I bought an inexpensive car a couple of days ago, a 2009 Toyota Corolla with 19,700 miles on it. ?It’s in almost perfect condition. ?I paid ~$10,300 in cash to get it, inclusive of tax and tags.

Sound like a good deal? ?I think so, but let me give you the negatives:

Only one key, and no manual.

I had to spend some extra time looking for it, and had to travel 50+ miles twice to get it. ?(And a third time to get permanent plates…)

The vehicle was previously a total loss, as its front end was badly mangled in an accident. ?Thus, it only has a salvage title, which limits the ability to finance the vehicle — few banks will lend against it. ?That doesn’t affect me, but it might affect others.

Also, if?it gets wrecked, selling and re-titling a vehicle with a salvage title can be problematic. ?(Not that I expect that, but in 2007, I had a car totaled that was parked in front of my house, mostly on my yard.)

I had to wait for it to be repaired.

But on the plus side:

I traded away an older vehicle to a family that needed a large 15-seat van, at a price that helped them.

My auto insurance costs have gone down.

Gas mileage has gone up.

I’ve bought three vehicles from this niche dealer before, and they have all worked out well. ?He selectively buys Toyotas and Hondas at auto auctions that have been deemed total wrecks by insurers, after analyzing them to see what it would take to make them as good as new. ?Then he fixes and sells them; that’s all he does.

Because I’ve bought from this fellow before, when he heard I was in the market for a car, he mentioned that he had one car he had not listed yet — the one I bought. ?All of his deals are good, but this one more so. ?I’m flexible about what I drive, and so I’m happy to get a car in good condition for a good price.

Now, most of my readers don’t live in the DC area, so this won’t be so relevant to most of you. ?You might not have a niche dealer in your area doing something similar, assuming that you can live with the disadvantages, and get comfortable with the quality of the repaired vehicle.

This does point up the idea of going off the beaten track, and looking non-conventionally for a car, which is a decent-sized expense for most people. ?Flexibility helps. ?I look for cars that have good repair records on average, and am not wedded to any particular style. ?I think that older cars with relatively few miles are at present a niche that few actively target to purchase. ?Pricing models break down for them, because they are rare, almost all of them have a story behind them, and many people don’t like driving older cars, even if they are in very good condition.

You may have a better way of finding cars than I do — if you do, feel free to share it below in the comments. ?As it is, I’m not really a writer on personal finance, so this is a rare article that may help you practically in buying a car. ?A few final points:

Befriend someone trustworthy who knows cars well, and is willing to help you. ?People who love cars often like helping others find a good deal.

When you find someone who offers unusual value, stick with him.

Be flexible. ?I’ve known a lot of people who have paid a lot more than they needed to for what my father called, “Fancy Rolling Stock.”

Consider total costs of ownership. ?Older cars don’t need collision insurance. ?Some makes and models wear better than others, so repair costs could be lower for those cars. ?Analyze likely fuel efficiency.

Finally, if you have a deal that is?pretty good, be happy with it. ?Don’t overspend time looking for the absolute best deal. ?In my opinion,?the best is elusive, you can never truly know if you have it, and pretty good is attainable. ?And that is true for more than just buying cars — don’t let perfection become the enemy of the pretty good. ?(Shall I write about that for investment analysis? ?When do we ever get to certainty?…)

Recently I was approached by Moneytips to ask my opinions about retirement. They sent me a long survey of which I picked a number of questions to answer. You can get the benefits of the efforts of those writing on this topic today in a free e-book, which is located here: http://www.moneytips.com/retiree-next-door-ebook.??The eBook will be available free of charge?through September 30th. ?I have a few quotes in the eBook.

Before I move onto the answers, I would like to share with you an overview regarding retirement, and why current and future generations are unlikely to enjoy it to the degree that the generations prior to the Baby Boomers did.

The first thing to remember is that retirement is a modern concept. That the world existed without retirement for over 5000 years may mean that it is not a necessary institution. For a detailed comment on this, please consult my article, “The Retirement Tripod: Ancient and Modern.” Here’s a quick summary:

In the old days, when people got old, they worked a reduced pace. They relied on their children to help them. Finally, they relied on savings.

Savings is the difficult concept. How does one save, such that what is set aside retains its value, or even grows in value?

If you go backwards 150 years or further in time, there weren’t that many ways to save. You could set aside precious metals, at the risk of them being stolen. You could also invest in land, farm animals, and tools, each of which would be the degree of maintenance and protection in order to retain their value. To the extent that businesses existed, they were highly personal and difficult to realize value from in a sale. Most businesses and farms were passed on to their children, or dissolved at the death of the proprietor.

In the modern world we have more options for when we get old ? at least, it seems like we have more options. In retirement, we have three ways to support ourselves: we have government security programs, corporate security programs, and personal savings.

Think of this a different way, and ignore markets for a moment.? How do we take care of those that do not work in society?? Resources must be diverted from those that do work, directly or indirectly, or, we don?t take care of some that do not work.

Back to?markets: Social Security derives its ways of supporting those that no longer work from the wages of those that do work.? That?s one reason to watch the ratio of workers to retired.? When that ratio gets too low, the system won?t work, no matter what.? The same applies to Medicare.? With a population where growth is slowing, the ratio will get lower. If the working population is shrinking, there is no way that benefits for those retiring will be maintained.

Pensions tap a different sort of funding.? They tap the profit and debt servicing streams of corporations and other entities.? Indirectly, they sometimes tap the taxpayer, because of the Pension Benefit Guaranty Corporation, which guarantees defined benefit pensions up to a limit.? There is no explicit taxpayer backstop, but in this era of bailouts, who can tell what will be guaranteed by the government in a crisis?

That said, not many people today have access to Defined-Benefit pensions. Those are typically the province of government workers and well-funded corporations. That leaves savings as the major way that most people fund retirement aside from Social Security.

