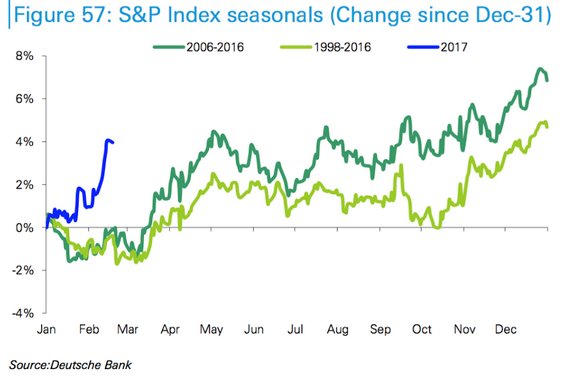

The S&P 500 move this year is completely outside the historical seasonal trends.

Graph Credit: Deutsche Bank via @SoberLook at The Wall Street Journal

Averages reveal, but they also conceal. ?When I look at a graph like this, I know that any given year is highly likely to look different than an average of years. ?So, no surprise that the returns on the S&P 500 are different than the averages of the prior 11 or 19 years.

But how has the S&P 500 fared versus the last 68 years? ?At present this year is 20th out of 68, which is good, but not great or average. ?But look at the graph at the top of this article: up until the close of the 25th trading day of the year (February 7th) the market had performance very much like a median year. ?All of the higher performance has come out of the last nine days. ?(For fun, it is the ninth best out of 68 for that time of year; even that is not top decile.)

I can tell you something easy: you can have a lot of different occurrences over nine days in the market. ?The distribution of returns would be quite wide. ?Therefore, don’t get too excited about the returns so far this year — they aren’t that abnormal. ?You can be concerned as you like about valuation levels — they are high. ?But 2017 at present is a “high side of normal” year compared to past price performance.

And, if you want to be concerned about a melt-up, it is this kind of low positive momentum that tends to persist, at least for a while. ?Trading behavior isn’t nuts, even if valuations are somewhat steamy.

I’m around 83% invested in equity accounts, so I am conservative, but I’m not thinking of hedging yet. ?Let the rally run.

I am a fiduciary in my work that I do for my clients. I am also the largest investor in my own strategies, promising to keep a minimum of 80% of my liquid net worth in my strategies, and 50% of my total net worth in them (including my house, etc.).

I believe in eating my own cooking. ?I also believe in treating my clients well. ?I’ve treated part of this in an earlier post called?It?s Their Money, where I describe how I try to give exiting clients a pleasant time on the way out. ?For existing clients, I will also help them with situations where others are managing the money at no charge, no payment from another party, and no request that I manage any of those assets. ?I do that because I want them to be treated well by me, and I know that getting good advice is hard. ?As I wrote in a prior article?The Problem of Small Accounts:

We all want financial advice.? Good advice.? And we want it for free.? That?s why we come to the Aleph Blog, where advice is regularly dispensed, and at no cost.

But? I can?t be personal, and give you advice that is tailored to your situation.? And in my writing here, much as I try to be highly honest, I am not acting as a fiduciary, even though I still make my writings hold to such a standard.

Ugh.? Here?s the problem.? Good advice costs money.? Really good advice costs a lot of money, and is worth it, if you have enough money to spread the cost over.

But when you have a small account, you have a problem in getting advice.? There is no way for someone who is fiduciary (like me) to make money addressing your concerns.? That is why I have a high minimum for investing: $100,000.? With that, I can spend time on clients, even helping them with assets from which I make no money.

What extra things have I done for clients over time? ?I have:

Analyzed asset allocations.

Analyzed the performance of other managers.

Advised on changing jobs, negotiating salary, etc.

Explained the good and bad points of certain insurance companies and their policies, and suggested alternatives.

Analyzed chunky assets that they own elsewhere, aiding them in whether they keep, sell, or sell part of the asset.

Analyzed a variety of funky and normal investment strategies.

Advised on buying a building, and future business plans.

Told a client he was better off reinvesting the slack funds in his business that needed?financing, rather than borrow and invest the funds with me.

Told a client to stop sending me money, and pay down his mortgage. ?(He has since resumed sending money, but he is now debt-free.)

I take the fiduciary side of this seriously, and will?tell clients that want to put a?lot of their money in my stock?strategy that they need less risk, and should put funds in my bond strategy, where I earn less.

I’ve got a lot already. ?I don’t need to feather my nest at the expense of the best interests of my clients.

Over the last six years, around half of my clients have availed themselves of this help. ?If you’ve read Aleph Blog for awhile, you know that I have analyzed a wide number of things. ?Helping my clients also sharpens me for understanding the market as a whole, because issues come into focus when the situation of a family makes them concrete.

So informally, I am more than an “investments only” RIA [Registered Investment Advisor], but I only earn money off of my investment fees, and no other way. ?Personally, I think that other “investments only” RIAs would mutually benefit their clients if they did this as well — it would help them understand the struggles that they go through, and inform their view of the economy.

