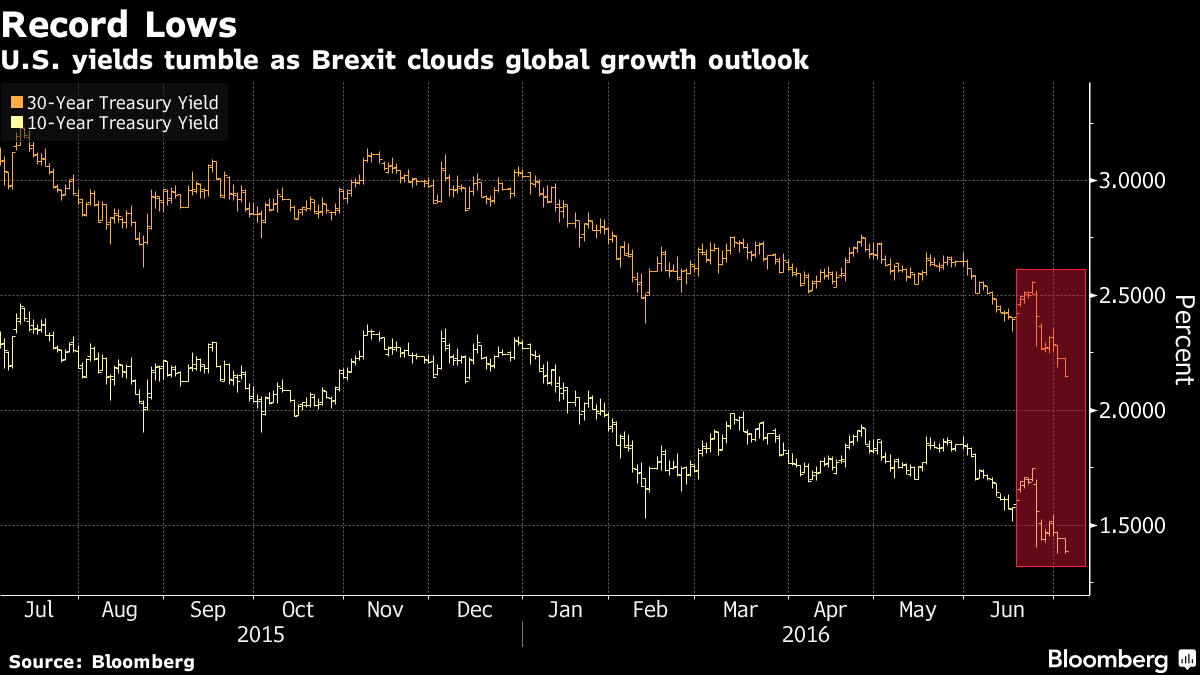

Rates can go lower from here. ?For as long as I can remember, I have been told by many experts that rates can’t go lower, or, that they must go up — there is no way they can go lower. ?I have argued with that idea, as has Hoisington (Lacy Hunt), Gary Shilling and a few others.

Note also that the Fed and most central banks have been on the wrong side of this as well. ?They keep saying that inflation will come, economic activity will pick up,?and that interest rates will rise.

The Fed keeps saying that they will tighten policy. ?I’ll tell you this — with only 0.82% between the yields on 10- and 2-year Treasuries, the Fed is not tightening.

WIth debt levels as high as they are (both government and private), trying to influence economic activity though interest rates is a dumb idea. ?Incenting borrowers to borrow more is difficult, aside from the government — and they rarely do anything with the money that helps produce opportunities for greater economic activity.

We would be better off without “policymakers” trying to “stimulate” the economy, “manage” it, “stabilize” it, etc. ?(But where is the political will to change things — the populace wants easy prosperity, and who is there to tell them to accept a rough world where work and competition is tough, and there is no “Big Daddy” to make life easy? ?The people are the problem. ?The politicians are only a symptom.)

There is one thing that could change this, but it would lay bare the intellectual and moral bankruptcy of what policymakers have been trying to do, which is try to maintain the real value of debt claims while still trying to “stimulate” the economy. ?They could burn away the value of debt claims through an inflation greater than that of the 1970s.

So far, they aren’t willing to do that. ?But their existing policies will prolong the stagnation.

And as such, rates can fall further — with a lot of noise/variation around it.

Picture Credit: Peanuts Reloaded || Roughly: “Perhaps today Brexit;?Monday an exit from Italy or Spain; [then]?Europe dismantles”=-==-=-=-=-=-=-=-=-=-=-=-=-=-==-=-

At a time like this, when the Brexit Boogeyman goes “Boo!” it’s time to take stock of the situation amid panic.

Though the UK will face some political unrest as the Prime Minister resigns, and article 50 is likely but not certainly invoked, the nature of political discourse hasn’t shifted in full. ?Though an important question, it is only one question, and more things will remain stable than change.