One of the reasons why the present generations are less secure than prior generations with respect retirement is that the forebears who originally set up defined-benefit pensions and Social Security system set up in such a way that they gave benefits that were too generous to early participants, defrauding those who would come later. Though the baby boomers are not blameless here, it is their parents that are the most blameworthy. If I could go back in time and set things right, I would’ve set the defined-benefit pension funding rules to set aside considerably more assets so that funding levels would’ve been adequate, and not subject to termination as the labor force aged.

I also would’ve required the US government to set benefits at a level equal to that contributed by each generation, and given no subsidy to the generations at the beginning of the system. Truth, I would eliminate the Social Security system and Medicare if I could. I think it is a bad idea to have collective support programs. There are many reasons for that, but a leading reason is that it removes the incentive to marry and have children. Another reason is that it politicizes generational affairs, which will become obvious to the average US citizen over the next 10 to 15 years.

Back to Savings

As for personal savings today we have more options than our great-great-great-grandparents did 150 years ago. We can still buy land and we can still store precious metals ? both of those have a great ability to retain value. But, we can buy shares in businesses and we can buy the debt claims of others. We can also build businesses which we can sell to other people in order to fund our retirement.

But investing is tricky. With respect to lending, default is a significant risk. Also, at the end of the term of lending, what will the money be worth? We have to be aware of the risks of inflation and deflation.

In evaluating businesses more generally, it is difficult to determine what is a fair price to pay. In a time of technological change, what businesses will survive? Will the business managers be clever enough to make the right changes such that the business thrives?

You have an advantage that your parents did not have, though. You can invest in the average business and debt of public companies in the US, and around the world through index funds. This is not foolproof; in fact, this is a pretty new idea that has not been tested out. But at least this offers the capability of opening a fraction of the productive assets in our world, diversified in such a way that it would be difficult that you end up with nothing, unless the governments of the world steal from the custodians of the assets.

With that, I leave you to read my answers to some of the questions that were posed to me regarding retirement:

What is a safe withdrawal rate?

A safe withdrawal rate is the lesser of the yield on the 10 year treasury +1%, or 7%. The long-term increase in value of assets is roughly proportional to something a little higher than where the US government can borrow for 10 years. That’s the reason for the formula. Capping it at 7% is there because if rates get really high, people feel uncomfortable taking so much from their assets when their present value is diminished.

How should you handle a significant financial windfall?

If you have debt, and that debt is at interest rates higher than the 10 year treasury yield +2%, you should use the windfall to reduce your debt. If the windfall is still greater than that, treat it as an endowment fund, invest it wisely, and only take money out via the safe withdrawal rate formula.

What are some ways to learn to embrace frugality?

This is a question of the heart. You have to master your desires to have goods and services today that are discretionary in nature. Life is not about happiness in the short term but happiness and long-term. Embrace the concept of deferred gratification that your great-grandparents did and recognize that work and savings provide for a secure and happy future.

How can the average worker start earning passive income?

Passive income is a shibboleth. People look at that as a substitute for investing, because they can’t control investment returns, and they think they can control income.

Income comes from debt or a business. If from debt, it is subject to prepayment or default; it is not certain. Also, income that comes from debt is typically fixed. That income may be sufficient today, but it may not be so if inflation rises. Also your capital is tied up until the debt matures. When the debt matures, reinvestment opportunities may be better or worse than they were when you started.

If income comes from a business, it is subject to all the randomness of that business; it is not certain. It is subject to all of the same problems that an investment in the stock market is subject to, except that you have to oversee the business.

There is no such thing as a truly passive income. Get used to the fact that you will be investing and working to earn an income.

What can those workers who are not employed by a large company or the public sector do to maximize their retirement savings?

You can start an IRA. Until the rules change, you can create healthcare savings account, not use it, and let it accrue tax-free until you’re 59 1/2. Oh, you get an immediate income deduction for that too.

If you are a little more enterprising, you can start your own business. If your business succeeds, there are a lot of ways to put together a pension, deferring more income than an individual can. By the time you get there, the rules will have changed, so I won’t tell you how to do it today; at the time, get a good pension consultant.

Why is calculating how much you’ll need for retirement an important exercise?

You have to understand that retirement is a new concept. In the ancient world, retirement meant continued work at a slower pace on your farm, living off of savings (what little was storable then ? gold, silver, etc.), and help from your children whom you helped previously as you raised them.

Today’s society is far more personal, far less family centered, and far more reliant on corporate and governmental structures. Few of us produce most of the goods and services that we need. We rely on the division of labor to do this.? Older people will still rely on younger people to deliver goods and services, as the older people hand over their accumulated assets in exchange for that.

Practically, modern retirement is an exercise in compromise. You will have to trade off:

How long you will work

At what you will work

What corporate and governmental income plans you participate in

How much income with safety your assets can deliver, with an allowance for inflation

How much you will help your children

How much your children will help you

As such, calculating a simple figure how much your assets should be may be useful, but that one variable is not enough to help you figure out how you should conduct your retirement.

Why don’t more people consult investment professionals? What keeps them from doing so?

There are two reasons: first, most people don’t have enough income or assets for investment professionals to have value to them. Second, people don’t understand what investment professionals can do for them, which is:

They can keep you from panicking or getting greedy

They can find ways to reduce your tax burdens

They can diversify your assets so that you are less subject to large drawdowns in the value of your assets

Other than maximizing your annual contribution, what other things can you do to get the most out of your IRA and 401(k)?

Diversify your investments into safe and risky buckets. The safe bucket should contain high quality bonds. The risky bucket should contain stocks, tilted toward value investing, and smaller stocks. New contributions should mostly feed investments that have been doing less well, because investments tend to mean-revert.

Stocks are clearly risky and investors have emotional reactions to that. How can investors rationally manage their stock investments so that they are less likely to regret their decisions?

When I was a young investor, I had to learn not to panic. I also had to learn not to get greedy. That means tuning out the news, and focusing on the long run. That may mean not looking at your financial statements so frequently.

