This will be a short post, though I want to toss this question out to readers: what investment strategies do you know of that are simple, and work on average over the long-term?

Here are four (together with posts of mine on the topic):

I chose these because they are simple. ?Average people without a lot of training could do them. ?There are other things that work, but aren’t necessarily simple, like value investing, momentum investing, low volatility investing, and a few other things that I will think of after I hit the “Publish” button.

That said, most people don’t need to work on investing. ?They need to work on cash management, and I have written a small fleet of articles there. ?Managing cash is simple, but it takes self-control, and that is what most people lack in their financial lives.

But for those that have gotten their cash under control, with a full buffer fund, the above strategies will help, and they aren’t hard.

Final note: I realize valuations are high now, so buy-and-hold is not as attractive as at other times. ?I realize that interest rates are low, so bond ladders aren’t so great, seemingly. ?Indexing may be overused. ?Most?of the elements of the Permanent Portfolio look unappealing.

But what’s the alternative, and simple enough for average people to do? ?My answer is simple. ?If they can buy and hold, these strategies will pay off over time, and far better than those that panic when things get bad. ?There are few regularities in the markets more reliable than this.

The time that I?did a competitive study of the most aggressive life insurers, and how it did not dissuade my client’s management team from trying to imitate them.

With quotations and links to the source documents, I show what Ben Graham really said in the article commonly cited to say that he gave up on value investing.

The tech market washes out about every eight years or so.? The broad market, which is a more robust beast, washes out far less frequently.? My question: are these variants of the same phenomenon?

When do employee and corporate incentives line up?? Ideally, incentive schemes should reward people with a fraction of the additional profitability that resulted from the additional work that they did.? Difficulties: measurement impossible in many cases, people could receive a bonus when the firm is not profitable, neglects synergies (both positive and negative).

This is a small thing, and so this will be a small post.

Learn to set your expectations right.

When you buying something and see a price like $19, $19.95, or $19.99, think $20.

When you are buying a car, and see prices like $19,000, $19,900, $19,990, or $19,999, think $20,000. ?The same thing applies to homes, and be sure you have a strong estimate of all of the extra taxes and fees that will get thrown into the price.

People tend to look at the front number(s) and get mesmerized. ?Learn to round it up as a buyer. ?We tend to get too quick in our judgments, and be too optimistic when we buy, so round prices up — especially true if you are on a budget, and you are keeping a running total of costs.

Now, if you think this doesn’t happen in institutional pricing, it happens there as well. ?I remember cases where I was trying to sell bonds, and I could not get a deal done, I would ask my sales coverage, “Why? How is the other side pricing the bond?” ?If it was a dollar price like $100, I would make a note of it, and if the market fell for general reasons under that price, I would make an offer a little under the price, say $99.95. ?Frequently, I would sell?the bonds for my client, even if the yield spread had worsened in relative terms, and the bonds were less attractive to a more rational buyer. ?The same applied to other means of pricing bonds, and applied the opposite way if I was trying to buy bonds. ?You would be surprised how many were looking for a shiny price like $105, and after a general rally deals would get done at $105.01.

Buffett has sometimes had a phrase, “Your price, my terms.” ?If there are other facets to the deal than merely price, try giving the other guy his price in a prominent way, with other terms that favor what you want to achieve.

You would think that people would be more rational, but they are often not, and you and I aren’t much better. ?That is why I encourage you to think conservatively in your economic decisions to avoid undue optimism.

PS — remember that this happens with institutional investors in setting target prices as well — they like the glossy round numbers.

To my readers, for a little while, I am going to be doing some “best of” posts along with some smaller articles. ?You should see eleven “best of” articles before this is done. ?If this bugs you, just turn me off for a little while. ?These articles are important, because there are some re-publishers that mine these pieces for content, and sometimes translate highlighted articles into languages other than English.

This era probably had the greatest density of “Rules” posts. ?In my view, these were my best posts written between May and July?2013:

Thinking about the different streams of income in society, and which might be more likely to fail. ?Also, thoughts on how low interest rates fit into this picture.

On how life insurers compromise rules on reserving using reinsurers that they own as subsidiaries. ?Also examines other ways that insurers weaken solvency.

On how insurance has changed for investors over the past ten years, Price-to-Book vs Return on Equity Diagrams, and miscellaneous issues for those investing in insurance companies.

Really, it is not an insurable risk, which is why most companies underwriting LTC have lost money on it, and coverage has become less and less generous.