At least that is most likely. ?If you think of “real options” theory, you could say, “Okay, a door opened today that was previously locked. ?What new doors beyond that one could be opened?” ?Other countries could leave the EU and/or?Eurozone [EZ]. ?The EU/EZ could dissolve. ?The odds of other countries leaving isn’t that high. ?For the EU or EZ to dissolve would take a lot of doing, and the odds of that happening is very low, though higher than the odds yesterday.

As I said a week ago:

Governments are smaller than markets; markets are smaller than cultures.

What I am saying is that almost everything affecting the needs of people will get done when there is sufficient freedom. ?If Brexit occurs, the UK will negotiate some agreement that is mutually beneficial to the UK and the EU, and most things will go on as they do today. ?Even with a subpar agreement,?perfidious Albion is very effective at getting what they need completed. ?This is especially true of their very effective and creative financial sector in the City of London without which most effective international secrecy, taxation avoidance and regulatory avoidance business could not be done.

Whatever happens, it will happen slowly. ?Leaving a complex multinational group like the EU takes two years at least. ?How it all works out in detail is not predictable.

I can say that human systems tend toward stability. ?People act to preserve the things that they like. ?Only under severe conditions does that cease to be true, and even then typically only for short periods of time.

I can also say something a little more controversial. ?Wealth, assets, and money [WAM] act like they are alive and have more votes than people do under most conditions. ?Why am I saying this?

Governments come in, and go out, but for the most part, the same things get done. ?Those thinking that radical change will come are usually deeply disappointed. ?WAM tend to maintain the status quo, not because their owners bribe politicians and suborn regulators pay political action contributions, ?but because people want the streams of goods and services that help make WAM valuable. ?Only a genuine crisis at least as large as?the Great Depression or the Civil War can create truly radical change that reshapes the basic desires of most of the people in a nation.

Capitalist democracies that respect the rule of law (e.g., the government is also governed by?a higher law) are usually pretty stable; systems that don’t have significant capitalism or democracy may last a couple generations, but tend to fall apart.