Thus I say to my competitors: do you want to justify your fees? ?This is a way to do it; perhaps you should consider it.

Postscript

Having some people in an “investment only” shop that understand the basic questions that most clients face also has some crossover advantages when it comes to understanding financial companies, and different places that institutional money gets managed. ?It gives you a better idea of the investment ecosystem that you live and work in.

In general, I don’t like books on personnel management. ?That’s mostly because good management techniques are mostly obvious, and there are typically a lot of good strategies that are somewhat different, and most of them will work, if applied with a little common sense. ?Pick one. ?Apply it. ?Be consistent. ?Get feedback. ?Adjust. ?Repeat.

No one has the “holy grail.” ?That is true of this book also. ?What I appreciate about “The Difference” is its emphasis on creating a good culture. ?I’ve worked in companies with good cultures, bad cultures and mixed cultures. ?What?Subir?Chowdhury gets right is the key difference is attitude, and it flows from the top.

Some?firms fail because employees are afraid to tell the truth. ?That was true within areas of AIG when I worked for it. ?Do you want?a culture based on truth? ?Be honest, ask for it from your bosses, and expect it from your subordinates. ?Don’t punish anyone for telling the truth; instead reward it.

Some firms fail because of a lack of emphasis on quality. ?The need for short-term profits outweighs quality products and services. ?Low quality is a cancer — it can spread from employee relationships to products, services, accounting, vendor relations, marketing, etc. ?Cultural change is needed, starting at the top. ?If management doesn’t put quality ahead of short term profits, quality will not characterize a company. ?Management has to lead efforts on quality by example, instructions, and rewards. ?Employees won’t care about quality if management doesn’t care about them, and reward them for stopping bad quality even if it slows production.

The book takes an approach like this, only much better than I can. ?It provides a cutesy acronym to summarize the approach for creating a great corporate culture, which to me trivializes ideas, but aids memory for others.

The author peppers the book with his experiences in his life ?and work, from youth to the present. ?I found those to be a mixed bag. ?Like most people, a lot of it sounds like he is tooting his own horn repeatedly. ?Many of them are quite instructive, a few aren’t. ?I particularly found his example of giving to beggars to be weak. ?Yes, the poorest need money, but what they need more is relationships. ?The poorest lose relationships due to disease, accidents, substance abuse, selfishness on the part of their family and their own selfishness, an attitude of blaming the world around rather than look at their own failures, and more.

Giving them money does not break the problem; it often feeds the problem. ?Creating relationships for them can allow them to reboot their lives, if they want to live a new life. ?Don’t get me wrong; I’m no great shakes here. ?I just know that the poorest need radical personal change if they ever want to escape their poverty. ?Money won’t make the difference necessary most of the time.

That last rant aside, I liked the book and would recommend it. ?It’s kind of expensive for its size, but maybe you want a short book that you can read in 1-2 hours. ?You’ll get enough to make you think, and maybe make a difference. ?It’s “good enough” to help you, but not outstanding.

Quibbles

Already mentioned.

Summary / Who Would Benefit from this Book

You may not need another management book. ?If you need something short to motivate a need for corporate and personal change, this could be the book for you.? If you want to buy it, you can buy it here: The Difference: When Good Enough Isn’t Enough.

Full disclosure:?The publisher asked me if I wanted a free copy and I assented.

If you enter Amazon through my site, and you buy anything, including books, I get a small commission. This is my main source of blog revenue. I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip. Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book. Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website. Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites. Whether you buy at Amazon directly or enter via my site, your prices don?t change.

What if your time horizon was 60 years? Would a 5% real return be achievable?

I am answering this as part of an irregular “think deeper” series on the problems of modeling investment over the very long term… the last entry was roughly six years ago. ?It’s a good series of five articles, and this is number six.

On to the question. ?The model forecasts over a ten-year period, and after that returns return to the long run average — about 9.5%/year nominal. ?The naive answer would then be something like this: the model says over a 60-year period you should earn about 8.85%/year, considering that the first ten years, you should earn around 5.63%/year. ?(Nominally, your initial investment will grow to be 161x+ as large.) ? If you think this, you can earn a 5% real return if inflation over the 60 years averages 3.85%/year or less. ?(Multiplying your capital in real terms by 18x+.)

Simple, right?

Now for the problems with this. ?Let’s start with the limits of math. ?No, I’m not going to teach you precalculus, though I have done that for a number of my kids. ?What I am saying is that math reveals, but it also conceals. ?In this case the math assumes that there is only one variable that affects returns for ten years — the proportion of investor asset held in stocks. ?The result basically says that over a ten-year period, mean reversion will happen. ?The proportion of investor asset held in stocks will return to an average level, and returns similar to the historical average will come?thereafter.