“As for those with long-term care policies, if they are old, keep paying on them, you will likely do well on them when you finally need to draw on the policies.? You have benefits that benefits that can no longer be purchased.? Enjoy the exclusive club you are in.”

“In summary, all news is not equal.? The reactions to news, and the lack thereof, can tell us a lot about the intentions of large market actors.? Do your homework well, and prosper off of the knowledge that it gives you regarding reactions, over-reactions, and under-reactions.”

The beginning of my arguments against the pointy-headed Financial Stability Oversight Commission [FSOC] and their inability to understand the solvency of non-bank financials.

It’s easier for a generation to become prosperous if they push the bills onto their children and grandchildren. ?Eventually it catches up with a nation, and reduces opportunity for average people.

There is probably money to be made in analyzing the foibles of money managers, to create new strategies by taking on the opposite of what they are doing.

The trouble with VAR and other mathematical models of risk is that if it becomes the dominant paradigm, and everyone begins to use it, it creates distortions in the market, because institutions gravitate to asset classes that the model makes to appear artificially cheap.? Then after a self-reinforcing cycle that boosts that now favored asset class to an unsupportable level, the cashflows underlying the asset can no longer support it, the market goes into reverse, and the VAR models encourage an undershoot.? The same factors that lead to buying to an unfair level also cause selling to an unfair level.

Benchmarking and risk control through VAR only work when few market participants use them.? When most people use them, it becomes like the portfolio insurance debacle of 1987.? VAR becomes pro-cyclical at that point.

“Unions create inefficiency.? This creates an opportunity for new technologies that perform the same function, but aren?t as labor-intensive.? (E.g. integrated steel vs. mini-mills)”

If businesses anticipate a flow of financing, they will depend on it.? Then a diminution or increase in the flow of investable funds will affect markets, even if the flow of investable funds remains positive or negative.

During a panic, it is useful to reflect on the degree to which the real economy has been driven by the financial economy.? In the Great Depression, the degree was heavy; in the seventies, it was light.? Today, my guess is that it is in-between, which makes it difficult to figure out the right strategy.

Market rents are typically fixed in size.? When a strategy to exploit a particular market inefficiency gets too big, returns to the rent disappear, or even go negative prospectively, even if they appear exceedingly productive retrospectively.

If an asset-backed security can produce a book return less than zero for reasons other than default, that asset-backed security should not be permitted as a reserve investment.

A somewhat humorous article of mistakes that I have made in job interviews. ?Also a comment on making sure that you fit the culture of the firm at which you are interviewing.

So you think that the market is overvalued? ?How do you adapt to that condition, while still leaving some room for opportunity if the market continues to rise.

I will admit, when I first read about the Permanent Portfolio in the late-80s, I was somewhat skeptical, but not totally dismissive.? Here is the classic Permanent Portfolio, equal proportions of:

S&P 500 stocks

The longest Treasury Bonds

Spot Gold

Money market funds

Think about Inflation, how do these assets do?

S&P 500 stocks ? mediocre to pretty good

The longest Treasury Bonds ? craters

Spot Gold ? soars

Money market funds ? keeps value, earns income

Think about Deflation, how do these assets do?

S&P 500 stocks ? pretty poor to pretty good

The longest Treasury Bonds ? soars

Spot Gold ? craters

Money market funds ? makes a modest amount, loses nothing

Long bonds and gold are volatile, but they are definitely negatively correlated in the long run.? The Permanent Portfolio concept attempts to balance the effects of inflation and deflation, and capture returns from the overshooting that these four asset classes do.

What did I do?

I got the returns data from 12/31/69 to 9/30/2011 on gold, T-bonds, T-bills, and stocks.? I created a hypothetical portfolio that started with 25% in each, rebalancing to 25% in each whenever an asset got to be more than 27.5% or less than 22.5% of the portfolio.? This was the only rebalancing strategy that I tested.? I did not do multiple tests and pick the best one, because that would induce more hindsight bias, where I torture the data to make it confess what I want.

I used a 10% band around 25% ( 22.5%-27.5%) figuring that it would rebalance the portfolio with moderate frequency.? Over the 566 months of the study, it rebalanced 102?times. ?At the top of this article is a graphical summary of the results.

The smooth-ish gold line in the middle is the Permanent Portfolio.? Frankly, I was surprised at how well it did.? It did so well, that I decided to ask, what if we drop out the T-bills in order to leverage the idea.? It improves the returns by 1%, but kicks up the 12-month drawdown by 7%.? Probably not a good tradeoff, but pretty amazing that it beats stocks with lower than bond drawdowns. ?That’s the light brown line.

