solid rates in recent months, and the housing sector has improved further; however, net exports have been soft.

Household spending and business fixed investment have been increasing at moderate rates in recent months, and the housing sector has improved further; however, net exports have been soft and inventory investment slowed.

Shades household spending down.

A range of recent labor market indicators, including ongoing job gains and declining unemployment, shows further improvement and confirms that underutilization of labor resources has diminished appreciably since early this year.

A range of recent labor market indicators, including strong job gains, points to some additional decline in underutilization of labor resources.

Shades labor employment up.

Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports.

Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports.

No change.

Market-based measures of inflation compensation remain low; some survey-based measures of longer-term inflation expectations have edged down.

Market-based measures of inflation compensation declined further; survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy.

The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will continue to expand at a moderate pace and labor market indicators will continue to strengthen.

The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will continue to strengthen.

Shifts language to reflect moving from easing to tightening.

Overall, taking into account domestic and international developments, the Committee sees the risks to the outlook for both economic activity and the labor market as balanced.

Sentence dropped.

Inflation is expected to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further.

Inflation is expected to remain low in the near term, in part because of the further declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further.

Shades inflation down in the short run due to energy prices.

The Committee continues to monitor inflation developments closely.

The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.

Says that they watch every economic indicator only for their likely impact on labor employment and inflation.

The Committee judges that there has been considerable improvement in labor market conditions this year, and it is reasonably confident that inflation will rise, over the medium term, to its 2 percent objective.

Dropped sentence.

Given the economic outlook, and recognizing the time it takes for policy actions to affect future economic outcomes, the Committee decided to raise the target range for the federal funds rate to 1/4 to 1/2 percent.

Given the economic outlook, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent.

No real change.

The stance of monetary policy remains accommodative after this increase, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

No change.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

No change.? Gives the FOMC flexibility in decision-making, because they really don?t know what matters, and whether they can truly do anything with monetary policy.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

No change.? Says that they will go slowly, and react to new data.? Big surprises, those.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Says it will keep reinvesting maturing proceeds of agency debt and MBS, which blunts any tightening.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Jeffrey M. Lacker; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Esther L. George; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo.

Changing of the guard of regional Fed Presidents, making them ever so slightly more hawkish, and having no effect on policy.

Comments

Policy stalls, as their view of the economy catches up with reality.

The changes for the FOMC is that labor indicators are stronger, and GDP weaker.

Equities fall and bonds rise. Commodity prices rise and the dollar falls.? Maybe some expected a bigger move.

The FOMC says that any future change to policy is contingent on almost everything.

The key variables on Fed Policy are capacity utilization, labor market indicators, inflation trends, and inflation expectations. As a result, the FOMC ain?t moving rates up much, absent much higher inflation, or a US Dollar crisis.

{kind=link}