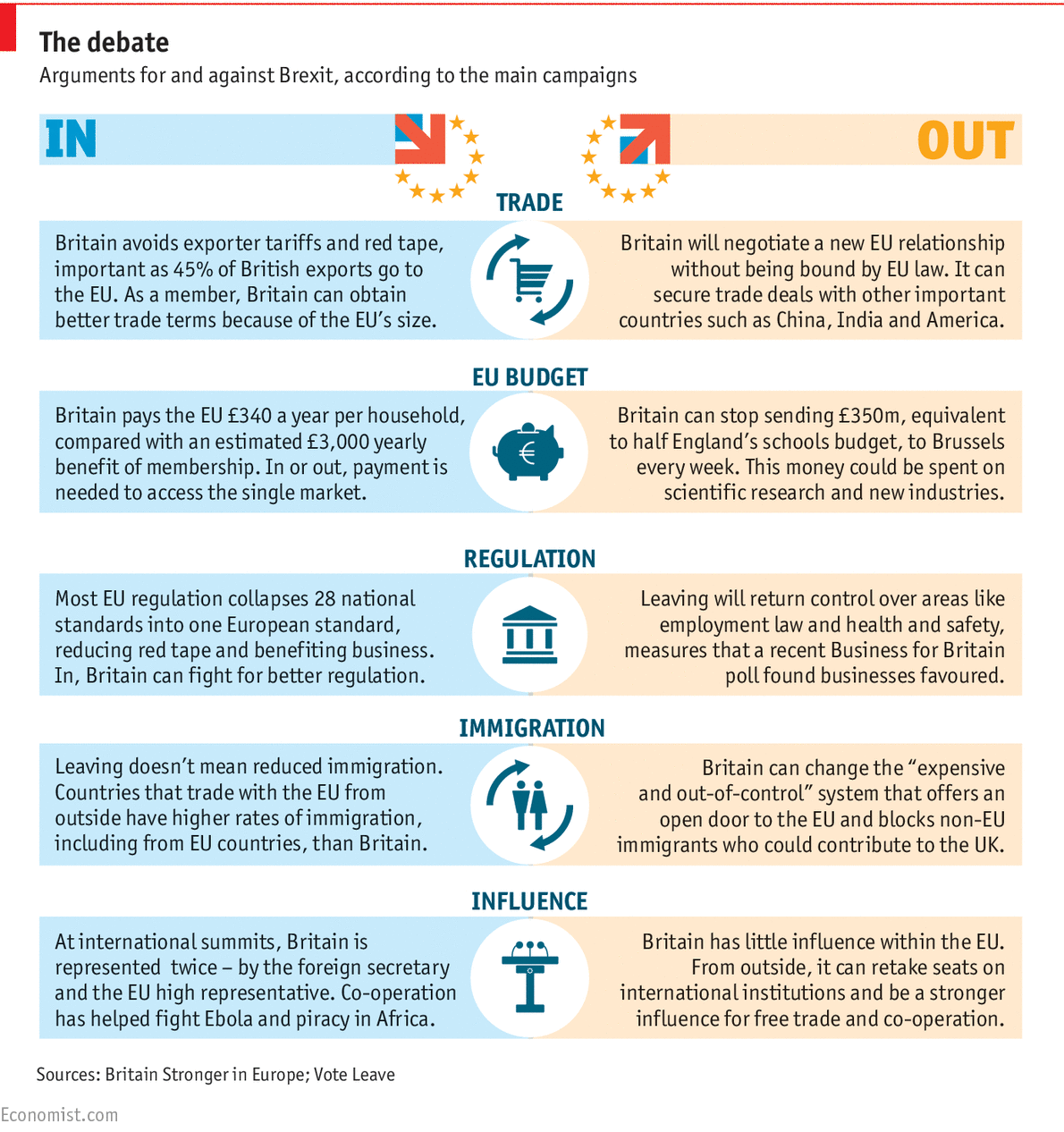

All that said, there is significant economic pressure to do two things after the Brexit:

Rethink the single currency and common laws

Maintain a free-ish trade zone in goods and services

The Eurozone does not allow for the necessary economic adjustments across nations in a fiat?monetary system. ?Nations need their own currencies, central banks, etc. ?They also need to govern themselves via their local culture, not someplace far away with misguided idealists who think they know what’s best for all.

Free-ish trade maintains most of what is needed?for human needs. ?The European Union is a political construct meant to prevent war from ever recurring in Europe. ?The best way to do that is through trade. ?Severe wars rare start between nations that rely on each other and interact through commerce.

My view is that ten years from now, the goods and services that people want will get delivered, regardless of the governmental structures in Europe. ?I will invest accordingly.

Practical Implications

Things will be rocky in the short run, and there will be more bumps along the road as the Brexit negotiations go on. ?I will be resisting panic and euphoria in modest ways. ?This isn’t the sum total of my strategies, but I expect that profitable business will continue, and that people and nations will pursue generally intelligent long-term self-interest as events unfold.

When I say modest, I tweak my portfolios at the edges. ?Brexit does not comprise more than 5% of what I would do with assets. ?As with any investment idea, spread your bets, diversify, don’t bet the farm.

And, I would say the same even to governments — if you don’t have contingency plans for the possibility of the EU shrinking or even disappearing, you are not truly prepared for all contingencies. ?As Warren Buffett once said (something like) “We’re paid to think about the things that ‘can’t happen.'”

In closing, many thought that Brexit could not happen. ?Now, what else “can’t happen?” 😉

When do you admit that you are wrong? ?Do you do it publicly? ?Do you hide it?

Do you hide it plain sight?

When I look at the graph for Fed funds for 2017 and later, I think the FOMC is admitting that they were wrong for a long time, and now hide that in plain sight.

They don’t admit that they were wrong. ?They don’t admit that the economy has proven to be a lot weaker than they ever expected, and that they now expect that to persist for a while.

That’s what the graphs for Fed funds and GDP say.

But what does the FOMC say in its statement? ?It expresses confidence in future GDP robust growth, even though their expectations have collapsed to 2% real growth as far as they care to opine.

Look at the above graph, and see how it has all converged to 2%.

PCE Inflation? They assume it will be 2% before the year starts, and then they adapt to incoming data.

There’s no model here, just a disappointed ideology that says they wish to ?produce a 2% PCE inflation rate, dubious as that goal is.

The only thing more dubious there is their ability to achieve their ideology.

Remember after the financial crisis? There were those who said unemployment would never return to 5% — that the natural rate of unemployment was permanently higher.

I may have been among them.

Well, now the FOMC has a new consensus. ?Unemployment below 5%?as far as they care to opine.

When I look at these graphs, particularly the ones for Fed funds and GDP growth, I see a paradigm shift where Bayesian priors have been dragged kicking and screaming by the data to No Man’s Land.

Grudgingly they acknowledge the data in the graphs, but they don’t have a theory to go along with it, so their statements and minutes sound the same.

Nothing is changed. ?Soon our policies will restore robust real GDP growth, produce inflation and then we will tighten policy and restore normalcy.

Well, that’s what their minutes and statements say.

But who are you going to believe? ?The FOMC and their words, or your lying eyes looking at their graphs?

Information received since the Federal Open Market Committee met in March indicates that labor market conditions have improved further even as growth in economic activity appears to have slowed.

Information received since the Federal Open Market Committee met in April indicates that the pace of improvement in the labor market has slowed while growth in economic activity appears to have picked up.

FOMC shades GDP up and employment down, which is the opposite of last time.

Although the unemployment rate has declined, job gains have diminished.

Sentence moved up in the statement.? Expresses less confidence in the labor market.

Growth in household spending has moderated, although households’ real income has risen at a solid rate and consumer sentiment remains high.

Growth in household spending has strengthened.