Results

S&P TR

Bond TR

T-bill TR

Gold TR

PP TR

PP TR levered

Annualized Return

10.40%

8.38%

4.77%

7.82%

8.80%

9.93%

Max 12-mo drawdown

-43.32%

-22.66%

0.02%

-35.07%

-7.65%

-14.75%

Now the above calculations assume no fees.? If you decide to implement it using SPY, TLT, SHY and GLD, (or something similar) there will be some modest level of fees, and commission costs.

?What Could Go Wrong

Now, what could go wrong with an analysis like this?? The first point is that the history could be unusual, and not be indicative of the future.? What was unusual about the period 1970-2017?

Went off the gold standard; individual holding of gold legalized.

High level of gold appreciation was historically abnormal.

Deregulation of money markets allowed greater volatility in short-term rates.

ZIRP crushed money market rates.

Federal Reserve micro-management of short-term rates led to undue certainty in the markets over the efficacy of monetary policy ? ?The Great Moderation.?

Volcker era interest rates were abnormal, but necessary to squeeze out inflation.

Low long Treasury rates today are abnormal, partially due to fear, and abnormal Fed policy.

Thus it would be unusual to see a lot more performance out of long Treasuries. The stellar returns of the past can?t be repeated.

Three hard falls in the stock market 1973-4, 2000-2, 2007-9, each with a comeback.

By the end of the period, profit margins for stocks were abnormally high, and overvaluations are significant.

But maybe the way to view the abnormalities of the period as being ?tests? of the strategy.? If it can survive this many tests, perhaps it can survive the unknown tests of the future.

Other risks, however unlikely, include:

Holding gold could be made illegal again.

The T-bills and T-bonds have only one creditor, the US Government. Are there scenarios where they might default for political reasons?? I think in most scenarios bondholders get paid, but who can tell?

Stock markets can close for protracted periods of time; in principle, public corporations could be made illegal, as they are statutory creations.

The US as a society could become less creative & productive, leading to malaise in its markets. Think of how promising Argentina was 100 years ago.

But if risks this severe happen, almost no investment strategy will be any good.? If the US isn?t a desirable place to live, what other area of the world would be?? And how difficult would it be to transfer assets there?

Summary

The Permanent Portfolio strategy is about as promising as any that I have seen for preserving the value of assets through a wide number of macroeconomic scenarios.? The volatility is low enough that almost anyone could maintain it.? Finally, it?s pretty simple.? Makes me want to consider what sort of product could be made out of this.

I delayed on posting this for a while — the original work was done five years ago. ?In that time, there has been a decent amount of digital ink spilled on the Permanent Portfolio idea of Harry Browne’s. ?I have two pieces written:?Permanent Asset Allocation, and?Can the ?Permanent Portfolio? Work Today?

Part of the recent doubt on the concept has come from three sources:

Zero Interest rate policy [ZIRP] since late 2008, (6.8%/yr PP return)

The fall in Gold since late 2012 (2.7%/yr PP return), and

The fall in T-bonds in since mid-2016 (-4.7%?annualized PP return).

Out of 46 calendar years, the strategy makes money in 41 of them, and loses money in 5 with the losses being small: 1.0% (2008), 1.9% (1994), 2.2% (2013), 3.6% (2015), and 4.5% (1981). ?I don’t know about what other people think, but there might be a market for a strategy that loses ~2.6% 11% of the time, and makes 9%+?89% of the time.

Here’s the thing, though — just because it succeeded in the past does not mean it will in the future. ?There is a decent theory behind the Permanent Portfolio, but can it survive highly priced bonds and stocks? ?My guess is yes.

Scenarios: 1) inflation runs, and the Fed falls behind the curve — cash and gold do well, bonds tank, and stocks muddle. ?2) Growth stalls, and so does the Fed: bonds rally, cash and stocks muddle, and gold follows the course of inflation. 3) Growth runs, and the Fed swarms with hawks. Cash does well, and the rest muddle.

It’s hard, almost impossible to make them all do badly at the same time. ?They react differently to?changes in the macro-economy.

Upshot

There are a lot of modified permanent portfolio ideas out there, most of which have done worse than the pure strategy. ?This permanent portfolio strategy?would be relatively pure. ?I’m toying with the idea of a lower minimum ($25,000) separate account that would hold four funds and rebalance as stated above, with fees of 0.2% over the ETF fees. ?To minimize taxes, high cost tax lots would be sold first. ?My question is would there be interest for something like this? ?I would be using a better set of ETFs than the ones that I listed above.