As for me as a financial professional, I look at the assets that I manage for my clients and me every day, but I have rules that limit trading. I do almost all trading once per quarter, at mid-quarter, when the market tends to be sleepy, and not a lot of news is coming out. When I trade, I am making business decisions that reflect my long-term estimates of business prospects.

Closing

And if that is not enough for you, please consult my piece The Retirement Bubble. ?You can retire if you put enough away for it, but it is an awful lot of money given that present investments yield so little.

The dirty truth is that some investments in this life are sold, and not bought. ?The prime reason for this is that many people are not willing to learn enough to save and invest on their own. ?Instead, they rely on others to corral them and say, “You ought to be saving and investing. ?Hey, I’ve got just the thing for you!”

That thing could be:

Life Insurance

Annuities

Front-end loaded mutual funds

Illiquid securities like Private REITs, LPs, some Structured Notes

Etc.

Perhaps the minimal effort necessary to avoid this is to seek out a fee-only financial planner, and ask him to set up a plan for you. ?Problem solved, unless…

Unless the amount you have is so small that when look at the size of the financial planner’s fee, you say, “That doesn’t work for me.”

But if you won’t do it yourself, and you can’t find something affordable, then the only one that will help you (in his own way) is a commissioned salesman.

Now, to generate any significant commission off of a financial product, there have to be two factors in place: 1) the product must be long duration, and 2) it must be illiquid. ?By illiquid, I mean that either you can’t easily trade it, or there is some surrender charge that gets taken out if the contract is cashed out early.

The long duration of the contract allows the issuer of the contract the ability to take a portion of its gross margins over life of the contract, and pay a large one-time commission to the salesman. ?The issuer takes no loss as it pays the commission, because they spread the acquisition cost over the life of the contract. ?The issuer can do it because it has set up ways of recovering the acquisition cost in almost all circumstances.

Now in some cases, the statements that the investor will get will?explicitly reveal the commission, but that is rare. ?Nonetheless, to the extent that it is required, the first statement will?reveal how much the contractholder would lose if he tries to cash out early. ?(I think this happens most of the time now, but it would not surprise me to find some contract where that does not apply.)

Now the product may or may not be what the person buying it needed, but that’s what he?gets for not taking control of his?own finances. ?I don’t begrudge the salesman his commission, but I do want to encourage readers to put their own best interests first and either:

Learn enough so that you can take care of your own finances, or

Hire a fee-only planner to build a financial plan for you.

That will immunize you from financial salesmen, unless you eventually become rich enough to use life insurance, trusts, and other instruments to limit your taxation in life and death.

Now, I left out one thing — there are still brokers out there that make their money through lots of smallish commissions by trading a brokerage account of yours aggressively, or try to sell you some of the above products. ?Avoid them, and?let your fee-only planner set up a portfolio of low cost ETFs for you. ?It’s not sexy, but it will do better than aggressive trading. ?After all, you don’t make money while you trade; you make it while you wait.

If you don’t have a fee only planner and still want to index — use half SPY and half AGG, and add funds periodically to keep the positions equal sized. ?It will never be the best portfolio, but over time it will do better than the average account.

One final note before I go: with insurance, if you want to keep your costs down, keep your products simple — use term insurance for protection, and simple deferred annuities for saving (though I would buy a bond ETF rather than insurance in most cases). ?Commissions go up with product complexity, and so do expenses. ?Simple products are easy to compare, so that you know that you are getting the best deal. ?Unless you are wealthy, and are trying to achieve tax savings via the complexity, opt for simple insurance products that will cover basic needs. ?(Also avoid product riders — they are really expensive, even though the additional premiums are low, the likely benefits paid are lower still.)

I’m sure a lot of people have already told you but I want to tell you anyway: Your blog is awesome! I came across The Aleph Blog a couple of months ago and I?m very impressed with your content. I particularly like that 4-part article on Using Investment Advice. I am in the financial industry myself and it makes me wish I came up with the kind of ideas that you have on your blog. Awesome stuff!

Keep up the good work,

Many thanks to the reader, and if you want to read that series, it is located here. ?But when I considered what he wrote to me, it made me think, “Why do we have to tell people how to think about investment advice?”

Then it hit me: because people are looking for easy tips to execute. ?After all, when I wrote the 4-piece series, I had?listening to Jim Cramer in mind. ?The ?tip culture? of inexperienced investors don?t want to learn the ideas behind investing, but just want someone to say, ?Buy this.?? There is little if any guarantee that the same pundit?will ever update his opinion.

We see this on the web, in magazines, newsletters, newspapers, etc. ?On rare occasion, I will print one out, and add it to my “delayed research stack” which means I will look at it in 1-3 months. ?I just did my quarterly clean-out a few days ago — anything I add to the stack now will wait until November.

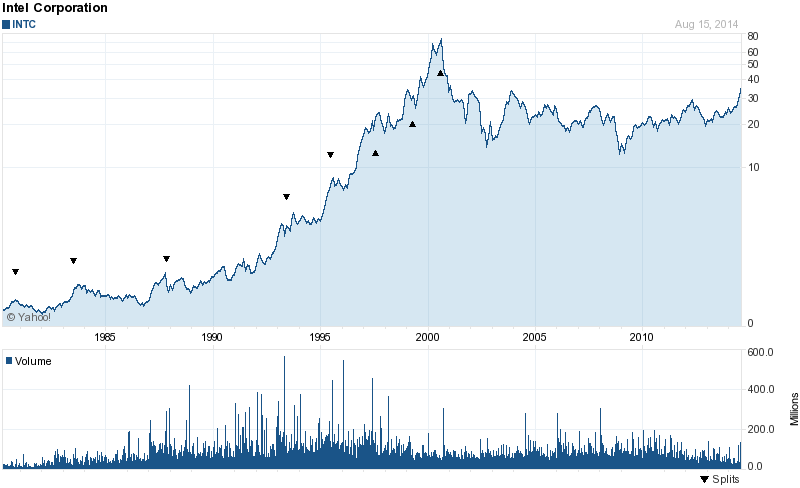

But why read articles like, “Ten Undervalued Large Cap Stocks with Growth Potential,” “Nine Stocks to Buy and Hold Forever,” “Eight Stocks that are Taking Off, Don’t Miss Out,” “Seven Hidden Gens Among Small Caps,” “Six Stocks for Income and Growth,” “Five Energy Stocks that are Poised to Surge,” Four Titanic Stocks that Every Investor Should Own,” “Three Turnaround Stocks with Potential for Large Capital Gains,” “Two Stocks with Breakthrough Technologies,” and “The One Stock that You Should Own for the Next Decade.”