Shades up household spending.

Since the beginning of the year, the housing sector has improved further but business fixed investment and net exports have been soft.

Since the beginning of the year, the housing sector has continued to improve and the drag from net exports appears to have lessened, but business fixed investment has been soft.

Shades up net exports.

A range of recent indicators, including strong job gains, points to additional strengthening of the labor market.

?

Sentence moved up in the statement.

Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and falling prices of non-energy imports.

Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports.

No change.

Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Market-based measures of inflation compensation declined; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy.

The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will continue to strengthen.

The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will strengthen.

No change.

Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further.

Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further.

The Committee continues to closely monitor inflation indicators and global economic and financial developments.

The Committee continues to closely monitor inflation indicators and global economic and financial developments.

No change.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent.

No change.

The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

No change.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

No change.? Gives the FOMC flexibility in decision-making, because they really don?t know what matters, and whether they can truly do anything with monetary policy.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

No change.? Says that they will go slowly, and react to new data.? Big surprises, those.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

No change.? Says it will keep reinvesting maturing proceeds of agency debt and MBS, which blunts any tightening.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Esther L. George; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo.

Back to unanimity in the monoculture of neoclassical economics.

Voting against the action was Esther L. George, who preferred at this meeting to raise the target range for the federal funds rate to 1/2 to 3/4 percent.

?

Say bye to the small dissent.

Comments

The FOMC meets too frequently. Often the economic signals at one meeting get reversed at the next meeting, as was true this time.? Rather than hyper-interpreting every wiggle, maybe the FOMC should meet every six months, with the proviso that the chairman could call an interim meeting if the situation demanded it.

That this is true regarding economic aggregates has been known since the ?50s. For a variety of reasons, it is difficult to distinguish signal from noise over periods of less than a year.

Then again, maybe the FOMC meets to make it look like they are doing something. 😉

This statement was a nothing-burger.

Policy continues to stall, as the economy muddles along.

But policy should be tighter. Savers deserve returns, and that would be good for the economy.

The changes for the FOMC?s view are that labor indicators are weaker, and GDP and household spending are stronger.

Equities fall and bonds rise a little. Commodity prices rise and the dollar falls.

The FOMC says that any future change to policy is contingent on almost everything.

The key variables on Fed Policy are capacity utilization, labor market indicators, inflation trends, and inflation expectations. As a result, the FOMC ain?t moving rates up much, absent much higher inflation, or a US Dollar crisis.

Investors need things to scare them, or they don’t have a normal life. ?This is kind of like the bachelor uncle who tells little?nieces and nephews about scary things that lurk under their beds, and only come out at night for mischief and mayhem. ?(Then the parents pick up the pieces later, when they wonder why William or Elizabeth no longer sleep well at night.)

That’s the way I feel about US & international market reactions to the possibility of UK/Britain exiting the EU, otherwise called “Brexit.” ?It’s overblown. ?Quoting from an older article of mine:

Governments are smaller than markets; markets are smaller than cultures.

What I am saying is that almost everything affecting the needs of people will get done when there is sufficient freedom. ?If Brexit occurs, the UK will negotiate some agreement that is mutually beneficial to the UK and the EU, and most things will go on as they do today. ?Even with a subpar agreement, perfidious Albion is very effective at getting what they need completed. ?This is especially true of their very effective and creative financial sector in the City of London without which most effective international secrecy, taxation avoidance and regulatory avoidance business could not be done.

There are other reasons not to worry as well if you live outside the UK. ?The biggest reason is that the UK is only a small part of the global economy, and the economic effects on non-EU trade and finance are smaller still. ?And unlike the idea was small but “contained,” in this case, large second order effects aren’t there. ?Yes, someday other nations may wise up and decide to leave the EU, but?no major countries are likely to do that over the next decade, absent some crisis. ?(Crises in the EU? Those aren’t allowed to happen; ask any Eurocrat, they’ll tell ya.)

A second reason not to worry is that leaving the EU ends a second level of regulation of UK economic activity. ?This will enable better growth in the longer term. ?Are there things that the UK will lose? ?Sure, they won’t have as good of a trade deal with the EU, but they will have the ability to try to craft better deals elsewhere, like a Transatlantic Free Trade Area.

Looking over this, the UK already depends less on the EU than most member states, making the exit less of a big deal for the UK and the EU.

My view is this: leaving the EU won’t be a big thing in the long run for the UK. ?In the short-run, there will be some uncertainty and volatility as things get worked out. ?For the rest of the world, it will be a big fat zero, so ignore this, and focus on something with more meaning, like bizarre monetary policy, and the twisting effects it is having on our world, or the global entitlements crisis — too many people retiring, too few to support them, especially medically.

So, be willing to take some additional risk if people mindlessly panic if the UK/Britain exits the EU.

The Z.1 report came out yesterday, giving an important new data point to the analysis. ?After all, the most recent point gives the best read into current conditions. ?As of March 31st, 2016 the best estimate of 10-year returns on the S&P 500 is 6.74%/year.