Implicitly, this assumes that the return series underlying the regression is the perfectly normal return series, and the future will be just like it, only more so. ?Let me tell you about some special things involved in the history of the last 71 years:

We have not lost a war on our home soil.

We have not had socialism to the destructive levels experienced by China under Mao, the USSR. North Korea, Cuba, etc. ?(Ordinary socialism isn’t so damaging, though there are ethical reasons for not going that way. ?People deserve freedom, not guarantees. ?Note that stock returns in moderate socialist countries have been roughly as high as those in the US. ?See the book Triumph of the Optimists.)

We have continued to have enough children, and they have become moderately productive workers. ?Also, we have welcomed a lot of hard working and creative people to the US.

Technology has continued to improve, and along with it, labor productivity.

Adequate energy to multiply force and distribute knowledge is inexpensively available.

We have not experienced hyperinflation.

There are probably a few things that I have missed. ?This is what I mean when I say the math conceals. ?Every mathematical calculation abstracts quantity away from every other attribute, and considers it to be the only one worth analyzing. ?Qualitative analysis is tougher and more necessary than quantitative analysis — we need it to give meaning to mathematical analyses. ?(What are the limits? ?What is it good for? ?How can I use it? ?How can I use it ethically?)

If you’ve read me long enough, you know that I view economies and financial markets as ecosystems. ?Ecosystems are stable within limits. ?Ecosystems also can only develop so quickly; there may be no limits to growth, but there are limits to the speed of growth in mature economies and financial systems.

Thus the question: will these excellent conditions continue? ?My belief is that mankind never truly changes, and that history teaches us that all governments and most cultures eventually die. ?When they do, most or all economic arrangements tend to break, especially complex ones like financial markets.

But here are three more limits, and they are more local:

Can you really hold for 60 years, reinvesting and never taking a material amount?out?

Will the number investing in the equity markets remain small?

Will stock be offered and retired at ordinary prices?

Most people can’t lock money away for that long without touching it to some degree. ?Some of the assets?may get liquidated because of panic, personal emergency needs, etc. ?Besides, why be a miser? ?Warren Buffett, one of the greatest compounders of all time, might have ended up happier if he had spent less time compounding, and more time on his family. ?It would have been better to take a small?part of it, and use it to make others happy then, and not wait to be the one of the most famous philanthropists of the 21st century before touching it.

Second, returns may be smaller in the future because more pursue them. ?One reason?the rewards for being a capitalist are large on average is that?there are relatively few of them. ?Also, I have sometimes wondered if stock returns will fall when the whole world is employed, and there is no more cheap labor to be had. ?Should that bold scenario ever come to pass, labor would have more bargaining power in aggregate, and profits would likely fall.

Finally, you have to recognize that the equity return statistics are somewhat overstated. ?I’m not sure how much, but I think it is enough to reduce returns by 1%+. ?Equity tends to be offered for initial purchase expensively, and tends to get retired inexpensively. ?Businessmen are rational and tend to go public when stock valuations are high, pay employees in stock when valuations are high, and do stock deals when valuations are high. ?They tend to go private when stock valuations are low, pay employees cash in ordinary times, and do cash?deals when valuations are low.

As a result, though someone that buys and holds the stock index does best, less money is in the index when stocks are low, and a lot more when stocks are high.

Inflation Over 60 Years?

I mentioned the risk of hyperinflation above, but who can tell what inflation will do over 60 years? ?If the market survives, I feel confident that stocks would outperform inflation — but how much is the open question. ?We haven’t paid the price for loose monetary policy yet. ?A 1% rise in inflation tends to cut stock returns by 2% for a year in real terms, but then businesses adjust and pass through higher prices. ?Vice-versa when inflation falls.

Right now the 30-year forecast for inflation is around 2.1%/year, but that has bounced around considerably even within a calm environment. ?My estimate of inflation over a 60-year period would be the weakest element of this analysis; you can’t tell what the politicians and central bankers will do, and they aren’t sure themselves.

Summary

Yes, you could earn 5% real returns on your money over a 60-year period… potentially. ?It would take hard work, discipline, cleverness, frugality, and a cast iron stomach for risk. ?You would need to be one of the few doing it. ?It would also require the continued prosperity of the US and global economies. ?We don’t prosper in a vacuum.

Thus in closing I will tell you that yes, you could do it, but there is a large probability of failure. ?Don’t count on buying that grand villa on the Adriatic Sea in your eighties, should you have the strength to enjoy it.

I recently received two sets of questions from readers. Here we go:

David,

I am a one-time financial professional now running a modest ?home office? operation in the GHI?area.? I have been reading your blog posts for a couple years now, and genuinely appreciate your efforts to bring accessible, thoughtful, and modestly stated insights to a space too often lacking all three characteristics.? If I didn?t enjoy your financial posts so much, I?d request that you bring your approach to the political arena ? but that?s a different discussion altogether?