Now, I made those titles up, though the last one was based off a Smart Money article on Intel in late 1999 which came very close to top-ticking ?the market. ?As you can see, Intel still hasn’t made it back to the tech bubble peak.

As I Googled phrases like, “Ten Best Stocks,” it was fascinating to see the range of pitches employed:

Appeals to Buffett (that never gets old)

Best stocks for this year

Favorite stocks of an author, manager or publication

With high dividends

With a low price

In emerging markets

That won’t lose money

That our patented investment screener spat out

For the rest of your life

Etc.

I know that I could get a lot more readers with list articles that tout stocks. ?I don’t do it because most of the articles that you read like that are bogus. ?[I also don’t want the inevitable scad of complaints that come with the territory.) ?So why do such articles?draw readers?

People would rather have false certainty than live in the reality that choosing good investments is difficult. ?Even very good investors hit rough patches where they do not outperform. ?Also, people aren’t comfortable with uncertain horizons for realizing value in investments — article tout holding forever, ten years, one year, but rarely 3-5 years or a market cycle.

The truth is, you can’t tell when a stock will perform, but when it does perform, the results will be lumpy. ?The performance of a stock is rarely smooth. ?During times when the success or failure of a stock idea is realized, the moves are often violent.

Now remember, those who write such articles are looking for media revenue — such articles are sensational, and pander to the desire for easy money. ?But where are the articles telling you to sell ten stocks now? ?(Yes, I know there are some, but they are not so common.) ?Or, where are follow up pieces indicating how well prior picks have done, and whether one should sell, hold, or buy more now?

My main point is this: good amateur investing is like having a part-time job. ?A part-time job, well, takes time. ?Weigh that against other priorities in your life — family, friends, church, public service, fun, etc. ?You may not want a part-time job, and so you can index your investments, or outsource them to a trusted advisor, who hopefully digs up his own ideas, and does not have a consensus, index-like portfolio (If he does, why not index?)

So, avoid tips if you can. ?If you can’t, develop a research discipline, or set them aside like I do, and revisit them when the original reason for buying it is forgotten, and you must evaluate for yourself now. ?The investment that you do not understand why you bought it, you will never know when it is the right time to sell it.

Either learn to evaluate investments on your own, or index your investments, or find a good investment advisor. ?But don’t think that you will do well off of tips.

1) I’ve been a bull on the long end of the Treasury curve for a while. ?It’s been a winning bet, and the drumbeat of “interest rates have nowhere to go but up” continues. ?Here’s an argument from Jeffrey Gundlach on why long rates should remain low, and maybe go lower:

Gundlach, however, was one of the very few people?who believed rates would stay low, especially with the Federal Reserve committed to keeping rates low with its loose monetary policy.

It’s important to note that U.S. Treasuries don’t have the lowest yields in the world. French and?German government bonds have yields?that are about 100 basis points lower than those of Treasuries. In other words, those European bonds actually make U.S. bonds look cheap, meaning that yields have room to go lower.

This will trend toward lower rates will eventually have to end, but neither GDP growth, inflation, or business lending justifies it at present.

2) From Josh Brown, he notes that correlations went up considerably with all risk assets in the last bitty panic. ?Worth a read. ?My two cents on the matter comes from my recent article, On the Recent Anxiety in High Yield Bonds, where I noted how much yieldy stocks got hit — much more than expected. ?I suspect that some asset allocators with short-dated or small stop-loss trading rules began selling into the bitty panic, but that is just a guess.

Isn’t it a bit odd to say lots of people sold quickly *and* that there isn’t enough liquidity??

Liquidity means a number of things. ?In this situation, spreads widened enough that parties that wanted to sell had to give up price to do so, allowing the brokers more room to sell them to skittish buyers willing to commit funds. ?Sellers were able to get trades done at unfavorable levels, but they were determined to get the trades done, and so they were done, and a lot of them. ?Buyers probably had some spread target that they could easily achieve during the bitty panic, and so were willing to take on the bonds. ?Having a balance sheet with slack is a great thing when others need liquidity now.

One other thing to note from the article is that it mentioned that retail investors now own 37%?of credit, versus?29% in 2007, according to RBS. Also that?investment funds has been able to buy?all?of the new corporate debt sold since 2008.

There’s more good stuff in the article including how “matrix pricing” may have influenced the selloff. ?When spreads were so tight, it may not have taken a very large initial sale to make the estimated prices of other bonds trade down, particularly if the sales were of lower-rated, less-traded bonds. ?Again, worth a read.

Fair Isaac?Corp.?said Thursday that it will stop including in its FICO credit-score calculations any record of a consumer failing to pay a bill if the bill has been paid or settled with a collection agency. The San Jose, Calif., company also will give less weight to unpaid medical bills that are with a collection agency.

I think there is less here than meets the eye. ?This only affects those borrowing from lenders using the particular FICO scores that were modified. ?Not all lenders use that particular score, and many use FICO data disaggregated to create their own score, or ask FICO to give them a custom score that they use. ?Again, from the WSJ article:

Fair Isaac releases new scoring models every few years, and it is up to lenders to choose which ones to use. The new score will likely be adopted by credit-card and auto lenders first, says John Ulzheimer, president of consumer education at CreditSesame.com and a former Fair Isaac manager.