The sharp-eyed reader will say, “Wait a minute! ?That’s higher than last time, and the market is higher also! ?What happened?!” ?Good question.

First, the market isn’t higher from 12/31/2015 to 3/31/2016 — it’s down about a percent, with dividends. ?But that would be enough to move the estimate on the return up maybe 0.10%. ?It moved up 0.64%, so where did the 0.54% come from?

The market climbs a wall of worry, and?the private sector has been holding less stock as a percentage of assets than before — the percentage?went from 37.6% to 37.1%, and the absolute amount fell by about $250 billion. ?Some stock gets eliminated by M&A for cash, some by buybacks, etc. ?The amount has been falling over?the last twelve months, while the amount in bonds, cash, and other assets keeps rising.

If you think that return on assets doesn’t vary that much over time, you would?conclude that having a smaller amount of stock owning the assets would lead to a higher rate of return on the stock. ?One year ago, the percentage the private sector held in stocks was 39.6%. ?A move down of 2.5% is pretty large, and moved the estimate for 10-year future returns from 4.98% to 6.74%.

Summary

As a result, I am a little less bearish. ?The valuations are above average, but they aren’t at levels that would lead to a severe crash. ?Take note, Palindrome.

Bear markets are always possible, but a big one is not likely here. ?Yes, this is the ordinarily bearish David Merkel writing. ?I’m not really a bull here, but I’m not changing my asset allocation which is 75% in risk assets.

Postscript for Nerds

One other thing affecting this calculation is the Federal Reserve revising estimates of assets other than stocks up prior to 1961. ?There are little adjustments in the last few years, but in percentage terms the adjustments prior to 1961 are huge, and drop the R-squared of the regression from 90% to 86%, which also is huge. ?I don’t know what the Fed’s statisticians are doing here, but I?am going to look into it, because it is?troubling to wonder if your data series is sound or not.

That said, the R-squared on this model is better than any alternative. ?Next time, if I get a chance, I will try to put a confidence interval on the estimate. ?Till then.

There were four?main ideas that came out of those articles:

Saudi Arabia would allow the price of crude oil to fall to hurt competitors/rivals, particularly Iran.

The price of crude oil would stay near $50/barrel.

Lots of overlevered companies dependent on a high price for crude oil would go bankrupt.

But?bankruptcy would happen to fewer, and more slowly, because of all the private equity wanting to buy distressed assets.

All that said, my view has changed a little recently. ?I could be wrong, but I think that the ceiling price for crude oil may be $70/barrel for a few years, with the average remaining at $50. ?I believe this because I think the Saudis are more desperate for cash than most believe.

Here’s my reasoning:

First, you have them selling off a?5%?interest in Saudi Aramco. ?When you need?money, there is a tendency to sell high quality easily saleable assets, because they will sell for a high price, and with little fuss. ?Admittedly, they aren’t rushing to do it, which weakens my point. ?My view is that you would sell off lesser things that aren’t core, rather than complicate life by selling off a portion of a top quality asset.

Fifth, and most speculatively, I wonder if many of the US Treasury holdings have been pledged to cover other debts. ?No proof here, but it’s not uncommon to use highly liquid assets as collateral for privately contracted debts. ?That may explain the musing by some that there had to be more US Treasuries ?there… but where are they?

What this implies to me is that Saudi Arabia is now little different than most of their associates in OPEC. ?Their financial situation is tight enough that they must pump crude oil without respect?to the strategy of holding crude oil off the markets to get better prices. ?It’s not just punishing US shale oil production and Iranian crude production — the Saudis need the money.

If the Saudis need the money, and must pump, then OPEC lacks any significant coalition to raise prices. ?Prices will rise with growth in demand, and cheap resource depletion… but as for right now, there are enough barrels to come out of the ground below $70.

The Saudi need for money is a much simpler explanation than trying to knock out US shale oil, or gouge the Iranians, because it has the Saudis acting directly in their own interests, and it fits the price series for crude oil better.

PS — One more note: this is mildly bearish for the US Dollar as the US does not have the same dedicated buyer of US Dollar assets as it once did. ?I say mildly bearish, because most of the damage is already past.

Nine years ago, I wrote about the so-called “Fed Model.” The insights there are still true, though the model has yielded no useful signals over that time. It would have told you to remain in stocks, which given the way many panic,, would not have been a bad decision.

I’m here to write about a related issue this evening. ?To a first approximation, most investment judgments are a comparison between two figures, whether most people want to admit it or not. ?Take the “Fed Model” as an example. ?You decide to invest in stocks or not based on the difference between Treasury yields and the earnings yield of stocks as a whole.