I am writing today with two questions about your work on the elegant market valuation approach you?ve credited to @Jesse_Livermore.?? I apologize in advance for any naivety evidenced by my lack of statistical background?

I noticed that you constructed a ?homemade? total return index ? perhaps to get you data back to the 1950s.? Do you see any issue using SPXTR index (I see data back to 1986)?? The 10yr return r-squared appears to be above .91 vs. investor allocation variable since that date.

The most current Fed/FRED data is from Q32016.? It appears that the Q42016 data will be released early March (including perhaps ?re-available? data sets for each of required components http://research.stlouisfed.org/fred2/graph/?g=qis ).? While I appreciate that the metric is not necessarily intended as a short-term market timing device, I am curious whether you have any interim device(s) you use to estimate data ? especially as the latest data approaches 6 months in age & the market has moved significantly?

I appreciate your thoughts & especially your continued posts?

JJJ

These questions are about the Estimating Future Stock Returns posts. ?On question 1, I am pulling the data from Shiller’s data. ?I don’t have a better data feed, but that should be the S&P 500 data, or pretty near it. ?It goes all the way back to the start of the Z.1 series, and I would rather keep things consistent, then try to fuse two similar series.

As for question 2, Making adjustments for time elapsed from the end of the quarter is important, because the estimate is stale by 70-165 days or so. ?I treat it like a 10-year zero coupon bond and look at the return since the end of the quarter. ?I could be more exact than this, adjusting for the exact period?and dividends, but the surprise from the unknown change in investor behavior which is larger than any of the adjustment simplifications. ?I take the return since the end of the last reported quarter and divide by ten, and subtract it from my ten year return estimate. ?Simple, understandable, and usable, particularly when the adjustment only has to wait for 3 more months to be refreshed.

PS — don’t suggest that I write on politics. ?I annoy too many people with my comments on that already. 😉

Now for the next question:

I have a quick question. If an investor told you they wanted a 3% real return (i.e., return after inflation) on their investments, do you consider that conservative? Average? Aggressive? I was looking at some data and it seems on the conservative side.

EEE

Perhaps this should go in the “dirty secrets” bin. ?Many analyses get done using real return?statistics. ?I think those are bogus, because inflation and investment returns are weakly related when it comes to risk assets like stocks and any other investment with business risk, even in the long run. ?Cash and high-quality bonds are different. ?So are precious metals and commodities as a whole. ?Individual commodities that are not precious metals have returns that are weakly related to inflation. ?Their returns depend more on their individual pricing cycle than on inflation.

I’m happier projecting inflation and real bond returns, and after that, projecting the nominal returns using my models. ?I typically do scenarios rather than simulation?models because the simulations are too opaque, and I am skeptical that the historical relationships of the past are all that useful without careful handling.

Let’s answer this question to a first approximation, though. ?Start with the 10-year breakeven inflation rate which is around 2.0%. ?Add to that a 10-year average life modification of the Barclays’ Aggregate, which I estimate would yield about 3.0%. ?Then go the the stock model, which at 9/30/16 projected 6.37%/yr returns. ?The market is up 7.4% since then in price terms. ?Divide by ten and subtract, and we now project 5.6%/year returns.

So, stocks forecast 3.6% “real” returns, and bonds 1.0%/year returns over the next 10 years. ?To earn a 3% real return, you would have to invest 77% in stocks and 23% in 10-year high-quality bonds. ?That’s aggressive, but potentially achievable. ?The 3% real return is a point estimate — there is a lot of noise around it. ?Inflation can change sharply upward, or there could be a market panic near the end of the 10-year period. ?You might also need the money in the midst of a drawdown. ?There are many ways that a base scenario could go wrong.

You might say that using stocks and bonds only is too simple. ?I do that because I don’t trust return most risk and return estimates for more complex models, especially the correlation matrices. ?I know of three organizations that I think have good models — T. Rowe Price, Research Affiliates, and GMO. ?They look at asset returns like I do — asking what the non-speculative returns would be off of the underlying assets and starting there. ?I.e. if you bought and held them w/reinvestment of their cash flows, how much would the return be after ten years?

Earning 3% real returns is possible,?and not that absurd, but it is a little on the high side unless you like holding?77% in stocks and 23% in 10-year high-quality bonds, and can bear with the volatility.