I write this, knowing that I was disappointed when I started out with my equity management. ?Many indicated interest; few carried through. ?Small accounts and a low fee structure do not add up to a scalable model unless two things happen: 1) enough accounts want it, and 2) all reporting services are provided by Interactive Brokers.

Closing

Besides, anyone could do the rebalancing strategy. ?It’s not rocket science. ?There are enough decent ETFs to use. ?Would anyone truly want to pay 0.2%/yr on assets to have someone select the funds and do the rebalancing for him? ?I wouldn’t.

Information received since the Federal Open Market Committee met in December indicates that the labor market has continued to strengthen and that economic activity has continued to expand at a moderate pace.

Information received since the Federal Open Market Committee met in February indicates that the labor market has continued to strengthen and that economic activity has continued to expand at a moderate pace.

No real change.

Job gains remained solid and the unemployment rate stayed near its recent low.

Job gains remained solid and the unemployment rate was little changed in recent months.

No real change.

Household spending has continued to rise moderately while business fixed investment has remained soft.

Household spending has continued to rise moderately while business fixed investment appears to have firmed somewhat.

Shades up business fixed investment.

Measures of consumer and business sentiment have improved of late.

That sentence lasted for one statement.

Inflation increased in recent quarters but is still below the Committee’s 2 percent longer-run objective.

Inflation has increased in recent quarters, moving close to the Committee’s 2 percent longer-run objective; excluding energy and food prices, inflation was little changed and continued to run somewhat below 2 percent.

Shades their view of inflation up.

Excluding two categories that have had high though variable inflation rates is bogus. Use a trimmed mean or the median.

Market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance.

Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

No change. Any time they mention the ?statutory mandate,? it is to excuse bad policy. But don?t blame the Fed, blame Congress.

The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, labor market conditions will strengthen somewhat further, and inflation will rise to 2 percent over the medium term.

The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, labor market conditions will strengthen somewhat further, and inflation will stabilizearound 2 percent over the medium term.

Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

No change.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1/2 to 3/4 percent.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 3/4 to 1 percent.

Kicks the Fed Funds rate up ?%.

The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a return to 2 percent inflation.

The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

Suggests that they are waiting to see 2% inflation for a while before making changes.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation.

No change.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

No change.? Gives the FOMC flexibility in decision-making, because they really don?t know what matters, and whether they can truly do anything with monetary policy.

In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal.

The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal.

Now that inflation is 2%, they have to decide how much they are willing to let it run before they tighten with vigor.

The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

No change.? Says that they will go slowly, and react to new data.? Big surprises, those.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

No change.? Says it will keep reinvesting maturing proceeds of treasury, agency debt and MBS, which blunts any tightening.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Patrick Harker; Robert S. Kaplan; Neel Kashkari; Jerome H. Powell; and Daniel K. Tarullo.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Patrick Harker; Robert S. Kaplan; Jerome H. Powell; and Daniel K. Tarullo.

Large agreement.

Voting against the action was Neel Kashkari, who preferred at this meeting to maintain the existing target range for the federal funds rate.

Kashkari willing to be the lone dove amid rising inflation.? I wonder if he is thinking about systemic issues?

Comments

2% inflation arrives, and the FOMC tightens another notch.

They are probably behind the curve.

The economy is growing well now, and in general, those who want to work can find work.

The change of the FOMC?s view is that inflation is higher. Equities and bonds rise. Commodity prices rise and the dollar weakens.

The FOMC says that any future change to policy is contingent on almost everything.

