There is no getting something for nothing. ?There is always a cost involved, even if it is feeling vaguely obligated to listen to the person?giving you a gift. ?We are social creatures, and we want to favor people who are kind to us.

I get a lot a pitches in the mail because I profile?well to wealth managers and those?like them. ?The age, assets, income add up to a likely client, except that I am in a related business, and am not interested in making my assets?less flexible, at least right now.

My advice to you is that you do not respond to free gifts, whether it is good food, baubles, etc. ?It’s not worth it, and if you have a need, it would be far better to draw up your own story, and send it to five wealth managers, putting them in competition with one another, so that you can compare and contrast what they do and charge.

Even in my own limited experience, going to free conferences I find that I am the product being sold, and for months thereafter I have to tell marketers that I am not interested — and to the pesky ones point out some flaw in what they do.

Your time is valuable. ?So is your money. ?Thus remember what I always say:

“Don’t buy what someone else wants to sell you. ?Buy what you have researched that you want to buy.”

Thus, make them play your game. ?Don’t play their game. ?Send out your proposal for competitive bid, and choose the one that is best for you.

Today I saw an article about a high school investing contest, and like most contests of that type, it does not teach investing, but speculation.

I’ve wanted to try this for about ten years or so. ?I’d like to try running a?stock picking contest, but only if I can offer decent prizes, and get enough participants. ?I’ve written about this before, these would be the rules:

No leverage and no shorting

No trading — buy & hold

No Exchange Traded Products, and only common stocks

Minimum market capitalization of $100 million

Only stocks traded on US exchanges

Forced diversification — a portfolio of ten stocks equally weighted

One stock from each of ten volatility buckets, to reduce speculation

Highest geometric mean return wins — this gives a bonus to consistency, which also reduces speculation. ?(Alternative rule: the best return on the?seventh best stock in each portfolio wins.)

Six month time frame.

One entry per person.

The most critical rules are seven and eight. ?The idea is to get people to think like investors, not speculators. ?By forcing investors to buy a broad range of companies from conservative to aggressive will force them to evaluate individual companies, with an eye to avoiding big losers. ?Rule number one, as many say, is don’t lose money. ?This would?honor the idea of avoiding losses while trying to make gains. ?It would be a lot like what intelligent investing in a portfolio of stocks is really like.

The idea is to promote stock-picking. ?Now lest you think I have taken all of the speculation out of this, let me tell you what my rules don’t stop:

Factor tilts — you can assemble a portfolio with price momentum

Industry and sector tilts

Foreign tilts

Size tilts

Valuation tilts

Investing in special situations

Copying famous investors

Now, Who Would Be Sponsors?

I can’t fund this on my own. ?Also, I don’t think registration fees could fund such a contest. ?Parties that could benefit from the branding and free advertising would include financial information companies and brokerages — they are some of the logical beneficiaries of promoting stock-picking. ?So, would the following consider sponsoring such a contest?

Wall Street Journal, Yahoo Finance, Bloomberg, Marketwatch, Reuters, Money, Value Line, theStreet.com, etc.

Nasdaq OMX, Intercontinental Exchange

Schwab, E-Trade, Scottrade, Interactive Brokers,?Ameritrade, Fidelity, ETrade, etc.

I don’t know, but I would want to have at least 1,000 entrants and $50,000 in prize money if were going to run a contest like this. ?I’m sure it would be a lot of fun, and would teach investors a lot about investing, as opposed to speculation.

Thoughts? ?Send them to me. ?(Especially if you are interested in sponsoring the event.)

I can’t help but think after the financial crisis that we have drawn some wrong conclusions about systemic risk. Systemic risk is when the financial system as a whole threatens to fail, such that short-term obligations can’t be paid out in full. ?It is not a situation where only big entities fail — the critical factor is whether?it creates a run on liquidity across the system as a whole.

Why does a bank fail? ?It can’t pay in full when there was a demand for liquidity in the short run. ?Typically, there is an asset-liability mismatch, with a lot of payments payable now, and assets that cannot be easily liquidated for what their stated value reported to?the regulators.

Imagine the largest bank failing, and no one else. ?Yes, it would be a mess for the FDIC to clean up, but it could be done. ? Stockholders?and?preferred stockholders get wiped out. Bondholders, junior bondholders, and large depositors take a haircut. ?Future deposit insurance premiums might have to rise, but there would be enough time to do that, with banks adjusting their prices so that they could afford it.

But banks don’t fail one at a time, except perhaps in good times with a really incompetently managed bank. ?Why do some banks tend to fail at the same time?

They own many of the same debt securities, or same types of loans where the underlying asset values are falling.

They own securities of other banks, or other deposit-taking institutions.

Generalized panic.

What can stop?a bank from failing? ?Adequate short-term cash flow from assets. ?Why don’t banks make sure that they always have more cash coming in than going out? ?That would be a lower profitability way of running a bank. ?It is almost always more profitable to borrow short and lend long, and make money on the natural term spread that exists — but that creates the very conditions that makes some banks run out of liquidity in a panic.

You will hear the banks say, “We are solvent, we just aren’t liquid.” That statement is always hogwash. ?That means that the bank did not adequately plan to have enough liquidity under all circumstances.