Mortgages are likely to lag, since the FICO scores used by most mortgage lenders are two versions old.

The?impact of the changes on borrowers is likely to be significant. Accounts that are sent to collections, including credit-card debts and utility bills, can stay on borrowers’ credit reports for as long as seven years, even when their balance drops to zero, and can lower their scores by up to 100 points, said Mr. Ulzheimer.

The lower weight given to unpaid medical debt could increase some affected borrowers’ FICO scores by 25 points, said Mr. Sprauve.

But lowering the FICO score by itself doesn’t do anything. ?Some lenders don’t adjust their hurdles to reflect the scores, if they think the score is a better measure of credit for their time-horizon, and they want more loan volume. ?Others adjust their hurdles up, because they want only a certain volume of loans to be made, and they want better quality loans at existing pricing.

Megan McArdle at Bloomberg View asks a different question as to whether it is good to extend more credit to marginal borrowers? ?Didn’t things go wrong doing that before? ?Her conclusion:

That in itself [DM: pushing for more loans to marginal borrowers as a matter of policy] is an interesting development. Ten years ago, politicians were pressing hard for banks to extend the precious boon of homeownership to every man, woman and shell corporation in America. Five years ago, when people were pushing for something like the CFPB, the focus of the public debate had dramatically shifted toward protecting people from credit. Oh, there were complaints about the cost of subprime loans, but ultimately, on most of those loans, the problem?wasn?t the interest rate but the principal: Too many people had taken out loans that they could not realistically afford to pay, especially if anything at all went wrong in their lives, from a job loss to a divorce to an unexpected illness. And so you heard a lot of complaints about predatory lenders who gave people more credit than they could handle.

Credit has tightened considerably since then, and now, it appears, we?re unhappy with that. We want cheaper, easier credit for everyone, and particularly for the kind of financially struggling people who have seen their credit scores pummeled over the last decade. And so we see the CFPB pressing FICO to go easier on people with satisfied collections.

That?s not to say that the CFPB is wrong; I don?t know what the ideal amount of credit is in a society, or whether we are undershooting the mark. What I do think is that the U.S. political system — and, for that matter, the U.S. financial system — seems to have a pretty heavy bias toward credit expansion. Which explains a lot about the last 10 years.

Personally, I look at this, and I think we don’t learn. ?Credit pulls demand into the present, which is fine if it doesn’t push losses and heartache into the future. ?We are better off with a slower, less indebted economy for a time, and in the end, the economy as a whole will be better off, with people saving to buy in the future, rather than running the risk of defaults, and a very punk economy while we work through the financial losses.

There are several reasons to avoid illiquidity in investing, and some reasons to embrace it. ? Let me go through both:

Embrace Illiquidity

You are offered a lot of extra yield for taking on a bond that you can’t easily sell, and where you are convinced that the creditor is impeccable, and there are no sneaky options that you have implicitly sold embedded in the bond to take value away from you.

An unusual opportunity arises to invest in a private company that looks a lot better than equivalent public companies and is trading at a bargain valuation with a sound management team.

You want income that will last for your lifetime, and so you take some of the money you would otherwise allocate to bonds, and buy a life annuity, giving you some protection against longevity. ?(Warning: inflation and credit risks.)

In the past, you bought a Variable Annuity with some good-looking?guarantees. ?The company approaches you to buy out your annuity at a 10-20% premium, or a 20-30% premium if you roll the money into a new variable annuity with guarantees that don’t seem to offer much. ?Either way, turn the insurance company down, and hold onto the existing variable annuity.

In all of these situations, you have to treat the money as money lost to present uses. ?If there is any significant probability that you might need the money over the term of the asset, don’t buy the illiquid asset.

Avoid Illiquidity

Often the premium yield on an illiquid bond is too low, or the provisions take value away with some level of probability that is easy to underestimate. ?Wall Street does this with structured notes.

Why am I the lucky one? ?If you are invited to invest in a private company, be skeptical. ?Do extra due diligence, because unless you bring something more than money to the table (skills, contacts), the odds increase that they are after you for your money.

Then again, those that owned that broker-dealer put all their assets on the line, and ended up losing it all. ?They weren’t young guys with a lot of time to bounce back from the loss. ?They saw the opportunity of a lifetime, and rolled the bones. ?They lost.

We tend to underestimate how much we might need liquidity in the future. ?In the mid-2000s people encumbered?their future liquidity by buying houses at inflated prices, and using a lot of debt. ?When everything has to go right, the odds rise that everything will not go right.

And yet, there are?two more?more reason to avoid illiquidity — commissions, and inability to know what is going on.

Commissions

Illiquid assets offer the purveyor of the assets the ability to pay a significant commission to their salesmen in order to move the product. ? And by “illiquid” here, I include all financial instruments that carry a surrender charge. ?Do you want to know how much the agent made selling you an insurance product? ?On single-premium products, it is usually very close to the difference between the premium you paid, and the cash surrender value the next day.

Financial companies build their margins into their products, and shave off a portion of them to pay salesmen. ?This not only applies to insurance products, but also mutual funds with loads, private REITs, etc. ?There are many?brokers masquerading as financial advisers, who do not have to?act strictly in the best interests of the client. ?The ability to receive a commission makes them less than neutral in advising, because they can make a lot of money selling commissioned products. ?In general, it is good to avoid buying from commissioned salesmen. ?Rather, do the research, and if you need such a product, try to buy it directly.

Not Knowing What Is Going On

There are some that try to turn a bug into a feature — in this case, some argue that the illiquid asset has no volatility, while its liquid equivalents are more volatile. ?Private REITs are an example here: the asset gets reported at the same price period after period, giving an illusion of stability. ?Public REITs bounce around, but they can be tapped for liquidity easily… brokerage commissions are low. ?Some private REITs take losses and they come as a negative surprise as you find ?large part of your capital missing, and your income reduced.