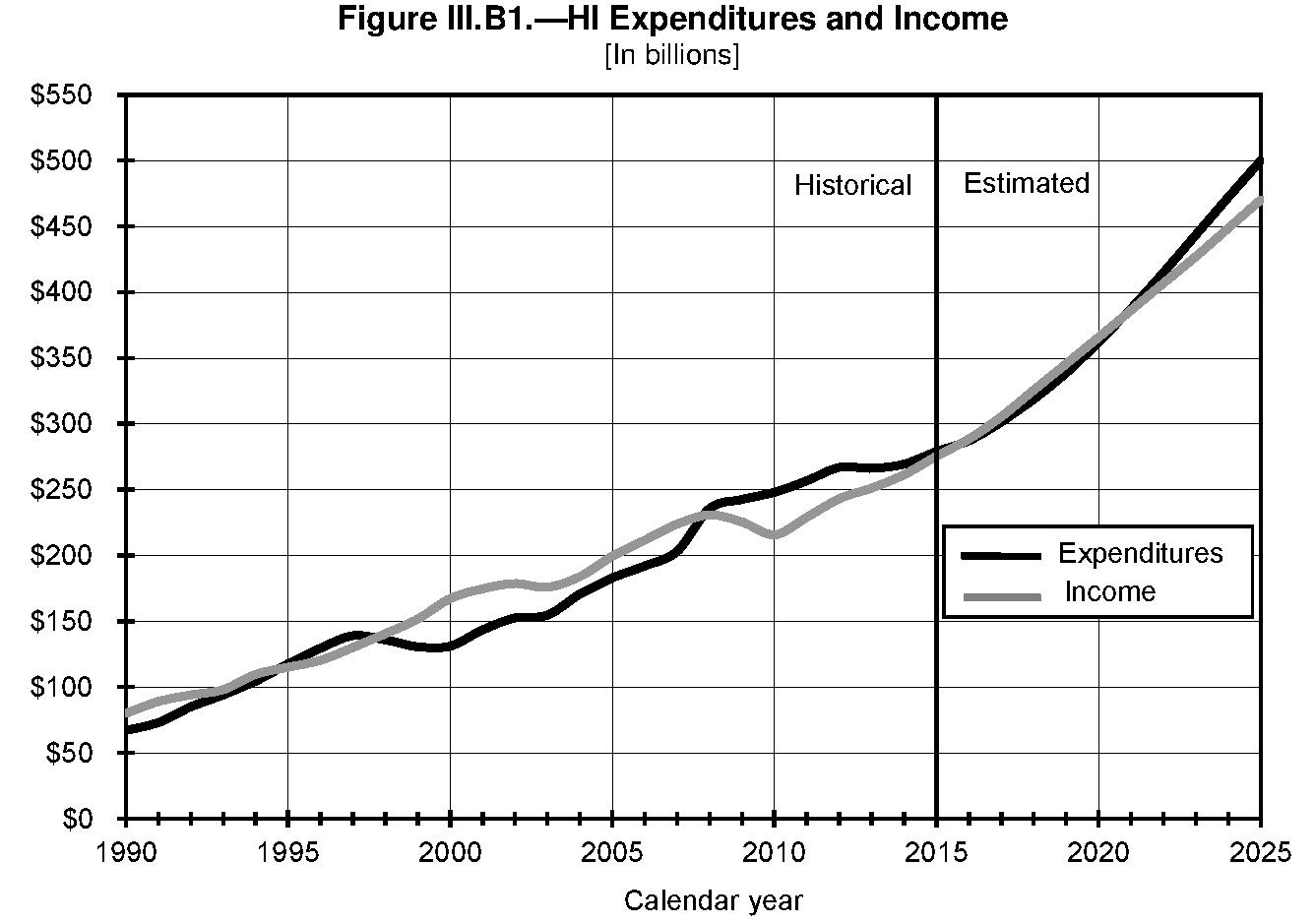

The last time I wrote about this was four years ago. ?I have covered this topic off and on for the last 25 years. ?As usual, the report got released during a relatively dead time, January 12th, where most people were listening to the preparations for the inauguration. ?I’ll give them some credit though — not as much of a dead time as usual; it was in the middle of a work week, AND earlier than usual. ?(It would be nice to know when it’s coming, though.)

I have two main messages to go with my two graphs. ?The first message is one I have been saying before — beware some of the estimates that you hear, should you hear them at all. ?No one wants to talk about this, but what few that do will look at a few headline numbers and leave it there. ?Really you have to look at it for years, and look at the footnotes and other explanatory sections in the back when things seemingly change for no good reason. ?Also, you have to add all the bits up. ?No one will do that for you. ?Even with that, you are relying on the assumptions that the government uses, and they are not biased toward making the estimates sound larger. ?They tend to make them smaller.

Thus you will see two things that adjust the headline figures. ?In 2004, when Medicare part D was created, the Financial Report of the US Government began mentioning the Infinite Horizon Increment. ?Now, that liability always existed, but the actuaries began calculating how solvent is the system as a whole if it were permanent, as opposed to lasting 75 years.

The second is the Alternative Medicare Scenario. ?When the PPACA (Obamacare) was created in 2010, there was considerable chicanery in the cost estimates. ?The biggest part was that they assumed Medicare Part A (HI) would cost a lot less because they would reduce the amount that they would reimburse. ?They legislated away costs by assuming them away, and then each year Congress would restore the funding so that there wouldn’t be a firestorm when doctors stopped taking Medicare. ?But they left it in for budget and forecast purposes, and showed what the projections would be like if these cuts never took place in what they called the?Alternative Medicare Scenario.