Thus, planning to avoid systemic risk across an economy as a whole should focus on looking for the entities that make a lot of promises where payment can be demanded in the short run with no adjustments for market conditions versus assets available to make payments. ?Typically, that means banks and things like banks that take deposits, including money market funds. ?What does it not include?

Life insurers, unless they write a lot of unusual annuities that can get called for immediate payment, as happened to General American and ARM Financial in 1999. ?The liability structure of life insurance companies is so long that there can never be a run on the bank. ?That doesn’t mean they can’t go insolvent, but it does mean they won’t be part of a systemic panic.

Property & Casualty and Health insurers do not have liabilities that can run from them. ?They can write bad business and lose money in the short-run, but that doesn’t lead to systemic panic.

Investment companies do not have liabilities that can run from them, aside from money-market funds. ?Since the liabilities are denominated in the same terms as the assets managed, there can’t be a “run on the bank.” ?Even if assets are illiquid, the rules for valuing illiquid assets for liquidation are flexible enough that an investment firm can lower the net asset value of the payouts, while liquidating other assets in the short run.

Even any large corporation that has financed itself with too much short-term debt is not a threat to systemic panic. ?The failure would be unique when it could not roll over its debts. ?Further, it would take some effort to actually do that, because the rating agencies and lenders would have to allow a non-financial firm to take obvious risks that non-financial firms don’t take.

What might it include?

Money market funds are different because of the potential to “break the buck.”

Any financial institution that relies on a?repurchase [repo] market for financing is subject to systemic risk because of the borrow short to finance a long-dated asset mismatch inherent in the market.

Watch any entity that has to be able to post additional margin in order maintain leveraged asset finance.

How then to Avoid Systemic Risk?

Regulate banks, money market funds and other depositary financials tightly.

Don’t let them invest in one another.

Make sure that they have more than enough liquid assets to meet any conceivable liquidity withdrawal scenario.

Regulate repurchase markets tightly.

Raise the amount of money that has to be deposited for margin agreements, until those are no longer a threat.

Perhaps break up banks by ending interstate branching. ?State regulation is good regulation.

But aside from that, there is nothing to do. ?There are no systemic risks from investment companies or those that manage them, because there can’t be a self-reinforcing “run on the bank.” ?Insurance companies are similar, and their solvency is regulated far better than any bank.

Thus, there shouldn’t be any lists of systematically important financial institutions that contain investment managers or insurance companies. ?Bigness is not enough to create a systemic threat. ?Even GE Capital could have failed, and it would not have had significant effects on the solvency of other financials.

I think it is incumbent on those that would?call such enterprises systemically important to show one historical example of where such enterprises ever played a significant role in a financial crisis like the ones that happened in the 1870s, 1900s, 1930s, or 2000s. ?They won’t be able to do it, and it should tell them that they are wasting effort, and should focus on the short-tailed liabilities of financial companies.

Tonight’s topic comes from a note sent to me by a friend. Here it is:

David, I have heard you say that you have entered into partnerships in the past.? What are your rules for partnerships, who will you enter with?? I have a neighbor who is interested in starting a business, the start up cash is small $5000.? I think there might be good opportunity, but I am concerned for good reason about my time availability, as well as Not being “unequally yoked”.? What business relations do Paul’s words govern.? do you have different rules for minority, majority, or controlling shares?

I appreciate your thoughts.

I have two “partnership” investments. ?One is very successful and is an S Corporation. ?The other is a limited partnership, and I wonder whether it will ever amount to anything. ?Both were done with friends.

There are a few?things that you have to think about with partnerships:

Is your liability limited to the amount of money you invested, or could you be on the hook for more if there are losses/lawsuits?

Are there likely to be future periods where capital might need to be raised? ?Under what conditions will that be done?

What non-capital obligations are you?taking on as a result of this? ?Labor, counsel, facilities, tools, etc?

How will profits and losses be allocated? ?Voting interests??How will it be managed??When will the partnership end? ?How can terms be modified? How can partnership interests be transferred, if at all? ?Etc.

Do you like the people that you will be partners with? ?You may be partners for a long time.

Be ready for the additional tax complexity of filling out schedule C, or a K-1, or some other tax form.

Go into a partnership with your eyes wide open, and check everything. ?If your partnership interests have limited liability, and the economics are structured similar to that of a corporation, then things are clearer, and you don’t have to worry as much.

Take note of any obligations that you might have that don’t fit into the “passive provider of limited capital with proportionate ownership” framework. ?Those obligations are the ones that need greater scrutiny. ?Include in that how those working on the partnership get compensated for their labor. ?Parties to the partnership may have multiple roles, and there can be conflicts of interest — imagine a partnership where one partner works in the business and receives a large salary, thus depressing profits for the non-working partners. ?How does that conflict of interest get settled? ?(Note that the same problems that exist in being an outside, passive, minority public stock investor reappear here.)

Also be aware of how ownership interests can change, and whether you may be forced to add more capital to maintain your proportionate interest in the business.

Try to have a good sense of the skill of the partner or employee managing the business. ?That makes all the difference in whether a business succeeds.

Most of what I say here assumes that you will not be a controlling majority partner, and that you will have limited influence over the business. ?If you do have control, the?problems of getting cheated by someone else go away, but get replaced with the problem of making sure the business is run adequately for the interests of all partners. ?Your ethical obligations also expand.