Now with interest rates so low, belief in the Fed Model?is tantamount to saying “there is no alternative to stocks.” [TINA] ?That should make everyone take a step back and say, “Wait. ?You mean that stocks can’t do badly when Treasury yields are low, even if it is due to deflationary conditions?” ?Well, if there were only two assets to choose from, a S&P 500 index fund and 10-year Treasuries, and that might be the case, especially if the government were borrowing on behalf of the corporations.

Here’s why: in my?prior piece on the Fed Model, I showed how the Fed Model was basically an implication of the Dividend Discount Model. ?With a few simplifying assumptions, the model collapses to the differences between the earnings yield of the corporation/index and its cost of capital.

Now that’s a basic idea that makes sense, particularly when consider how corporations work. ?If a corporation can issue cheap debt capital to?retire stock with a higher yield on earnings, in the short-run it is a plus for the stock. ?After all, if the markets have priced the debt so richly, the trade of expensive debt for cheap equity makes sense in foresight, even if a bad scenario comes along afterwards. ?If true for corporations, it should be true for the market as a whole.

The means the “Fed Model” is a good concept, but not as commonly practiced, using Treasuries — rather, the firm’s cost of capital is the tradeoff. ?My proxy for the cost of capital?for the market as a whole is the long-term Moody’s Baa bond index, for which we have about 100 years of yield data. ?It’s not perfect, but here are some reasons why it is a reasonable proxy:

Like equity, which is a long duration asset, these bonds in the index are noncallable with 25-30 years of maturity.

The Baa bonds are on the cusp of investment grade. ?The equity of the S&P 500 is not investment grade in the same sense as a bond, but its cash flows are very reliable on average. ?You could tranche?off a pseudo-debt interest in a way akin to the old Americus Trusts, and the cash flows would price out much like corporate debt or a preferred stock interest.

The debt ratings of most of the S&P 500 would be strong investment grade. ?Mixing in equity and extending to a bond of 25-30 years throws on enough yield that it is going to be comparable to the cost of capital, with perhaps a spread to compensate for the difference.

As such, I think a better comparison is the earnings yield on the S&P 500 vs the yield on the Moody’s BAA index if you’re going to do something like the Fed Model. ?That’s a better pair to compare against one another.

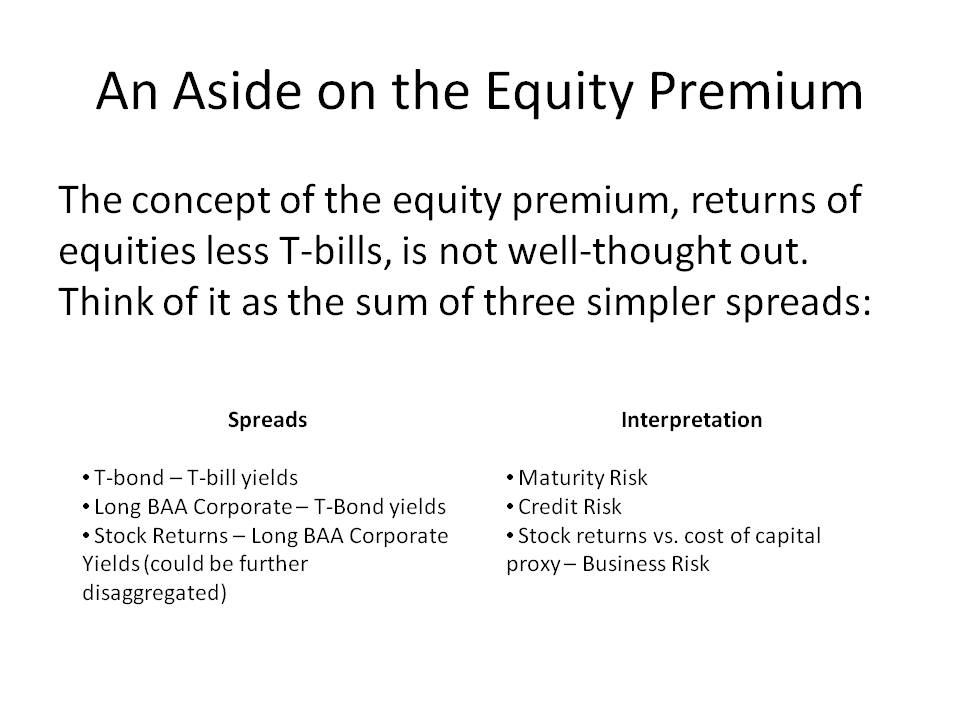

A new take on the Equity Premium!

=-=-=-=-=-=-

That brings up another bad binary comparison that is common — the equity premium. ?What do?stock returns?have to with the returns on T-bills? ?Directly, they have nothing to do with one another. ?Indirectly, as in the above slide from a recent presentation that I gave, the spread between the two of them can be broken into the sum of three spreads that are more commonly analyzed — those of maturity risk, credit risk and business risk. ?(And the last of those should be split into a economic earnings ?factor and a valuation change factor.)