So, did the cuts to Medicare part A take place? No.

As you can see they have gone up almost every year since 2010. The liability should not have gone down. If you think the?Alternative Medicare Scenario is conservative enough, the liability has remained relatively constant since 2010, not diminished dramatically.

How is the load relative to GDP? ?It keeps growing, but since 2010 at a less frantic clip. ?The adjusted ratio below includes the?Alternative Medicare Scenario.

Final Notes

Remember that we have had a recovery since 2009. ?The statistics never assume that we will have another recession, much less a full fledged crisis like 2008-9. ?Without adjustment, the Medicare part A trust fund will run out in 2028. ?There is no provision for what the reimbursements will be made if the trust fund runs dry. ?Social Security’s trust fund will run out a few years after that, and instead of getting 12 checks a year, people will only get 9 of that same amount. ?If there is a significant recession, those statistics will move forward by an unknown number of years. ?Without congressional action, because there will be a recession, I would expect that both will run out somewhere in the middle of the 2020s, and then the real political fun will begin.

The tendency has been over time to turn these from entitlements to old age welfare schemes. ?FDR always wanted them to be self funded entitlements with everybody getting roughly the same treatment by formula, because he wanted the program to have widespread legitimacy across all classes, and no sense of stigma for being a poor old person on the dole.

Given the strategies that exist around qualifying for Medicaid, those days are gone, so I would expect that benefits will be limited for those better off, inflation adjustments eliminated, taxes raised to some degree, eligibility ages quickly raised a few more years, with elimination of strategies that allow people to get more out of the system by being clever. ?(As an example, expect the favorable late retirement factors to get reduced, and the early retirement factors to go down even more.)

Does this sound fun? ?Of course not, but remember that cultures are larger than economies, which are larger than governments. ?The cultural need for supporting poor elderly people will lead funding to continue, unless it makes the government, and the culture as a whole fail in the process, and that would never happen, right?

Well, this market is nothing if not special. ?The S&P 500 has gone 84 trading days without a loss of 1% or more. ?As you can see in the table below, that ranks it #17 of all streaks since 1950. ?If it can last through February 27th, it will be the longest streak since 1995. ?If it can last through March 23rd, it will be the longest streak since 1966. ?The all-time record (since 1950) would take us all the way to June.

Here’s another way to think about this — look at the VIX. ?It closed today at 10.85. ?Sleepy, sleepy… no risk to be found. ?When you don’t have any significant falls in the market, the VIX tends to sag. ?Aside from the election, which is an exception to the rule, the last two peaks of the VIX over the last six months were after 1%+ drops in the S&P 500.

The same would apply to credit spreads, which are also tight. ?No one expects a change in liquidity, a credit event, a national security incident, etc. ?But as I commented on Friday:

I think the thing that would hurt the most money managers is a melt-up that they would feel forced 2 chase, followed by a hard correction $$

This is an awkward time when you have a lot of people arguing that the market CAN’T GO HIGHER! ?Let me tell you, it can go higher.

Will it go higher? ?Who knows?

Should it go higher? ?That’s the better question, and may help with the prior question. ?If you’re thinking strictly about absolute valuation, it shouldn’t go higher — we’re in the mid-80s on a percentile basis. ?On a relative valuation basis, where are you going to go? ?On a momentum basis, it should go higher. ?It’s not a rip-roarer in terms of angle of ascent, which bodes well for it. ?The rallies that fail tend to be more violent, and this one is kinda timid.

We sometimes ask in investing “who has the most to lose?” ?As in my tweet above, that very well could be asset allocators with low stock allocations that conclude that they need to chase the rally. ?Or, retail waking up to how great this bull market has been, concluding that they have been missing out on “free money.”

Truth, I’m not hearing many people at all banging the drum for this rally. ?There is a lot of skepticism.

As for me, I don’t care much. ?It’s not a core skill of mine, nor is it a part of my business. ?I am finding cheap stocks still, and I will keep investing through thick and thin, unless the 10-year forecast model that I use says future returns are below 3%/year. ?Then I will hedge, and encourage my clients to do so as well.

Until then, the game is on. ?Let’s see how far this streak goes.

Aside from the bankruptcy of a plan sponsor, the benefits of someone being paid their pension can’t be cut. ?Right?

Well, mostly true. ?With governments in trouble, benefits have been cut, as in Rhode Island, Detroit, and a variety of other places with badly managed finances. ?Usually that’s a big political fight. ?Concessions come partly as a result that you could end up with less if you fight it, and don’t take the deal.