You mention the “unequally yoked” passage from Second Corinthians 6, verses 14 and following. ?In one sense, that doesn’t have much?more application here than it does in all investing if one is a Christian. ?Don’t involve yourself in businesses that of necessity involve you in things that you would not do yourself as a Christian. ?Don’t invest in enterprises where it is obvious that management does not care about ethics — you can see it in their behavior. ?This will be a little clearer and close to home in a partnership with a friend — you will know a lot more about what is going on.

With a non-limited partnership, there is an?additional way the “unequally yoked” passage applies. ?You expose your entire economic well-being to risk when you are a general partner. ?It is like a marriage — it is very difficult to negotiate your way out of the unlimited guarantee that you make there. ?It is like being a co-signer, which the Bible says to avoid.

Of itself, that doesn’t expose you to the unequal yoke, but when you are in an economic agreement that binding, if your partner takes the business in an ethical direction you find dubious, you will be in a weak position to do something about this. ?There is where the unequal yoke appears amid unlimited liability.

That’s all for now. ?There’s a lot more to consider here, but this is meant to be an introduction to the issues involved in partnerships. ?Hope it works well for you.

I imagine the SEC (or the Fed, IRS, or the FSOC) saying: “If we only have enough data, we can answer the policy questions that we are interested in, create better policy, prosecute bad guys, and regulate markets well.”

If they deigned to listen to an obscure quantitative analyst like me, I would tell them that it is much harder than that. ?Data is useless without context and interpretation. ?First, you have to have the right models of behavior, and understand the linkages between disparate markets. ?Neoclassical economics will not be helpful here, because we aren’t rational in the ways that the economists posit.

Second, in markets you often find that causation is a squirrelly concept, and difficult to prove statistically. ?Third, the question of right and wrong is a genuinely difficult one — what is acceptable behavior in markets? ?Do we run a market for “big boys” who understand that this is all “at your own risk,” or a market that protects the interests of smaller players at a cost to the larger players? ?Do we run a market that encourages volume, speed and efficiency, or one that avoids large movements in prices?

People take actions in the markets for a wide number of reasons. ?Some are hedging; some are investing; others are speculating. ?Some invest for long periods, and others for seconds, and every period in-between. ?Some are intermediaries, while others are direct investors. ?Some are in one market, while others are operating in many markets at once. ?Some react rapidly, and others trade little, if at all. ?Just seeing that one party bought or sold a given security tells you little about what is going on and why.

Following price momentum works as an investment strategy, until the volume of trading following momentum strategies gets too high. ?Then things go nuts. ?Actions that by themselves are innocent may add up to an event that is unexpected. ?After all, that is what dynamic hedging led to in 1987. ?There was no sinister cabal looking to drive the market down. ?And, because the event did not reflect any fundamental change to?where valuations should be, price came back over time.

My contention is even with the huge amount of data, there will still be alternative theories, information that might be material excluded, and fuzziness over whether a given investment action was wrong or not.

After that, we can ask whether the proposed actions of the government provide any significant value to the market. ?Some are offended when markets move rapidly for seemingly no reason, because they?lose money on orders placed in the market at that time. ?There is a much simpler, money saving solution to that close to home for each investor: DON’T USE MARKET ORDERS! ?Set the?price levels for your orders carefully, knowing that you could get lifted/filled at the level.

This is basic stuff that many investors counsel regarding investing. ?If you use a market order you could get a price very different than what you anticipate, as I accidentally experienced in this tale. ?I could complain, but is the government supposed to protect us from our own neglect and stupidity? ?If we wanted that, there is no guarantee that we would end up with a better system. ?After all, when the government sets rules, it does not always do them intelligently.

One of the beauties of capitalism is that it enables intelligent responses as a society to gluts and shortages without having a lot of rules to insure that. ?Volatility is not a problem in the long run for a capitalist society.

If you lose money in the short run due to market volatility, no one told you that you had to trade that day. ?Illogical market behavior, as in 1987 or the “flash crash” could be waited out with few ill effects. ?Most of the difficulties inherent in a flash crash could be solved by people taking a longer view of the markets, and thinking like businessmen.

“It’s Baseball, Mom.”

I often spend time watching two of my younger children play basketball,?baseball and softball. ?They are often in situations where they might get hurt. ?In those situations, after an accident, my wife gets antsy, while I watch to see if a rare?severe injury has happened. ?My wife asked one of my sons, “Don’t you worry about getting hurt?” ?His response was,?”It’s Baseball, Mom. ?If you don’t get hurt every now and then, you aren’t playing hard enough.” ?That didn’t put her at ease, but she understood, and accepted it.

In that same sense, I can tell you now that regardless of what the SEC does, there will be accidents, market events, and violent movements. ?There will be people that complain that they lost money due to unfair behavior. ?This is all a part of the broader “game” of the markets, which no one is required to play. ?You can take the markets on your own terms and trade rarely, and guess what — you will likely do better than most, and avoid short-term volatility.

The SEC can decide what it wants to do with its scarce resources. ?Is this the best use for the good of small investors? ?I can think of many other lower cost ways to improve things… even just hiring more attorneys to prosecute cases, because most of the true problems the SEC faces are not problems of knowledge, but problems of the will to act and bear the political fallout for doing so. ?And that — is a different game of baseball.