This is why I’m not a fan of the concept of the equity premium. ?The concept relies on the idea that equities and T-bills?are a binary choice within the beta calculation, as if only the risky returns trade against one another. ?The returns of equities can be explained in a simpler non-binary way, one that a businessman or bond manager could appreciate. ?At certain points lending long is attractive, or taking credit risk, or raising capital to start a business. ?Together these form an explanation for equity returns more robust than the non-informative academic view of the equity premium, which mysteriously appears out of nowhere.

Summary

When looking at investment analyses, ask “What’s the comparison here?” ?By doing that, you will make more intelligent investment decisions. ?Even a simple purchase or sale of stock makes a statement about the relative desirability of cash versus the stock. ?(That’s why I prefer swap transactions.) ?People aren’t always good at knowing what they are comparing, so pay attention, and you may find that the comparison doesn’t make much sense, leading you to ask different questions as a result.

Photo Credit: duncan c || It wasn’t my intent initially to compare the words of the FOMC with the scrawlings of a vandal, but ya know, some things are surprise fits

*/*/

I wasn’t surprised to hear in the FOMC minutes that members of the committee thought:

For these reasons, participants generally saw maintaining the target range for the federal funds rate at 1/4 to 1/2 percent at this meeting and continuing to assess developments carefully as consistent with setting policy in a data-dependent manner and as leaving open the possibility of an increase in the federal funds rate at the June FOMC meeting.

and

Participants agreed that their ongoing assessments of the data and other incoming information, as well as the implications for the outlook, would determine the timing and pace of future adjustments to the stance of monetary policy. Most participants judged that if incoming data were consistent with economic growth picking up in the second quarter, labor market conditions continuing to strengthen, and inflation making progress toward the Committee’s 2 percent objective, then it likely would be appropriate for the Committee to increase the target range for the federal funds rate in June. Participants expressed a range of views about the likelihood that incoming information would make it appropriate to adjust the stance of policy at the time of the next meeting. Several participants were concerned that the incoming information might not provide sufficiently clear signals to determine by mid-June whether an increase in the target range for the federal funds rate would be warranted. Some participants expressed more confidence that incoming data would prove broadly consistent with economic conditions that would make an increase in the target range in June appropriate. Some participants were concerned that market participants may not have properly assessed the likelihood of an increase in the target range at the June meeting, and they emphasized the importance of communicating clearly over the intermeeting period how the Committee intends to respond to economic and financial developments.

I was surprised to see some of the markets take it seriously. ?Here’s why:

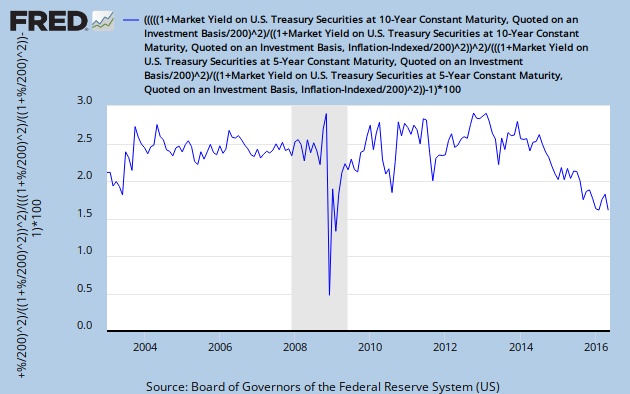

1)?The FOMC loves to talk hawk and them be doves. ?They don’t think the?costs to waiting are significant, particularly given how low measured inflation and and implied future inflation are. ?Five-year inflation, five years forward implied from TIPS spreads is?not high at present as you can see here:

2) The FOMC is well known for giving with the right hand and taking with the left. ?They would like if possible to have the best of both worlds — gentle movement of what they view as key variables, while usually not dramatically changing the forward estimates of those

3) The FOMC’s natural habitat is wishful thinking. ?Their GDP forecasts are usually high, and they suspect their policy tools will move the economy the way they want and quickly, and it’s just not true.

4) LIBOR rates have done a better job of the FOMC at estimating future policy, and they have barely budged since the FOMC minutes came out.

5) The FOMC always has more doves than hawks, and that is the way the politicians who appoint and approve the board members like it. ?They will live with inflation. ?That was yesterday’s problem. ?Today’s problem is stagnant median incomes — and looser monetary policy will help there, right?

Well, no, but I’m sure they clapped when Peter Pan asked them to save Tinkerbell. ?There is no link between inflation and faster real growth over the long haul. ?There may be measurement errors in the short run.

6) They don’t like moving against foreign rates, but that’s not a big factor.

7) GDP isn’t showing much lift at all.

Summary

Unless we have a change in management at the Fed, where they are?not trying to manipulate markets through their words, but maybe one that said little and acted quietly, like the pre-1986 FOMC, they really aren’t worth listening to. ?They act like politicians. ?Let them study Martin and Volcker, and learn from when the FOMC was more effective.