With corporations, the protection of the Pension Benefits Guarantee Corporation [PBGC] has kept pensions safe up to a limit — as of 2016, up to roughly $60K/year for those retiring at age 65 (less for younger retirees) from single-employer plans, and $12,870/year at most for those in multiemployer plans. ?(For some complexities, read more here. ?Also note that the PBGC itself is underfunded and faces antiselection problems as well.)

Multiemployer plans are an inherently weak structure, because?insolvent employers can’t contribute to fund plan deficits, and typically, multiemployer plans arise from collective bargaining arrangements, so that the firms employing the laborers are all in the same industry. ?Insolvency in industries, particularly where there is collective bargaining pushing up costs and limiting work process flexibility, tends to be correlated across firms. ?My poster child for that was the steel industry in 2002, where 20+ firms went insolvent. ?Employer insolvencies in an underfunded multiemployer plan affect all participants, including those working for solvent firms. ?(Note that solvent employers have to pay their pro-rata?share of underfunding in order to exit a multiemployer plan, as I noted for UPS in this article.)

Now in 2014, Congress passed a law called the?Kline-Miller Multiemployer Pension Reform Act of 2014. ?That allowed the PBGC, together with the Departments of Treasury and Labor, to negotiate benefit cuts to the pension plans in order to avoid the plans going insolvent — at which point, all pensioners would be limited to the PBGC limits for their payments. ?Workers in the plan — active, vested, and retired, would have to vote on any deal. ?Majority of those voting wins, so to speak.

The first plan to successfully go through this procedure and cut benefits to participants happened a few weeks ago, in the Iron Workers Local 17 Pension fund. ?Average benefits were cut 20%, with some cut as much as 60%, and some not cut at all. ?The plan was funded to a 24% level, and there are only 632 active employed workers to cover the benefits of 2,042 participants. ?The fund would likely run out of money in 2024. ?Note that only 900+ voted on the cuts, with the cuts passing at roughly 2-1.

There are at least four other multiemployer plans with similar applications to cut benefit payments. ?Prior to this four other multiemployer plans had such applications denied — there were a variety of reasons for the denials: the cuts were done in an inequitable way in some cases, return assumptions were unreasonably high, etc.

My original source for this piece is note by David Gonzales of Moody’s. ?They rate these actions as credit positive because it potentially ends the process where an underfunded multiemployer plan would encourage an employer to default because it can’t afford the liability. ?Somewhat perverse in a way, because the pain has to go somewhere on an underfunded plan — it’s all a question of who gets tapped. ?Note that it also protects the PBGC Multiemployer Trust, which itself is likely to run out of money by 2025. ?After that, those relying on the PBGC for multiemployer pension payments get zero, unless something changes.

You might think this is an extreme situation, and yes, it is extreme. ?It’s not so extreme that there aren’t other underfunded plans as bad off as this multiemployer plan. ?I would encourage everyone who has a defined benefit plan to take a close look at their funded status. ?I don’t care about what your state constitution says on protecting your pension benefits. ?If the cash gets close to running out, “the?powers that be” will find a way around that. ?After all, what happened with the?Iron Workers Local 17 Pension Fund was illegal prior to 2014. ?Now it is 2017, and benefits were cut.

Because of underfunding, there will be more cuts. ?Depend on that happening for the worst funds, and at least run through the risk analysis of what you would do if your pension benefit were cut by 20% for a municipal plan, or to the PBGC limit for a corporate plan. ?Why? ?Because it could happen.

If you do remember the first time I wrote about yield being poison,?you are unusual, because it was the first real post at Aleph Blog. ?A very small post — kinda cute, I think when I look at it from almost ten years ago… and prescient for its time, because a lot of risky bonds were about to lose value (in 19 months), aside from the highest quality bonds.

I decided to write this article this night because I decided to run my bond momentum model — low and behold, it yelled at me that everyone is grabbing for yield through credit risk, predominantly corporate and emerging markets, with a special love for bank debt closed end funds.

I get the idea — short rates are going to rise because the Fed is tightening and inflation is rising globally, and there is no credit risk anymore because economic growth is accelerating globally — it’s not just a US/Trump thing. ?I just have a harder time playing the game because we are in the wrong phase of the credit cycle — profit growth is nonexistent, and debts are growing.

I have a few other concerns as well. ?Even if encouraging exports and discouraging imports aids the US economy for a while (though I doubt it — more jobs rely on exports than are lost by imports, what if there is retaliation?) there is a corresponding opposite impact on the capital account — less reinvestment in the US. ?We could see higher yields…

Charles Gave:THE END OF THE DOLLAR STANDARD https://t.co/WZxUWX15SN I have wondered the same: Won’t Trump’s policies undo USD standard? $$

That said, I would be more bearish on the US Dollar if it had some real competition. ?All of the major currencies have issues. ?Gold, anyone? ?Low short rates and rising inflation are the ideal for gold. ?Watch the real cost of carry go more negative, and you get paid (sort of) for holding gold.