What I Prefer

In general, I favor liquid investments unless there is a compelling reason to go illiquid. ?I have two private equity investments, both of which are doing very well, but most of my net worth is tied up in my equity investing, which has done well. ?I like the ability to make changes as time goes along; there is value to being able to look forward, and adjust.

No one knows the future, but having some slack capital available to invest, like Buffett with his “elephant gun,” allows for intelligent investing when liquidity is scarce, and yet you have some. ?Many wealthy people run a liquidity “barbell.” ?They have a concentrated interest in one company, and balance that out by holding very safe cash equivalents.

So, in closing, avoid illiquidity, unless you don’t need the money, and the reward is very, very high for making that fixed commitment.

I got cold-called this last week while I was away on business. ?I googled the phone number, and found that it came from Melitello Capital. ?I went through their site, and read most of their articles.

It’s an interesting firm, though I have no interest in working with them. ?The article I would like to comment on tonight is “HOW DOES AN RIA JUSTIFY ITS 1% FEE?”

I will explain why a 1% fee?can be justified. ?Now, I am an old school RIA [Registered Investment Adviser]. ?I only manage assets. ?I don’t allocate across asset classes. ?I don’t manage taxes in entire (though I help). ?I don’t structure the means to escape estate taxes. I don’t set up insurance schemes to minimize taxes; I could do it, but it would be boring. ?I could make a lot more money than I do, but I make enough, and I really like the challenge of outperforming the market.

RIAs offer value to clients in a large number of ways:

Reducing income taxes

Holding the hands of clients during the manic and panic periods of the market. ?Discourage them from taking more risk when the market is hot, and encourage them to take more risk, or at least, don’t leave when the market is panicking.

Hedging risks, whether it is a collar on a large single stock position, or a macro hedge.

Aiding in covering insurance needs.

Setting up financial plans.

Structuring estates, such that everything goes where the client wants, and estate taxes are minimized.

Asset allocation, including regular rebalancing.

And more… free advice on other issues, entertainment, bragging rights, etc.

Look, it’s easy to trash talk your competition. ?Some registered investment advisers are worth their ~1% fee, and some not. ?It depends on the package of services that they deliver — alpha, taxes, insurance, legal help, asset allocation (tsst… be wary of the efficient frontier. ?It does not exist.).

In general, if the investment advisers themselves do not give in to panic and greed, they are worth a 1%/year fee. ?So seek out advisers that do not give in to market pressure.

Note: this is unpopular, because that means hanging onto advisers that underperform during hot markets. ?In the long run you will do better following advice like this– after all, they dissed Buffett in 1999, and my Mom told me I was a fuddy-duddy. ?(Note: when a parent tells you that you are behind the times, it stings. ?It does not mean that you are wrong.)

I am not telling you to invest with me; that is not what my blog is about. ?I am saying that there is value in separate accounts with RIAs. ?And, be choosy. ?Lower fees are better, subject to the same levels of competence.

This is a great book. ?I encourage ?you to buy it. ?Though it talks of “effortless savings,” sorry, you’re going to have to work to get those savings. ?Often the work won’t be much, but you have to focus your life to save, and that takes effort.

What area do I have the most expertise in? ?Insurance. ?When I read the book, I looked at the insurance area closely, and said to myself, “a very good chapter, except he excluded warranties.”

Then as I read on, he handled warranties later, in discussions on electronics, where warranties are presently hot.

This is one of those books, that as you read it, you should make a list. ?Prioritize the areas where you are overspending, and take action one-by-one, to reduce your spending in a wise way. ?If you did this over a whole year, you might be able to do this in such a way that you don’t notice any significant changes to your life.

Full disclosure: The author asked me if I would like a copy and I said yes.

If you enter Amazon through my site, and you buy anything, I get a small commission.? This is my main source of blog revenue.? I prefer this to a ?tip jar? because I want you to get something you want, rather than merely giving me a tip.? Book reviews take time, particularly with the reading, which most book reviewers don?t do in full, and I typically do. (When I don?t, I mention that I scanned the book.? Also, I never use the data that the PR flacks send out.)

Most people buying at Amazon do not enter via a referring website.? Thus Amazon builds an extra 1-3% into the prices to all buyers to compensate for the commissions given to the minority that come through referring sites.? Whether you buy at Amazon directly or enter via my site, your prices don?t change.

Every hundred or so posts, I take a step back, and try to think about broader issues about blogging about finance. ?Tonight, I want to explain to new readers what the Aleph Blog is about.

There have been many new followers added to my blog recently, ?through e-mail, RSS, and natively. ?This is because of this great article at Marketwatch, which builds off of this great article at Michael Kitces’ blog.

I am humbled to be included among Barry Ritholtz, Josh Brown, and Cullen Roche, and am genuinely surprised to be at number 4 among RIAs in social media influence. ?Soli Deo Gloria.

What Does the Aleph Blog Care About?

I’m writing this primarily for new readers, because I’ve written a lot, and over a lot of areas. ?I write about a broader range of topics than almost all finance bloggers do because:

I’m both a quantitative analyst and a qualitative analyst.

I’m an economist that is skeptical about the current received wisdom.

I like reading books, so I write a lot of book reviews.

I’m also a skeptic regarding Modern Portfolio Theory, and would like to see it discarded from the CFA and SOA syllabuses.

I believe in value investing, in both the quantitative and qualitative varieties.

I believe that risk control is a core concept for making money — you make more money by not losing it.

I believe that good government policy focuses on ethics, not results. ?The bailouts were not fair to average Americans. ?What would have been fair would have been to let the bank/financial holding companies fail, while protecting the interests of depositors. ?The taxpayers would have been spared, and there would have been no systematic crisis had that been done.

I care about people not getting cheated. ?That includes penny stocks, structured notes, private REITs, and many other financial innovations. ?No one on Wall Street wants to do you a favor, so do your own research and buy what you want to own, not what someone wants to sell you.