Let me start at the beginning. ?NAHC was an insurer with a niche presence in New Jersey. ?They competed only in personal lines, which usually is easy to analyze. ?New Jersey was a tough but not impossible state to operate in, and NAHC was a medium-sized fish for the size of the pond that they were in.

Chubb was not in NewJersey at that point in time, and so they wanted to insure autos, homes, and personal property, particularly that of wealthy people.

I thought it was an interesting company, trading slightly below tangible book, with a single-digit multiple on earnings, good protective boundaries, and a motivated management team. ?The CEO owned over 10% of the firm, which seemed to be enough to motivate, but not enough to ignore shareholders.

In 2005, we bought a 5%+ stake in the company, which in 2006 became 10%+, and eventually topped out at 17%. ?We might have bought more with the approval of the NewJersey Department of Insurance, which was easy at lower levels, and harder at higher levels, which was an interesting anti-takeover defense.

The company showed promise in many ways, but always seemed to have performance issues — little to medium surprises every few quarters. ?The stock price didn’t do that much bad or good. ?When I left Hovde at the end of July 2007, the position was at a modest gain. ?Hovde had a hard time finding long names in that era, so the performance up to that point wasn’t that bad.

If you want to see my original logic for buying the stock after I left Hovde, you can read it here.

Here was the stock price graph from May 2007 to May 2008:

My old employer Hovde owned 17%. ?I eventually owned 0.15%, at the prices you see there, at an average cost of $6.67 for me. ?I eventually sold out at an average price of around $6.10. ?(In the above graph, “Exit” was not a sale, but where I cut off the calculation.) ?This wasn’t my worst loss by any means, but it cost my former employer badly, and it was my fault, not theirs.

What Went Wrong?

Their competitive position deteriorated as companies that previously avoided New Jersey entered the state.

They announced that they had reserving errors, and reported moderate?losses as a result.

They announced a sale to Palisades Insurance, a private New Jersey insurer for $6.25/sh, valuing the company at less than 60% of tangible book value. ?The fairness opinion was a bad joke. ?The company would have been worth more in run-off.

Really, the management team was weak.

The first problem would be a tough one to solve. ?On the second problem, I never got a good answer to how the loss reserves got so cockeyed, and somehow no one was to blame for it. ?This is personal lines insurance — the reserves validate themselves every year.

But the third problem made me think the management was somewhat?dishonest. ?A larger company could have paid a higher price for NAHC, but that probably would have meant that management would lose their jobs. ?They gave shareholders the short end of the stick for the good of management, and perhaps employees.

My biggest error was giving too much credit, and too much patience to the management team. ?I met far better management teams in my time as a buy-side analyst, and they were on the low end of the competence scale. ?I let cheapness and a strong balance sheet blind me to the eroding competitiveness, and weak ability to deal with the problem.

Ultimately, Hovde found itself in a weak position because it could not file for appraisal rights, a fraud case would have been weak, and the NJ Department of Insurance would not let them acquire enough to block the deal. ?Besides, once arbs got a hold of over 40% of the shares, the deal was almost impossible to block.

As I often say, risk control is best done on the front end. ?On the back end, solutions are expensive, if they are available at all.

The front end for you can be learning from my errors. ?Wise men learn from the mistakes of others. ?Average men learn from their own mistakes. ?Dumb men never learn.

In closing, be conservative in investing, and be wise. ?I thought I was being both, so seek the counsel of others to check your logic.

Photo Credit: Ian || Watching Capital Implode is a Marvel to Behold!

This is one of the many times that I wish RealMoney.com had not changed its file structure, losing virtually all content prior to 2008. ?(It is also a reason that I am glad I started blogging. ?It’s more difficult to lose this content.) ?When I was a stock analyst at Hovde Capital Advisors, I made 2 humongous blunders. ?I wrote about them fairly extensively at RealMoney as the?situation unfolded, so if I had those posts, it would make the following article better. ?As it is, I am going to have to go from memory, because both companies are no longer in business. ?Here we go:

Scottish Re

Sustainable competitive advantage is difficult to find in insurance. ?Proprietary methods are as good as the employees creating and using them, and they can leave when they would like to. ?This applies to underwriting,?investing, and expense management. ?What else is there in an insurance company? ?There are back end processes of valuation?and?cash flow management, but those financial reporting processes serve to inform the front end of how an insurer operates.

One area that had and continues to have sustainable competitive advantage is life reinsurance. ?An global oligopoly of companies grew organically and through acquisitions to become dominant in life reinsurance. ?Their knowledge and mortality databases make them far more knowledgeable the life insurers that seek to pass some of the risk of the death of their policyholders to them. ?They can be very profitable and stable. ?I already owned shares of RGA for Hovde, and in 2005 wanted to expand the position by buying some of the cheaper and more junior company Scottish Re.

Scottish Re had only been in business since 1998, versus?RGA since 1973. ?These were the only pure play life reinsurers in the world. ?Scottish Re had grown organically and through acquisition to become the #5 member of the oligopoly. ?The top 5 life reinsurers controlled 80% of the global market. ?I made the case to the team at Hovde, and we took a medium-sized position.

The first thing I should have noticed was the high level of complexity of the holding company structure. ?Unlike RGA, they operated to a high degree?in a wide number of offshore tax and insurance haven domiciles — notably Bermuda, Ireland, Cayman Islands, and others. ?Second, their ownership diagrams rivaled AIG for complexity, and their market capitalization was less than 2% of AIG’s at the time. ?[Note: balance sheet complexity did not bode well for AIG either — down 98% since then, but it beats Scottish Re going out at zero.]