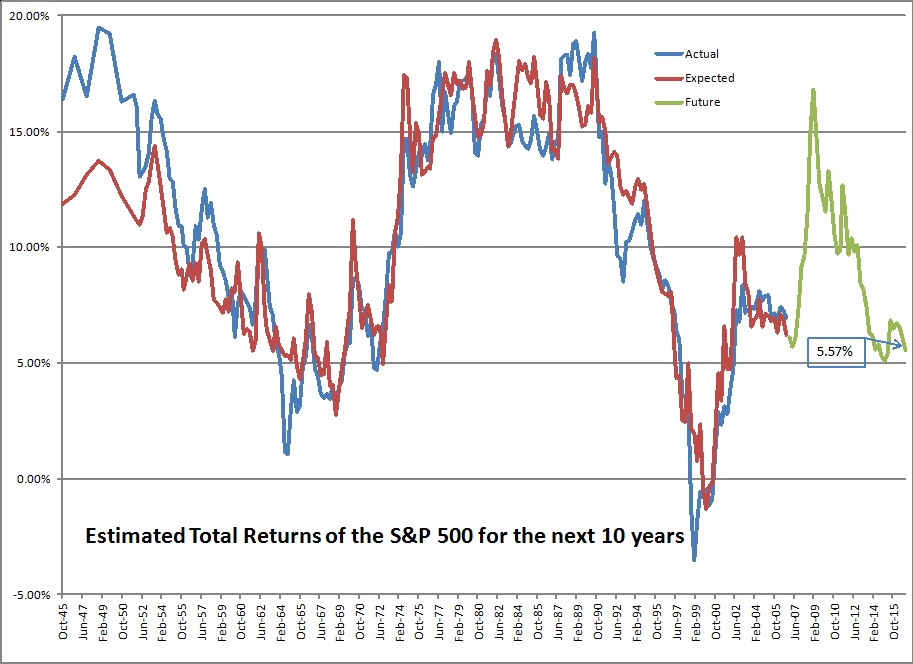

Are you ready to earn 6%/year until 9/30/2026? ?The data from the Federal Reserve comes out with some delay. ?If I had it instantly at the close of the third quarter, I would have said 6.37% ? but with the run-up in prices since then, the returns decline to 6.01%/year.

So now I say:

Are you ready to earn 5%/year until 12/31/2026? ?The data from the Federal Reserve comes out with some delay. ?If I had it instantly at the close of the fourth?quarter, I would have said 5.57% ? but with the run-up in prices since then, the returns decline to 5.02%/year.

A one percent drop is pretty significant. ?It stems from one main factor, though — investors are allocating a larger percentage of their total net worth to stocks. ?The amount in stocks moved from 38.00% to 38.75%, and is probably higher now. ?Remember that these figures come out with a 10-week delay.

Remember that the measure in question covers both public and private equities, and is market value to the extent that it can be, and “fair value” where it can’t. ?Bonds and most other assets tend to be a little easier to estimate.

So what does it mean for the ratio to move up from 38.00% to 38.75%? ?Well, it can mean that equities have appreciated, which they have. ?But corporations buy back stock, pay dividends, get acquired for cash which reduces the amount of stock outstanding, and places more cash in the hands of investors. ?More cash in the hands of investors means more buying power, and that gets used by many long-term institutional investors who have fixed mandates to follow. ?Gotta buy more if you hit the low end of your equity allocation.

And the opposite is true if new money gets put into businesses, whether through private equity, Public IPOs, etc. ?One of the reasons this ratio went so high in 1998-2001 was the high rate of business formation. ?People placed more money at risk as they thought they could strike it rich in the Dot-Com bubble. ?The same was true of the Go-Go era in the late 1960s.

Remember here, that average returns are around 9.5%/year historically. ?To be at 5.02% places us in the 88th percentile of valuations. ?Also note that I will hedge what I can if expected 10-year returns get down to 3%/year, which corresponds to a ratio of 42.4% in stocks, and the 95th percentile of valuations. ?(Note, all figures in this piece are nominal, not inflation-adjusted.) ?At that level, past 10-year returns in the equity markets have been less than 1%, and in the short-to-intermediate run, quite poor.)

You can also note that short-term and 10-year Treasury yields have risen, lowering the valuation advantage versus cash and bonds.

The investors? positioning suggests burgeoning optimism, with TD Ameritrade clients increasing their net exposure to stocks in February, buying bank shares and popular stocks such as Amazon.com Inc. and sending the retail brokerage?s Investor Movement Index to a fresh high in data going back to 2010. The index tracks investors? exposure to stocks and bonds to gauge their sentiment.

?People went toe in the water, knee in the water and now many are probably above the waist for the first time,? said JJ Kinahan, chief market strategist at TD Ameritrade.

This is sad to say, but it is rare for a rally to end before the “dumb money” shows up in size. ?Running a small asset management shop like I do, at times like this I suggest to clients that they might want more bonds (with me that’s short and high quality now), but few do that. ?Asset allocation is the choice of my clients, not me. ?That said, most of my clients are long-term investors like me, for which I give them kudos.