Again, I don’t want to see people cheated, so I write about ?insurance. ?As a former actuary, and insurance buy-side analyst, I know a lot about insurance. ?I don’t know this for sure, but I think this is the blog that writes the most about insurance on the web for free. ?I write as one that invests in insurance stocks, and generally, I buy the stocks because I like the management teams. ?Ethical, hard working insurance management teams do the best.

Oddly, this is regarded to be a good accounting blog, because as a user of accounting statements, I write about accounting issues.

I am a skeptic on monetary and fiscal policy, and believe both of them tend to sacrifice the future to benefit the present. ?Our grandchildren will hate us. ? That brings up another issue: I write about the effects of demographics on the markets. ?In a world where populations are shrinking in developed nations, and will be shrinking globally by 2040, there are significant economic impacts. ?Economies don’t do well when workers are shrinking in proportion to those who are not working. ?(Note: include stay-at-home moms and dads in those who work. ?They are valuable.)

I care about the bond market. ?There aren’t that many good bond market blogs. ?I won’t write about it every day, but I will write about i when it is important.

I care about pensions. ?Most of the financial media knows things are screwed up there, but they do not grasp how bad the eventual outcome will likely be. ?This is scary stuff — choose the state you live in with care.

My blog is not for everyone. ?I write about what I feel most strongly about each evening. ?Since I have a wide array of interests, that makes for uneven reading, because not everyone cares about all the things that I do. ?If that makes my readership smaller, so be it. ?My blog expresses my point of view; it is not meant to be the largest website on finance. ?I want to be special, even if that means small, expressing my point ?of view to those who will listen.

I thank all of my readers for reading me. ?I appreciate all of you, and thank you for taking the time to read me.

As one final comment, I need to say this. ?I note people unfollowing my blog at certain times, and I say to myself, “Oh, I haven’t been writing about his pet issue for a while.” ?Lo, and behold, after these people leave, I start writing about it again. ?That is not intentional, but it is very similar to how the market works. ? People buy and sell investments at the wrong times.

To all my readers, thank you for reading me. ?I value all of you, and though I can’t answer all e-mails, I read all e-mails.

In summary: the Aleph Blog is about ethics and competence. ?I want to do what is right, and do what gives the best investment performance, in that order.

Giving Yourself an Investing Makeover?http://t.co/u1MmwlWiKP?@jasonzweigwsj describes Guy Spier & his efforts 2b a more rational investor $$?May 24, 2014

The Bearish Signs Junk Buyers Reject in Stoking ?14 Rally?http://t.co/xsYEJeKTnU?BBs beat CCCs amid a falling Russell 2000 index $$ #odd?May 23, 2014

Penny Stocks Like Latteno Foods Rally, Fueling Big-Dollar Dreams?http://t.co/IiqCWeAyOW?Fascinating 2c this amid a pullback in small caps $$?May 23, 2014

Buffett Too Rich for Buffett Is Sign Bargains Are Gone?http://t.co/cbjQ0MDmSR?I’m still finding some cheap stocks but they r unusual $$ $SPY?May 23, 2014

For Sale: 20% Stake in Hedge Fund. Terms: Complicated.?http://t.co/kDoik1H4LT??You don?t want to be wearing someone else?s underwear.? $$?May 23, 2014

Boomers Cash In as Bull Market Aids Exodus From Workforce?http://t.co/uKRIfO4qMQ?Asset illusions delude Boomers who think they r rich $$?May 23, 2014

Wall Street Finds New Subprime With 125% Business Loans?http://t.co/USvBIvP5Vj?The businesses would get better rates on Prosper $$ #dumb?May 23, 2014

Debt Rises in Leveraged Buyouts Despite Warnings?http://t.co/6T8TIpdxWc?Debt makes financial systems less flexible; depend on fixed pmts $$?May 21, 2014

Chasing Yield, Investors Plow Into Junk Bonds?http://t.co/lWFufDu7Hy?Yields have never been lower 4 CCC-rated debts $$?May 21, 2014

?

Rest of the World

What China Property Crash? Economists See Growth Bump?http://t.co/kcXGitJH1l?Economists c new empty buildings & mark up GDP $$ $FXI #FTL?May 23, 2014

Putin?s Singapore Dream Costs Crimea Banks and Burgers?http://t.co/OmmtpYDB7G?Singapore is not so much created by laws but by ppl culture $$?May 23, 2014

Russia, China Sign $400B Gas Deal After Decade of Talks?http://t.co/4k8PSE5NrM?The infrastructure must b created 2 make this work; not ez $$?May 23, 2014

Brazil World Cup Win Risks Stock Drop in Boon to Rousseff?http://t.co/dPb8GVbtSZ?Brazil wins, Rousseff win odds rise, stocks will fall $$?May 23, 2014

BlackRock Has Cut Portugal Bond Holdings Over Past Couple of Weeks?http://t.co/U3CuYpUu81?Some Emerging-Market Debt > Euro-Zone Bonds $$?May 23, 2014

Norway Loses Reputation as Stable Investment as Firms Recoil?http://t.co/fqQkiM2H3k?Tax 2 highly & businesses run away $$?May 21, 2014

It’s a Good Time to Globalize Your Stock Portfolio?http://t.co/8pqTAwFbqj?Many foreign companies r trade cheaper than US stocks $$ $SPY $EFA?May 21, 2014

UK House Prices Rise to Record High in April?http://t.co/vo6gYZNlAQ?B sure 2add wealthy foreigners buying in London as investment/hedge $$?May 19, 2014

Bank of England’s Mark Carney Highlights Housing Market’s Threat to UK Economy?http://t.co/5XOwH0cIsJ?100% of all UK mtges r short-dated $$?May 19, 2014

Good Time To Be A Farmer In China??http://t.co/04V9YEmSQm?China aggressively pushing crop insurance, & larger scale agriculture $$ $FXI $SPY?May 19, 2014

Energy

Without Keystone XL?http://t.co/qpDcgET7J3?Economic & public health costs of forgoing a new oil pipeline $$ {Sound of oil train derailing}?May 24, 2014