The second thing I should have noticed was the high degree of underwriting leverage. ?Relative to RGA, it reinsured much more life risk relative to the size of its balance sheet.

The third thing I should have noticed was the cleverness of some of the financing methods of Scottish Re — securitization was uncommon in life reinsurance, and they were doing it successfully.

The final thing that I should have noticed was that earnings quality was poor. ?They usually made their earnings, but often because their tax rate was so low… and the deferred tax assets were a large part of book value. ?(Note: deferred tax assets only have value if you are going to have pretax income in the future. ?That was soon not to be.)

In 2005, Scottish Re won the auction for buying up another member of the oligopoly, ING Life Re. ?I asked the CFO of RGA why they didn’t buy it, and his comment was that he didn’t think anyone would pay more than they bid. ?That should have led me to sell, but I didn’t. ?The price of Scottish Re drifted down, until August 3, 2006, when they announced second quarter earnings, reporting a huge loss, writing off a large portion of their deferred tax assets, and the stock price dropped 75% in one day. ?I eventually wrote about that at RealMoney, noting it was the single worst day in the hedge funds history, and it was due to my errors. ?You can also read my questions/comments from the conference call here?(pages 50-53).

If you look at the RealMoney article, you might note that we tripled our position at around $6.90?after the disaster. ?That took a lot of guts, and we didn’t know it then, but it was the wrong thing to do. ?The stock rallied all the way up to $10 or so. ?If it hit $11, we were going to sell out. ? That was not to be.

I spent hours and hours going through obscure insurance filings. ?I analyzed every document that I could get my hands on including?the rating agency analyses, because they had access to inside data in aggregate that no one else had outside of the company. ?The one consistent thing that I learned was that insolvency was unlikely — which would later prove wrong.

The stock price fell and fell all the way down to $3, with rumors of insolvency swirling, when Mass Mutual and Cerberus rode to the rescue on November 27, 2006, buying 69% of the company for a paltry $600 million in convertible preferred stock. ?At that point, I finally got it right. ?All of my prior research had some value, because when I read through the documents that day and saw the liquidity raised relative to the amount of ownership handed over. ?Given the data that they now handed out, I concluded that Scottish Re was worth $1/share, and possibly zero.

But there was a relief rally that day, and we sold into it. ?We ended up selling about 4% of the total market cap of Scottish Re that day at a price of $6.25.

The bright side of the whole matter was that we could have lost a lot more. ?Scottish Re was eventually worth zero, and?Mass Mutual and Cerberus took significant losses, as did the remaining shareholders.

As it was, the fault was all mine — my colleagues at Hovde deserved none of the blame.

The Lesson Learned

One year later, I wrote a note to the late Greg Newton who wrote the notable blog, Naked Shorts, when he was critical of Cerberus (they had a lot of failures in that era). ?This was the summary that I gave him on Scottish Re:

Cerberus got into SCT @ $3; it’s now around $2.? For me, on the bright side, when their deal with SCT was announced, I quickly went through the data, and recommended selling.? We got out @ $6.25.? That limited our losses, but it was still my biggest failure when I was at Hovde.? The mixture of leverage, alien domiciled subsidiaries, reinsurance underwriting leverage, plus complex and novel securitization structures was pure poison.? I was?mesmerized?by the?seemingly cheap valuation and actuarial studies that indicated that mortality experience was a little better than expected. ?I?violated my leverage and simplicity rules on that one.

He gave me a very kind response, better than I deserved. ?As it was Scottish Re went dark, delisting in May 2008, and trading for about a nickel per share at the last 10K?in July of 2008. ?It eventually went to zero.

The biggest lesson is to do the research better on illiquid and opaque financial companies, or, avoid them entirely. ?Complexity and leverage there are typically not rewarded. ?I’d like to say that I fully learned my lesson there, but I got whacked again by the same lesson on a personal investment later in 2008. ?That’s a subject for a later article.

I have one more bad equity investment from my hedge fund days, and I will write about that sometime soon, to end this part of the series.

Full disclosure: still long RGA for my clients and me

This will be the post where I cover the biggest mistakes that I made as an institutional bond and stock investor. In general, in my career, my results were very good for those who employed me as a manager or analyst of investments, but I had three significant blunders over a fifteen-year period that cost my employers and their clients a lot of money. ?Put on your peril-sensitive sunglasses, and let’s take a learning expedition through my failures.

Manufactured Housing Asset Back Securities — Mezzanine and Subordinated Certificates

In 2001, I lost my boss. ?In the midst of a merger, he?figured his opportunities in the merged firm were poor, and so he jumped to another firm. ?In the process, I temporarily became the Chief Investment Officer, and felt that we could take some chances that the boss would not take that in my opinion were safe propositions. ?All of them worked out well, except for one: The?– Mezzanine and Subordinated Certificates of?Manufactured Housing Asset Back Securities [MHABS]. ?What were those beasts?

Many people in the lower middle class live in prefabricated housing in predominantly in trailer parks around the US. ?You get a type of inexpensive independent living that is lower density than an apartment building, and?the rent you have to pay is lower than renting an apartment. ?What costs some money is paying for the loan to buy the prefabricated housing.