Then there is this piece over at Bloomberg.com called:?Wall Street’s Buzz Over ‘Great Leader’ Trump Gives Shiller Dot-Com Deja Vu. ?I want to see the next data point in this analysis, which won’t be available by mid-June, but I do think a lot of the rally can be chalked up to willingness to take more risk.

I do think that most people and corporations think that they will have a more profitable time under Trump rather than Obama. ?That said, a lot of the advantage gets erased by a higher cost of debt capital, which is partly driven by the Fed, and partly by a potentially humongous deficit. ?As I have said before though, politicians are typically limited in what they can do. ?(And the few unlimited ones are typically destructive.)

Shiller’s position is driven at least partly by the weak CAPE model, and the rest by his interpretation of current events. ?I don’t make much out of policy uncertainty indices, which are too new. ?The VIX is low, but hey, it usually is when the market is near new highs. ?Bull markets run on complacency. ?Bear markets plunge on revealed credit risk threatening economic weakness.

One place I will agree with Shiller:

What Shiller will say now is that he?s refrained from adding to his own U.S. stock positions, emphasizing overseas markets instead.

That is what I am doing. ?Where I part ways with Shiller for now is that I am not pressing the panic button. ?Valuations are high, but not so high that I want to hedge or sell.

That’s all for now. ?This series of posts generates more questions than most, so feel free to ask away in the comments section, or send me an email. ?I will try to answer the best questions.

=========================

Late edit: changed bolded statement above from third to fourth quarter.

I wrote this to summarize my thoughts from a chat session that I was able to participate in at Thompson Reuters Global Markets Forum yesterday.? It was wider ranging than this, but was a very enjoyable time.? Thanks to Manoj Rawal for inviting me.

On the Pursuit of Economic Growth

I think one of the conceits of the modern era is the degree of trust we place in governments.? We want them to do everything for us.? The truth is that their power is limited.? Even if we delegate more power to them, that doesn?t mean the power can/will be used by the government for the purposes intended.

The government is composed of people with their own goals.? It?s not much different than shareholders delegating power of the corporation to a board of directors, who collectively oversee management, should they care to do so.? Often delegated power gets misdirected for the ends of the power- and money-hungry.

Who watches the watchers?? It is one reason why we have ?rule of law? in many republics ? there is law that governs the government, if we have the will to maintain that.? It differs from ?rule by law? which exists more commonly on Earth ? laws exist so that the rulers can maintain their rule over those they rule ? of which China is an excellent example.? Freedom that is good for the interests of the Communist Party is allowed to exist, but not other freedoms.? There are no rights that are God-given, not subject to the dictates of governments.

Sorry for the digression ? my main point is that even the most powerful governments get bogged down, and can?t do nearly what people imagine they can do.? It is akin to what Peter Drucker said on management, that where managers proliferate, it takes progressive more people to manage all of the people ? you might actually be able to get more done with fewer people.

Governments face another constraint ? because people think the government can stimulate the economy, we have had governments stretch past their budgetary limits, borrow a lot of money, and make long-dated promises that they can?t keep.? This is not just a US phenomenon.? This is happening globally.? It is rare, possibly even non-existent to find countries that run balanced budgets, have sound monetary policy, and haven?t overpromised on entitlements.

As such, there isn?t that much that governments can do in terms of discretionary spending.? Even when they do allocate money, most projects of any significance don?t produce immediate results, but take years to start and more years to complete.? China may be able to run roughshod over its citizens, but where rule of law exists, there is necessary delay for most projects.? Obama or Trump can long for ?shovel ready? projects.? They don?t exist, at least not many of them exist that are sizable.

As such, when I look at the plans of Donald Trump, I don?t give them a lot of weight in investment decisions that I make.? The same goes for any US or foreign leader, central banker, or whatever.? Short of starting a war, the amount of truly impactful things he can do is limited, especially for overly indebted governments.

What does matter then?? I think culture matters a lot.? Here are some questions to think about:

What priority do we place on taking risk?

How do you balance the competing needs of creditors and debtors?

How easy is it to start a business?

How do we feel about people using natural resources for profit?

How predictable is government policy, so that people can make long-term plans, and not worry about whether they will be able to see those plans to their fruition or not?

Does the culture protect private property?

Do we encourage men and women to marry, start families, and raise intelligent children?

Do we encourage charitable endeavors, so that effective help can be given to those who genuinely want to escape poverty? (rather than perpetuate it through continual handouts?)

How much do we play favorites across and within industries?

To what degree do we force uneconomic growth objectives through tax incentives, such as owning a home, rather than renting?