Secrecy of Oil-by-Train Shipments Causes Concern Across the US?http://t.co/knapJHOx1k?Butane, propane & ethane should be removed b4 shpng $$?May 23, 2014

Oil Nations Put Out Welcome Mat for Western Companies?http://t.co/cvarvyMDCt?If u make the cost of drilling2high, fewer bbls get produced $$?May 19, 2014

US Politics & Policy

How Timothy Geithner failed his stress test?http://t.co/qSu9V6oZvX?When @rortybomb & I agree on something, that is notable $$ #housingbubble?May 23, 2014

Meet Jessica Rosenworcel, the FCC Swing Vote?http://t.co/VtIzieSnqI?Marches to her own drummer, willing to cut deals 4 the greater good $$?May 23, 2014

How to Turn Homes Back Into Piggy Banks?http://t.co/fB9PTlBwxZ?Housing Personal Savings Acct & Equity Principal Tax Credit; elim mtge ded $$?May 23, 2014

NJ Gov. Christie under fire for cutting pension payments to state workers?http://t.co/rGwAKla3aT?Definite mistake; cashflows compound $$?May 23, 2014

BlackRock?s Fink Says Housing Structure More Unsound Now?http://t.co/xeMYQmjYGG?GSEs took too much default risk pre-crisis, returning $$?May 21, 2014

GOP’s Business Wing Sends Tea Party a Chilling Message?http://t.co/W5QCHBrJrW?Business fights small government GOP candidates $$?May 19, 2014

Why Republicans Should Take Rick Santorum Seriously?http://t.co/wN7tUmnhbV?Represents the middle class populist part of the GOP $$?May 19, 2014

California’s Drinking Problem?http://t.co/GZnmdInHGY?California does not have enough water for Ag, Industry, People, w/o right incentives $$?May 19, 2014

US Monetary Policy

New Faces Behind Fed Dots Seen Roiling Markets as Forecasts Move?http://t.co/M2AcqPEQTX?Y publish estimates if u don’t want us 2read them $$?May 23, 2014

Bubble States Underemployment Rates Haunt Yellen?http://t.co/fRzLYozafe?Monetary policy is impotent w/debt defation; Fed on wrong track $$?May 23, 2014

New Faces Behind Fed Dots Seen Roiling Markets as Forecasts Move?http://t.co/M2AcqPEQTX?Y publish estimates if u don’t want us 2read them $$?May 23, 2014

Yellen Adds Disadvantaged to Full-Employment Definition?http://t.co/10PSrxYI9c?Alas, monetary policy is weak when dealing e/employment $$?May 21, 2014

Fed’s Rate-Change System Up for Revamp?http://t.co/srqZoDDMhK?The Fed is lost. The Fed is lost. The Fed is lost. The Fed is lost… $$ $TLT?May 19, 2014

?

Companies & Industries

Google Developing Tablet With Advanced Vision Capabilities?http://t.co/ABO9NObY1h?Will b interesting 2c what new apps get developed $$ $GOOG?May 23, 2014

Planting Corn at Warp Speed Using High-Tech Tools?http://t.co/tDF9EaJoy6?Astounding application of technology transforms planting seed $$?May 23, 2014

Golf Market Stuck in Bunker as Thousands Leave the Sport?http://t.co/ju7aFEx2lp?Costs 2 much $$ takes up 2 much time, but growing in Asia?May 23, 2014

Family Dining Offers Barometer of Middle Income?http://t.co/5IzzOFfS3j?Ugly valuations means stocks will fall if sales don’t rise 4%/yr+ $$?May 23, 2014

Silicon Valley’s Laundry-App Race?http://t.co/GyvIWxd5ux?Long article on the efforts to turn laundry into a scalable attractive business $$?May 23, 2014

Personal Finance

Dueling Strategies for 401(k)s, IRAs and Your Other Retirement Funds?http://t.co/DGzSDVhDZ6?Do what maxes long-term purchasing power $$ $SPY?May 23, 2014

40 Financial Things You Should Know by 40?http://t.co/8qqFlp1TUB?2013 article, but I thought it covered the personal financial basics $$?May 19, 2014

Other

New Study: Is No Degree Better Than A Liberal Arts Degree??http://t.co/MOYUZTngoD?Depends. It helps in getting some jobs, but not all $$?May 21, 2014

BBC News – ‘Biggest dinosaur ever’ discovered?http://t.co/Yg2qTuS27T?Interesting b/c it probably was once much warmer in Patagonia $$?May 19, 2014

Haverford Speaker Bowen Criticizes Students Over Protests?http://t.co/QXkWoAh0iE?Former Princeton President calls them “immature.” Bingo! $$?May 19, 2014

?

Wrong

Overrated: Russia, China sign deal to bypass USD?http://t.co/YNgu6bwK7H?What matters is where u invest the proceeds from goods exported $$?May 23, 2014

Wrong: Investing: The herd isn’t always dumb?http://t.co/dt0xuXKNCJ?Then explain y dollar-weighted returns underperform buy & hold $$ #panic?May 23, 2014

Wrong: Cutting Off Emergency Unemployment Benefits Hasn?t Pushed People Back to Work?http://t.co/3GwlHcvq70?We run unsustainable deficits $$?May 23, 2014

Wrong: Ikea Economics Lure Central Bankers Seeking New Tools?http://t.co/peVUXrPpKs?Don’t try negative interest rates; will b a disaster $$?May 23, 2014

Wrong: The Retirement Apocalypse That Isn’t Coming?http://t.co/ILYSCOzKTm?I might buy this if we weren’t running large deficits $$ $TLT $SPY?May 21, 2014

?

Retweets, Replies & Comments

‘ @DGenchev I am analyzing the investors as a group, thus what % of the mkt cap is relevant. I go to EDGAR and copy XML files into Excel?May 24, 2014

If I were doing your project, I would not have chosen any of your “governance experts.” I would have chosen a group?http://t.co/XWlYm8HaVD?May 22, 2014