Those loans would get gathered into bunches, put into a securitization trust, and certificates would get sold allocating cash flows with different probabilities of default. ?Essentially there were four levels (in order of increasing riskiness) — Senior, Mezzanine, Subordinated, and Residual. ?I focused on the middle two classes because they seemed to offer a very favorable risk/reward trade-off if you selected carefully.

In 2001, it was obvious that there was too much competition for lending to borrowers in Manufactured Housing [MH] — too many manufacturers were trying to sell their product to a saturated market, and underwriting suffered. ?But, if you looked at older deals, lending standards were a lot higher, but the yields on those bonds were similar to those on the badly underwritten newer deals. ?That was the key insight.

One day, I was able to confirm that insight by talking with my rep at Lehman Brothers. ?I talked to him about the idea, and he said, “Did you know we have a database on the loss stats of all of the Green Tree (the earliest lender on MH) deals since inception?” ?After the conversation was over, I had that database, and after one day of analysis — the analysis was clear: underwriting standards had slipped dramatically in 1998, and much further in 1999 and following.

That said, the losses by deal and duration since issuance followed a very predictable pattern: a slow ramp-up of losses over 30 months, and then losses tailing off gradually after about 60 months. ?The loss statistics of all other MH lenders aside from Vanderbilt (now owned by Berkshire Hathaway) was worse than Green Tree losses. ?The investment idea was as follows:

Buy AA-rated mezzanine and BBB-rated subordinated MHABS originated by Green Tree in 1997 and before that. ?The yield spreads over Treasuries are compelling for the rating, and the loss rates would have to jump and stick by a factor of three to impair the subordinated bonds, and by a factor of six to impair the mezzanine bonds. ?These bonds have at least four years of seasoning, so the loss rates are very predictable, and are very unlikely to spike by that much.

That was the thesis, and I began quietly acquiring $200 million of these bonds in the last half of 2001. ?I did it for several reasons:

The yields were compelling.

The company that I was investing for was growing way too rapidly, and we needed places to put money.

The cash flow profile of?these securities matched very well the annuities that the company was selling.

The amount of capital needed to carry the position was small.

By the end of 2001, two things happened. ?The opportunity dried up, because I had acquired enough of the bonds on the secondary market to make a difference, and prices rose. ?Second, I was made the corporate bond manager, and another member of our team took over the trade. ?He didn’t much like the trade, and I told my boss that it was his portfolio now, he can do what he wanted.

He kept the positions on, but did not add to them. ?I was told he looked at the bonds, noticed that they were all trading at gains, and stuck with the positions.

Can You Make It Through the Valley of the Shadow of Death?

I left the firm about 14 months later, and around?that time, the prices for MHABS fell apart. ?Increasing defaults on MH loans, and failures of companies that made MH, made many people exceptionally bearish and led rating agencies to downgrade almost all MHABS bonds.

The effects of the losses were similar to that of the Housing Bubble in 2007-9. ?As people defaulted, the value of existing prefabricated houses fell, because of the glut of unsold houses, both new and used. ?This had an effect, even on older deals, and temporarily, loss rates spiked above the levels that would impair the bonds that I bought if the levels stayed that high.

With the ratings lowered, more capital had to be put up against the positions, which the insurance company did not want to do, because they always levered themselves up more highly than most companies — they never had capital to spare, so any loss on bonds was a disaster to them.

They feared the worst, and sold the bonds at a considerable loss, and blamed me.

[sigh]

Easy to demonize the one that is gone, and forget the good that he did, and that others had charge of it during the critical period. ?So what happened to the MHABS bonds that I bought?

Every single one of those bonds paid off in full. ?Held to maturity, not one of them lost a dime.

What was my error?

Part of being a good investor is knowing your client. ?In my case, the client was an impossible one, demanding high yields, low capital employed, and no losses. ?I should have realized that at some later date, under a horrific scenario, that the client would not be capable of holding onto the securities. ?For that reason, I should have never bought them in the first place. ?Then again, I should have never bought anything with any risk for them under those conditions, because in a large enough portfolio, you will have some areas where the risk will surprise you. ?This was less than 2% of the consolidated assets of the firm, and they can’t hold onto securities that would likely be money good amid a panic?!

Sadly, no. ?As their corporate bond manager, before I left, I sold down positions like that that my replacement might not understand, but I did not control the MHABS portfolio then, and so I could?not do that.

Maybe $50 million went down the drain here. ?On the bright side, it helped teach me what would happen in the housing bubble, and my next employer benefited from those insights.

Thus the lesson is: only choose investments that your client will be capable of holding even during horrible times, because the worst losses come from panic selling.

Next time, my two worst stock losses from my hedge fund days.

Information received since the Federal Open Market Committee met in January suggests that economic growth has moderated somewhat.

Information received since the Federal Open Market Committee met in March suggests that economic growth slowed during the winter months, in part reflecting transitory factors.

Shades GDP down. ?Why can?t the FOMC accept that the economy is structurally weak?

Labor market conditions have improved further, with strong job gains and a lower unemployment rate. A range of labor market indicators suggests that underutilization of labor resources continues to diminish.

The pace of job gains moderated, and the unemployment rate remained steady. A range of labor market indicators suggests that underutilization of labor resources was little changed.