How much are we willing to allow technology to eliminate jobs, such that labor is directed away from simple tasks to tasks of higher complexity?

It is my opinion that those are the greater drivers of economic growth, and that the government can do little to foster growth, aside from having simple long-term policies, and letting us get on with being productive.

As such, I don?t see a lot going on right now that should promote higher growth.? Note that high growth is not necessary for a strong stock market, but it is necessary if you want to see ordinary laborers benefit in society.

This post may fall into the “Dog bites Man” bucket, but I will see if I can’t shed a little more light on the phenomenon. ?Here’s the question: “When do we see new highs in the stock market most often?” ?The punchline: “After a recent new high.”

The red squares above show the probability of hitting a new high so many days after a new high. ?The black line near it is a best fit power curve. ?The blue diamonds?above show the probability of hitting a new high so many days after not hitting a new high. ?The green triangles?above show the ratio of those two probabilities, matching up against the right vertical axis. The black line near it is a best fit power curve.

As time goes to infinity, both probabilities converge to the same number, which is presently estimated to be 6.8%, the odds that we would hit a new high on any day between 1951 and 2015. ?Here’s the table that corresponds to the above graph:

Probability of a new high after

Days after no new high

Days after new high

Probability Ratio

1st day

3.1%

57.3%

18.29

2nd day

4.2%

43.3%

10.39

3rd day

4.6%

36.7%

7.90

4th day

4.8%

33.8%

6.99

5th day

5.1%

30.0%

5.87

6th day

5.2%

28.2%

5.37

7th day

5.5%

24.2%

4.36

8th day

5.7%

22.5%

3.97

9th day

5.6%

23.4%

4.18

10th day

5.6%

22.6%

4.00

11-15

5.9%

19.0%

3.22

16-20

6.0%

17.2%

2.86

21-30

6.1%

16.4%

2.71

31-40

6.2%

14.5%

2.35

41-50

6.2%

15.2%

2.47

51-60

6.3%

14.2%

2.28

61-75

6.3%

13.9%

2.21

76-90

6.3%

13.6%

2.16

91-105

6.3%

12.8%

2.02

106-120

6.4%

12.5%

1.96

121-140

6.4%

12.0%

1.87

141-160

6.5%

11.3%

1.75

161-180

6.4%

11.5%

1.79

181-200 days

6.4%

11.8%

1.84

E.g., as you go down the table the probability 43.3% represents the probability that you get a new high?on the second day after a new high.

Here’s an intuitive way to think about it: if you are not at a new high, you are further away from a new high than if you were at a new high recently. ?Thus with time the daily probability of hitting a new high gets higher. ?If you were at a new high recently, you daily odds of hitting a new high are quite high, but fall over time, because?the odds of drifting lower at some point increase. ?Valuation is a weak daily force, but a strong ultimate force.

That said, the odds of hitting new highs a long time away from a new high are significantly higher than the odds of hitting a new high where there has been no new high for the same amount of time.

Closing Thoughts

I could segment the data another way, and this could be clearer: If you are x% away from a new high, what is?the odds you will hit a new high n days from now? ?As x gets bigger, so will the numbers for n. ?Be that as it may, when you have had new highs recently, you tend to have more of them. ?New highs clump together.

The same is true of periods with no new highs — they tend to clump together and persist even more.

Valuation and momentum are hidden variables here — momentum aids persistence, and valuation is gravity, eventually causing markets that don’t fairly price likely future cash flows to revert to pricing that is more normal. ?Valuation is powerful, but takes a long while to act, often waiting for a credit cycle to do its work. ?Momentum works in the short-run, propelling markets to heights and depths that we can only reach from human mimickry.

I didn’t originate this rule, and I am not sure who did. ?I learned it at Provident Mutual from the Senior Executives of Pension Division when I worked there in the mid-’90s. ?There is a broader rule behind it that I will get to in a moment, but first I want to explain this.

There are many efforts in business, particularly in sales, where some?want to hide what they are truly making, so that they can make an above average income off of the unsuspecting. ?At the Pension Division of Provident Mutual, the sales chain worked like this: our representatives would try to sell our investment products to pension plans, both municipal and corporate. ?We preferred going direct if we could, but often there would be some fellow who had ingratiated himself with the plan sponsor, perhaps by providing other services to the pension plan, and he would become a gateway to the pension plan. ?His recommendation would play a large role in whether we made the sale or not.