If growth and inflation?persist globally (consider some of the work @soberlook has ?been doing at The WSJ Daily Shot — a new favorite of mine, even his posts are?too big) then almost no bonds except the shortest bonds will be any good in the intermediate-term — back to the ’70s phrase “certificates of confiscation.” ?One other effect that could go this way — if the portion of Dodd-Frank affecting bank leverage is repealed, the banks will have a much greater ability to lend overnight, which would be inflationary. ?Of course, they could just pay special dividends, but most corporations lean toward growing the business, unless they are disciplined capital allocators.

As Trump Team Enters Office, Repealing Dodd-Frank Could Have Inflationary Risks https://t.co/RCMcV5ksdv I talk about excess bank capital $$

But it is not assured that the current growth and inflation will persist. ?M2 Monetary velocity is still low, and the long end of the yield curve does not have yield enough priced in for additional growth and inflation. ?Either long bonds are a raving sell, or the long end is telling us we are facing a colossal fake-out in the midst of too much leverage globally.

Summary

I’m going to stay high quality and short for now, but I will be watching for the current trends to break. ?I may leg into some long Treasuries, and maybe some foreign bonds. ?Gold looks interesting, but I don’t think I am going there. ?I’m not making any big moves in the short run — safe and short feels pretty good for the?bond portfolios that I manage. ?I think it’s a time to preserve principal — there is more credit risk than the market is pricing in. ?It might take a year or two to get there, or it might be next month… I would simply say stay flexible and look for a time where you have better opportunities. ?There is no fat pitch at present for long only investors like me.

Postscript

To those playing with fire buying dividend paying common stocks, preferred stocks, MLPs, etc. for yield — if we hit a period where credit risk becomes obvious — all of your “yield plays” will behave like stocks in a poisoned sector. ?There could be significant dividend cuts. ?Dividends are not guaranteed like bonds — bonds must pay or it is bankruptcy. ?Managements avoid defaulting on their bonds and loans, but will not hesitate to cut or not pay dividends in a crisis — it is self-preservation, at least in the short-run. ?Even if they get replaced by angry shareholders, the management typically gets some sort of parachute if the company survives, and far less in bankruptcy.

One final note on this point — stocks that have a lot of yield buyers behave more like bonds. ?If bond yields rise above current stock earnings yields, the stock prices will fall to reprice the yield of the stock, even if there is no bankruptcy risk.

And, if you say you can hold on and enjoy the rising dividends of your high quality companies? ?Accidents happen, the same way they did to some people who bought houses in the middle of the last decade. ?Many could not ride out the crisis because of some life event. ?Make sure you have a margin of safety. ?In a really large crisis, the return on risk assets may look decent from ten years before to ten years after, but a lot of people get surprised by their need to draw on those assets at the wrong moment — bad events come in bunches, when the credit cycle goes bust. Be careful, and don’t reach for yield.

It was shortly after the election when I last moved my trading band. ?Well, time to move it again, this time up 4%, with a small twist. ?I’m at my cash limit of 20%, with a few more stocks knocking on the door of a rebalancing sale, and none near a rebalancing buy. ?(To decode this, you can read my article on portfolio rule seven.) ?Here is portfolio rule seven:

Rebalance the portfolio whenever a stock gets more than 20% away from its target weight. Run a largely equal-weighted portfolio because it is genuinely difficult to tell what idea is the best. Keep about 30-40 names for diversification purposes.

This is my interim trading rule, which helps me make a little additional money for clients by buying relatively low and selling relatively high. ?It also reduces risk, because higher prices are riskier than lower prices, all other things equal.

There are two companies that are double-weights in my portfolio, one half-weight, and 32 single-weights. ?The half-weight is a micro-cap that is difficult to buy or sell. (Patience, patience…) ?With cash near 20%, a?single-weight currently runs around 2.2% of assets, with buying happening near 1.75%, and selling near 2.63%.

But, I said there was a small twist. ?I’m going to add another single-weight position. ?I don’t know what yet. ?Also, I’m leaving enough in reserve to turn one of the single-weights into a double-weight. ?That company is a well-run Mexican firm that has ?had a falling stock price even though it is still performing well. ?If it falls another 10%, I will do more than rebalance. ?I will rebalance and double it.

Part of the reason for the move in both number of positions and position size at the same time is that both the half-weight and one single-weight that is at the top of its band are being acquired for cash, and so they (3.5% of assets) behave more like cash than stocks.

Thus, amid a portfolio that has been performing well, I am adjusting my positioning so that if the market continues to do well, the portfolio doesn’t lag much, or even continues to outperform. ?I’m not out to make big macro bets; I will make a small bet that the market is high, and carry above average cash, but it will all get deployed if the market falls 25%+ from here.

I keep the excess cash around for the same reason Buffett does. ?It gives you more easy options in a bad market environment. ?Until that environment comes, you’ll never know how valuable is is to keep some extra cash around. ?Better safe, than sorry.