Shades labor use down.

Household spending is rising moderately; declines in energy prices have boosted household purchasing power. Business fixed investment is advancing, while the recovery in the housing sector remains slow and export growth has weakened.

Growth in household spending declined; households’ real incomes rose strongly, partly reflecting earlier declines in energy prices, and consumer sentiment remains high. Business fixed investment softened, the recovery in the housing sector remained slow, and exports declined.

Shades down their view of household spending.? Adds a comment on consumer sentiment.

Also shades down business fixed investment and exports.

Inflation has declined further below the Committee’s longer-run objective, largely reflecting declines in energy prices. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations have remained stable.

Inflation continued to run below the Committee’s longer-run objective, partly reflecting earlier declines in energy prices and decreasing prices of non-energy imports. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy.

The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate.

Although growth in output and employment slowed during the first quarter, the Committee continues to expect that, with appropriate policy accommodation, economic activity will expand at a moderate pace, with labor market indicators continuing to move toward levels the Committee judges consistent with its dual mandate.

No real change. They are fitting Einstein?s definition of insanity ? doing the same thing, and expecting a different outcome.

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of energy price declines and other factors dissipate. The Committee continues to monitor inflation developments closely.

The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced. Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

No change.

Consistent with its previous statement, the Committee judges that an increase in the target range for the federal funds rate remains unlikely at the April FOMC meeting.

Deleted

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term.

No change.

No rules, just guesswork from academics and bureaucrats with bad theories on economics.

This change in the forward guidance does not indicate that the Committee has decided on the timing of the initial increase in the target range.

Deleted

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

No change.? Changing that would be a cheap way to effect a tightening.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

?Balanced? means they don?t know what they will do, and want flexibility.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Jeffrey M. Lacker; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Jeffrey M. Lacker; Dennis P. Lockhart; Jerome H. Powell; Daniel K. Tarullo; and John C. Williams.

No change, sadly.

We need some people in the Fed and in the government who realize that balance sheets matter ? for households, corporations, governments, and central banks.? Remove anyone who is a neoclassical economist ? they missed the last crisis; they will miss the next one.

Comments

With this FOMC statement, people should conclude that they have no idea of when the FOMC will tighten policy, if ever. This is the sort of statement they issue when things are ?steady as you go.?? There is no hint of imminent policy change.

The FOMC has a weaker view of GDP, labor use, household spending, business fixed investment and exports.

Despite lower unemployment levels, labor market conditions are still pretty punk. Much of the unemployment rate improvement comes more from discouraged workers, and part-time workers.? Wage growth is weak also.

Forward inflation expectations have reversed direction and are rising, and the twitchy FOMC did not note it.

Equities rise and long bonds rise. Commodity prices fall and the dollar rises.? The FOMC says that any future change to policy is contingent on almost everything.

Don?t know they keep an optimistic view of GDP growth, especially amid falling monetary velocity.

The key variables on Fed Policy are capacity utilization, labor market indicators, inflation trends, and inflation expectations. As a result, the FOMC ain?t moving rates up, absent improvement in labor market indicators, much higher inflation, or a US Dollar crisis.

We have a congress of doves for 2015 on the FOMC. Things will be boring as far as dissents go.? We need some people in the Fed and in the government who realize that balance sheets matter ? for households, corporations, governments, and central banks.? Remove anyone who is a neoclassical economist ? they missed the last crisis; they will miss the next one.

Saving unicorns from themselves? There was an interesting piece last week from Martin Peers in The Information?(sub req), arguing that the private markets need some sort of shorting mechanism so that there is a check on unreasonable valuation inflation. It would make the market more efficient, Peers argues, even though implementation would require several structural changes (particularly to stock transfer rules). He writes:

“Private companies will probably resist the development of a short-selling market, given it would hurt valuations, which in turn can undermine the value of employee option programs, and give them less control over their shareholder group. But those risks are likely to be outweighed by the long term benefits of bringing more buyers into the market and ensuring the company’s valuation can be sustained outside of the constraints of the private market.”

Leaving out the technical difficulties — including?the lack of ongoing price discovery — one big counter could be that shorts didn’t so much to stop the earlier dotcom bubble (which largely took place in the public markets).

Adam D’Augelli of True Ventures pointed me to a 2002 academic paper (Princeton/London Biz School) that found “hedge funds during the time of the technology bubble on the Nasdaq… were heavily tilted towards overpriced technology stocks.” They add that “arbitrageurs are concerned about attacking the bubble too early without support from their peers,” and that they’re more likely to ride the bubble until just a few months before the end.

That would seem to be?too late to impose price discipline in private markets, but I’m curious in your thoughts. Does some sort of private shorting system make sense? And, if so, how would it be structured?

I’m going to take a stab at answering the final questions. ?There is often a reason why the financial world is set up the way it is, and why truly helpful financial innovations are rare. ?The answer is “no, we should not have any way of shorting private companies, and it is not a flaw in the system that we don’t have any easy way to do it.”

Two notes before I start: 1) I haven’t read the paper at The Information, because it is behind a paywall, but I don’t think I need to do so. ?I think the answer is obvious. ?2) I ran into this question answered at Quora. ?The answers are pretty good in aggregate, but what exists here are my own thoughts to present the answer in what I hope is a simple manner.