Naturally, he wanted a commission. ?That’s where the rule came in, and from what I?remember at the time, many companies similar to us did not play by the rule. ?When the sale was made, the client would see a breakdown of what he was going to be charged. ?If we were paying disclosed compensation to the “gatekeeper,” we would point it out and mention that that was *all* the gatekeeper was making. ?If the compensation was not disclosed, the client would see the bottom line total charge, and he would have to evaluate if that was good or bad deal for plan participants.

Our logic was this: the plan sponsor would have to analyze the total cost anyway for a bundled service against other possible bundled and unbundled services. ?We would bundle or unbundle, depending on what the gatekeeper and client wanted. ?If either wanted everything spelled out we would do it. If neither wanted it spelled out, we would only provide the bottom line.

What we would never do is provide a breakdown that was incomplete, hiding the amount that the gatekeeper was truly earning, such that client would see the disclosed compensation, and think that it was the entire compensation of the gatekeeper.

We were the smallest player in the industry as far as life insurers went, but we were more profitable than our peers, and growing faster also. ?Our business retention was better because compensation surprises did not rise up to bite us, among other reasons.

Here’s the broader rule:

“Don’t be a Pig.”

Some of us?had a saying in the Pension Division, “We’re the good guys. ?We are trying to save the world for a gross margin of 0.25%/year on assets, plus postage and handling.” ?Given that what we did had almost no capital requirements, that was pretty good.

Most scandals over pricing involve some type of hiding. ?Consider the pricing of pharmaceuticals. ?Given the opaqueness is difficult to tell who is making what. ?Here is another?article on the same topic?from the past week.

In situations like this, it is better to take the high road, and make make your pricing more transparent than your competitors, if not totally transparent. ?In this world where so much data is shared, it is only a matter of time before someone connects the dots on what is hidden. ?Or, one farsighted competitor (usually the low cost provider) decides to lay it bare, and begins winning business, cutting into your margins.

I’ll give you an example from my own industry. ?My fees may not be the lowest, but they are totally transparent. ?The only money I make comes from a simple assets under management fee. ?I don’t take soft dollars. ?I make money off of asset management that is?aligned with what I myself own. ?(50%+ of my total assets and 80%+ of my liquid assets are invested exactly the same as my clients.)

Why should I muck that up to make a pittance more? ?It’s a nice model; one that is easy to defend to the regulators, and explain to clients.

We probably would not have the fuss over the fiduciary rule if total and prominent disclosure of fees were done. ?That said, how would the brokers have lived under total transparency? ?How would life insurance salesmen live? ?They would still live, but there would be fewer of them, and they would probably provide more services to justify their compensation.

Even as a bond trader, I learned not to overpress my edge. ?I did not want to do “one amazing trade,” leaving the other side wounded. ?I wanted a stream of “pretty good” trades. ?An occasional tip to a broker that did not know what he was doing would make a “friend for life,” which on Wall Street could last at least a month!

You only get one reputation. ?As Buffett said to the Subcommittee on Telecommunications and Finance of the Energy and Commerce Committee of the U.S. House of Representatives back in 1991 regarding Salomon Brothers:

I want the right words and I want the full range of internal controls. But I also have asked every Salomon employee to be his or her own compliance officer. After they first obey all rules, I then want employees to ask themselves whether they are willing to have any contemplated act appear the next day on the front page of their local paper, to be read by their spouses, children, and friends, with the reporting done by an informed and critical reporter. If they follow this test, they need not fear my other message to them: Lose money for the firm, and I will be understanding; lose a shred of reputation for the firm, and I will be ruthless.

This is a smell test much like the Golden Rule. ?As Jesus said, “Therefore, whatever you want men to do to you, do also to them, for this is the Law and the Prophets.” (Matthew 7:12)

That said, Buffett’s rule has more immediate teeth (if the CEO means it, and Buffett did), and will probably get more people to comply than God who only threatens the Last Judgment, which seems so far away. ?But I digress.

Many industries today are having their pricing increasingly disclosed by everything that is revealed on the Internet. ?In many cases, clients are asking for a greater justification of what is charged, or, are looking to do price and quality comparison where they could not do so previously, because they did not have the data.

Whether in financial product prices, healthcare prices, or other places where pricing has been bundled and secretive, the ability to hide is diminishing. ?For those who do hide their pricing, I will offer you one final selfish argument as to why you should change: given present trends, in the long-run, you are fighting a losing battle. ?Better to earn less per sale with happier clients, than to rip off clients now, and lose then forever, together with your reputation.

{kind=link}