PS — I’m not saying they can’t tighten in June. ?I’m just saying it’s unlikely, and to ignore the comments in the FOMC minutes. ?What the FOMC says is of little consequence. ?It’s what they do that counts. ?They are like a little dog that barks a lot, but rarely bites.

This is another piece in the irregular Simple Stuff series, which is an attempt to make complex topics simple. ?Today’s topic is:

What is risk?

Here is my simple definition of risk:

Risk is the probability that an entity will not meet its goals, and the degree of pain it will go through depending on?how much?it?missed the goals.

There are several good things about this definition:

Note that the word “money” is not mentioned. ?As such, it can cover a wide number of situations.

It is individual. ?The same size of a miss of a goal for one person may cause him to go broke, while another just has to miss a vacation. ?The same event may happen for two people — it may be a miss for one, and not for the other one.

It catches both aspects of risk — likelihood of a bad event, and degree of harm from?how badly the goal was missed.

It takes into account the possibility that there are many goals that must be met.

It covers both composite entities like corporations, families, nations and cultures, as well as individuals.

It doesn’t make life easy for academic economists who want to have a uniform definition of risk so that they can publish economics and finance papers that are bogus. ?Erudite, but bogus.

It doesn’t specify that there has to be a single time horizon, or any time horizon.

It doesn’t specify a method for analysis. ?That should vary by the situation being analyzed.

But this is a blog on finance and investing risk, so now I will focus on that large class of situations.

What is Financial Risk?

Here are some things that financial risk can be:

You don’t get to retire when you want to, or, your retirement is not as nice as you might like

One or more of your children can’t go to college, or, can’t go to the college that the would like to attend

You can’t buy the home/auto/etc. of your choice.

A financial security plan, like a defined benefit plan, or Social Security has to cut back benefit payments.

The firm you work for goes broke, or gets competed into an also-ran.

You lose your job, can’t find another job?as good, and you default on important regular bills as a result. ?The same applies to people who run their own business.

Levered financial businesses, like banks and shadow banks, make too many loans to marginal borrowers, and find at some point that their borrowers can’t pay them back, and at the same time, no one wants to lend to them. ?This can be harmful not just to the?banks and shadow banks, but to the economy as a whole.

Let’s use retirement as an example of how to analyze financial risk. ?I have a series of articles that I have written on the topic based on the idea of the?personal required investment earnings rate [PRIER]. ?PRIER is not a unique concept of mine, but is attempt to apply the ideas of professionals trying to manage the assets and liabilities of an endowment, defined benefit plan, or life insurance company to the needs of an individual or a family.

The main idea is to try to calculate the rate of return you will need over time to meet your eventual goals. ?From my prior “PRIER” article, which was written back in January 2008, prior to the financial crisis:

To the extent that one can estimate what one can reasonably save (hard, but worth doing), and what the needs of the future will cost, and when they will come due (harder, but worth doing), one can estimate personal contribution and required investment earnings rates.? Set up a spreadsheet with current assets and the likely savings as positive figures, and the future needs as negative figures, with the likely dates next to them.? Then use the XIRR function in Excel to estimate the personal required investment earnings rate [PRIER].

I?m treating financial planning in the same way that a Defined Benefit pension plan analyzes its risks.? There?s a reason for this, and I?ll get to that later.? Just as we know that a high assumed investment earnings rate at a defined benefit pension plan is a red flag, it is the same to an individual with a high PRIER.

Now, suppose at the end of the exercise one finds that the PRIER is greater than the yield on 10-year BBB bonds by more than 3%.? (Today that would be higher than 9%.)? That means you are not likely to make your goals.?? You can either:

Save more, or,

Reduce future expectations,whether that comes from doing the same things cheaper, or deferring when you do them.

Those are hard choices, but most people don?t make those choices because they never sit down and run the numbers.? Now, I left out a common choice that is more commonly chosen: invest more aggressively.? This is more commonly done because it is ?free.?? In order to get more return, one must take more risk, so take more risk and you will get more return, right?? Right?!

Sadly, no.? Go back to Defined Benefit programs for a moment.? Think of the last eight years, where the average DB plan has been chasing a 8-9%/yr required yield.? What have they earned?? On a 60/40 equity/debt mandate, using the S&P 500 and the Lehman Aggregate as proxies, the return would be 3.5%/year, with the lion?s share coming from the less risky investment grade bonds.? The overshoot of the ?90s has been replaced by the undershoot of the 2000s.? Now, missing your funding target for eight years at 5%/yr or so is serious stuff, and this is a problem being faced by DB pension plans and individuals today.

The article goes on, and there are several others that flesh out the ideas further:

![Picture Credit: Peanuts Reloaded || Perhaps today Brexit; Monday an exit from Italy or Spain; [then] Europe dismantles](http://alephblog.com/http://alephblog.com/wp-content/uploads/2016/06/27818910396_39d46df053_o.jpg)

{kind=link}