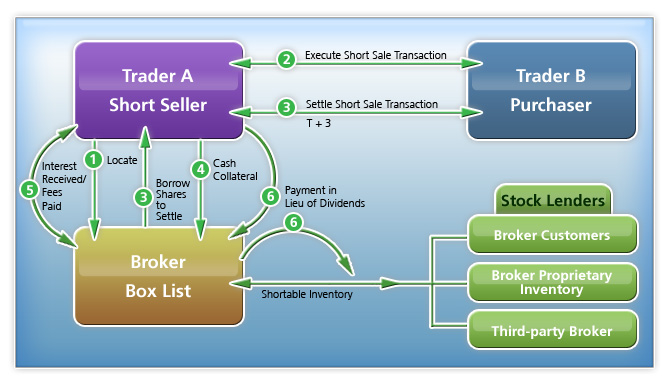

What is required to have an effective means of shorting assets

An asset must be capable of being easily transferred from one entity to another.

Entities willing to lend the asset in exchange for some compensation over a given lending term.

Entities willing to borrow the asset, put up collateral adequate to secure the asset, and then sell the asset to another entity.

An entity or entities to oversee the transaction, provide custody of the collateral, transmit payments, assure return of the asset at the end of the lending term, and gauge the adequacy of collateral relative to the value of the asset.

I’m leaving aside the concept of naked shorting, because there are a lot of bad implications to allowing a third party to create ownership interests in a firm, a power which is reserved for?the firm itself.

The Troubles Associated with Shorting Private Assets

I can think of four?troubles. ?Here they are:

The ability to sell, lend, or buy shares in a private company are limited by the private company.

Lending over long terms with no continuous?price mechanism to aid in the gradual adjustment of collateral could lead to losses for the lender if the borrower can’t put up additional capital.

The asset lender can decide only to lend over lending?terms that will likely be disadvantageous to the borrower. ?Getting the asset returned at the end of the lending term could be problematic.

It is difficult enough shorting relatively illiquid publicly traded assets. ?Liquidity is required for any regular?shorting to happen.

The first one is the killer. ?There are no advantages to a private company to allow for the?mechanisms needed to allow for shorting. That is one of the advantages of being private. ?Information is not shared openly, and you can use the secrecy to aid your competitive edge. ?Skeptical short-sellers would not be welcome.

The second problem is tough, because sometimes?successive capital rounds are at considerably higher prices. ?The borrower will likely not have enough slack assets to increase his collateral, and he will be forced to buy shares in the round to cover his short because of that. ?The lender could find that the borrower cannot make good on the loan, and so the lender loses a portion of the value his ownership stake.

But imagining the first two problems away, problem three would still be significant. ?If the term for lending were not all the way to the IPO, next capital round or dissolution/sale, at the end of the term, the borrower would have to look for someone to sell shares to him. ?It is quite possible that no one would sell them at any reasonable price. ?They know they have a forced buyer on their hands, and there could be informal collusion on the price of a sale.

Perhaps another way to put it is don’t play in a game where the other team has significant control over the rules of the game. ?One of the reasons I say this is from my days of a bond manager. ?There were a lot of games played in securities lending, and bonds?are?not the most liquid place to short assets. ?I remember it being very difficult to get a bond back from an entity that borrowed it, and the custodian and trustee did not help much. ?I also remember how we used to gauge the liquidity of bonds we lent out, and if one was particularly illiquid, we would always recall the bond before selling it, which would often make the price of the bond rise. ?Games, games, games…

What Might Be Better

Perhaps using collateralized options or another type of derivative could allow bets to be taken, if the term extended all the way to the IPO, the next capital round, or dissolution/sale of the company. ?The options would have to be limited to the posted collateral being the most the seller of the option could lose. ?Some of the above four issues would still be in play at various points, but aside from issue one, this would minimize the troubles.

What Might Be Better Still

The value of the shorts is that they share information with the rest of the market that there is a bearish opinion on an asset. ?Short-sellers are nice to have around, but not necessary for the asset pricing function. ?It is not unreasonable to live with the problem that some assets will be overvalued in the intermediate-term, rather than set up a complex method to try to enable shorting. ?As Ben Graham said:

?In the short run, the market is a voting machine but in the long run, it is a weighing machine.?

The weighing machine will do its job soon enough, showing that the overvalued asset will never produce free cash adequate to justify its current high price. ?Is it a trouble?to wait for that to happen? ?If you don’t own it, you shouldn’t care much.

If you want to short it, I’m not sure that will hasten the price adjustment process that much, unless you can convince the existing owners of the asset that it isn’t worth even the current price. ?Given that buyers have convinced themselves to own the asset, because they think it will be worth more in the future, intellectually, convincing them that it is worth less?is a tough sell.

In the end, only asset and liability cash flows count, regardless of what secondary buyers and sellers do. ?Secondary trading does not affect the value of assets, though it may affect the perception of value in the short run. ?Thus, you don’t need short sellers to aid in setting secondary market prices, but they are an aid there. ?In the primary markets, where whole companies are bought and sold, the perceived cash return is all that matters.

Conclusion

Ergo, live with short run overvaluation in private markets. ?It is a high quality problem. ?Sell overvalued assets?if you own them. ?Watch if you don’t own them. ?Shorting, even if possible, is not worth the bother.

{kind=link}